")

Back to Journals » Psychology Research and Behavior Management » Volume 15

Role of Environmental Sustainability, Psychological and Managerial Supports for Determining Bankers’ Green Banking Usage Behavior: An Integrated Framework

Authors Hasan MM , Al Amin M , Moon ZK, Afrin F

Received 17 June 2022

Accepted for publication 29 November 2022

Published 20 December 2022 Volume 2022:15 Pages 3751—3773

DOI https://doi.org/10.2147/PRBM.S377682

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Professor Mei-Chun Cheung

Md Mahedi Hasan,1 Md Al Amin,2,3 Zarin Khan Moon,4 Farhana Afrin2

1Faculty of Business Studies, Jashore University Science and Technology, Jashore, 7408, Bangladesh; 2Department of Marketing, Bangabandhu Sheikh Mujibur Rahman Science & Technology University, Gopalganj, Bangladesh; 3School of Business and Management, Queen Mary University of London, England, UK; 4Department of Accounting and Information Systems, Jashore University Science and Technology, Jashore, 7408, Bangladesh

Correspondence: Md Al Amin, Department of Marketing, Bangabandhu Sheikh Mujibur Rahman Science & Technology University, Gopalganj, 8100, Bangladesh, Email [email protected]

Purpose: Green banking, an ethical banking concept, concentrates on environmental protection and encourages social and environmental sustainability, perceived cognitive efforts, and subjective norms ensuring ecologically responsive banking services. Consequently, although there have been considerable green banking attempts in Bangladesh, it is yet unknown how environmental sustainability, perceived cognitive effort, and subjective norms affect usage behavior. The present research aims to uncover this gap, extending the Theory of Reasoned Action (TRA) to examine the determinants of the bankers’ green banking usage behavior during COVID-19.

Methods: Data were collected from 366 bankers in Bangladesh using a purposive sampling technique and analyzed with structural equation modeling (SEM) using SMART PLS 3 software.

Findings: The study found management support (0.291, t-statistics = 1.978, p 0.000), environmental sustainability (β = 0.278, t-statistics = 2.752, p < 0.001), perceived cognitive efforts (β = 0.401, t-statistics = 3.549, p < 0.000), and subjective norms (β = 0.309, t-statistics = 4.352, p < 0.000) influence bankers’ attitudes. Whereas environmental sustainability (β = 0.503, t-statistics = 3.726, p < 0.001), perceived cognitive efforts (β = 0.103, t-statistics = 2.020, p < 0.002), subjective norms (β = 0.281, t-statistics = 4.607, p < 0.000), and attitudes (= 0.602, t-statistics = 5.523, p 0.015) influence bankers’ green banking usage behavior. Finally, the mediating role of management supports, environmental sustainability, cognitive efforts and subjective norms on green banking usage behavior through attitudes was significant.

Contribution/Conclusion: The study contributed to existing literature validating the proposed holistic framework applying TRA and three contemporary dimensions explaining bankers’ behavior toward green banking practice. Finally, the implementers should focus on green banking practices as green banking is one of the key strategies to protect the environment, assure social justice, and create economic success.

Keywords: environmental sustainability, management supports, perceived cognitive efforts, green finance, sustainable banking

Introduction

The bankers’ concerns toward traditional banking activities have been interrogated over the last few decades due to several reasons. First, conventional banking ideologies are seldom seen in initiatives concerned with environmental protection. As a result, the potholed mechanization has disturbed the ecological balance, leading to natural and industrial disasters1 and raising social and ethical apprehensions over ecological issues.2 Second, during the COVID-19 pandemic, bank customers have expressed interest in green banking, a type of banking that considers environmental issues in its operations to mitigate the adverse effects of ecological imbalance and instigate environmental sustainability, which the customers might consider as a way to lessen the threats of COVID-19 transmission.3 Third, the traditional bankers’ cognitive efforts (eg, judgment, memory, and perception required for task completion) are being questioned due to the evolving provision of environmentally friendly products4–6 and how to extend the financial resources to save the environment, clean energy, green building, climate change, and social inclusion.3,7,8 Finally, the top management is becoming aware of their business sustainability and provides support in the form of managerial guidance in planning, design, development, and implementation activities to sustain banking activities that follow the sustainability laws.9,10 Subsequently, the top management enthusiastically accepts environmental commitment as a paramount business responsibility3,11 in banking, manufacturing, technology, electronics, and IT industries.1,12

To this end, a pivotal role in the sustainable development of a country is played by green banking, which refers to the investment solutions that protect the environment, guarantee social justice, and create economic success bringing precedence in the banking industry to shield banks and society against unexpected future economic issues,13,14 such as global financial instability, climate change, social unrest, and corporate scandals. Accordingly, the necessity of bankers’ green initiatives knows no bounds, and green banking practices are implemented globally.15 For example, The Rainforest Action Network (RAN) (2020) has recently reported that 35 leading investment banks started pouring $2.7 trillion into the fossil fuel industry from 2016 to 2019, despite the presence of an agreement within the United Nations Framework Convention on Climate Change, known as the Paris Agreement, which came into force in 2016. Since 2016, bank funding for the fossil fuel industry has increased yearly; by 2030, it is expected to reach $1 trillion yearly (RAN, 2020). The World Bank also announced its intentions to cease to support corporations and nations that place less emphasis on protecting the environment (Zhang et al,16 2019). Hence, the study aims at determining the dominant factors influencing bankers toward green banking practice.

The existing literature primarily concentrated on bank environmental performance, team effectiveness, corporate technological innovation, bankers’ sustainability performance, and green development.3,4,7,12,13,17–19 These existing studies also focused on Green Bank Loyalty based on Socially Responsible Investment (SRI) and Social Identity Theory (SIT);11,20 intention to practice green banking based on the theory of planned behavior (TPB) and SIT10,21,22 green banking sustainability based on Sustainable Business model and TPB;22–25 Perceived cognitive effort in using information system based applications;5 top management supports and commitment in green banking usage;10 management supports in artificial intelligence.26,27 Moreover, the researchers from developed countries, such as Greece28 and France,29 as well as developing countries, such as Bangladesh,30 India31 and Indonesia,29 have interested to explore the consequences of green banking practices.32 A study by Julia and Kassim33 investigated the green banking performance of Islamic banks versus conventional banks in Bangladesh based on the Maqasid Shariah framework. Sharma and Choubey15 discussed green banking initiatives in the Indian banking sector. Moreoverr, Shamshad et al34 also showed the sustainable growth of the Indian banking sector. Khairunnessa et al25 also reviewed the development of green banking in Bangladesh. Similarly, the Bangladesh government has also adopted substantial steps to address the issue, changing legislation, developing regulations and guidelines on green financing, and requiring all financial institutions to follow green financing practices.30

Despite the growing necessity of green banking or financing, the existing studies did not focus on the perceived cognitive effort (PCE), environmental sustainability, and management support for Green banking usage behavior (GBUB) in the context of Bangladesh. Consequently, it is imperative to examine how PCE, sustainability perception (SP), and management support (MS) impact GBUB in the context of Bangladesh. Hence, the study aims to empirically validate a unique model incorporating perceived cognitive effort, sustainability perception, and management supports into the Theory of Reasoned Action,35 filling these gaps in green banking usage behavior. More significantly, the present study has the following research objectives (ROs):

RO1: To examine the influence of perceived cognitive effort, sustainability perception, and management support on attitudes and green banking usage behaviour in Bangladesh during the COVID-19 pandemic.

RO2: To scrutinise the impacts of subjective norms on bankers’ attitudes and green banking usage behaviour in Bangladesh during the COVID-19 pandemic.

RO3: To test indirect influences of subjective norms, perceived cognitive effort, environmental sustainability, and management support on green banking usage behaviour through bankers’ attitudes in Bangladesh during the COVID-19 pandemic.

Correspondingly, this study contributes to the green finance literature in three ways. First, it applies and extends based on the theory of reasoned action (TRA), developed by Fishbein36 and tested by Ajzen and Fishbein,37 which can be utilised to understand individuals’ complex decision-making processes and to determine bankers’ attitudes toward green banking and GBUB by integrating three new dimensions, eg, perceived cognitive efforts, management supports, and environmental supports to predict bakers’ green finance continuance behaviour. Second, this study examines attitudes’ impact as a critical mediating variable to confirm green bank usage behaviour. Third, this study offers an understanding from the perspective of an emerging economy (ie, Bangladesh), which has been, so far, less represented in the mainstream literature (Sainaghi,38 2020).

We will go over the literature review first, then the conceptual framework and hypothesis development in the following parts. The research technique will be discussed next, followed by the results and discussion. Following that, we will look at the theoretical and managerial implications. Finally, we will discuss the study’s shortcomings and the potential for future research.

