Back to Journals » ClinicoEconomics and Outcomes Research » Volume 17

Willingness of Urban Formal Sector Workers to Support a Community-Based Health Insurance Scheme in Ethiopia

Authors Mebratie AD ![]() , Shamebo D

, Shamebo D ![]() , Alemu G, Shigute Z, Bedi AS

, Alemu G, Shigute Z, Bedi AS

Received 14 May 2025

Accepted for publication 20 August 2025

Published 28 August 2025 Volume 2025:17 Pages 601—613

DOI https://doi.org/10.2147/CEOR.S533996

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Professor Samer Hamidi

Anagaw Derseh Mebratie,1 Dessalegn Shamebo,2 Getnet Alemu,3 Zemzem Shigute,4,5 Arjun S Bedi6

1School of Public Health, Addis Ababa University, Addis Ababa, Ethiopia; 2Department of Development Economics, Ethiopian Civil Service University, Addis Ababa, Ethiopia; 3Institute of Development and Policy Research and Center for Rural Development, College of Development Studies, Addis Ababa University, Addis Ababa, Ethiopia; 4 International Institute of Social Studies, Erasmus University Rotterdam, Rotterdam, The Netherlands; 5Institute of Development and Policy Research, Addis Ababa University, Addis Ababa, Ethiopia; 6International Institute of Social Studies, Erasmus University, Rotterdam, The Netherlands

Correspondence: Anagaw Derseh Mebratie, School of Public Health, Addis Ababa University, P. O. Box: 9086, Addis Ababa, Ethiopia, Tel +251 944121769, Email [email protected]

Introduction: The Ethiopian health system is largely financed through household out-of-pocket payments and external donor support, increasing the risk of catastrophic health expenditures. To address these challenges, the government introduced two health insurance schemes: Community-Based Health Insurance (CBHI) targeting the informal sector and a still to be implemented Social Health Insurance (SHI) scheme for the formal sector. Although designed to operate separately, the long-term goal is to integrate them into a unified national risk pool. Achieving this integration requires cross-group solidarity, especially as formal sector employees may subsidize CBHI. This study investigates the willingness of formal sector workers to support CBHI, which is critical for long-term financial sustainability in the Ethiopian health insurance landscape.

Methods: The paper is based on a survey of 1,919 formal sector workers and pensioners in major administrative regions of Ethiopia. A survey-based experiment was used to elicit support for CBHI. Respondents were randomly assigned to one of five cases that varied by the information provided on CBHI subsidies and benefits. Descriptive statistics and logit models were used to analyze willingness to support CBHI.

Results: There is strong support from urban formal sector employees for the CBHI. Regardless of the scenario presented, after adjusting for non-response, at least 66% of participants supported the scheme. Regional variations were observed, and knowledge of health insurance was positively associated with support. Existing access to formal insurance was linked with lower support.

Discussion: Strong evidence of solidarity among formal sector workers bodes well for further expansion of the CBHI. Despite supporting CBHI, formal sector employees are resisting SHI due to cost concerns and skepticism about its benefits, unlike CBHI’s known outcomes. SHI resistance signals the need for targeted communication and trust-building as the country moves toward achieving universal health coverage.

Keywords: health insurance schemes, insurance premiums, cross-subsidization, solidarity, Ethiopia

Introduction

In the past two decades, Ethiopia has made considerable progress in expanding health infrastructure and reducing child and maternal mortality rates. For instance, primary healthcare service coverage, as measured by access to a healthcare facility within a two-hour walk, increased from 51% in 2000 to greater than 90% in 2019.1,2 Ethiopia is one of the few Sub-Saharan African countries which achieved the Millennium Development Goal (MDG) of reducing its under-five child mortality rate which fell from 123 per 1,000 livebirths in 2000 to 46 per 1,000 live births by 2015.3 The country’s maternal mortality rate (MMR) has fallen from 953 in 2000 to 267 in 2020.4 This is a decline that is attributed to the use of low-cost interventions such as the provision of health extension services.5 The country has also been successful at reducing the prevalence of malaria and tuberculosis. For example, between 2000 and 2019, the number of malaria cases fell from 5.6 million to 1.8 million, and the incidence of tuberculosis fell from 400 cases to 140 cases per 100,000 people.6–8

Despite such stellar progress, utilization of health care remains limited. For instance, in 2022, there were 1.09 outpatient visits per capita while the WHO recommendation is between two and three out-patient visits per capita.3,9 Moreover, the country’s health system remains dependent on external donors and out-of-pocket health expenditure is substantial. In 2019–2020 about 33.5% of the health budget was covered by international donors and 30.5% of the budget was covered by individuals in the form of user fees.2 Dependency on international assistance raises the possibility that funds may not be released in a timely manner or when there are shocks that require immediate interventions.10–12 At the same time, reliance on out-of-pocket health payments leads to catastrophic health expenditure which has impoverishing effects such as depletion of productive assets, reduction in consumption, forgone human capital investment.13–16

Since 2008, to address these issues and specifically to mobilize domestic resources to finance healthcare and expand access to quality care, the Ethiopian government introduced several healthcare financing reforms.17 One of the components of these reforms was the introduction of pre-payment insurance schemes. Specifically, a voluntary CBHI scheme for the informal sector and a still to be implemented, mandatory SHI scheme for the formal sector. In 2011, a pilot CBHI scheme was rolled out in 13 selected districts. By 2023, it had expanded to 1,011 districts and towns, covering approximately 87.4% of the districts and town administrations in the country and reaching about 12.1 million households—equivalent to 78% of the eligible households in the pilot districts.18

As compared to other Sub-Saharan African countries, the scheme has been successful.19,20 Impact evaluation studies show that the scheme has enhanced access to healthcare services and reduced the incidence of borrowing.21,22 While the scheme does not provide complete financial protection as households still have to pay for healthcare services due to limited knowledge of scheme design or lack of drug or laboratory equipment at health facilities, it has certainly alleviated the financial burden.20

The value of the CBHI may be witnessed by the willingness to pay (WTP) for health insurance in rural Ethiopia. Such studies have shown WTP rates ranging from 65% to 78%, with average annual contributions ranging between 233 and 256 ETB.23,24 In contrast, urban formal sector workers are reluctant to pay for the SHI. For instance, a recent study in Addis Ababa found that while 67% supported the introduction of the SHI, only 24% were willing to pay the proposed premium of 3% of income.25 Similarly, in Dessie City in Northern Ethiopia, only 29.6% of civil servants expressed willingness to pay for the SHI.26

While these findings suggest a much lower interest in contributing to insurance schemes in urban areas compared to rural areas, the continued scaling up of the CBHI requires strong and continued political and financial support from the government. Consistent with the basic insurance principle of risk pooling whereby larger risk pools enhance scheme sustainability, the long-term aim of the government is to combine the CBHI and the still to be introduced SHI.27 This arrangement is expected to spread risk, enable cross-subsidization of financial resources from the formal to the informal sector and ensure sustained access to health care regardless of socio-economic status.28–30 Given the expected financial burden on the formal sector, a prerequisite for combining the two health care insurance schemes is solidarity across the two groups targeted by the schemes. Accordingly, this study aims to assess the extent to which formal sector employees are willing to support the CBHI.

