Back to Journals » ClinicoEconomics and Outcomes Research » Volume 14

Retrospective Database Analysis to Explore Patterns and Economic Burden of Switchback to Brand After Generic or Authorized Generic Utilization

Authors Alderfer J, Aggarwal J ![]() , Gilchrist K, Alvir JMJ, Cook J

, Gilchrist K, Alvir JMJ, Cook J ![]() , Park SH, Stephens JM

, Park SH, Stephens JM ![]()

Received 11 May 2021

Accepted for publication 1 March 2022

Published 27 April 2022 Volume 2022:14 Pages 281—291

DOI https://doi.org/10.2147/CEOR.S319796

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Prof. Dr. Dean Smith

Justine Alderfer,1 Jyoti Aggarwal,2 Kim Gilchrist,1 Jose Maria Jimenez Alvir,3 Joseph Cook,4 Sang Hee Park,5 Jennifer M Stephens5

1Medical Affairs, Pfizer Inc., Collegeville, PA, USA; 2Evidence & Access, OPEN Health, Newton, MA, USA; 3Global Product Development, Pfizer Inc., New York, NY, USA; 4Clinical Development and Medical Affairs, Viatris, Canonsburg, PA, USA; 5Evidence & Access, OPEN Health, Bethesda, MD, USA

Correspondence: Justine Alderfer, US Medical Affairs, Pfizer, 500 Arcola Rd., Collegeville, PA, 19426, USA, Tel +1 484-865-3105, Email [email protected]

Background: Despite demonstration of bioequivalence of generics to brands and the potential for reduced costs, some patients switch back from a generic to the brand. A prior retrospective analysis suggested that this switchback rate may be lower among patients that had initially switched to authorized generics (AG), often both produced and marketed by the brand company, compared to those initially switched to another generic.

Objective: Explore switching patterns of brands, AGs, and generics, switchback rates, and the potential impact of switchbacks on healthcare costs.

Methods: An analysis of the Pharmetrics Plus™ database (2007– 2019), a United States (US) payer administrative database, was conducted to examine the use of Upjohn medications available as AGs across multiple therapeutic areas. Patients initiating treatment with brand medication in the 6 months prior to generic market entry were identified and switch rates to generics and AGs, as well as switchback rates, were evaluated. Costs were descriptively compared between patients who switched back to brand and those who remained on any generic.

Results: Across 14 brand medications, more than half of the patients initiating treatment with the brand medication were switched to a generic. Generally, switching to AG, which ranged from 0.5 to 39.6%, was lower than switching to non-AG generics (16.7– 79.9%). The comparison of switchback rates from AGs to brand and non-AGs to brand showed similar results (AG:1.3– 7.5%; non-AG:1.4– 12.9%); however, the most substantial differences were observed where non-AG switchbacks were higher. Patients that switched back to brand remained on AG or generic for an average of 1– 3 months (32– 88 days). The analysis showed a tendency towards increased medical costs in the period immediately preceding switchback for all medications except sildenafil in both indications (erectile dysfunction and pulmonary arterial hypertension). For the remaining medications, medical costs ranged from $63 to $1544 higher for the switchback population. Pharmacy costs similarly tended to be higher for patients who had a switchback, with the exception of sildenafil for pulmonary arterial hypertension and sirolimus.

Conclusion: Patients receiving a brand medication are likely to be switched to a generic upon market availability. Some patients switch back to the brand medication, usually within 1– 3 months; this may be associated with increased medical costs. Additional research is needed to understand switching, its potential disruption to patients, and the role of brands, generics, and AGs.

Keywords: authorized generic, Generic, medication switching, costs

Introduction

Generic drugs comprise the same active ingredients as their brand-name products and are approved by the United States (US) Food and Drug Administration (FDA) based on the demonstration of bioequivalence to the brand-name counterpart.1 Real-world studies examining the impact of generics on patient outcomes have shown mixed results across and within therapeutic areas, suggesting a need for a more targeted vs compulsory approach to generic switching. In epilepsy, for example, the concept of “generic brittleness” has emerged whereby patients switching between antiepileptic drugs experience negative health outcomes such as increased frequency of seizure and adverse events.2–4 Other studies have shown that generic drugs have comparable efficacy as their branded counterparts.5–9

Being substantially less expensive, the use of generic drugs may reduce the economic burden on patients, cost-related medication non-adherence, and overall pharmacy costs in the healthcare system.10 Limiting dispense as written requests (eg, requests to use the brand-name product when a generic alternative is available) has the potential to reduce cost for the patients and charges to health plans.11 However, despite the increased use of generic drugs over the years, there remains a proportion of physicians and patients who remain uncertain or skeptical of generic equivalence.12–14 Some of these patients who use generics end up switching back to the original brand-name product. Nevertheless, the increased use of generics is indicative of increased receptiveness among physicians and patients.15–17

Authorized generics (AGs) are a category of generic drug that are the same in composition as the brand-name product, but may have a different color or markings.18 AGs are marketed under the same new drug application (NDA) as the brand-name product, but do not use the brand-name on the label.18 Given the important role that generic drugs have in the US health care system, studies have investigated the comparative effectiveness and switchback rates between generic drugs, including AGs, and their branded counterparts; overall comparable clinical outcomes were reported with subtle differences observed at the individual medication level.9,19 Of additional interest, Desai et al compared the switchback rates of 8 branded drug products for patients who switched from branded to AG versus those who switched from branded to non-authorized generics (non-AGs), and observed switchback rates were 28% lower for patients who switched to an AG compared with patients who switched to a non-AGs.20 This has important implications as there are no differences in prescribing, payments, or distribution between AGs and non-AGs. Switching back to the brand-name product could imply that patients or physicians may not be satisfied with the generic equivalents in certain cases, a concern which could be actual or based on perception. While, in theory no therapeutic difference is expected between AGs and non-AGs, there have been reports of tolerability issues across groups based on inert substances that are part of pharmaceutical excipients in product formulations.21–23 An analysis on the switchback period may help provide additional insights into switchbacks including when and how switchbacks may impact the healthcare system.