Literature Review

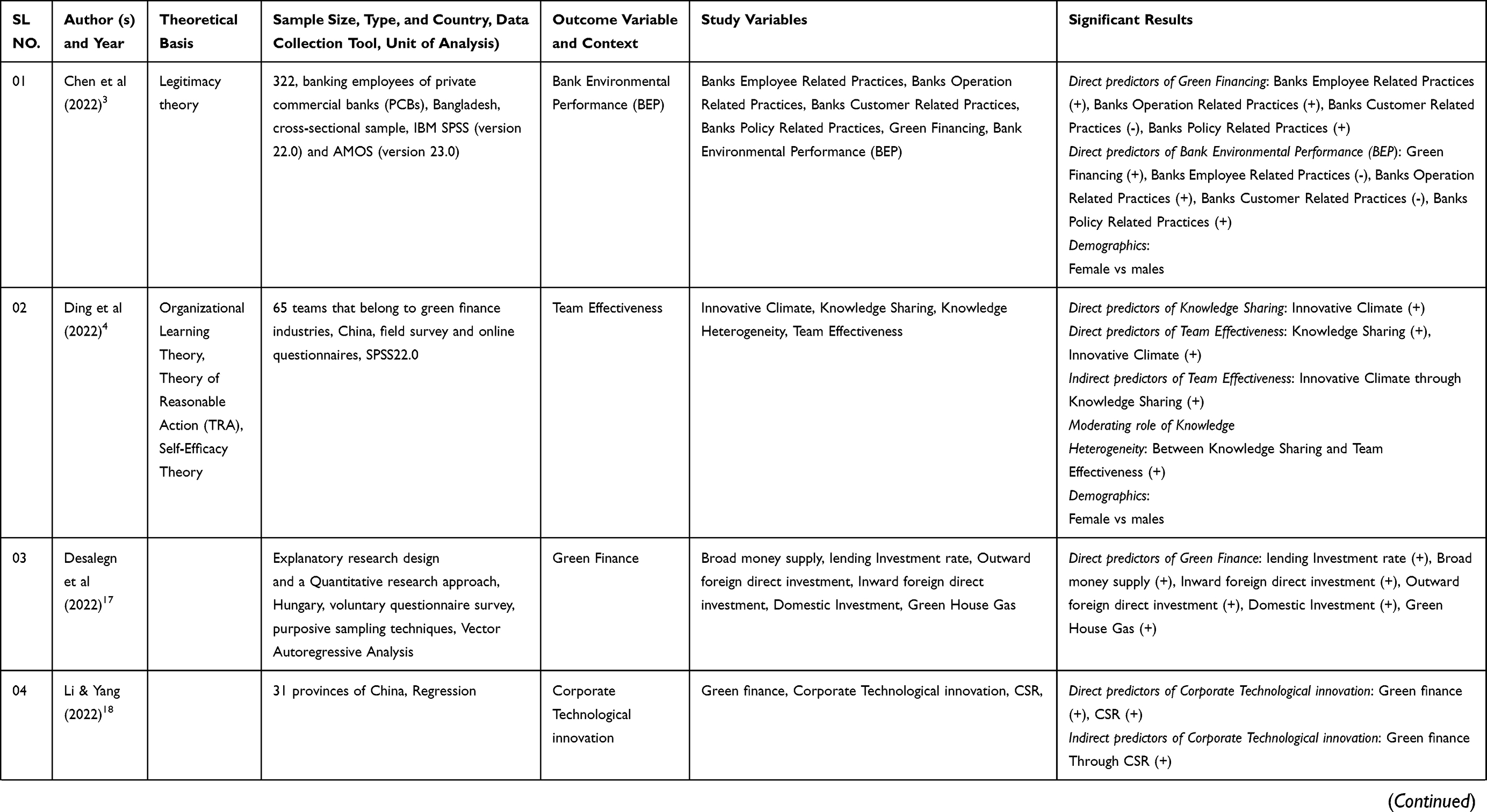

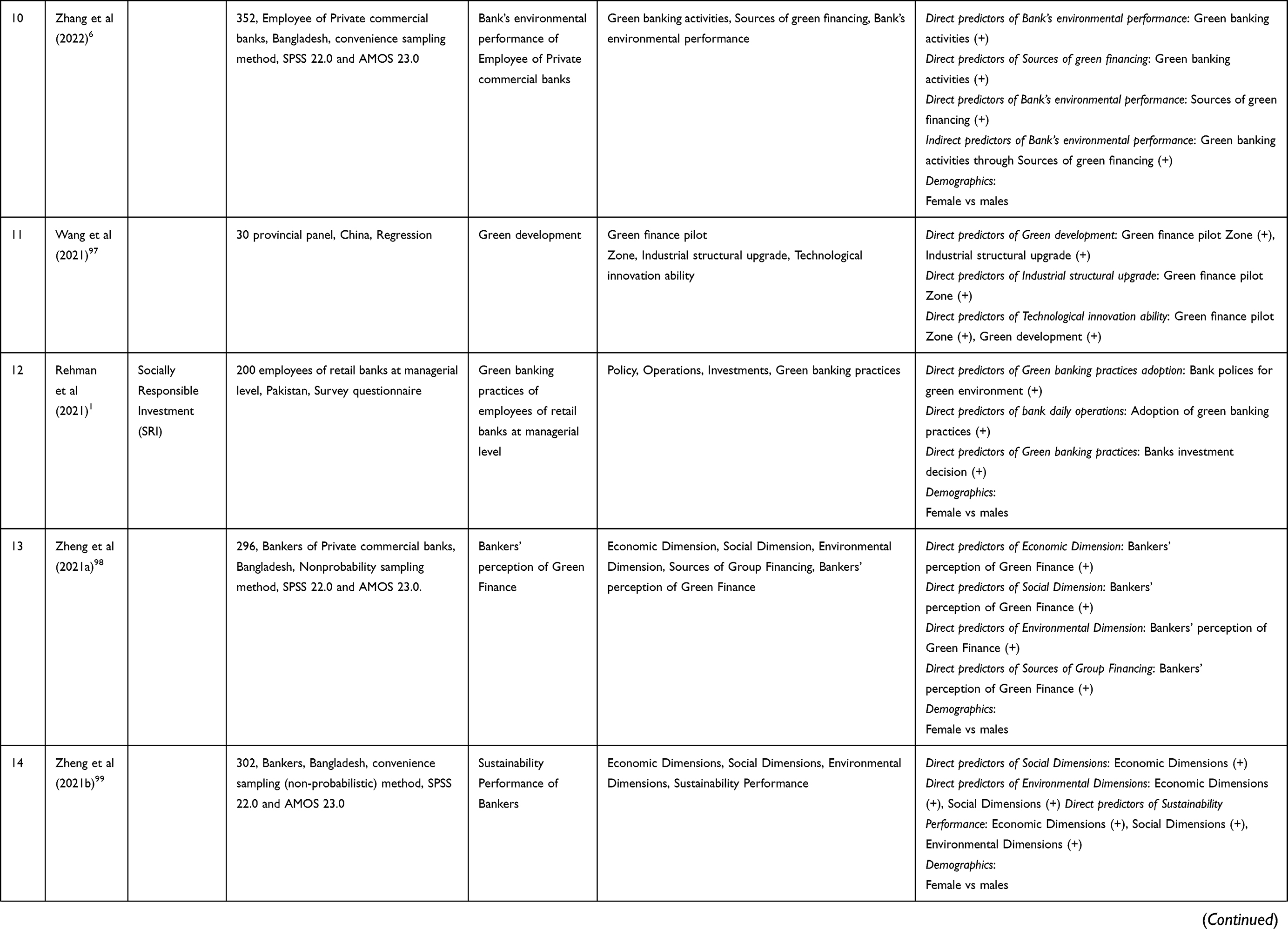

Green banking is defined as “banking in all its business components” (deposit-taking, credit disbursement, trade finance, leasing operations, mutual funds, and custodian services, among others) that is focused on environmental preservation39 and also known as ethical banking, social banking, responsible banking,29 or sustainable banking.40 A green bank promotes and uses green technology in its internal and external operations to minimize carbon emissions and better manage the environment.23 Accordingly, the number of studies on green banking is also growing at a more increasing rate (see Table 1 for the summary of existing relevant green banking literature). The existing literatures primarily focused on bank environmental performance, team effectiveness green finance, corporate technological innovation, bankers sustainability performance, green development,3,4,7,12,13,17–19 green banking initiatives,15 adoption of green banking practices,1 green consumer loyalty,11 consumer guilt and green banking services,21 green banking practices on bank loyalty,20 green banking and Islam,41 sustainable banking,22,42,43 a review of recent developments of green banking in Bangladesh,25 a transition towards green banking,29 exploring sustainability and green banking disclosures,23,24 exploring green banking performance of Islamic banks vs conventional banks,33 underpinning the benefits of green banking,44 sustainable growth of Indian banking sector.34

|  |  |  |

Table 1 The Summary of Relevant Green Banking Literature |

Recently, a study by Sharma and Choubey15 found green product development, green CSR, green internal process, and green banking initiatives impact green brand trust and green brand image in the context of green banking initiatives. That is the qualitative study of the Indian banking sector. This study was conducted on 36 middle-to-senior-level bank employees in India. Besides, Rehman et al1 showed green banking practices to 200 employees of retail banks at the managerial level based on the Socially Responsible Investment (SRI) theory. The researcher also found policies, operations, and investments in the context of adopting green banking practices in Pakistan. In addition, Sun et al11 conducted research on 429 respondents over 18 years old with a bank account based on Social Identity Theory (SIT) in the context of CSR, co-creation, and green consumer loyalty, where green banking initiatives are important in Pakistan. CSR, co-creation, and green banking influenced green consumer loyalty in this study. Another study by Burhanudin et al21 used the Self-Regulation Theory (SRT) and the Theory of Planned Behavior (TPB) to find the intention to use green banking services, which is influenced by guilt, attitude towards green banking, perceived consumer effectiveness, and negative word-of-mouth. The study was conducted on 313 respondents of commercial banking customers in Indonesia in the context of consumer guilt and green banking services. Ibe-Enwo et al20 found bank loyalty influenced by green banking, green image, and bank trust based on the socially responsible investment (SRI) theory. In this research, 850 customers of the retail banking sector were the respondents in North Cyprus, Turkey, in the context of green banking practices on bank loyalty.

However, despite the significant potential, the existing literature has ignored the direct and indirect influences of subjective norms, perceived cognitive efforts, environmental sustainability, management support, attitudes toward green banking, and green banking usage behavior in the context of green banking in Bangladesh. Hence, it is worth studying how subjective norms, perceived cognitive efforts, environmental sustainability, and management support reshape bankers’ attitudes and green banking usage behavior.

Conceptual Framework and Hypothesis Development

Conceptual Framework

The existing studies emphasized customers’ green banking usage behavior based on different models, eg, socially responsible investment (SRI),1,20 social identity theory (SIT),11 self-regulation theory,21 theory of planned behavior,21,22 Theory of Self-congruity,41 sustainable business model,25,43 theory of change,29 legitimacy theory,44 and the institutional theory.23 Moreover, the theory of reasoned action (TRA) is also a renowned model utilized by45–48 in determining the different forms of banking use behavior.

In this study, we have utilized TRA, developed by Fishbein in 1967 and tested by Ajzen and Fishbein37 to understand individuals’ complex decision-making processes and to determine bankers’ attitudes toward green banking and GBUB. According to the theory, decision-making begins with beliefs, attitudes toward the behavior, and intention, ending with the behavior itself. Many researchers have used TRA45–48 in the context of the usage of Islamic rural bank services, the religious leaders’ intention to use Islamic bank services in Indonesia, the public’s intention to adopt Islamic bank services in Uganda, and the adoption of green information technology, respectively. For instance, Effendi et al45 used the TRA model and found sharia compliance, product knowledge of sharia, promotion, services, attitudes, subjective norms, intention, and customer decisions to use the Islamic rural banks’ services, particularly in Indonesia. Besides, Janah et al46 also used the TRA. They incorporated the influence of attitude, community influence, religious obligation, and subjective norms to predict the intentions of religious leaders in using Islami bank services in Indonesia. Furthermore, Lujja et al47 used TRA as a theoretical framework to investigate the integration of attitude, subjective norm, and public intention in Uganda to adopt an Islamic bank. Moreover, using the TRA model, Mishra et al48 indicated that external factors such as person-related beliefs, sector of respondents’ establishment, and level of awareness significantly impact attitudes towards adopting green information technology in Turkey.