To realize its objectives, a survey of 1,919 formal sector employees and pensioners residing in the major administrative regions of the country was conducted. A survey experiment was used to elicit support for the CBHI scheme. Respondents were randomly allocated to one of five cases. These cases differed in terms of the information provided on the source of the CBHI subsidy and the benefits associated with it. After receiving information, respondents were asked to signal their level of support for the scheme.

To preview our results, we find that there is strong support from urban formal sector employees for the CBHI scheme. Regardless of the scenario presented, and despite some regional variation, the key result is that even after adjusting for 13% non-response, about 66% of the surveyed participants supported the CBHI scheme. Such a high level of support suggests that, when the time comes, it should be possible to combine the two schemes without substantial friction. Such evidence is clearly useful in informing the efforts of the government and the EHIS as they strive to meet the country’s goal of developing a sustainable health insurance system.

The Design of Health Insurance Schemes in Ethiopia – A Brief Description

In 2008, in collaboration with development partners, the Ethiopian Federal Ministry of Health prepared a health insurance strategy to establish two types of health insurance schemes. These were a CBHI scheme to cater for rural and informal sector workers in urban centers and a SHI scheme for formal sector employees and pensioners. International experience and local feasibility studies informed scheme design. Subsequently, the CBHI was piloted in 13 districts in 2011 and the scheme was evaluated in 2013.31 Based on the evaluation, the initial design of the scheme was revised and it was scaled up in 2016. The basic design features of the Ethiopian CBHI and SHI are described below.

Community Based Health Insurance Scheme

The CBHI is a voluntary health insurance scheme offered to rural workers and informal sector workers in urban areas. While district and regional governments are responsible for the implementation and administration of the CBHI schemes, community members are involved in management and evaluation. Specific tasks for community members include community mobilization, premium collection, membership renewal and scheme monitoring.

Enrolment in the scheme is only possible at the household level and includes coverage for core family members (wife, husband, and children under 18). Other household members may be covered based on additional payment. At inception, the premium amount and the frequency of payment was sensitive to local contexts and varied across regions. However, since 2017, greater uniformity has been imposed and the premium also varies depending on household size. In rural areas, depending on household size, the annual premium amounts to between ETB 800 and ETB 1100 per annum and in urban areas between ETB 900 and ETB 3500.32 While the monthly contribution may be considered modest as compared to the expected benefits, the scheme still includes a fee waiver system for indigent groups – up to 10% of the eligible households in a district may enroll in the scheme as fee waiver beneficiaries. To enhance financial sustainability and retain affordability, the federal government provides a general subsidy to support the CBHI. Since 2015 this subsidy was reduced from 25% to 10% of the total premiums collected by the CBHI scheme.33–35 While the bulk of the schemes pool risk at the district level, in some parts of the country risk is pooled at a higher level of aggregation.

Enrolled members and their families are entitled to inpatient and outpatient care from public sector health facilities.36,37 There are no deductibles and co-payments and payment is not required at point-of-use. Care at private health facilities and medical treatment abroad is not covered. The scheme follows a gatekeeper system and scheme members first need to visit the nearest health center and subsequently they may be referred to tertiary care facilities. The benefit package excludes health services such as those related to drug abuse, traffic accidents, occupational injuries, cosmetic surgeries, organ transplants, eyeglasses, and contact lenses. The scheme does not provide financial coverage for treatment of injuries resulting from social unrest and natural disasters.36,37

Social Health Insurance Scheme

The legal and administrative aspects of the SHI scheme have been established, and the Ethiopian Health Insurance Service (EHIS) has been created to manage the scheme.36 Operational documents have been prepared, and in 2014, the EHIS – agency established to manage the schemes – setup branch offices in selected towns.33,36,37

Despite all the background preparations, the scheme has not yet been implemented. While the actual policy may differ from the initial design, at the moment, the proposed SHI is expected to be introduced in one go and enrolment is mandatory for all formal sector (private, public, NGO, pensioners) employees. The SHI proclamation sets the premium at 6% of an employees’ gross salary and requires an equal contribution (3% each) from both the employee and the employer. For pensioners, the premium is set at 2% of their pension amount with 1% to be covered by the pensioner and a government contribution of 1%.36,38 The benefit package is the same as in the case of the CBHI, that is, enrolled members and their families are entitled to inpatient and outpatient care from public sector health facilities.37,39

While scheme launch has often seemed imminent, it has been delayed, mainly for two reasons. First, formal sector employees have expressed their unwillingness to pay the proposed SHI premium. Although there are no national-level studies, formal willingness to pay (WTP) studies conducted on various samples of civil servants in Addis Ababa show that between 17% and 35% of the sampled respondents are willing to pay the premium with a mean WTP ranging between 1.5% and 2.5% of gross monthly salaries.25 A meta-analysis covering 18 studies showed that, on average, about 42% of formal sector workers are WTP for SHI.40 The second reason for the delay is the scheme’s healthcare coverage. The scheme is likely to restrict coverage to public health facilities rather than covering potentially higher quality private care. This restriction is likely to drive up the costs of health care as it requires SHI enrollees to pay the premium and yet they may continue to seek care at private health facilities. A recent paper on healthcare seeking behavior of formal sector workers shows that restricting access to public health facilities is at odds with the healthcare seeking behavior of formal sector employees, especially for outpatient care.25