To date, there is a lack of evidence quantifying the economic burden during the switchback period following an initial switch to a generic. Evaluation of switchbacks to branded medication from both AGs and non-AGs may help illustrate real-world prescription differences between AGs and non-AGS as both are categorized as generic medications, but non-AGs may have minor differences in inactive ingredients and may be a different color, shape, or size than an AG or branded medication. Hence this study aimed to (1) describe the switch rate from brand-name products to the respective AGs and non-AGs, (2) describe the switchback rates from AGs and non-AGs to the brand-name products, and (3) assess the economic burden preceding an observed switchback (ie, switchback period).

Methods

Study Design

This is a retrospective database analysis conducted using the Pharmetrics Plus™ database from 2007 to 2019. The Pharmetrics Plus™ database is a commercially available, de-identified and integrated database of commercial insurers and includes all paid medical and pharmacy claims for more than 70 million members from more than 100 health plans across the US. The database comprises inpatient, outpatient, and retail and mail order pharmacy claims. Because the database is de-identified and publicly available for purchase, IRB approval was not required.

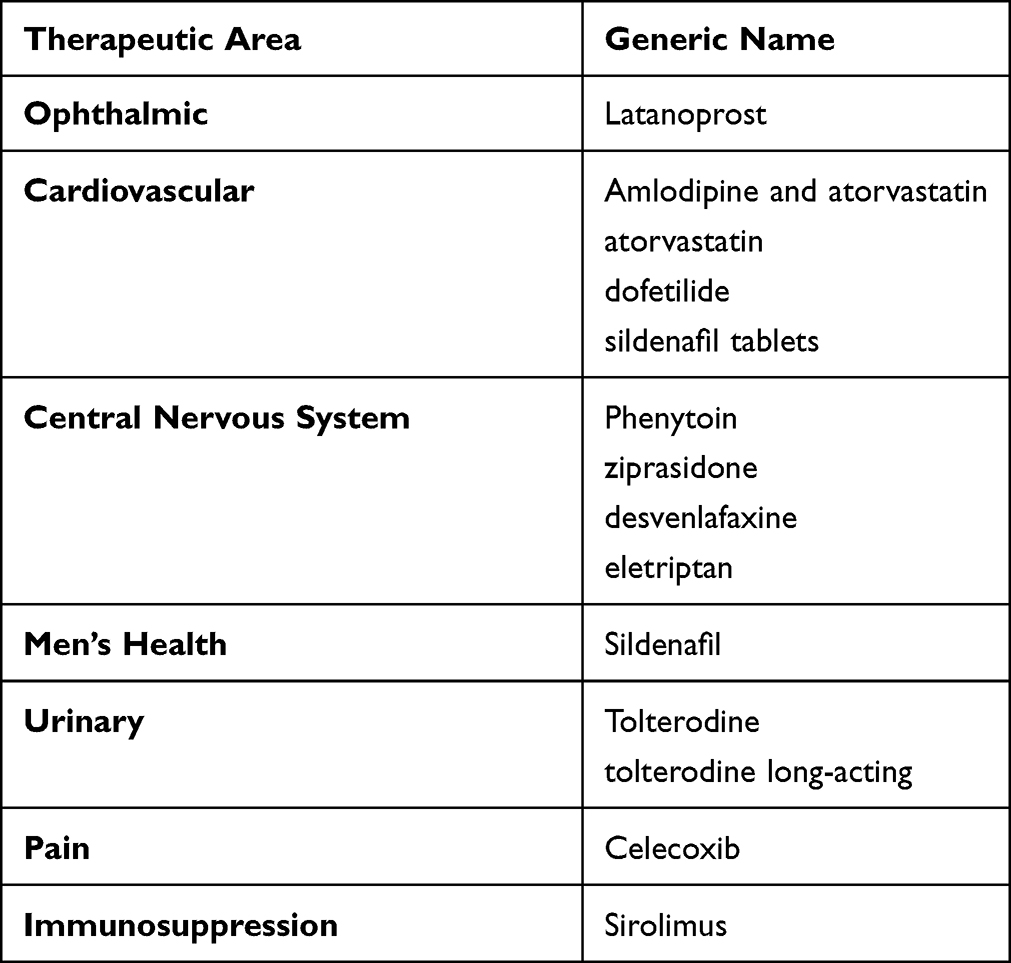

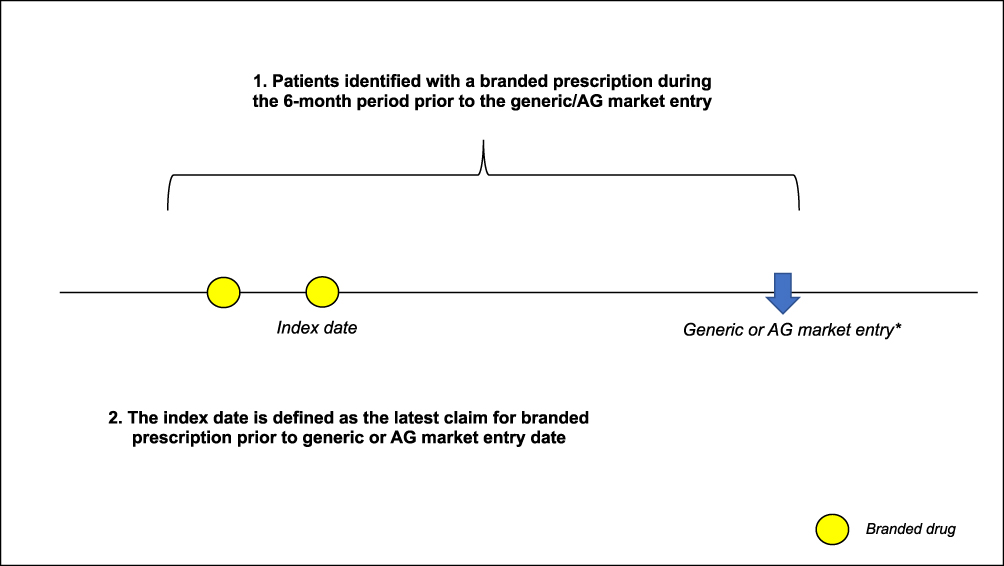

The study period was product-specific and included the period 6 months prior to the generic or AG market entry date and followed patients for 12 months after the index date, which is defined as the latest claim date for a branded prescription prior to generic market entry. We included 14 Upjohn products in this analysis (Table 1). Upjohn products were selected because the company and affiliates (Pfizer, Viatris) had a mature brand and AG business across many therapeutic areas. The study cohort comprised patients, age 18 years and older, with a claim for a brand-name product within 6 months prior to the non-AG or AG market entry (Figure 1). The earliest claim for generic use (AG or non-AG) in the database was used to proxy the generic or AG market entry date. Except for 2 products (amlodipine and atorvastatin and atorvastatin), all other products had the first claim in the database for an AG or non-AG within a 14-day window, which implies that both the AG or non-AG were concurrently available during the study timeperiod. The windows for amlodipine and atorvastatin were approximately 2 and 1 years, respectively, with AGs coming onto the market later than other generics.