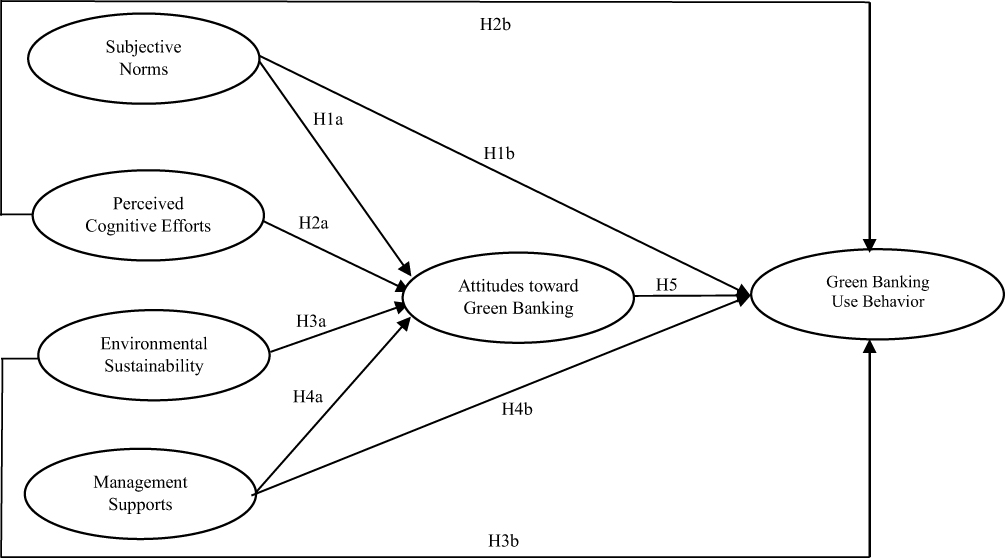

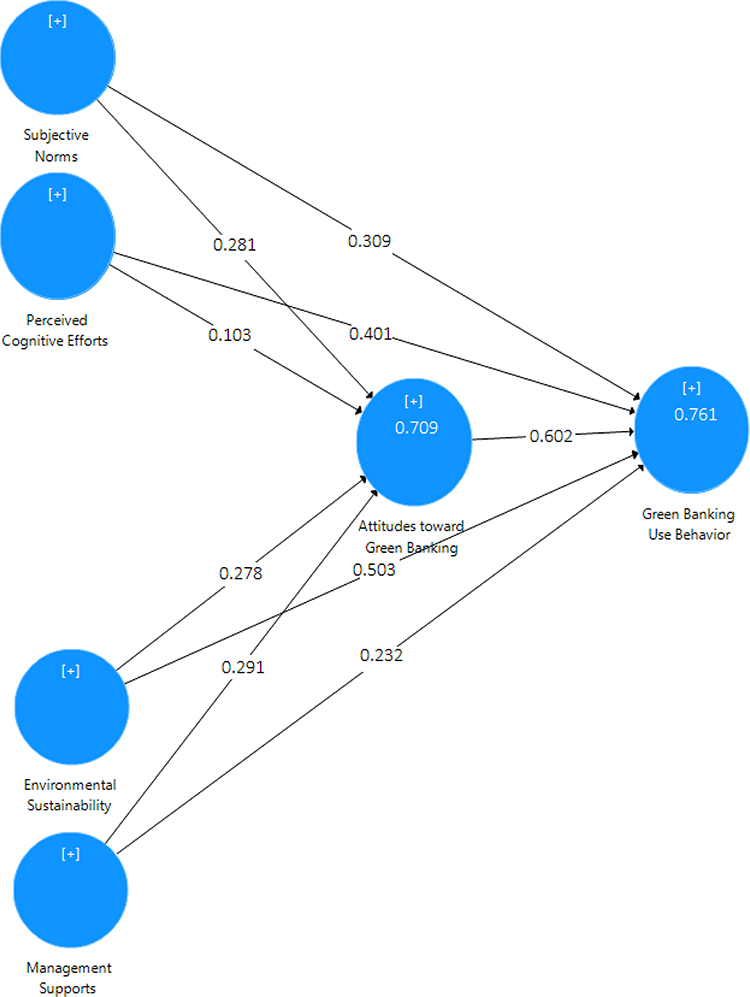

However, the existing studies ignored the role of the perception of cognitive efforts, environmental sustainability, and management support in developing a theoretical framework based on the TRA model in determining the banking or GBUB. Whereas Yang and Yoo5 stated perceived cognitive effort as an important factor that is used in previous studies49–51 as the independent variable to determine user behavior (eg, technology use, banking use, etc.) in the context of revisiting the technology acceptance model to determine the impact of internet agent on end users’ performance or to understand the effect of information overload on employees. Besides, environmental sustainability is also an important determinant. Obiora et al52 used ecological sustainability as the crucial determinant of banking and financial systems. Many understood the role of managerial support in determining attitudes toward knowledge sharing and artificial intelligence.25,26 Hence, the current study has developed and tested a holistic model that integrates perceived cognitive efforts, environmental sustainability, and management support into the TRA model in examining GBUB in a single framework. Figure 1 represents the structural relationship of the study.

|

Figure 1 The conceptual framework. |

Hypothesis Development

Subjective Norms, Attitudes, and Green Banking Usage Behavior

Subjective norms (SN) refer to the extent to which people feel encouraged to act in a specific way by others in their community who are significant to them (family, friends, and coworkers).53 Accordingly, the users of green banking often embrace the opinions, attitudes, and behavior of significant people in their community. For example, Taneja and Ali21 explored the influence of SN on banking customers’ attitudes toward sustainable banking. Other studies discovered direct and moderating effects of subjective norms on attitude54–58 in the context of buying organic food, cross-cultural investigation, quality of life and life satisfaction among university students, organic food, and airline B2C eCommerce websites, respectively. Thus, we posited the following hypothesis:

H1a: The subjective norms positively influence bankers’ attitudes toward green banking usage behavior.

In addition, behavior based on one’s willingness that affects the use of a particular behaviour is referred to as behavioral intention.59 For instance, Taneja & Ali22 explored the influence of SN on banking customers’ intention to use digital banking services. Moreover, the extent of literature found subjective norms influence use behavior60,61 in the context of low-carbon travel and perceived behavioral control on managers, respectively. Several other studies also found the role of subjective norms on behavioral intention62–64 in the context of antibiotic prophylaxis, bibliometric analysis, and environmental sustainability, respectively. Thus, the following hypothesis is posited in the context of green banking in Bangladesh.

H1b: The subjective norms positively influence bankers’ green banking usage behavior.

Perceived Cognitive Efforts, Attitudes, and Green Banking Usage Behavior

Perceived cognitive effort (PCE) can be defined as an antecedent consisting of cognitive resources (eg, judgment, memory, and perception required for task completion).51 Researchers have argued that effort minimization is important in selecting a decision strategy. According to the effort-accuracy framework of cognitive proposed by Payne, the primary objectives of a decision-maker are to maximize accuracy and minimize cognitive effort. Accordingly, it is assumed that bankers’ attitudes and behavior are predominantly influenced by how bankers use their cognitive resources. A series of studies investigated decision-makers’ strategy selection and choice behavior when assisted by decision support systems (DSS).65 Many studies find that cognitive effort influences attitudes.5 in the context of revisiting the technology acceptance model.

Moreover, cognitive efforts also influence green banking usage behavior (GBUB). According to Yang and Yoo5 the affective and cognitive dimensions are independent variables that affect behavioral intention. Thus, we argue that cognitive efforts significantly influence attitudes in explaining bankers’ attitudes and GBUB. Therefore, the current study developed the following hypotheses:

H2a: In the context of green banking, cognitive efforts positively influence bankers’ attitudes toward green banking usage behavior.

H2b: Perceived cognitive efforts positively influence bankers’ green banking usage behavior.

Sustainability, Attitudes, and Green Banking Usage Behavior

Sustainability refers to the approach that assists a business firm “to meet its current requirements without compromising its ability to meet future needs” (World Commission Report on Environment and Development 1987, p 41). Caniato et al and Peattie and Belz66,67 defined sustainability as having three dimensions: environmental, social, and economic. The environmental dimension included natural resource usage, carrying capacities, and ecosystem integrity. The social dimension included participation, empowerment, socioeconomic mobility, and cultural preservation. Home necessities, labor efficiency, and industrial and agricultural expansion were among the environmental variables.68 Chuang et al67 discovered the influence of sustainability on attitudes and intention to use69 in travellers’ choices for pro-environment behavioral intentions. The study argues that environmental sustainability significantly influences attitudes and GBUB. Thus, the following hypotheses are deposited:

H3a: Environmental sustainability positively influences bankers’ attitudes in the context of green banking.

H3b: Environmental sustainability positively influences bankers’ green banking usage behavior.

Management Supports, Attitudes, and Green Banking Usage Behavior

Management support can take the form of managerial guidance in planning, design, development, and implementation activities.9 Overall, higher management involvement is directly and positively linked to higher labor productivity, quality, and financial performance.70 Management might be able to engage the employees and support them to create an environment for determining their attitudes, motivation, and opinions.71 Accordingly, it is essential to comprehend the role of these management supports in explaining bankers’ attitudes and use behavior. For example, several studies analogized the role of management support on attitudes toward knowledge sharing and artificial intelligence.21,22 Burhanuddin et al and Taneja and Ali26,27 understood the necessity of management support in testing GBUB. Other studies have found the positive influence of management support on the use of behavior72,73 in the context of knowledge sharing, teacher behavior management, e-HRM, innovative work behavior, and promoting firms’ energy-saving behavior. Consequently, the current study assumed that management support might determine the bankers’ attitudes and GBUB and hypothesized the following relationships:

H4a: Management support positively influences bankers’ attitudes toward green banking usage behavior.

H4b: The management support positively influences bankers’ green banking usage behavior.

Attitudes and Green Banking Usage Behavior

Attitude refers to the consumers’ overall reaction to performing a specific behavior within a particular technology.74 A person’s attitude is one of the essential predictors of use behavior,75 which may be identified through technology-based banking systems such as green banking. Besides, attitudes can predict behavioral intention to use green banking systems and significantly influence GBUB. Many studies found that attitudes influence user behavior21,22 in green banking. Some research also concentrated on determining the attitudes toward use behavior76,77 in food delivery application during COVID-19;76–78 in online shopping applications and mobile banking applications;64 in the context of environmental sustainability. Hence, the current study developed the following hypothesis:

H5: Attitudes positively influence bankers’ green banking usage behavior.

Role of Attitudes as a Mediator

In behavioral adoption research, it is crucial to comprehend the indirect role of attitudes in shaping users’ behavior. For example, Al Amin et al80 understood the mediating role of attitudes in determining continuance intention to use mobile banking applications during COVID-19. Swaim et al64 also validated the indirect influence of attitudes on behavior in the context of environmental sustainability. Accordingly, the influence of attitudes is essential in green banking since norms, environmental sustainability, cognitive efforts, and management supports indirectly form bankers’ green financing behavior. Hence, we deposited the following hypotheses:

H6: Bankers’ attitudes mediate the influence of a) subjective norms, b) environmental sustainability, c) cognitive efforts, and d) management supports on bankers’ green banking usage behavior.

Methodology

Research Design

This study is confined to the analysis of the impact of COVID-19 on the green performance of banks and financial organizations in Bangladesh. We targeted the employees of six state-owned commercial banks (SOCBs), three specialized development banks (SDBs), 20 private commercial banks (PCBs), and ten financial institutions (FIs) in Bangladesh who have prior practical experiences in green banking activities. Furthermore, because the population and sampling framework were unknown, the researchers adopted the non-probability sampling method, which allowed them to choose respondents based on their subjective opinion.81

In order to overcome the pitfalls (eg, lower representation of result, false data, researcher bias, difficulty replicating results) of the convenience sample methodology, the study used the purposive sampling method (ie, the judgmental sampling technique). This sampling strategy made data collection much easier and less expensive to achieve a maximum level of variation with a low margin of error.82,83 In addition, the study focused on a broader range of target respondents who were more representative of the general population. A questionnaire was generated with two sections (demographic information and measurement items). All the items of the questionnaire, initially written in English, were taken from previous studies and were back-translated into Bangla, the official language of Bangladesh, for better understanding by the respondents.84 Finally, to check the questionnaire’s clarity, we conducted a pilot test and an in-depth interview (IDI) before the data collection. Based on the respondents’ feedback, the questionnaire was adjusted accordingly to confirm the survey questionnaire’s clarity and relevance to the study.