Material and Methods

Data

This paper is based on a retrospective cross-sectional survey conducted in-person between June and July 2016. The survey was canvassed in four of the country’s main cities. These included Addis Ababa – the country’s capital, Bahir Dar, the largest city in the Amhara region, Hawassa, the largest city in the SNNP region, and Mekelle, the largest city in the Tigray region. These cities were purposively selected as they accounted for 20% of the estimated 4.3 million formal sector employees in the country. To obtain a representative sample and include those targeted by the SHI, the survey covered five categories of employees – civil servants, public sector enterprise employees, private sector workers, NGO workers, pensioners (former civil servant and public sector enterprise workers) and the distribution of the sample across cities and type of formal sector employees was determined based on the distribution of the population of formal sector workers in these cities. Population-level information was obtained from the Ethiopian Ministry of Civil Service, the Central Statistical Agency, the Ethiopian Chamber of Commerce and Sectorial Associations, and the Ethiopian social security agency. Considering the budget, a sample size of 2,100 respondents was targeted.25

After ensuring that a selected respondent was willing to participate in the survey, enumerators gathered individual and household-level information. The survey contained a household roster which gathered socio-economic information on all household members, their health status and lifestyle choices, outpatient and inpatient health care utilization, financing of heath care, understanding of health insurance and whether they currently had any form of health insurance. Specifically, for the purposes of the current paper, a survey-based experiment was used to gather information on respondent support or lack thereof for the CBHI. Details are provided in the subsequent section.

In total, while a little less than the targeted figure, the survey was able to cover 1,919 respondents distributed across the four cities and five types of employees. As shown in Supplementary Table 1, the distribution of the sample across types of employees is very similar to their distribution in the population. While not perfect, arguably the sample is representative of formal sector employees in urban Ethiopia.

Support for the CBHI Amongst Formal Sector Employees – A Survey-Based Experiment

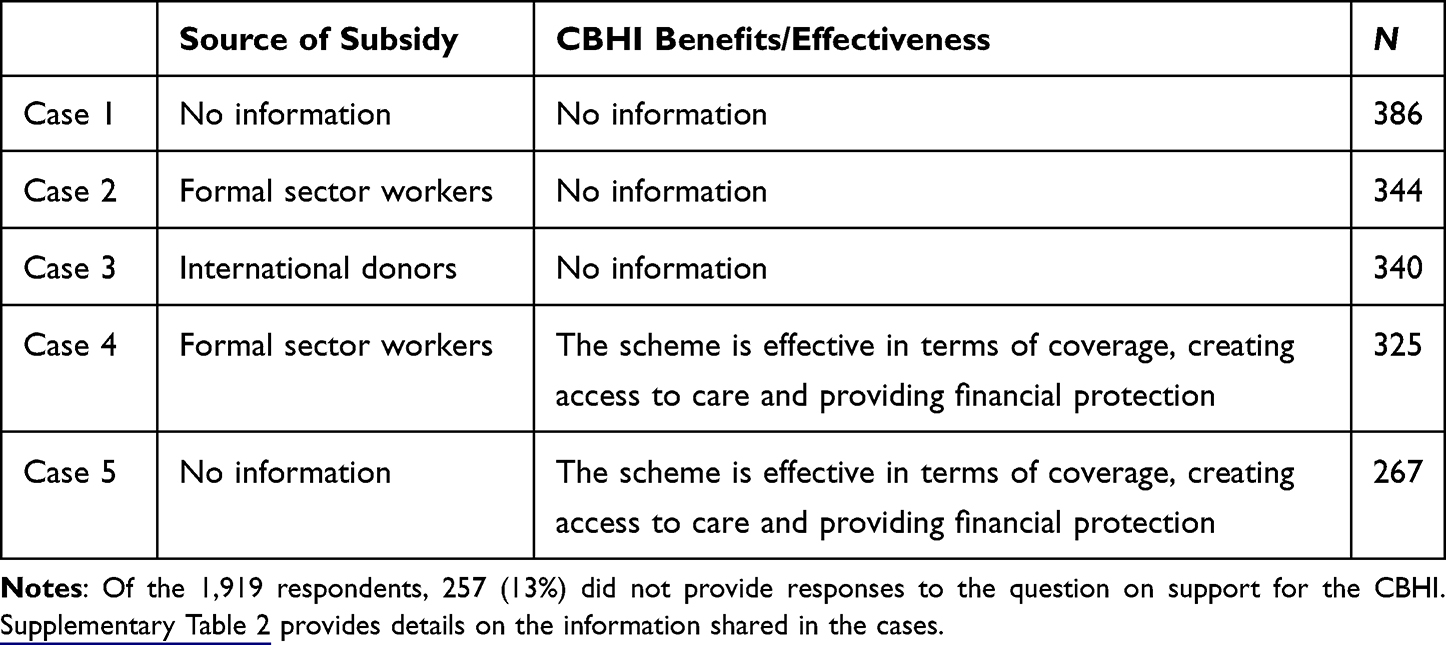

To elicit support for the CBHI amongst formal sector employees, the paper relies on a survey-based experiment. Survey respondents were randomly assigned to one of five different cases. Each case had two questions (see Table 1 and Supplementary Table 2). The first question in each case was whether respondents had heard of the CBHI scheme. The second question, which was posed after providing information on different ways of subsidizing the CBHI and/or providing information on benefits accruing due to the CBHI, asked respondents whether they opposed or supported the scheme using a five-point Likert scale. To guard against “cheap talk”, those who stated that they (strongly) supported the CBHI scheme were asked to sign a slip of paper to confirm their level of commitment endorsing continued government support of the CBHI scheme.

|

Table 1 Alternative Scenarios Presented to Survey Respondents |

As displayed in Table 1 and in more detail in Supplementary Table 2, the first case did not provide any information but simply asked respondents whether they support the CBHI scheme (baseline case). The second case explicitly stated that the cost of subsidizing the scheme would be borne by those working in the formal sector. The third case stated that the subsidy would be covered by international donors. The fourth case indicated that the subsidy would be covered by taxpayers but provided research-based information on scheme effectiveness in terms of enhancing access to health care and reducing OOP health expenditure. The final case did not contain any information on how the subsidy would be financed but provided the same information on scheme effectiveness as in case four.

As compared to the baseline case, the expectation is that support for the CBHI scheme or in other words, solidarity with rural and informal sector workers, will be lower when it is explicitly pointed out that formal sector workers subsidize the CBHI (Case 2) and higher as compared to the baseline case when the subsidy is financed by external sources (Case 3). The lower support for the CBHI scheme (Case 2) is expected to be ameliorated when research-based information is provided on the effectiveness of the scheme (Case 4). Support for CBHI in Case 5 is expected to be higher than the baseline. The rationale for the variations across cases is based on the main concerns highlighted in Section 2, that is, maintaining and enhancing the affordability of the CBHI requires continued government financial support and at the same time there is skepticism on the quality and usefulness of the health services which may be availed through the CBHI and eventually through the SHI.