|

Table 1 List of Products Evaluated in the Study |

|

Figure 1 Patient dentification. *Defined as the earliest generic or AG claim identified in the data source. Abbreviation: AG, Authorized Generic. |

Study Outcomes

After cohort identification, patients were evaluated for switching to a non-AG or AG from the brand-name product. Switchers were then followed-up to evaluate for switchback to the brand-name product, and switchback rates were compared between non-AG and AG users (Figure 2).

|

Figure 2 Study design. |

Healthcare costs were calculated during the time preceding switchback ie, switchback period (Figure 2) and this was compared to the healthcare costs incurred by the non-switchbacks (ie, people who switched from brand-name to generics and AGs and stayed on them) using a comparable time window. Costs were calculated as medical costs (summation of all reimbursed costs from hospitalizations, outpatient visits, emergency room visits, and physician office visits) and pharmacy reimbursed costs (all drugs dispensed in the switchback period). Medical costs and pharmacy costs were summed to estimate the total healthcare costs. Adherence was also evaluated during the same periods using the proportion of days covered (PDC) measure. PDC was calculated by dividing the total number of days the patient is covered by the medication by total number of days in the assessment period.

Statistical Analysis

Switch and switchback rates were calculated as the percentage of patients out of the study cohort who switched from a brand to AG or non-AG, and the percentage of patients who switched back from an AG or non-AG, respectively. All analysis in the study, including costs calculations, are descriptive in nature as it was not the intention of the study to evaluate any statistically significant differences between comparator groups.

Results

The analysis included 613,375 patients who initiated treatment with a brand medication. The sample size varied by medication and ranged from 759 patients receiving brand sildenafil to 353,504 patients receiving brand atorvastatin. The mean (SD) age of patients contributing to the analysis varied slightly by brand medication and ranged from 43.5 (14.33) for ziprasidone to 64.6 (10.60) for latanoprost. The proportion of male patients included in the analysis ranged from 11.6% for eletriptan to 72.5% for dofetilide. As expected, 99.8% of patients receiving sildenafil for men’s health were male (see Supplementary Table S1).