Data Collection

We collected the data during November and December 2021 in Bangladesh. A reply-paid envelope, a cover letter, and a questionnaire were mailed to the respondents following Dillman’s85 proposal. All the respondents were sent a questionnaire with a cover letter through their email addresses to facilitate their feedback.

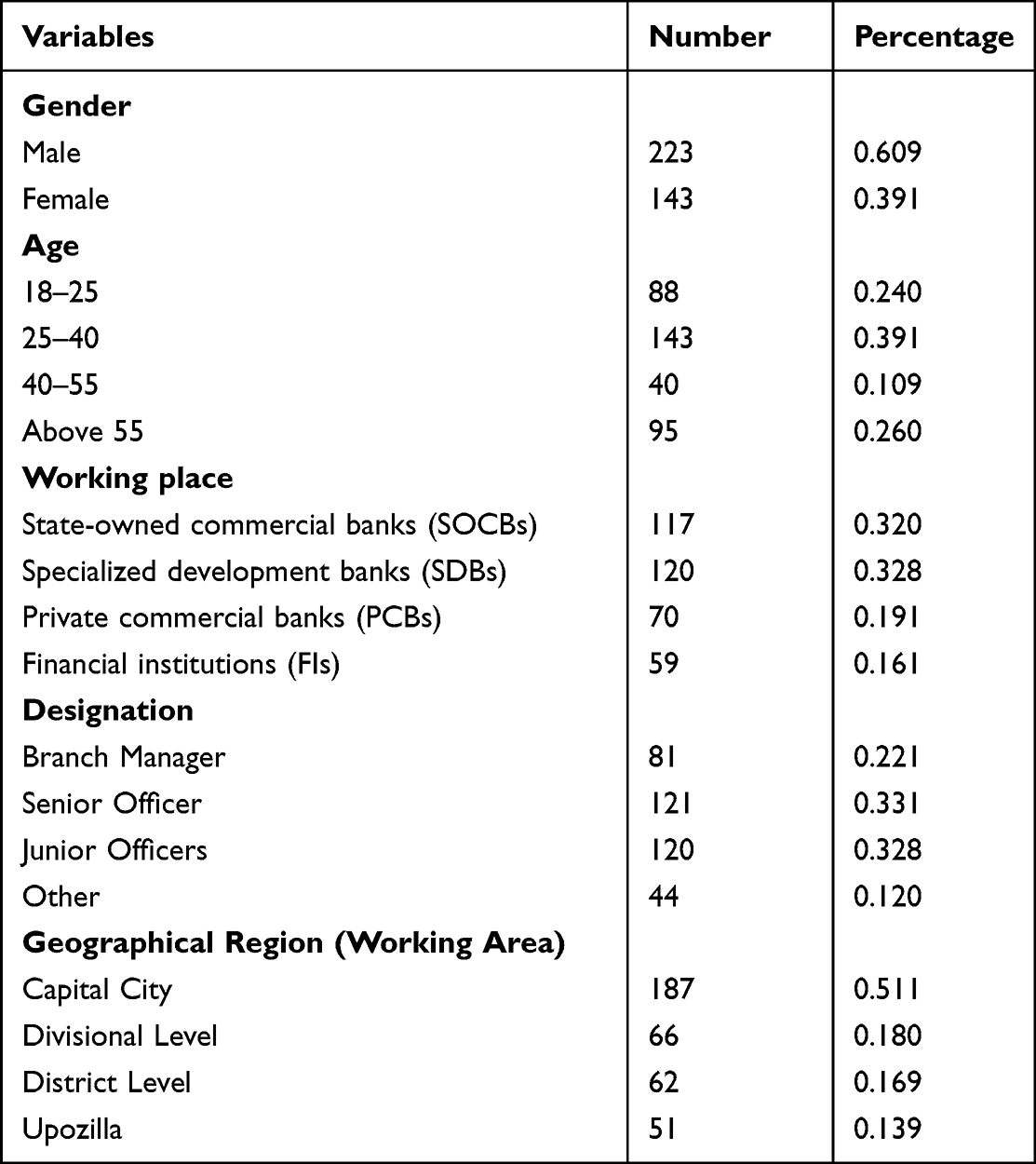

The respondents received an email from us asking them to return the completed questionnaire within two weeks. After another two weeks, we extended a final plea to the remaining respondents who did not respond to the survey after the two-week deadline. As previously reported, there were no significant differences between online and paper-based surveys85 (Chatterjee et al,101 2002; Hall,102 2008). We have distributed 554 questionnaires, and 376 feedbacks were received. After discarding the incomplete questionnaire, we found 366 complete responses (a response rate of 66.06%). Among them, 233 (60.9%) were male, and 143 (39.1%) were female. Most respondents were 18 to 40 years old (63.1%) and were working in one of the State-owned commercial banks or Specialized development banks (64.8%). Moreover, the respondents consisted from different geographical levels, such as Capital City (51.1%), Divisional Level (18.0%), District Level (16.9%), and Upozilla 13.9%). Table 2 summarizes the demographic profile of the respondents.

|

Table 2 Demographic Profile of the Respondents |

Measurement Items

We have utilized a seven-point Likert scale, ranging from 1 (strongly disagree) to 7 (strongly agree). The measurement items were adopted from existing works and were summarized in Appendix-A. Subjective norms were adapted from, Abdullah and Ward and Al Amin et al53,77 perceived cognitive efforts from, Dabholkar and Bagozzi, Kleijnen et al86,87 environmental sustainability from Kianpour et al103 (2014) and Kim et al104 (2015), management supports from Yap et al105 (1994) and Thong et al,88 attitudes toward green banking from Cho et al and Al Amin et al89,90 and GBUB from Farah et al.91 Because the constructs of perceived cognitive effort (PCE), environmental sustainability (ES), and management support (MS) are new in green banking literature, we have conducted an Exploratory Factor Analysis (EFA) to check the dimensionality of the measurement items. The EFA illustrates that PCE, ES, and MS items explained 79.66% of the total variance for these three factors.

Data Analysis

Structural equation modeling (SEM) tests the complex model with a series of dependent variables,90 (Cohen et al,106 2018). SEM is divided into two categories: CB-SEM and PLS-SEM. Based on the estimation, PLS-SEM (Partial Least Square SEM) evaluates the dependent and independent variables to maximize the explained variances, whereas CB-SEM (covariance-based SEM) checks the fit among the observed variables grounded in the covariance matrix.83 In this study, PLS-SEM was used to assess the degree to which endogenous constructs are affected by exogenous constructs and to measure structural correlations and confirmatory factor analysis (CFA).78,83

Common Method Bias

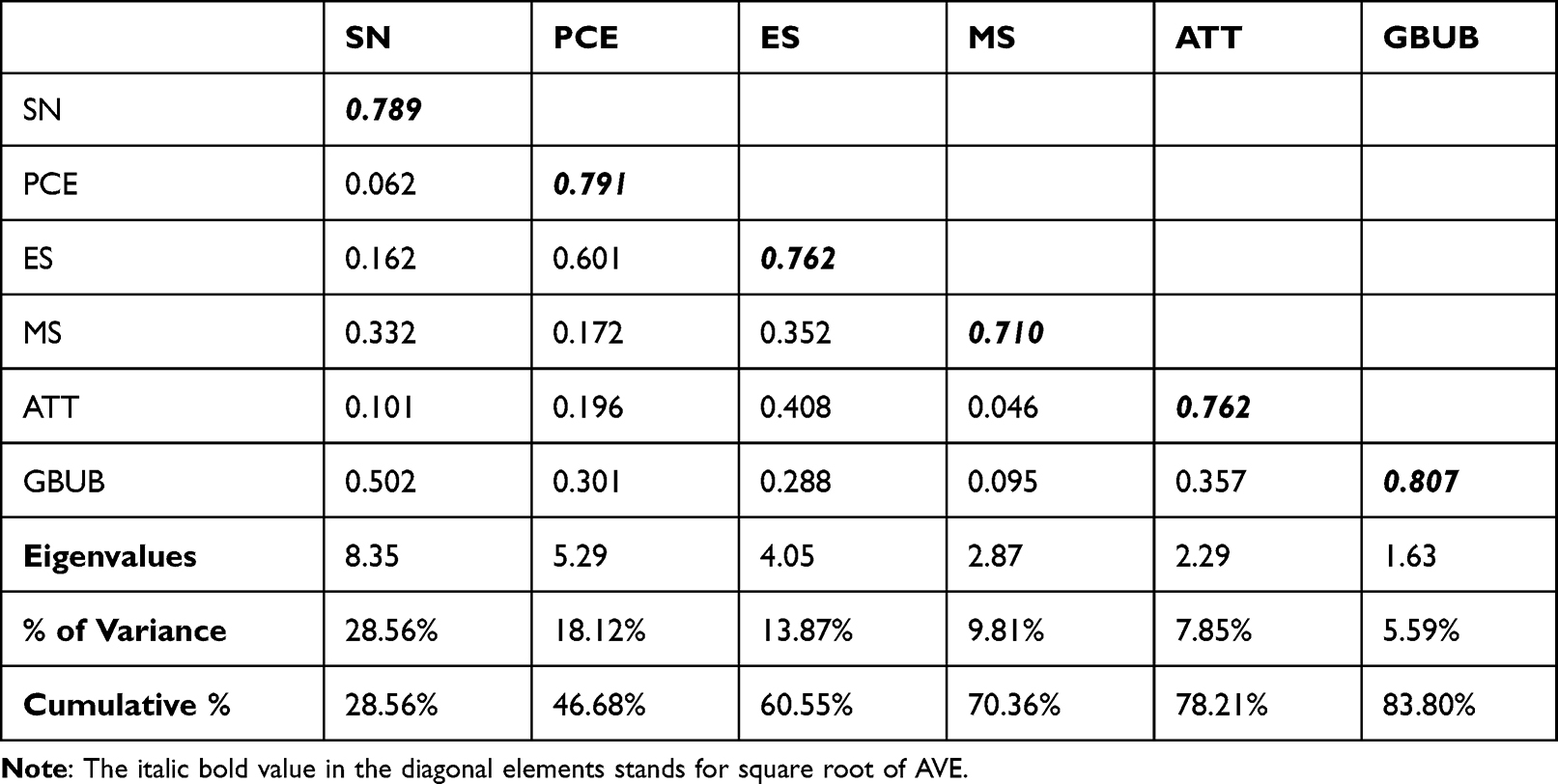

Researchers cannot rule out the probability of common method bias (CBM) when it comes to the perceptions of the target respondents . We ensured statistical and practical solutions before and after collecting the data to reduce the issues connected with CBM. The Lindell and Whitney107 (2001) test and Harman’s single-factor test were conducted to determine the likelihood of CMB. We also used a theoretically unrelated factor (i.e., switching cost) as a marker variable. The model’s R2 (correlation coefficient) and the marker variable revealed tolarable limit (maximum R2 = 0.00997). We followed Podsakoff et al108 (2003) the cut value (first factor < 50% of the total variance explained). Our PCA (principal component analysis) result picturizes that six factors having greater than 1.00 eigenvalues explained 83.80% variance. The first factor is responsible for only 28.56%, within the cut-off value shown in Table 4. Hence, data revealed that the CMB was not a problem for the current study.