As mentioned above, each of the respondents was randomly assigned to only one of the cases. Due to this randomization, there is no reason to expect that the sociodemographic and other traits of respondents differ across the five cases. Therefore, it should be possible to identify the effect of the variations in the cases on the level of support for the CBHI. In other words, while the sociodemographic traits of respondents may influence their support for the CBHI, their traits are not likely to influence the effect of the cases on support for the CBHI. Formal statistical tests clearly show that the profiles of the study participants do not differ across the five cases (Supplementary Table 3).

Methods

We use descriptive statistics to provide information on the sample respondents and to examine their understanding of health insurance. Subsequently, we probe whether respondents have heard of the CBHI and their level of support for the scheme. Finally, we examine willingness to support the scheme as a function of the characteristics of the case offered. To do so we estimate binary logit models (support, do not support) and an ordered logit model where the outcome variable has four options (strongly opposed or opposed, neither support nor opposed, support, and strongly support). We estimate versions of the logit models which control only for the cases proposed to the respondents and a specification which also controls for respondents’ sociodemographic characteristics (sex, age, sector of employment, educational and marital status, religion and ethnicity, income, house ownership, family size), health-related traits (household health care use, life style of family members – incidence of drinking, smoking, chewing chat, health insurance, knowledge of health insurance) and a set of geographical indicator variables.

Ethics Statement

Informed consent was obtained from respondents prior to data collection. Ethics approval (IDPR/LT-0005/2016) was provided by the Research Ethics Committee of the Addis Ababa University. All respondents provided informed consent to participate in the study after being briefed on its purpose and the confidentiality of the collected data. The study complies with the guidelines outlined in the Declaration of Helsinki.

Results

Descriptive Statistics

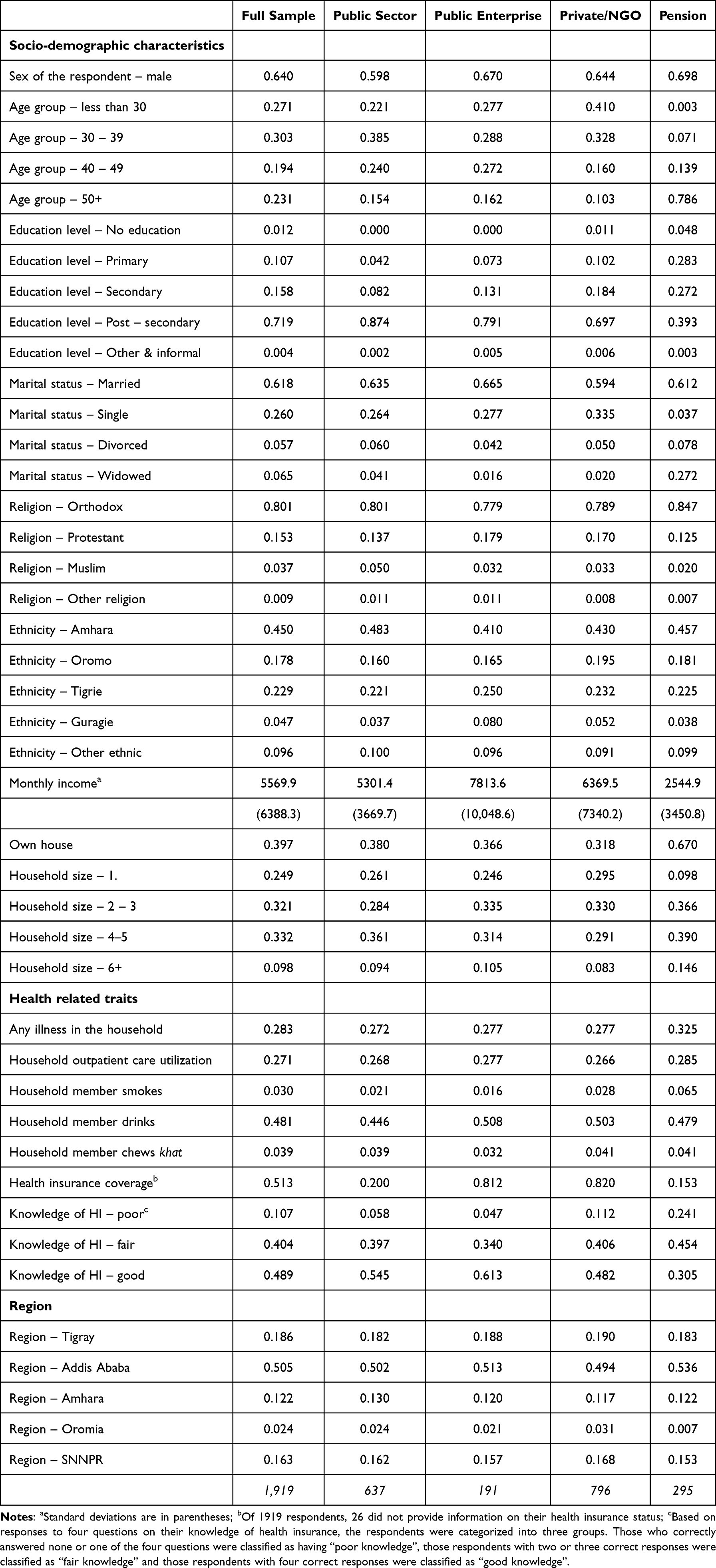

The sample consists of 1,919 individuals and as shown in Supplementary Table 1, the distribution of the sample across sectors matches their distribution in the population. The sample consists of 33% public sector workers, about 10% work in public enterprises, 41.4% are engaged in the private sector/NGO while the remainder (15%) are pensioners. About 64% of the sample is male. Since the sample consists of formal sector workers, it is not surprising that about 72% have tertiary education. Amongst those still working, education levels are highest amongst public sector workers – 87% have tertiary education as opposed to about 70% amongst private/NGO sector workers. Regarding monthly income, pensioners have the lowest income while workers in public sector enterprises record the highest income (Table 2).