Switch and Switchback Rates

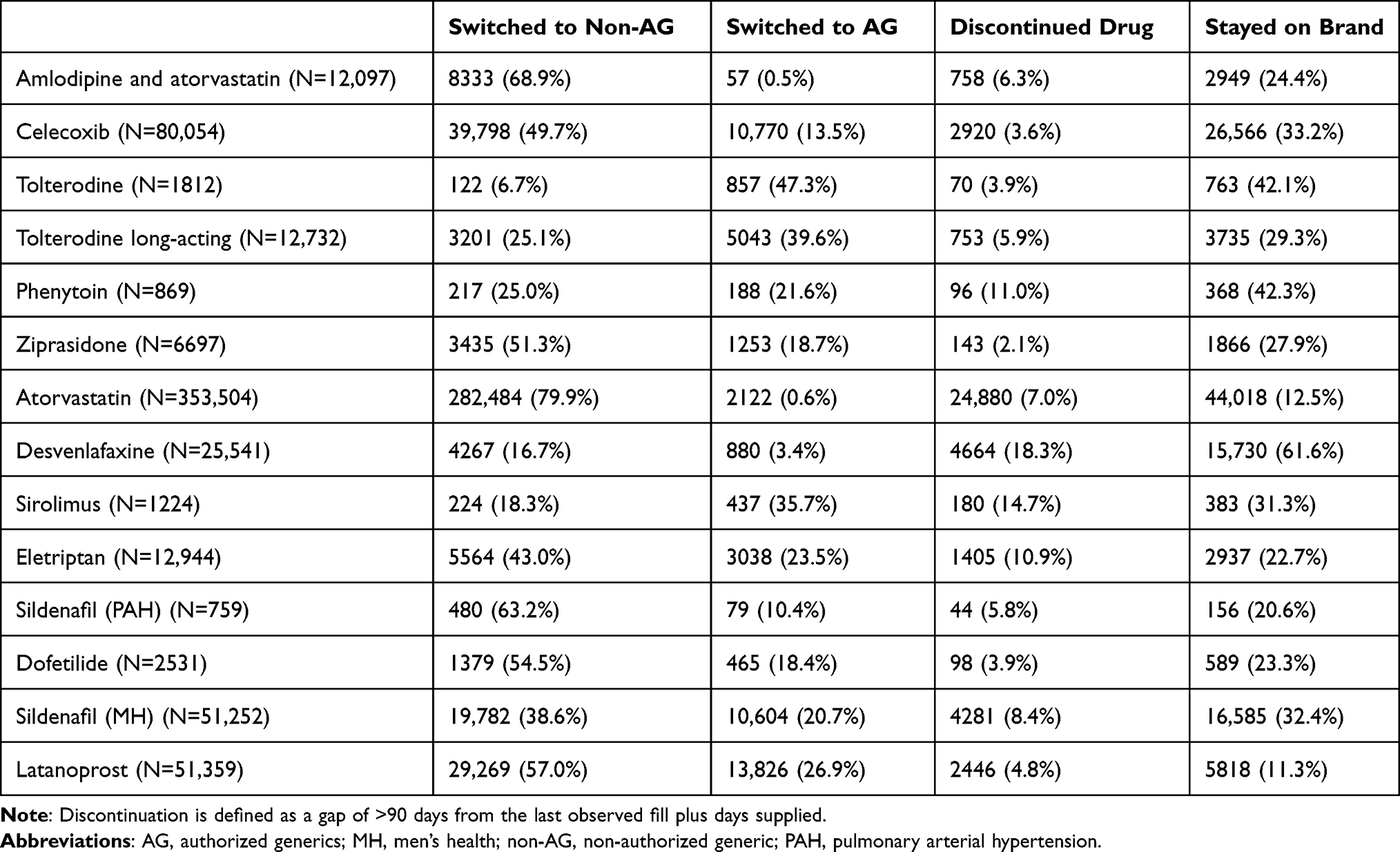

Across the 14 medications, more than half of the patients initiating treatment with a brand medication switched to an AG or non-AG (Figure 3). Generally, switching to AGs, which ranged from 0.5–39.6% was lower than switching to non-AGs (16.7–79.9%). Details on the switch rates from branded to AG or non-AG, including discontinuation rates, are presented in Table 2.

|

Table 2 Proportion of Patients Who Switched from Brand to Non-AG or AG, Discontinued Drug or Stayed on Brand |

|

Figure 3 Proportion of people who switched to authorized generics versus non-authorized generics. Abbreviations: AG, Authorized Generic; G, Generic. |

The comparison of switchback rates from AGs to brand and non-AGs to brand showed similar results with average switchback rates of 4.2% (1.3%-7.5%) for AGs compared to 4.7% (1.4–12.9%) for non-AGs. Median time to switchback was consistently around 1 month across all products evaluated, with exception of long-acting tolterodine at 2 months (Table 3). A less than 2% difference between AGs and non-AGs was observed for the majority of the products except for phenytoin and sirolimus, where the switchback rates from non-AGs had the most substantial numerical difference compared to that from the AGs (6% and 4.9%, respectively) (Figure 4). An exploratory analysis was also conducted to investigate the switch rates from AG or non-AG to brand, regardless of prior brand product exposure. We found that the switch-to-brand rates were also similar between AG and non-AG users (see Supplementary Table S2) and few patients, overall, switched to brands after receiving a generic. The proportion of patients who switched to a brand medication ranged from 0.1% to 5.7% for AGs and from 0.1% to 6.5% for non-AG users.