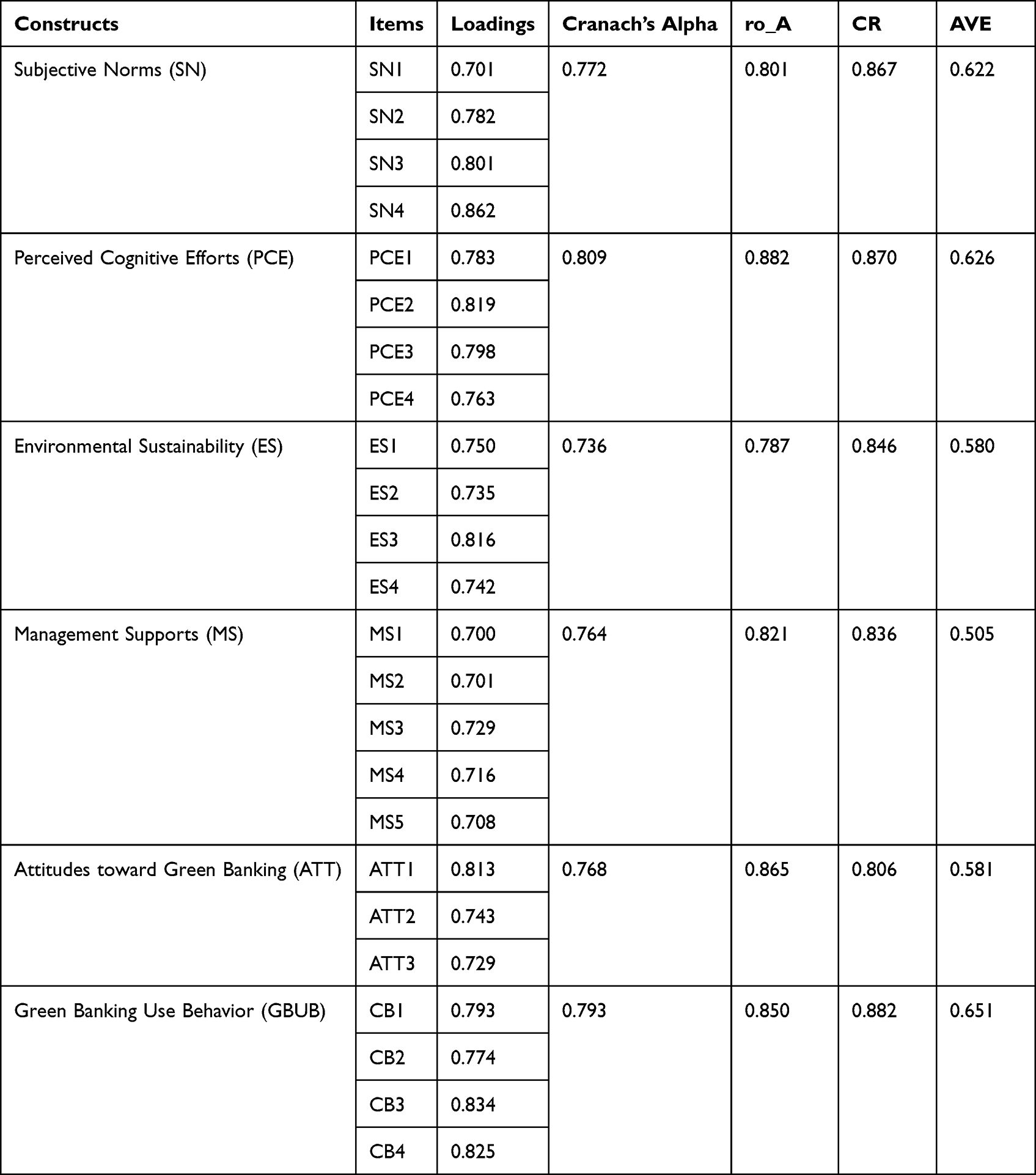

|

Table 3 Construct Reliability (roh_A, CR, and Cronbach Alpha), AVE, and Cross Loading |

|

Table 4 Fornell and Lacker Criteria |

Results

Measurement Model

The study used reliability, convergent validity, and discriminant validity to analyse the measurement model. Construct reliability of the model was evaluated by roh_A, composite reliability (CR), and Cronbach’s alpha. The convergent validity was tested using Average Variance Extracted (AVE) and cross-loading. The discriminant validity was assessed by analyzing the Fornell and Lacker criteria and HTMT, considering the procedures suggested by Hair et al.83

Construct Reliability

Composite reliability should not be less than 0.70, according to Hair et al83 recommendations. According to Hair et al,83 the minimum necessary value for Cranach’s alpha and roh_A is 0.70, which represents the model’s internal consistency. For all six constructs listed in Table 3, all three requirements (Cronbach’s alpha, roh_A, and CR) were met.

Convergent Validity

According to Hair et al,83 the AVE value should be larger than 0.5, and each item’s factor loadings should be greater than 0.7. The factor loadings ranged from 0.700 to 0.862 in Table 3, indicating the cross-loading of the constructs. Table 3 also depicts the AVE values, which range from 0.505 to 0.651.

Discriminant Validity

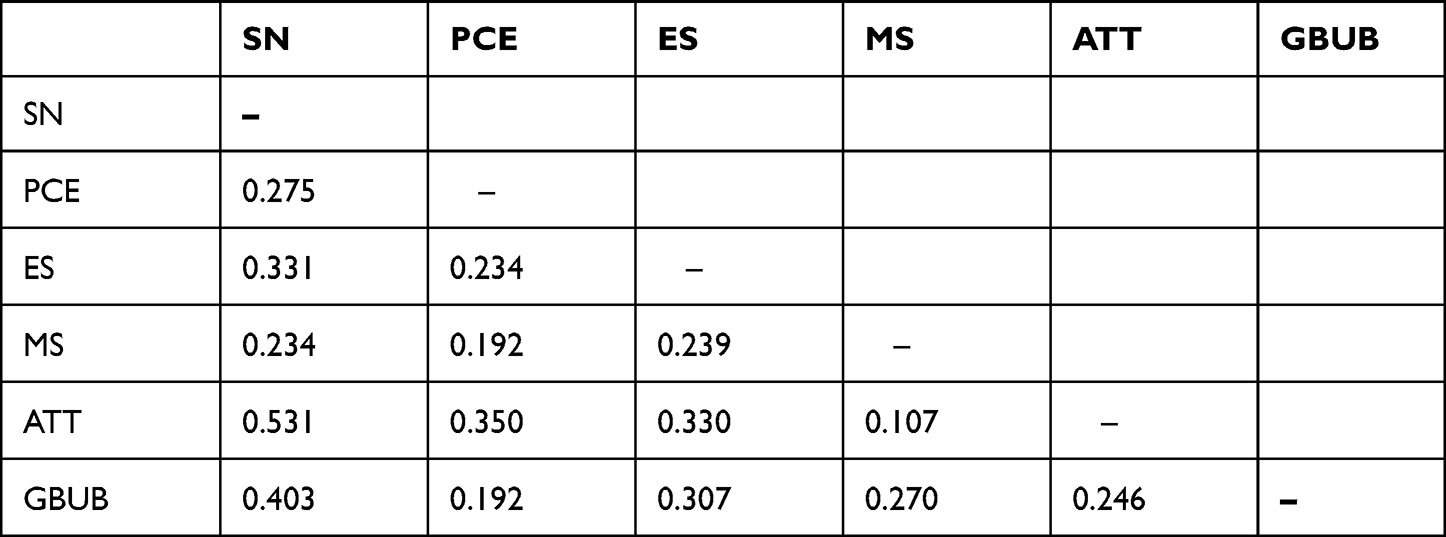

Discriminant validity was used to confirm the measurement model’s accuracy. Table 4 shows the Fornell and Lacker criterion, which states that all diagonal values (square root of AVE) are bigger than the off-diagonal values (correlations among the variables) shown in Table 4. The heterotrait-monotrait correlations ratio (HTMT) value, which must be less than 0.85 (HTMT>0.85) to assure validity,83,92 is shown in Table 5.

|

Table 5 Heterotrait-Monotrait Ratio (HTMT) |

Structural Model

According to Hair et al,83 the structural model is validated by the coefficient of determination (R2), the strength of the effect (f2), and the significance level of the path co-efficient. Researchers used the bootstrap with 5000 resamples to test all hypotheses and assessed t-statistics to test the path coefficient, as Henseler et al92 recommended.

Result of the Proposed Hypotheses, Multicollinearity, and Model Fit

The proposed hypotheses were tested using bootstrapping with 5000 resamples. Table 6 shows that SN positively influenced ATT (β = 0.309, t-statistics = 4.352, p < 0.000], and GBUB (β = 0.281, t-statistics = 4.607, p < 0.000). . Hence, H1a and H1b were supported. In H2a and H2b, we found that PCE positively influenced ATT (β = 0.401, t-statistics = 3.549, p < 0.000) and GBUB (β = 0.103, t-statistics = 2.020, p < 0.002). Thus, H2a and H2b were also supported. Moreover, in H3a and H3b, the results showed that ES significantly influenced ATT (β = 0.278, t-statistics = 2.752, p < 0.001) and GBUB (β = 0.503, t-statistics = 3.726, p < 0.001). Hence, the results supported H3a and H3b. MS positively influenced ATT (β = 0.291, t-statistics = 4.343, p 0.000). Hence, H4a was supported. Conversely, MS had also an influence on GBUB (β = 0.231, t-statistics = 1.426, p 0.071). Thus, the H4b was not supported. Moreover, H5 showed that ATT was associated with GBUB. Finally, the study results showed that ATT significantly influenced GBUB (β = 0.602, t-statistics = 5.523, p 0.015) in the context of green banking. Hence, H5 was accepted.

|

Table 6 Path Coefficient and Hypotheses Test Results |

Before validating the structural model, the researcher has considered and examined the variance inflation factor (VIF) to assess the lateral collinearity effect. Hair et al83 suggest that VIF values greater than 5 indicate lateral multicollinearity issues among the constructs, and the ideal value of VIF should be lower than 3.00 or close to 3.00. The study confirmed that no lateral VIF issue was found. Table 6 shows the VIF values for casual relationships, ranging from 1.002 to 2.273, representing no collinearity concern.

The study tested the model fit indices of the structural model, such as standardised root mean square residual (SRMR), RMS_theta, and the Normative Fit Index (NFI). Hair et al109 (2019) recommended that the value of SRMR be less than 0.08, RMS_theta be less than 0.1, and NFI be greater than 0.95 (Hu & Bentler,110 1999). Our research model satisfied the suggested threshold values (SRMR = 0.026, RMS_theta of 0.069, and NFI = 0.97). Finally, the structural model of the study is depicted in Figure 2.

|

Figure 2 Structural Model of the Study. |

Mediation Analysis

The research examined the indirect effects with 5000 bootstrap samples and the Sobel test93 to check the mediation effect of ATT. Moreover, the mediation effect was estimated with asymmetric confidence intervals (CI) by the procedure suggested by Baron and Kenny111 (1986).