|

Table 2 Socioeconomic Characteristics of Survey Respondents |

Table 2 also provides information on the current health insurance status and knowledge of health insurance of sample respondents. On average, about 51% of respondents have health insurance. This figure varies substantially across sectors with 81%–82% of public sector enterprise and private sector/NGO workers reporting that they have health insurance while the corresponding figures are 20% among public sector workers and 15% amongst pensioners. This sharp difference in coverage supports the idea that enterprises, both public and private, and NGOs offer health insurance to attract workers while those in the public sector are not offered similar benefits.41,42 While almost all respondents had heard of health insurance (92%), a much smaller fraction – about 49% - were able to provide correct answers to a set of four questions on the functioning of insurance (see Tables 2 and 3). There is some variation across sectors with “good knowledge” of insurance varying from a low of 30.5% amongst pensioners to a high of 61.3% amongst private sector/NGO workers.

|

Table 3 Understanding of Health Insurance (%) |

Awareness and Willingness to Support CBHI

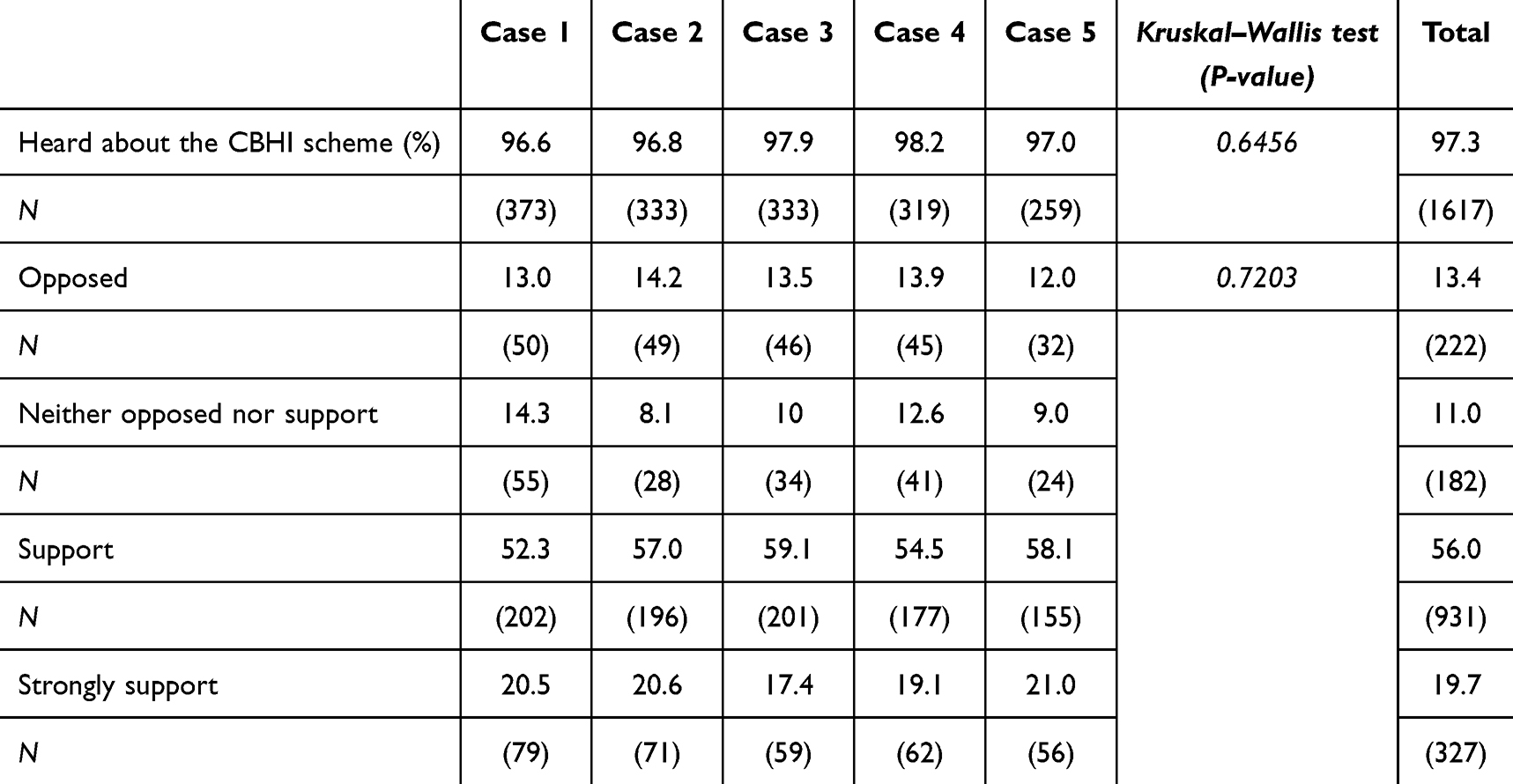

Of the 1,919 respondents, about 13% (257) refused to respond to the cases. The non-respondents tend to be older, less educated, more likely to be in the lower income categories, and more likely to reside in Tigray (see Supplementary Table 4). The reasons for their lack of response are unclear but it could indicate lack of support for the CBHI, thereby providing an inflated idea of support for the scheme. We return to this issue in the discussion. Conditional on (strongly) supporting the scheme, almost all (97%) signed a piece of paper indicating their commitment.

In response to the first question on scheme awareness, regardless of the case, almost all (97%) the respondents had heard about the scheme (Table 4). Subsequently, all those who had heard about the CBHI were asked to indicate their support or lack thereof, for it. As shown in Table 4, regardless of whether the case provided no information, or provided information on the source of subsidy (domestic or international support) or information on the subsidy and research-based findings on the benefits that the CBHI has yielded or only information on the benefits, there was strong overall support for the CBHI. Across all information scenarios, approximately 76% of formal sector respondents either supported or strongly supported the CBHI, while only 13% opposed the scheme. This high level of support affirms that a majority of formal sector employees are willing to contribute to the sustainability of CBHI, aligning with the scheme’s principle of solidarity and the government’s plan to integrate it with SHI. While there are no statistically significant differences in support across the cases, two notable patterns emerge. First, regardless of whether formal sector workers are expected to subsidize the scheme or not they do not waver in terms of their support (compare cases 1 and 2). Second, there is greater support when research findings on benefits are provided – 73% versus 79% (compare cases 1 and 5). This highlights the importance of raising awareness about the benefits of CBHI as a key strategy to strengthen formal sector support for pooled insurance schemes and, in turn, facilitate the successful integration of CBHI and SHI into a unified national system.