|

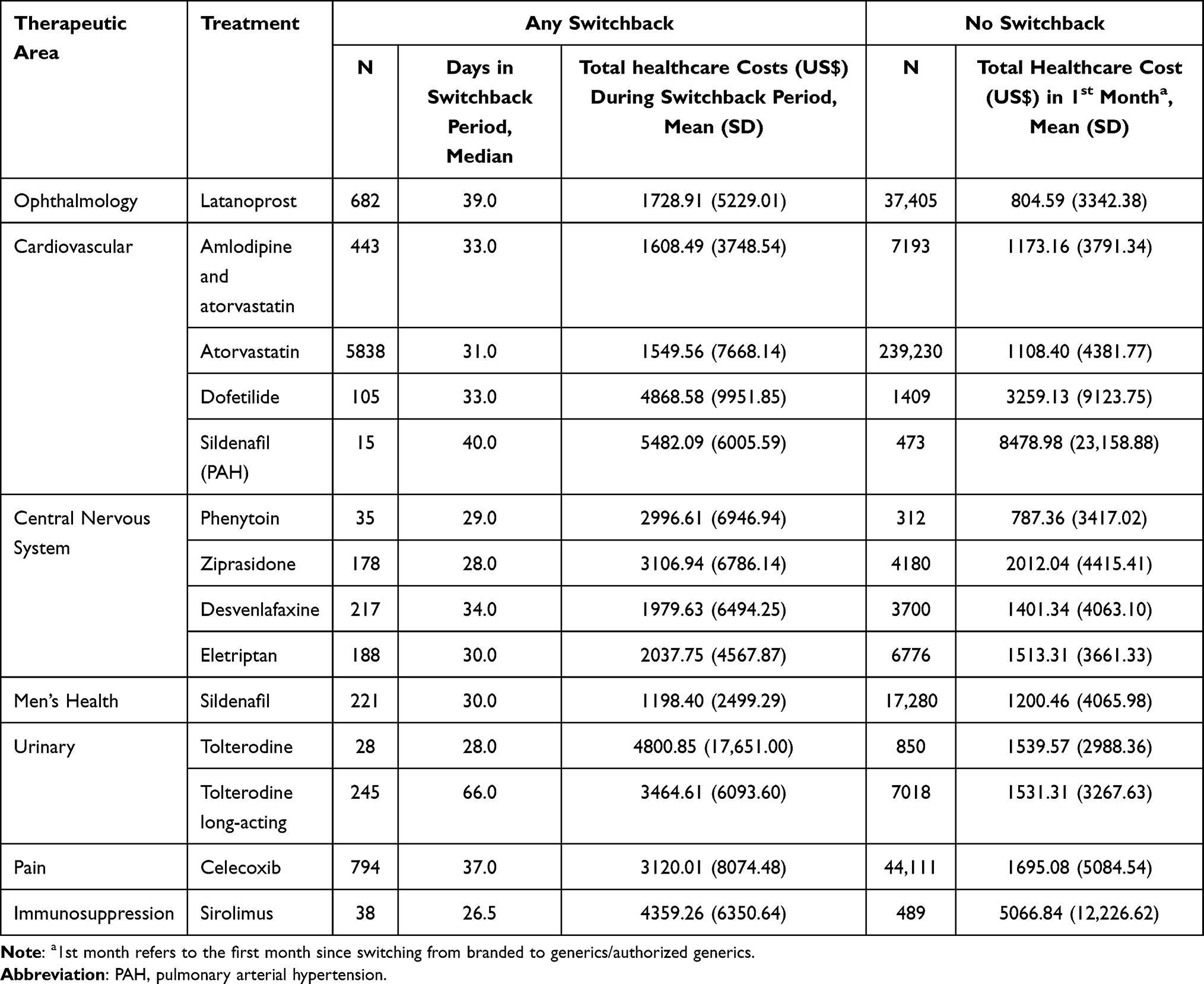

Table 3 Total Healthcare Costs (US$) Among People Who Had a Switchback versus People Without Switchback |

|

Figure 4 Difference in proportion of switchback from authorized generics and non-authorized generics to branded drug. Difference is calculated as (% of switchback from AG) – (% switchback from non-AG). Abbreviations: AG, Authorized Generic; MH, Men’s Health; non-AG, non-Authorized Generic; PAH, Pulmonary Arterial Hypertension. |