In Table 7, the results of the study found that the indirect effect between GBUB and SN (b = 0.186, CI [0.028, 0.036], z = 3.418), PCE (b = 0.241, CI [0.038, 0.022], z = 2.985), ES (b = 0.167, CI [0.043, 0.042], z = 1.555), and MS (b = 0.175, CI [0.019, 0.021], z = 3.414) were significant. According to Hair et al,83 the results suggested the partial (complementary) mediation effect of ATT between GBUB and SN, PCE, and MS; no mediation (direct only effect) between GBUB and ES.

|

Table 7 Mediated Model |

Coefficient of Determinations

The squared multiple correlations are shown in Table 6, where ATT’s coefficient of determination (R2) was 0.709, and GBUB was 0.761. The independent variables (SN, PCE, ES, and MS) explained 74.1% of the variance in the dependent variable (GBUB) in the model with an adjusted R2 value of 0.738.

Strength of Effect

The strength of effect sizes (f2) was tested to know the representative influence of different constructs in a single model.92 Chin112 (1998) and Henseler et al92 suggest the strength of effect sizes (f2) value of 0.02 as a small effect, 0.15 as the medium effect, and 0.35 as a more significant effect. Table 6 shows the strength of effect sizes ranging from 0.001 to 2.001. The study also assessed the predictive capability of given parameters in partial least square SEM (PLS-SEM) based on blindfolding-based cross-validated redundancy (Q2). According to Hair et al,83 the Q2 value greater than zero (0) for a specific endogenous construct shows the overall path model’s predictive relevance. The results of the Q2 shown in Table 6 satisfied the criterion.

Discussion

We aim to determine the influence of social norms, perceived cognitive efforts, environmental sustainability, and management support on bankers’ attitudes and green banking usage behavior (GBUB) during COVID-19 pandemic. We have developed and validated nine hypotheses based on TRA and three new dimensions.

As per our prediction, hypothesis H1a was supported by the test results, which were consistent with the existing studies, e.g,54,55 in the context of organic food and Cross-Cultural Investigation, whereas H1b was supported by Hu et al and Kashif et al60,61 in low-carbon travel and managers’ intentions to behave ethically. SN explains the bankers’ beliefs, values, attitudes, and behavioral intentions as they fulfill their responsibility to make an ecologically balanced environment by receiving guidelines and suggestions from their colleagues, friends, bosses, and family members. Moreover, this social pressure might instigate to comply with a greater awareness of environmental protection. In addition, aware bankers are more responsible for growing positive attitudes and constructing use behavior conducive to financing activities that conform to sustainability guidelines.

Hypotheses 2a and 2b predict that PCE positively influenced ATT and GBUB. H2a was supported by Yang and Yoo,5 as the cognitive efforts of bankers are shaping their attitudes to be positive toward GBUB due to the effect of the advantages on the environment and economic sustainability. Moreover, the role of PCE on GBUB was found to be significant by Chen94 in the context of shopping websites as individuals have to perform their mental representation to solve the problem. Similarly, according to our in-depth interview, we argue that the psychological involvement in completing a particular task (eg, protecting the environment, increasing sustainability) increases bankers’ mental satisfaction and decreases the anxiety related to COVID-19. This satisfaction and reduction in anxiety might influence the bankers to perform superior task presentation in terms of efficiency versus accuracy in ensuring green banking practices.

Moreover, in H3a and H3b, we found that environmental sustainability (ES) positively influenced attitudes (ATT) and GBUB, respectively, which were supported by the previous study69 to predict factors influencing potential travelers’ behavioral intentions. They argued that sustainability values affect travelers’ decision to respect nature and increase shared responsibility. Accordingly, the present study understood the role of sustainability in reforming the bankers’ attitudes and green behavior to ensure that the study supported these hypotheses in green banking. We also argued that the global biosphere is situated on the acknowledgment of sustainable environmental concern; humans jeopardize ecological balance where natural resources are scarce. These human beings always desire to conform to ecological balance.

Hypotheses 4a and 4b predicted that management support (MS) positively influenced ATT and GBUB. However, we found H4a supported and H4b not supported by our results. The same in H4a was also analogous by26,27 in the context of knowledge sharing and artificial intelligence, whereas the relationship between MS and GBUB (H4b) was inconsistent with the findings of73 in the context of promoting firms’ energy-saving behavior. Vasiljeva et al26 mentioned that the technological trends of doing a particular job depend on employee support from management. We suppose that the (top) management support might build bankers’ positive attitudes toward green practices only if top managers engage themselves and take proactive initiatives to encourage green banking practices.

Finally, H5, this study posited and found that attitudes toward green banking positively impacted GBUB. This hypothesis was supported and consistent with the previous studies by Mishal et al93 on green purchase behavior and by Hu et al and Kashif et al60,61 in the context of low-carbon travel and perceived behavioral control by managers. Attitudes toward green banking significantly influence GBUB because we argued that human nature is to evaluate everything based on some inclination favouring or disfavoring in line.95

Contribution

Theoretical Contribution

The current study has several theoretical contributions in exploring the factors affecting the bankers' green banking usage behavior o in Bangladesh in existing green banking literature. First, the present study has proposed and validated a comprehensive model incorporating perceived cognitive efforts (PCE), environmental sustainability (ES), and management support (MS) into the theory of reasoned action (TRA) in clarifying the factors affecting bankers GBUB during COVID-19 in Bangladesh. The model is unique, and no such combination has yet been developed in green banking literature. Second, the current study recognized the perception of cognitive efforts as an independent variable to determine bankers’ attitudes toward GBUB. This hypothesized relationship contributes to the comprehension of individual perception of the influences between fundamental cognitions and how they are associated with bankers’ intention to practice sustainable banking (ie, green banking).

Moreover, mental engagement in green practices influences bankers to develop positive attitudes and green behavior, which might increase psychological contentment essential to being strong during COVID-19. Third, environmental sustainability influences bankers’ attitudes and GBUB. These positive attitudes and behavior toward green practices might lessen the escalating concerns for unceasing degradation of the natural environment through ethical consumerism (ie, green consumerism). More specially, it is essentially theoretical and empirical evidence presented in this study as due to the negative influences of ecological imbalance, bankers might respect sustainability spectrum issues which specifies the goal accomplishment procedure. Fourth, the current research was conducted in social isolation setting where people feel worried and avoid being infected by the virus.

Moreover, existing literature on green or sustainable banking was conducted in a normal setting and primarily did not measure the influences of COVID-19 on bankers’ attitudes and GBUB. This study examined how the pandemic outbreaks figured the bakers’ green behavior during COVID-19. Finally, in this study, management support is a significant determinant in understanding bankers’ motivation to use green practices to increase the practical consciousness of limited and fragile natural resources. We found that management involvement and commitment work as motivators that assist bankers to overcome the confrontations to implement green financing.

Managerial Implications

As a result of this study, analysts and investors will better know sustainable green banking practices adoption and how these practices affect banks’ overall performance. This information could be used to assess a bank’s environmental management adoption and financial performance in Bangladesh in the future. This research has ramifications for the banking sector in Bangladesh in terms of legislative and compliance development. Hence, the current study has several managerial implications for green banking usage behaviour, in addition to its theoretical contributions.

At the institutional level, policymakers should strive to establish an environment that promotes the long-term viability of green banking practices. All listed banks should be required to declare their green banking plans in their final reports by the Bangladesh Securities and Exchange Commission to raise exact awareness of such practices among stakeholders. Furthermore, the Central Bank of Bangladesh must provide a solid strategic framework for banks to pursue green practices to help the environment. The authorities need to learn about bankers’ feelings, attitudes, and motivations and should provide commitments and support to raise awareness of green banking practices. According to the government, green banking practices for financial institutions should also be included as a condition in corporate governance regulations. This would validate banks’ green banking operations and help them perform better in terms of the environment.

Furthermore, utilitarian green banking motivation should be ensured as values through which motivation is cognitive, needs-based, value-focused, and goal-oriented. Thus, individuals who have utilitarian motivation tend to be more rational, and the implementers need to be careful in comprehending the bankers’ cognitive behaviors. Research has shown that the affective meaning of images, such as schematic faces, improves perceived enjoyment. Therefore, the management can use affective meanings of images such as “thumb-up” or “like” bankers might be more likely to perceive enjoyment when practicing green behavior. Active green bankers can motivate new one as bankers always attend to the recommendations from their colleagues, friends, and family members to comply with a particular task. Hence, these bankers should be taken care of primarily by giving extra facilities (eg, due time promotion, financial rewards, and other supports).

Limitations and Future Study

The current study, like most others, has some limitations. First, we collected the data during the COVID-19 pandemic in Bangladesh, a developing country, which may limit the generalization of study findings to different geographical locations and periods. Hence, future studies can be conducted considering the respondents from other culturally different countries. Second, because the study was cross-sectional, prone to methodological biases, and causation between variables may be limited. However, a follow-up study with a longitudinal design can confirm the causality of the association across time. Third, the information was acquired from the supply-side only (ie, bankers); the common method variance (CMV) might be an issue in this study. Although CMV test results found no CMV problem, future studies may collect data from customers and bankers (ie, demand and supply sides).

Concluding Remarks

The study aims to empirically validate a unique model incorporating perceived cognitive effort, sustainability perception, and management supports into TRA. First, the study understands the bankers’ complex decision-making processes. Second, it also determines bankers’ attitudes toward green banking and GBUB by integrating three new dimensions, eg, perceived cognitive efforts, management support, and environmental support. Finally explores that environmental sustainability, perceived cognitive efforts, subjective norms, and attitudes might reshape bankers’ green bank usage behavior. Accordingly, it provided theoretical and managerial contributions to relevant stakeholders.

Data Sharing Statement

The datasets used and/or analyzed during the current study are confidential and available upon the demand from corresponding author.

Ethics Statement

This study was approved by the committee from the office of Advisor of Research Cell, Jashore University Science and Technology, Bangladesh. Moreover, to confirm ethical issues, we have taken consent from all respondents in information sheets, which explained the study’s true purpose. The study was ethically approved by Research Cell, Jashore University Science and Technology, Bangladesh.

Acknowledgment

The authors would like to thank all of the researchers in green banking literature and Prof. Dr. Md. Masudur Rahman, Professor of Marketing, University of Dhaka, Bangladesh, for his invaluable support and inspiration in conducting this study.

Funding

The project is self-funded. No external fund is available for this project.

Disclosure

The authors declare that they have no known competing financial interests or personal relationships.