|

Table 4 Awareness and Support for the CBHI Scheme |

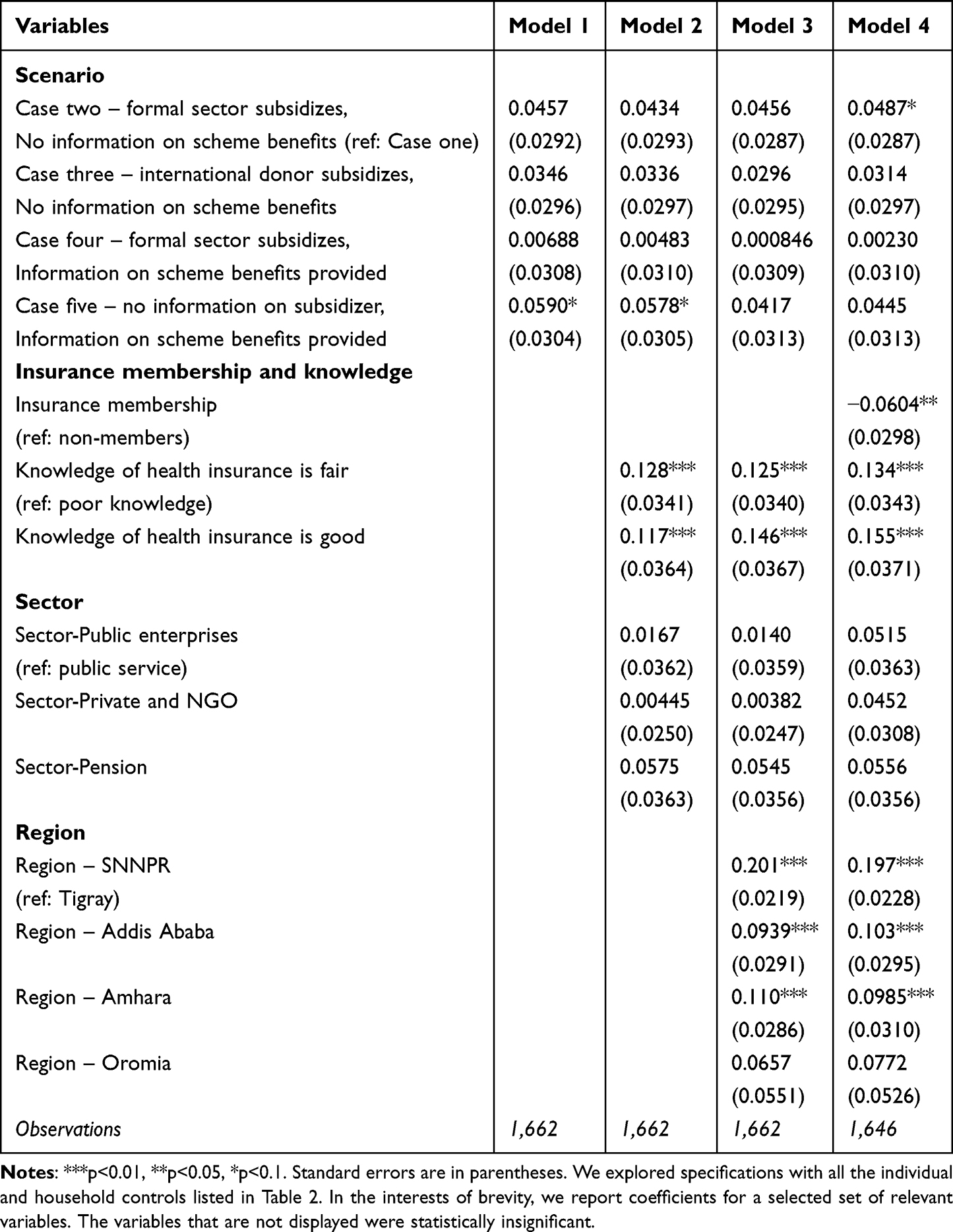

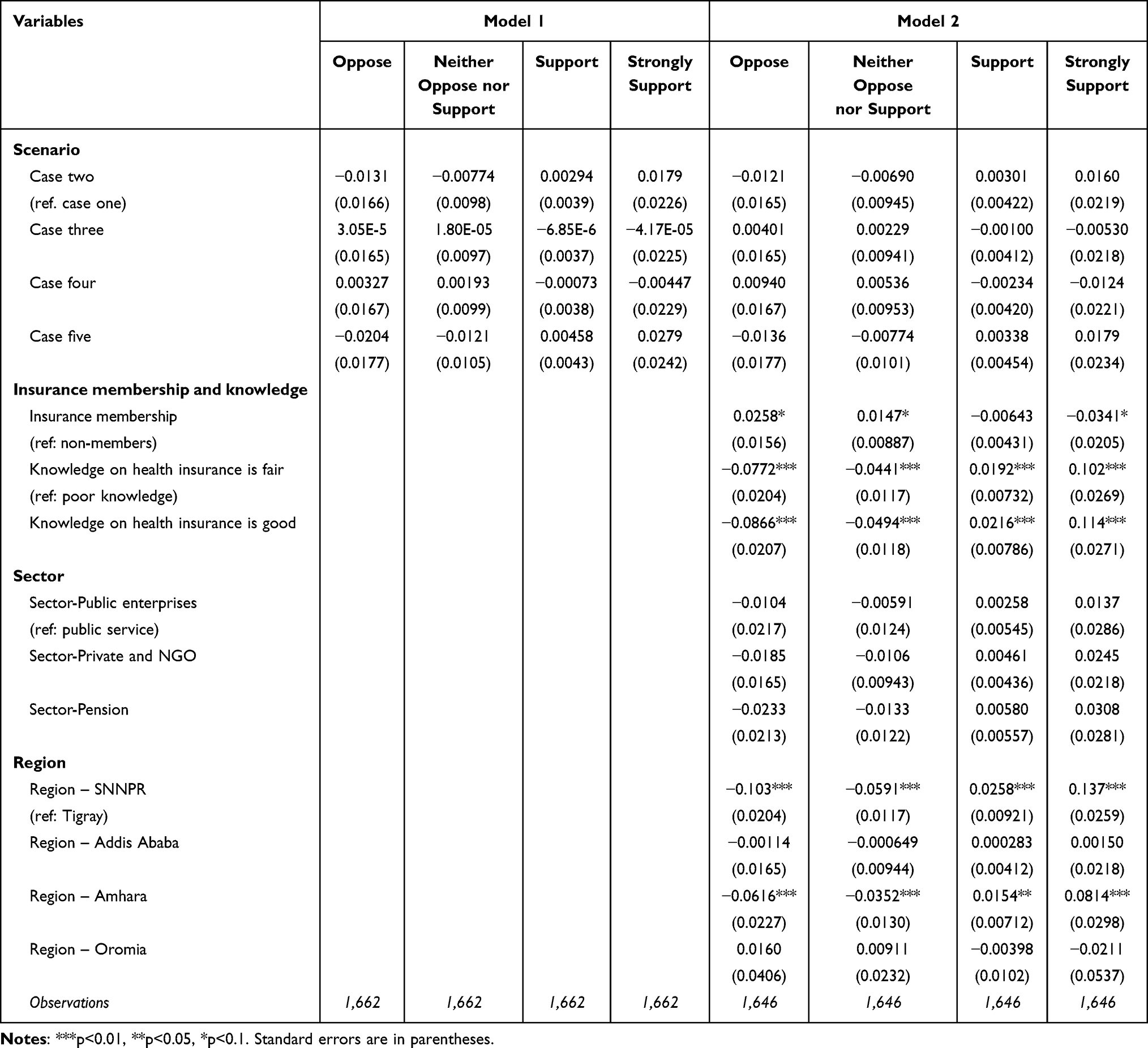

To investigate the traits of those who support/do not support the scheme, Table 5 provides marginal effects from a logit model. The table presents four sets of estimates. Consistent with the patterns noted in Table 4, the level of support does not vary between the baseline and cases two, three and four. However, there is a statistically significant 6 percentage point higher support amongst respondents who are provided with research-based findings on the benefits associated with CBHI (Table 5, model 1). The inclusion of several traits reduces the statistical significance of the case variables but the qualitative story remains the same. The additional information yielded by these specifications is that individuals who already have insurance are less likely to support CBHI (6 percentage point effect). Those respondents who have greater knowledge of insurance are more likely to support the CBHI – the effect is 12–16 percentage points higher depending on the model and whether an individual has fair or good knowledge of health insurance. Finally, there is large regional variation with the greatest support for the CBHI amongst formal sector workers in SNNPR, followed by Amhara and Addis Ababa (model 3). The lowest level of support in Tigray followed by the Oromia region.

|

Table 5 Probability of Supporting CBHI – Marginal Effects After Binary Logit Models |

As a final step, instead of a two-part (support/do not support specification) we estimated an ordered logit with four categories – ranging from opposing the CBHI to strong support (see Table 6). These estimates yield subtle insights. Like the results in Tables 4 and 5, there is no indication that the type of information provided about the design features of the CBHI has a bearing on the support expressed by formal sector employees. As in the case of the binary logit model, knowledge of health insurance has a bearing on support for the CBHI scheme. Employees with good knowledge of health insurance are 10 to 11 percentage points more likely to strongly support the development of the CBHI scheme compared to those with poor knowledge. Those with health insurance are not just neutral but more likely to oppose support for the CBHI. Similarly, while regional disparities remain salient, formal sector workers in Tigray and Oromia actively oppose support for the CBHI as opposed to being neutral. These differences across insurance status and across regions signal that any effort to merge SHI and CBHI should account for such disparities in acceptance and trust.

|

Table 6 Probability of Supporting CBHI – Marginal Effects After Ordered Logit |

Discussion

This paper examined formal sector employees’ willingness to support Ethiopia’s Community-Based Health Insurance (CBHI) scheme, a critical precursor to integrating it with the proposed Social Health Insurance (SHI). The findings revealed robust support (76%) for CBHI across all surveyed groups, even when respondents were informed that formal sector workers may need to subsidize the scheme. One possible reason for this widespread positive attitude is the remarkable progress that the CBHI has achieved in a relatively short period since its launch in 2011, especially as compared to the experiences in other sub-Saharan African countries.