Healthcare Costs

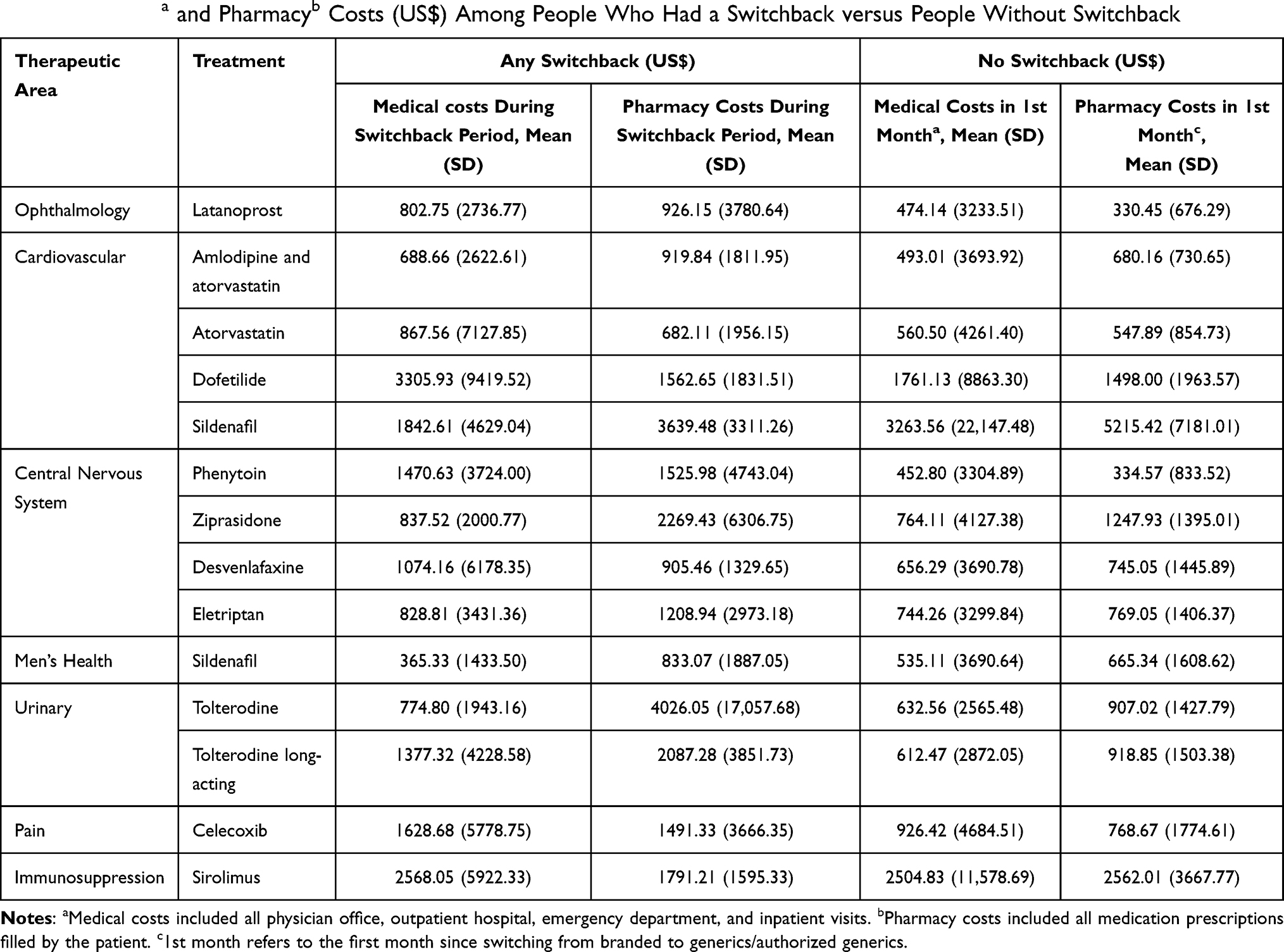

Total healthcare costs are presented in Table 3. Since the median time to switchback (ie, switchback period) was around 1 month for most products, we calculated the healthcare costs of the non-switchback patients (ie, those who remained on AG or non-AG) in the first month following their first switch from brand-name to AG or non-AG, to allow for a comparable time window. Total healthcare costs were higher during the switchback period compared to patients who remained on AG or non-AG, except for sildenafil (2 indications) and sirolimus. Total medical costs were generally higher in the switchback period compared to patients who remained on any generic (ie, AG or non-AG). Sildenafil, across both indications, was the only exception to this observed trend (Table 4). Pharmacy costs were similarly higher in the switchback period, with the exception of sildenafil for pulmonary arterial hypertension and sirolimus (Table 4). Adherence was almost always slightly lower among the patients with a switchback compared to those who remained on generics; however, it is important to note that the adherence results should consider the short duration of the switchback period (see Supplementary Table S3).

|

Table 4 Medicala and Pharmacyb Costs (US$) Among People Who Had a Switchback versus People Without Switchback |

Discussion

In this real-world observational study, we described the switch rates from 14 brand-name products to generics, AGs and non-AGs, and the switchback rates from these generics back to their respective brand-name counterparts among a pool of mostly commercially insured patients in the US. Further, we also examined the healthcare costs observed during the switchback period and a comparable period for those who did not switch back. From this analysis, we observed that a majority of the patients receiving a brand medication switched to a generic (either AG or non-AG) upon market availability and more switched to a non-AG compared to an AG. Although reasons for switching cannot be directly understood from claims data, we suspect that market supply relationships rather than deliberate choice of patients or their providers may be driving this observation. Generally, there are multiple non-AGs available for a given medication through various manufacturers for which a patient might be switched to at the pharmacy compared to AGs. Additionally, pharmacists do not typically discuss differences between AGs and non-AGs with their patients and rather inform patients of their equal therapeutic value, providing another possible reason for greater switching to non-AGs when coupled with non-AGs’ lower prices. Switchback rates from non-AGs and AGs are demonstrated to be generally similar in this study, except for drugs with narrow therapeutic index (eg, phenytoin and sirolimus). Patients who switch-back to the brand-name product typically do so within 1 month (and up to 2 months for long-acting products) of receiving a generic product. This could for instance be due to a nocebo effect where patients expect negative outcomes from generic use, which could in turn lead to reduced (or perceived reduced) efficacy and tolerability.24 However, understanding specific reasons for switchback requires further investigation of patient and provider preferences and decision-making as well as the possible impact of potential differences between products, such as changes in pill appearance, on switchbacks.

Hansen et al compared the switch rates for 10 drugs (alendronate, amlodipine, citalopram, gabapentin, glimepiride, losartan, metformin extended-release, paroxetine, sertraline and simvastatin) using electronic health records from a regional US healthcare system and observed a 4.8% overall switchback rate to branded medication.19 This is similar to the 4–5% average switchback rates observed with our study. Similar to what Hansen et al reported, we also observed fairly similar switchback rates from AG and non-AGs.19 However, our findings demonstrated that for certain drugs with a narrow therapeutic index (NTI) such as phenytoin and sirolimus, the switchback rate is lower from AG compared to non-AG. A survey of 606 physicians reported that almost half of them were extremely/very likely to request that a brand-name anti-epileptic not be substituted with a generic.25 The same survey also observed that three-quarters of the physicians perceived concerns with the efficacy of generic anti-epileptics.25 Hence, it is not surprising that our results demonstrated that phenytoin, an anti-epileptic with a NTI, has the largest difference in switchback rates from the AG compared to non-AG, where switchback from AG is 6% less than that from an non-AG. Further, NTI medications, including immunosuppressants such as sirolimus, require close clinical and therapeutic drug monitoring when converting to its generic formation,26 and thus, this could potentially explain why the rate of switching to a AG is higher compared a non-AG, and the switchback rate from an AG is likewise lower in this case.