References

1. Rehman A, Ullah I, Afridi F-A, et al. Adoption of green banking practices and environmental performance in Pakistan: a demonstration of structural equation modelling. Environ Dev Sustainability. 2021;23(9):13200–13220. doi:10.1007/s10668-020-01206-x

2. Chen Y-S. The Drivers of Green Brand Equity: green Brand Image, Green Satisfaction, and Green Trust. J Business Ethics. 2010;93(2):307–319. doi:10.1007/s10551-009-0223-9

3. Chen J, Siddik AB, Zheng G-W, Masukujjaman M, Bekhzod S. The Effect of Green Banking Practices on Banks’ Environmental Performance and Green Financing: an Empirical Study. Energies. 2022;15(4):1292. doi:10.3390/en15041292

4. Ding X, Li W, Huang D, Qin X. Does Innovation Climate Help to Effectiveness of Green Finance Product R&D Team? The Mediating Role of Knowledge Sharing and Moderating Effect of Knowledge Heterogeneity. Sustainability. 2022;14(7):3926. doi:10.3390/su14073926

5. Yang H, Yoo Y. It’s all about attitude: revisiting the technology acceptance model. Decis Support Syst. 2004;38(1):19–31. doi:10.1016/S0167-9236(03)00062-9

6. Zhang X, Wang Z, Zhong X, Yang S, Siddik AB. Do Green Banking Activities Improve the Banks’ Environmental Performance? The Mediating Effect of Green Financing. Sustainability. 2022;14(2):989. doi:10.3390/su14020989

7. Fang Y, Shao Z. Whether green finance can effectively moderate the green technology innovation effect of heterogeneous environmental regulation. Int J Environ Res Public Health. 2022;19(6):3646. doi:10.3390/ijerph19063646

8. Urban MA, Wójcik D. Dirty banking: probing the gap in sustainable finance. Sustainability. 2019;11(6):1745. doi:10.3390/su11061745

9. Bruwer PJS. A descriptive model of success for computer-based information systems. Information Manage. 1984;7(2):63–67. doi:10.1016/0378-7206(84)90010-7

10. Bukhari SAA, Hashim F, Amran A. Pathways towards Green Banking adoption: moderating role of top management commitment. Int J Ethics Sys. 2022;38(2):286–315. doi:10.1108/IJOES-05-2021-0110

11. Sun H, Rabbani MR, Ahmad N, et al. CSR, Co-Creation and Green Consumer Loyalty: are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. Sustainability. 2020;12(24):10688. doi:10.3390/su122410688

12. Yan C, Siddik AB, Yong L, Dong Q, Zheng G-W, Rahman MN. A Two-Staged SEM-Artificial Neural Network Approach to Analyze the Impact of FinTech Adoption on the Sustainability Performance of Banking Firms: the Mediating Effect of Green Finance and Innovation. Systems. 2022;10(5):148. doi:10.3390/systems10050148

13. Guang-Wen Z, Siddik AB. Do corporate social responsibility practices and green finance dimensions determine environmental performance? An Empirical Study on Bangladeshi Banking Institutions. Front Environ Sci. 2022;10. doi:10.3389/fenvs.2022.890096

14. Ziolo M, Filipiak BZ, Bak I, Cheba K. How to design more sustainable financial systems: the roles of environmental, social, and governance factors in the decision-making process. Sustainability. 2019;11(20):5604. doi:10.3390/su11205604

15. Sharma M, Choubey A. Green banking initiatives: a qualitative study on Indian banking sector. Environ Dev Sustain. 2021;1:654.

16. Zhang D, Zhang Z and Managi S. 2019. A bibliometric analysis on green finance: Current status, development, and future directions. Finance Research Letters. 2019; 29: 425–430. doi:10.1016/j.frl.2019.02.003

17. Desalegn G, Fekete-Farkas M, Tangl A. The effect of monetary policy and private investment on green finance: evidence from Hungary. J Risk Financial Manage. 2022;15(3):117. doi:10.3390/jrfm15030117

18. Li X, Yang Y. Does green finance contribute to corporate technological innovation? The moderating role of corporate social responsibility. Sustainability. 2022;14(9):5648. doi:10.3390/su14095648

19. Ye T, Xiang X, Ge X, Yang K. Research on green finance and green development based eco-efficiency and spatial econometric analysis. Sustainability. 2022;14(5):2825. doi:10.3390/su14052825

20. Ibe-Enwo I, Garanti, Popoola. Assessing the relevance of green banking practice on bank loyalty: the mediating effect of green image and bank trust. Sustainability. 2019;11(17):4651. doi:10.3390/su11174651

21. Burhanuddin B, Ronny R, Sihotang ET. Consumer guilt and green banking services. Int J Consum Stud. 2020;45(3):396–408. doi:10.1111/ijcs.12602

22. Taneja S, Ali L. Determinants of customers’ intentions towards environmentally sustainable banking: testing the structural model. J Retailing Consumer Services. 2020;102418. doi:10.1016/j.jretconser.2020.102418

23. Bose S, Khan HZ, Rashid A, Islam S. What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pacific J Manage. 2017;35(2):501–527. doi:10.1007/s10490-017-9528-x

24. Gunawan J, Permatasari P, Sharma U. Exploring sustainability and green banking disclosures: a study of banking sector. Environ Dev Sustain. 2021.

25. Khairunnessa F, Vazquez-Brust DA, Yakovleva N. A review of the recent developments of green banking in Bangladesh. Sustainability. 2021;13(4):1904. doi:10.3390/su13041904

26. Vasiljeva T, Kreituss I, Lulle I. Artificial intelligence: the attitude of the public and representatives of various industries. J Risk Financial Manage. 2021;14(8):339. doi:10.3390/jrfm14080339

27. Yeo RK, Gold J. Knowledge sharing attitude and behaviour in Saudi Arabian organisations: why trust matters. Int J Human Resources Dev Manage. 2014;14(1/2/3):97. doi:10.1504/IJHRDM.2014.068082

28. Lymperopoulos C, Chaniotakis IE, Soureli M. A model of green bank marketing. J Financial Services Marketing. 2012;17:177–186. doi:10.1057/fsm.2012.10

29. Park H, Kim JD. Transition towards green banking: role of financial regulators and financial institutions. Asian J Sustain Soc Responsibility. 2020;5(1). doi:10.1186/s41180-020-00034-3

30. Julia T, Rahman MP, Kassim S. Shariah compliance of green banking policy in Bangladesh. Humanomics. 2016;32(4):390–404. doi:10.1108/H-022016-0015

31. Bryson D, Atwal G, Chaudhuri A, Dave K. Antecedents of intention to use green banking services in India. Strategic Change. 2016;25:551–567. doi:10.1002/jsc.2080

32. Dialysa F. Green Banking: One Effort to Achieve the Principle of Good Corporate Governance (GCG). Atlantis Press; 2015.

33. Julia T, Kassim S. Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh based on Maqasid Shariah framework. J Islamic Marketing. 2019.

34. Shamshad M, Sarim M, Akhtar A, Tabash MI. Identifying critical success factors for sustainable growth of Indian banking sector using interpretive structural modeling (ISM). Int J Soc Econ. 2018;45(8):1189–1204. doi:10.1108/IJSE-10-2017-0436

35. Fishbein M, Ajzen I. Belief, Attitude, Intention and Behavior. Reading, MA: Addison-Wesley; 1975.

36. Fishbein MA. Attitude and the prediction of behaviour. In: Fishbein MA, editor. Readings in Attitude Theory and Measurement. New York: Wiley; 1967:477–492.

37. Ajzen I, Fishbein M. Understanding Attitudes and Predicting Social Behavior. Englewood Cliffs, NJ: Prentice-Hall; 1980.

38. Sainaghi R. (2020). The current state of academic research into peer-to-peer accommodation platforms. International Journal of Hospitality Management, 89 102555. doi:10.1016/j.ijhm.2020.102555

39. Zhelyazkova V, Kitanov Y. Green banking – definition, scope, and proposed business model. Ecol Safety. 2015;9:309–315.

40. Gill C. Top 5 Sustainable Banks. World Finance; 2018.

41. Bukhari SAA, Hashim F, Amran AB, Hyder K. Green Banking and Islam: two sides of the same coin. J Islamic Marketing. 2019;11(4):977–1000. doi:10.1108/JIMA-09-2018-0154

42. Kumar K, Prakash A. Developing a framework for assessing sustainable banking performance of the Indian banking sector. Soc Respons J. 2018;2:86.

43. Nosratabadi S, Pinter G, Mosavi A, Semperger S. Sustainable Banking; Evaluation of the European Business Models. Sustainability. 2020;12(6):2314. doi:10.3390/su12062314

44. Sharmeen K, Hasan R, Miah MD. Underpinning the benefits of green banking: a comparative study between Islamic and conventional banks in Bangladesh. Thunderbird Int Business Rev. 2018;61(5):735–744. doi:10.1002/tie.22031

45. Effendi I, Murad M, Rafiki A, Lubis MM. The application of the theory of reasoned action on services of Islamic rural banks in Indonesia. J Islamic Marketing. 2020;12(5):951.

46. Janah N, Medias F, Pratiwi EK. The intention of religious leaders to use Islamic banking services: the case of Indonesia. J Islamic Marketing. 2020;12(9):1786–1800. doi:10.1108/JIMA-01-2020-0012

47. Lujja S, Omar Mohammad M, Hassan R. Modelling public behavioral intention to adopt Islamic banking in Uganda. Int J Islamic Middle Eastern Finance Manage. 2016;9(4):583–600. doi:10.1108/IMEFM-08-2015-0092

48. Mishra D, Akman I, Mishra A. Theory of Reasoned Action application for Green Information Technology acceptance. Comput Human Behav. 2014;36:29–40. doi:10.1016/j.chb.2014.03.030

49. Hostler RE, Yoon VY, Guimaraes T. Assessing the impact of internet agent on end users’ performance. Decis Support Syst. 2005;41(1):313–323. doi:10.1016/j.dss.2004.07.002

50. Maes P. Agents that Reduce Work and Information Overload. Association for Computing Machinery. Commun ACM. 1994;37:31–40. doi:10.1145/176789.176792

51. Russo JE, Dosher BA. Strategies for multiattribute binary choice. J Exp Psychol. 1983;9(4):676. doi:10.1037//0278-7393.9.4.676

52. Obiora SC, Bamisile O, Opoku-Mensah E, Kofi Frimpong AN. Impact of Banking and Financial Systems on Environmental Sustainability: an Overarching Study of Developing, Emerging, and Developed Economies. Sustainability. 2020;12(19):8074. doi:10.3390/su12198074

53. Abdullah F, Ward R. Developing a General Extended Technology Acceptance Model for E-Learning (GETAMEL) by analysing commonly used external factors. Comput Human Behav. 2016;56:238–256. doi:10.1016/j.chb.2015.11.036

54. Al-Swidi A, Mohammed Rafiul Huque S, Haroon Hafeez M, Noor Mohd Shariff M. The role of subjective norms in the theory of planned behavior in the context of organic food consumption. Br Food J. 2014;116(10):1561–1580. doi:10.1108/BFJ-05-2013-0105

55. Trongmateerut P, Sweeney JT. The Influence of Subjective Norms on Whistle-Blowing: a Cross-Cultural Investigation. J Business Ethics. 2012;112(3):437–451. doi:10.1007/s10551-012-1270-1

56. Tavakoly Sany SB, Aman N, Jangi F, Lael-Monfared E, Tehrani H, Jafari A. Quality of life and life satisfaction among university students: exploring, subjective norms, general health, optimism, and attitude as potential mediators. J Am Coll Health. 2021;1–8. doi:10.1080/07448481.2021.1920597

57. Tarkiainen A, Sundqvist S. Subjective norms, attitudes and intentions of Finnish consumers in buying organic food. Br Food J. 2005;107(11):808–822. doi:10.1108/00070700510629760

58. Kim H, Kim T, Shin SW. Modeling roles of subjective norms and eTrust in customers’ acceptance of airline B2C eCommerce websites. Tour Management. 2009;30(2):266–277. doi:10.1016/j.tourman.2008.07.001

59. Venkatesh V, Thong JY, Xu X. Consumer acceptance and use of information technology: extending the unified theory of acceptance and use of technology. MIS Quarterly. 2012:157–178.