Building on lessons from the initial pilot phase, the CBHI scheme has been scaled up and now covers approximately 87% of urban and rural districts, reaching about 78% of eligible households in the pilot districts.18 Existing studies also confirm the effectiveness of CBHI in Ethiopia—not only in terms of coverage but also in expanding access to primary healthcare services for underserved populations and offering financial protection against catastrophic health expenditures.43–45 The results of the current study align with prior research emphasizing the role of solidarity in health financing reforms.28,30 Notably, disseminating evidence on CBHI’s effectiveness increased support by 6 percentage points, echoing other findings in the literature that have highlighted the importance of awareness campaigns in fostering acceptance of risk-pooling mechanisms.46,47

However, the high support for CBHI contrasts sharply with resistance to SHI implementation.25,40 Evidence indicates that the willingness to join SHI among formal sector employees is relatively low. For instance, a study of public servants in Addis Ababa found that only 35.4% were willing to pay the proposed 3% salary premium, while just 29.6% of civil servants in Dessie City expressed their willingness to pay for the scheme.26,48

While CBHI’s proven track record in expanding access and reducing out-of-pocket costs inspires confidence, SHI faces skepticism due to cost concerns, perceived low quality of public healthcare, and exclusion of private facilities. This dichotomy underscores the need to address trust deficits and affordability barriers specific to SHI. Ethiopia’s Health Sector Transformation Plan II (2020/21–2024/25) recognizes this challenge and prioritizes expanding CBHI coverage to 80% of the population by 2025. It specifically highlights the need for transparent fund management and improved accountability as key strategies to build public trust and support the integration of CBHI and SHI.49

Regional disparities further complicate the picture. Support was lowest in Tigray (63%) and Oromia (69%), potentially reflecting historical grievances and distrust in federal initiatives.50,51 In contrast, SNNPR’s high support (88%) correlates with agrarian livelihoods and higher user satisfaction,52 though satisfaction metrics alone do not fully explain regional differences. Surprisingly, despite Tigray’s respondents exhibiting high insurance knowledge (82%), their support remained low, suggesting contextual factors like recent political tensions may play a role. The study also found that existing health insurance holders were less supportive of CBHI, likely fearing dual financial burdens.42 This highlights the challenge of balancing solidarity with individual financial security in hybrid insurance systems.

Conclusion

This study provides novel evidence that a substantial proportion of urban formal sector workers in Ethiopia are willing to financially support a CBHI scheme which is intended for workers in the informal sector. Depending on the specific scenario and adjusting for non-response, about 66% of formal sector workers were willing to support the CBHI even without a legal mandate. The results affirm the feasibility of integrating CBHI and SHI to create a unified risk pool, as envisioned by the government.53,54 However, the persistent resistance to SHI implementation—rooted in cost concerns and distrust in public healthcare quality—poses a critical barrier. To advance universal health coverage, policymakers must address SHI-specific challenges through targeted communication, improved service quality, and financial literacy programs, while leveraging CBHI’s success to build broader public trust in health insurance reforms.