Desai et al conducted a larger observational cohort study to compare switchback rates to brand medications from AG and non-AG for 8 drug products. The observed overall switchback rate was 8.2 per 100 persons across all drug products and ranged from 3.8–17.8 depending on the product being examined. Observed switchback rates were generally lower for patients switching from brand to AG (pooled hazard ratio 0.72, 95% confidence interval 0.64–0.81).20 The authors highlight that the observed differences in switchback rates between AGs and generic products are unlikely to be fully explained by differences in quality, safety, or efficacy; they may be related to negative perceptions of generic drugs. Since the AG is generally similar in appearance to its brand-name counterpart and is manufactured by the same manufacturer, there might be less perception bias associated with the AG as compared to its non-AG counterpart in patients originally receiving the brand. The overall switchback rates reported by Desai et al are higher than what we observed, however similar to Desai, we found that the largest differences in switchback rates between AGs and non-AGs favored AGs, suggesting that for specific medications (eg, phenytoin and sirolimus), some patients may be more likely to switch back to a brand from a non-AG compared to an AG. Generally, the observed difference in switchback rates for AGs compared to non-AGs was less than 2%, suggesting minimal differences between the two types of generic medicines. The differences observed between this study and the previously reported results from Desai et al may be driven by differences in therapeutic areas, products assessed, and overall study methodology.

In addition to previous literature focusing on the switch and switchback rates among brand, AG and non-AG products, our study further examined the costs incurred during the switchback period compared to a similar time window for those patients who did not switch back ie, remained on the generic. It appeared that total healthcare costs were generally higher during the period preceding switchback compared to patients who remained on generic, suggesting that patients who ultimately switch back to brand require some additional healthcare resources. The higher healthcare costs were driven mainly by non-inpatient (outpatient, physician office and emergency room) healthcare utilization (results not shown). Further research is warranted to better understand the healthcare resource utilization and costs incurred during the period preceding switchback. For example, whether the increase in health care resource use may be due to perception bias or actual issues of efficacy and safety, and if these differ by products from different therapeutic classes requires further exploration. Furthermore, multivariate analyses can be explored to evaluate if the differences in healthcare resource utilization between people who switchback to branded medication or not is driven by patient characteristics such as age and comorbidities that may increase the severity of disease and affiliated costs.27,28

Results from this study should be interpreted in light of several limitations. First, given that this is a preliminary exploratory analysis of selected Upjohn products and therapeutic areas, there are several potential reasons for switchback that could not be explored within the scope of this study. While it was assumed that AGs and non-AGs are equally accessible to patients, individual pharmacies or insurance plans may promote certain AGs or non-AGs over others, thus becoming a possible reason for switching. However, it was not feasible within this study to review distribution patterns within individual pharmacies or plans, limiting the analysis of product availability on switch behavior. Additional switchback reasons like patient preference and clinical effectiveness were also unable to be analyzed given the limits of a claim database analysis. Second, due to sample size limitations, we were unable to compare healthcare costs of patients who switched-back from a non-AG versus an AG. We were also unable to compare costs between different generic suppliers, and between pre- and post-switchback, which would help explain what is driving the high costs among patients who switchback. We surmise that patient characteristics such as clinical instability and distrust in generics, which result in increased medical claims and pharmacy costs, are a possibility, providing an avenue for further investigation. Third, the products chosen and data does not allow for evaluation of what happens during the immediate period of generic exclusivity when only the brand, AG, and a single other generic are on the market. Fourth, some bias may exist in the reporting of results given the authors’ affiliation with the pharmaceutical company that markets and sells the Upjohn products explored in this study. Therefore, the results are conditional on this affiliation and should be interpreted accordingly. Despite these limitations, the data are generalizable to the commercially and self-insured employer population in the United States.

Conclusion

Patients receiving a brand medication are likely to be switched to a generic upon market availability and it appears that patients are more often switched to a non-AG than an AG. Notably, not all patients remained on the AGs or non-AGs, and some of them switchback to the brand-name products. This exploratory analysis is suggestive of increased healthcare utilization and costs in the period preceding switchback. Previous studies have concluded that interventions that reduce switchbacks may allow for major costs savings.17 Additional research is needed to understand switching patterns, its potential disruption to patients, and the role of brands, generics, and AGs on differential switching behaviors, in order to implement such interventions.

Funding

Funding for this research was provided by Upjohn, a previous division of Pfizer, now part of Viatris and the makers of authorized generics.

Disclosure

Dr Justine Alderfer is an employee of Pfizer Inc, and holds stock from Pfizer Inc and Viatris, Inc. Ms Jyoti Aggarwal was an employee of OPEN Health at the time of research. Dr Kim Gilchrist is an employee and stockholder of Pfizer Inc. Dr Jose Maria Jimenez Alvir is an employee and stockholder of Pfizer Inc and Viatris, Inc. Dr Joseph Cook is an employee of Viatris, Inc and hold stocks from Pfizer Inc and Viatris, Inc. Ms Sang Hee Park was an employee of OPEN Health at the time of the research. Dr Jennifer M Stephens is an employee and shareholder of OPEN Health. OPEN Health received research funding from Upjohn to conduct the research. The authors report no other conflicts of interest in this work.

References

1. Mulhall JP, Giraldi A, Hackett G, et al. The 2018 revision to the process of care model for management of erectile dysfunction. J Sex Med. 2018;15(10):1434–1445. doi:10.1016/j.jsxm.2018.05.021

2. Das S, Jiang X, Jiang W, Ting TY, Polli JE. Relationship of antiepileptic drugs to generic brittleness in patients with epilepsy. Epilepsy Behav. 2020;105:106936. doi:10.1016/j.yebeh.2020.106936

3. Chaluvadi S, Chiang S, Tran L, Goldsmith CE, Friedman DE. Clinical experience with generic levetiracetam in people with epilepsy. Epilepsia. 2011;52(4):810–815. doi:10.1111/j.1528-1167.2011.03025.x

4. Lang JD, Kostev K, Onugoren MD, et al. Switching the manufacturer of antiepileptic drugs is associated with higher risk of seizures: a nationwide study of prescription data in Germany. Ann Neurol. 2018;84(6):918–925. doi:10.1002/ana.25353