60. Hu X, Wu N, Chen N. Young People’s Behavioral Intentions towards Low-Carbon Travel: extending the Theory of Planned Behavior. Int J Environ Res Public Health. 2021;18(5):2327. doi:10.3390/ijerph18052327

61. Kashif M, Zarkada A, Ramayah T. The impact of attitude, subjective norms, and perceived behavioural control on managers’ intentions to behave ethically. Total Quality Manage Business Excellence. 2016;29(5–6):481–501. doi:10.1080/14783363.2016.1209970

62. Liabsuetrakul T, Chongsuvivatwong V, Lumbiganon P, Lindmark G. Obstetricians’ attitudes, subjective norms, perceived controls, and intentions on antibiotic prophylaxis in caesarean section. Soc Sci Med. 2003;57(9):1665–1674. doi:10.1016/S0277-9536(02)00550-6

63. Si H, Shi J, Tang D, Wen S, Miao W, Duan K. Application of the theory of planned behavior in environmental science: a comprehensive bibliometric analysis. Int J Environ Res Public Health. 2019;16(15):2788. doi:10.3390/ijerph16152788

64. Swaim JA, Maloni MJ, Napshin SA, Henley AB. Influences on student intention and behavior toward environmental sustainability. J Business Ethics. 2013;124(3):465–484.

65. Todd P, Benbasat I. Inducing compensatory information processing through decision aids that facilitate effort reduction: an experimental assessment. J Behav Decis Mak. 2000;13(1):91–106. doi:10.1002/(SICI)1099-0771(200001/03)13:1<91::AID-BDM345>3.0.CO;2-A

66. Caniato F, Caridi M, Crippa L, Moretto A. Environmental sustainability in fashion supply chains: an exploratory case based research. Int J Production Economics. 2012;135(2):659–670. doi:10.1016/j.ijpe.2011.06.001

67. Peattie K, Belz F-M. Sustainability marketing — an innovative conception of marketing. Gallen. 2010;27(5):8–15. doi:10.1007/s11621-010-0085-7

68. Kong L, Liu Z, Wu J. A systematic review of big data-based urban sustainability research: state-of-The-science and future directions. J Clean Prod. 2020;273:123142. doi:10.1016/j.jclepro.2020.123142

69. Chuang L-M, Chen P-C, Chen -Y-Y. The Determinant Factors of Travelers’ Choices for Pro-Environment Behavioral Intention-Integration Theory of Planned Behavior, Unified Theory of Acceptance, and Use of Technology 2 and Sustainability Values. Sustainability. 2018;10(6):1869. doi:10.3390/su10061869

70. Jha AK, Dikshit S. Employee satisfaction: a comparative study between tata steel and central coalfield limited, Ranchi. Anusandhanika. 2015;7:111–119.

71. Bushra A, Masood M. The impact of organizational capabilities on organizational performance: empirical evidence from banking industry of Pakistan. Pakistan J Commerce Soc Sci. 2017;11:408–438.

72. Leflot G, van Lier PAC, Onghena P, Colpin H. The role of teacher behavior management in the development of disruptive behaviors: an intervention study with the good behavior game. J Abnorm Child Psychol. 2010;38(6):869–882. doi:10.1007/s10802-010-9411-4

73. Zhang Y, Wei Y, Zhou G. Promoting firms’ energy-saving behavior: the role of institutional pressures, top management support and financial slack. Energy Policy. 2018;115:230–238. doi:10.1016/j.enpol.2018.01.003

74. Alagoz SM, Hekimoglu H. A study on tam: analysis of customer attitudes in online food ordering system. Procedia Soc Behav Sci. 2012;62:1138–1143. doi:10.1016/j.sbspro.2012.09.195

75. Davis FD. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly. 1989;13(3):319–340. doi:10.2307/249008

76. Al Amin M, Arefin MS, Sultana N, Islam MR, Jahan I, Akhtar A. Evaluating the customers’ dining attitudes, e-satisfaction and continuance intention toward mobile food ordering apps (MFOAs): evidence from Bangladesh. Eur J Manage Business Economics. 2021a;30(2):211–229. doi:10.1108/ejmbe-04-2020-0066

77. Al Amin M, Arefin MS, Alam MR, Ahammad T, Hoque MR. Using Mobile Food Delivery Applications during COVID-19 Pandemic: an Extended Model of Planned Behavior. J Food Products Marketing. 2021b;27(2):105–126. doi:10.1080/10454446.2021.1906817

78. Al Amin M, Arefin MS, Hossain I, Islam MR, Hossain M, Sultana N. Evaluating the Determinants of Customers’ Mobile Grocery Shopping Application (MGSA) Adoption during COVID-19 Pandemic. J Global Marketing. 2021c;35(3):228–247. doi:10.1080/08911762.2021.1980640

79. Al Amin M, Arefin MS, Rasul. TF, Alam. MS. Understanding the Determinants of Mobile Banking Services Continuance Intention in Rural Bangladesh during the COVID-19 Pandemic. J Global Marketing. 2022c;35(4):324–347. doi:10.1080/08911762.2021.2018750

80. Al Amin M. The Influence of Psychological, Situational and the Interactive Technological Feedback-Related Variables on Customers’ Technology Adoption Behavior to Use Online Shopping Applications. J Global Marketing. 2022b;35(4):384–407. doi:10.1080/08911762.2022.2051157

81. Saunders M, Lewis P, Thornhill A, Bristow A. Research methods for business students’ chapter 4: understanding research philosophy and approaches to theory development. In: Saunders MNK, Philip L, Adrian T, Alex B, editors. Research Methods for Business Students. Pearson Education; 2019:128–171.

82. Battaglia MP. Nonprobability sampling. In: Lavrakas PJ, editor. Encyclopedia of Survey Research Methods. SAGE Publications; 2008:523–526.

83. Hair JF, Hult GTM, Ringle CM, Sarstedt M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM).

84. Brislin RW. Comparative research methodology: cross-cultural studies. Int J Psychol. 1976;11(3):215–229. doi:10.1080/00207597608247359

85. Dillman DA. Mail and Internet Surveys: The Tailored Design Method.

86. Dabholkar PA, Bagozzi RP. An attitudinal model of technology-based self-service: moderating effects of consumer traits and situational factors. J Academy Marketing Sci. 2002;30(3):184–201. doi:10.1177/0092070302303001

87. Kleijnen M, de Ruyter K, Wetzels M. An assessment of value creation in mobile service delivery and the moderating role of time consciousness. J Retailing. 2007;83(1):33–46. doi:10.1016/j.jretai.2006.10.004

88. Thong JYL, Yap C-S, Raman KS. Top Management Support, External Expertise and Information Systems Implementation in Small Businesses. Information Sys Res. 1996;7(2):248–267. doi:10.1287/isre.7.2.248

89. Cho M, Bonn MA, Li JJ. Differences in perceptions about food delivery apps between single-person and multi-person households. Int J Hospitality Manage. 2019;77:108–116. doi:10.1016/j.ijhm.2018.06.019

90. Al Amin M, Alam MR, Alam MZ. Antecedents of students’ e-learning continuance intention during COVID-19: an empirical study. E Learn Digital Media. 2022a;204275302211039. doi:10.1177/20427530221103915

91. Farah MF, Hasni MJS, Abbas AK. Mobile-banking adoption: empirical evidence from the banking sector in Pakistan. Int J Bank Marketing. 2018;36(7):1386–1413. doi:10.1108/IJBM-10-2017-0215

92. Henseler J, Ringle CM, Sarstedt M. A new criterion for assessing discriminant validity in variance-based structural equation modelling. J Acad Marketing Sci. 2015;43(1):115–135. doi:10.1007/s11747-014-0403-8

93. Sobel ME. Asymptotic confidence intervals for indirect effects in structural equation models. Sociol Methodol. 1982;13:290–312. doi:10.2307/270723

94. Chen C-W. Five-star or thumbs-up? The influence of rating system types on users’ perceptions of information quality, cognitive effort, enjoyment and continuance intention. Internet Res. 2017;27(3):478–494. doi:10.1108/IntR-08-2016-0243

95. Mishal A, Dubey R, Gupta OK, Luo Z. Dynamics of environmental consciousness and green purchase behaviour: an empirical study. Int J Climate Change Strategies Management. 2017;9(5):682–706. doi:10.1108/IJCCSM-11-2016-0168

96. Zeng Y, Wang F, Wu J. The Impact of Green Finance on Urban Haze Pollution in China: a Technological Innovation Perspective. Energies. 2022;15(3):801. doi:10.3390/en15030801

97. Wang Y, Zhao N, Lei X, Long R. Green Finance Innovation and Regional Green Development. Sustainability. 2021;13(15):8230. doi:10.3390/su13158230

98. Zheng G-W, Siddik AB, Masukujjaman M, Fatema N. Factors affecting the sustainability performance of financial institutions in Bangladesh: the role of green finance. Sustainability. 2021a;13(18):10165. doi:10.3390/su131810165

99. Zheng G-W, Siddik AB, Masukujjaman M, Fatema N, Alam SS. Green Finance Development in Bangladesh: the Role of Private Commercial Banks (PCBs). Sustainability. 2021b;13(2):795. doi:10.3390/su13020795

100. Xu H, Mei Q, Shahzad F, Liu S, Long X, Zhang J. Untangling the impact of green finance on the enterprise green performance: a meta-analytic approach. Sustainability. 2020;12(21):9085. doi:10.3390/su12219085

101. Chatterjee D, Grewal R and Sambamurthy V. (2002). Shaping up for E-Commerce: Institutional Enablers of the Organizational Assimilation of Web Technologies. MIS Quarterly, 26(2), 65. doi:10.2307/4132321

102. Hall R (2008). Applied Social Research: Planning, Designing and Conducting Realworld Research. Palgrave Macmillan.

103. Kianpour K, Jusoh A and Asghari M. (2014). Environmentally friendly as a new dimension of product quality. International Journal of Quality & Reliability Management, 31(5), 547–565. doi:10.1108/IJQRM-06-2012-0079

104. Kim J, Taylor CR, Kim KH, Lee KH Measures of perceived sustainability. Journal of Global Scholars of Marketing Science. 2015;25(2):182–193.

105. Yap CS, Thong JY, Raman KS Effect of government incentives on computerisation in small business. Eur J Inf Syst. 1994;3(3):191–206.

106. Cohen L, Manion L, Morrison K (2018). Research Methods in Education. Routledge.

107. Lindell MK and Whitney DJ. (2001). Accounting for common method variance in cross-sectional research designs. J Appl Psychol, 86(1), 114–121. doi:10.1037/0021-9010.86.1.114

108. Podsakoff PM, MacKenzie SB, Lee J and Podsakoff NP. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. J Appl Psychol, 88(5), 879–903. doi:10.1037/0021-9010.88.5.879

109. Hair JF, Risher JJ, Sarstedt M and Ringle CM. (2019). When to use and how to report the results of PLS-SEM. EBR, 31(1), 2–24. doi:10.1108/EBR-11-2018-0203

110. Hu L and Bentler PM. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. 10.1080/10705519909540118

111. Baron RM, Kenny DA The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J Pers Soc Psychol. 1986;51(6):1173–1182.

112. Chin WW Commentary: Issues and opinion on structural equation modeling. MIS Quarterly. 1998;22(1):vii–xvi.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.