5. Corrao G, Soranna D, Arfe A, et al. Are generic and brand-name statins clinically equivalent? Evidence from a real data-base. Eur J Intern Med. 2014;25(8):745–750. doi:10.1016/j.ejim.2014.08.002

6. Corrao G, Soranna D, Merlino L, Mancia G. Similarity between generic and brand-name antihypertensive drugs for primary prevention of cardiovascular disease: evidence from a large population-based study. Eur J Clin Invest. 2014;44(10):933–939. doi:10.1111/eci.12326

7. Jackevicius CA, Tu JV, Krumholz HM, et al. Comparative effectiveness of generic atorvastatin and lipitor® in patients hospitalized with an acute coronary syndrome. J Am Heart Assoc. 2016;5(4):e003350. doi:10.1161/JAHA.116.003350

8. Kesselheim AS, Misono AS, Lee JL, et al. Clinical equivalence of generic and brand-name drugs used in cardiovascular disease: a systematic review and meta-analysis. JAMA. 2008;300(21):2514–2526. doi:10.1001/jama.2008.758

9. Desai RJ, Sarpatwari A, Dejene S, et al. Comparative effectiveness of generic and brand-name medication use: a database study of US health insurance claims. PLoS Med. 2019;16(3):e1002763. doi:10.1371/journal.pmed.1002763

10. Briesacher BA, Andrade SE, Fouayzi H, Chan KA. Medication adherence and use of generic drug therapies. Am J Manag Care. 2009;15(7):450–456.

11. Shrank WH, Liberman JN, Fischer MA, et al. The consequences of requesting ”dispense as written”. Am J Med. 2011;124(4):309–317. doi:10.1016/j.amjmed.2010.11.020

12. Kesselheim AS, Gagne JJ, Franklin JM, et al. Variations in patients’ perceptions and use of generic drugs: results of a national survey. J Gen Intern Med. 2016;31(6):609–614. doi:10.1007/s11606-016-3612-7

13. Shrank WH, Cox ER, Fischer MA, Mehta J, Choudhry NK. Patients’ perceptions of generic medications. Health Aff. 2009;28(2):546–556. doi:10.1377/hlthaff.28.2.546

14. Kesselheim AS, Gagne JJ, Eddings W, et al. Prevalence and predictors of generic drug skepticism among physicians: results of a national survey. JAMA Intern Med. 2016;176(6):845–847. doi:10.1001/jamainternmed.2016.1688

15. Dunne SS, Dunne CP. What do people really think of generic medicines? A systematic review and critical appraisal of literature on stakeholder perceptions of generic drugs. BMC Med. 2015;13(1):173. doi:10.1186/s12916-015-0415-3

16. Hassali MAA, Shafie AA, Jamshed S, Ibrahim MIM, Awaisu A. Consumers’ views on generic medicines: a review of the literature. Int J Pharm Pract. 2009;17(2):79–88. doi:10.1211/ijpp/17.02.0002

17. Dunne SS. What do users of generic medicines think of them? A systematic review of consumers’ and patients’ perceptions of, and experiences with, generic medicines. Patient. 2016;9(6):499–510. doi:10.1007/s40271-016-0176-x

18. FDA List of authorized generic drugs. Available from: https://www.fda.gov/drugs/abbreviated-new-drug-application-anda/fda-list-authorized-generic-drugs.

19. Hansen RA, Qian J, Berg R, et al. Comparison of generic-to-brand switchback rates between generic and authorized generic drugs. Pharmacotherapy. 2017;37(4):429–437. doi:10.1002/phar.1908

20. Desai RJ, Sarpatwari A, Dejene S, et al. Differences in rates of switchbacks after switching from branded to authorized generic and branded to generic drug products: cohort study. BMJ. 2018;361:k1180. doi:10.1136/bmj.k1180

21. Zarmpi P, Flanagan T, Meehan E, Mann J, Fotaki N. Biopharmaceutical aspects and implications of excipient variability in drug product performance. Eur J Pharm Biopharm. 2017;111:1–15. doi:10.1016/j.ejpb.2016.11.004

22. Page A, Etherton-Beer C. Choosing a medication brand: excipients, food intolerance and prescribing in older people. Maturitas. 2018;107:103–109. doi:10.1016/j.maturitas.2017.11.001

23. Latwal B, Chandra A. Authorized generics vs. branded generics: a perspective. J Generic Med. 2021;17(1):5–9. doi:10.1177/1741134320947773

24. Bingel U. For the placebo competence T. Avoiding Nocebo effects to optimize treatment outcome. JAMA. 2014;312(7):693–694. doi:10.1001/jama.2014.8342

25. Berg MJ, Gross RA, Haskins LS, Zingaro WM, Tomaszewski KJ. Generic substitution in the treatment of epilepsy: patient and physician perceptions. Epilepsy Behav. 2008;13(4):693–699. doi:10.1016/j.yebeh.2008.06.001

26. Johnston A. Equivalence and interchangeability of narrow therapeutic index drugs in organ transplantation. Eur J Hosp Pharm Sci Pract. 2013;20(5):302. doi:10.1136/ejhpharm-2012-000258

27. Tamblyn R, Eguale T, Huang A, Winslade N, Doran P. The incidence and determinants of primary nonadherence with prescribed medication in primary care: a cohort study. Ann Intern Med. 2014;160(7):441–450. doi:10.7326/M13-1705

28. Roebuck MC, Liberman JN, Gemmill-Toyama M, Brennan TA. Medication adherence leads to lower health care use and costs despite increased drug spending. Health Aff. 2011;30(1):91–99. doi:10.1377/hlthaff.2009.1087

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.