Unlike prior research which has focused mainly on CBHI beneficiaries or SHI enrollees, this study captured the willingness of formal sector workers to support more inclusive coverage models.24,26,55 The results highlighted a critical solidarity-based financing opportunity that supports the integration of CBHI and SHI. These findings offer timely, policy-relevant insights to inform Ethiopia’s health insurance reforms and efforts to expand domestic health financing.17,56 The results are of broader relevance as they offer useful policy insights for building unified, equitable, and potentially sustainable health insurance systems in other low- and middle-income countries with contexts similar to Ethiopia.

Acknowledgments

This work was supported by D.P. Hoijer Fonds, Erasmus Trustfonds, Erasmus University Rotterdam, The Netherlands. Award/Grant number is not applicable.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Federal Ministry of Health. Health and Health Related Indicators 1992 E.C (2001/02). Addis Ababa: FMoH; 2002.

2. Federal Ministry of Health. Ethiopian Health Service Coverage - Fact Sheet 2020. Addis Ababa: FMoH; 2021 [cited December 15, 2021]. Available from: https://www.moh.gov.et/site/fact-sheets.

3. World Bank. Modeled estimation of Maternal Mortality Ratio in Ethiopia; 2023a [cited January 10, 2024]. Available from: https://data.worldbank.org/indicator/SH.STA.MMRT?locations=ET.

4. World Bank. UHC service coverage index – ethiopia; 2023b [cited February 5, 2024]. Available from: https://data.worldbank.org/indicator/SH.UHC.SRVS.CV.XD?locations=ET.

5. Rieger M, Wagner N, Mebratie A, Alemu G, Bedi A. The impact of the Ethiopian health extension program and health development army on maternal mortality: a synthetic control approach. Soc Sci Med. 2019;232:374–381. doi:10.1016/j.socscimed.2019.05.037

6. Alene KA, Elagali A, Barth DD, et al. Spatial codistribution of HIV, tuberculosis and malaria in Ethiopia. BMJ Glob Health. 2022;7(2):e007599. doi:10.1136/bmjgh-2021-007599

7. World Health Organization. World malaria report 2023. Geneva: WHO; 2023.

8. World Health Organization. Global tuberculosis report 2020 [Internet]. Geneva: World Health Organization; 2020 [cited February 16, 2025]. Available from: https://iris.who.int/bitstream/handle/10665/336069/9789240013131-eng.pdf.

9. Federal Ministry of Health. Ethiopia National Health Accounts Report 2019/20. Addis Ababa: Partnership and Cooperation Directorate, FMoH; 2022b.

10. FMOH. Health Sector Development plan IV (2010/11-2014/15). Addis Ababa: Federal Minstry of Health; 2010.

11. Zambia Ministry of Health. Health financing strategy: 2017–2027. Towards universal coverage for Zambia [Internet]. Lusaka: Ministry of Health; 2017 [cited January 15, 2025]. Available from: https://www.afro.who.int/sites/default/files/2020-09/Health%20Care%20Financing%20Strategy.pdf.

12. Nyamugira AB, Richter A, Furaha G, Flessa S. Towards the achievement of universal health coverage in the Democratic Republic of Congo: does the country walk its talk? BMC Health Serv Res. 2022;22(1):860. doi:10.1186/s12913-022-08228-3

13. De Weerdt J, Dercon S. Risk-sharing networks and insurance against illness. J Dev Econ. 2006;81(2):337–356. doi:10.1016/j.jdeveco.2005.06.009

14. Karami M, Najafi F, Karami M. Catastrophic health expenditures in Kermanshah, West of Iran: magnitude and distribution. J Res Health Sci. 2009;9(2):36–40.

15. O’Donnell O, van Doorslaer E, Rannan-Eliya RP, et al. Explaining the incidence of catastrophic expenditures on health care: comparative evidence from Asia. EQUITAP Working Paper 05 [Internet]. Manila: Equity in Asia-Pacific Health Systems; 2005.

16. Flores G, Krishnakumar J, O’Donnell O, Van Doorslaer E. Coping with health-care costs: implications for the measurement of catastrophic expenditures and poverty. Health Econ. 2008;17(12):1393–1412. doi:10.1002/hec.1338

17. Abt Associates. Health care financing reform in Ethiopia: improving quality and equity. Addis Ababa: Abt Associates Inc.; 2012.

18. Federal Ministry of Health. Annual Performance Report 2015 EFY. Addis Ababa: FMoH; 2023 [cited December 18, 2024]. Available from: https://arm.moh.gov.et/wp-content/uploads/2023/10/Annual-Performance-Report_2015-EFY_Final.pdf.

19. Alemu G, Shigute Z, Mebratie A, Sparrow R, Bedi AS. On the functioning of community-based health insurance schemes in rural Ethiopia. Soc Sci Med. 2024;345:115739. doi:10.1016/j.socscimed.2023.115739

20. Mebratie A, Sparrow R, Yilma Z, Alemu G, Bedi A. Dropping out of Ethiopia’s community based health insurance scheme. Health Policy Plan. 2015;30(10):1296–1306. doi:10.1093/heapol/czu142

21. Yilma Z, Mebratie A, Sparrow R, Alemu G, Bedi A. Impact of Ethiopia’s pilot Community based health insurance scheme on household economic welfare. World Bank Econ Rev. 2015;29(Suppl_1):S164–S173. doi:10.1093/wber/lhv009

22. Mebratie AD, Sparrow R, Yilma Z, Abebaw D, Alemu G, Bedi A. Impact of Ethiopian pilot community-based health insurance scheme on health-care utilisation: a household panel data analysis. Lancet. 2013;381:S92. doi:10.1016/S0140-6736(13)61346-X

23. Minyihun A, Gebregziabher MG, Gelaw YA. Willingness to pay for community-based health insurance and associated factors among rural households of Bugna District, Northeast Ethiopia. BMC Res Notes. 2019;12:55. doi:10.1186/s13104-019-4091-9

24. Negera M, Abdisa D. Willingness to pay for community based health insurance scheme and factors associated with it among households in rural community of South West Shoa Zone, Ethiopia. BMC Health Serv Res. 2022;22(1):734. doi:10.1186/s12913-022-08086-z

25. Zarepour Z, Mebratie A, Shamebo D, Shigute Z, Alemu G, Bedi AS. Social health insurance and healthcare seeking behavior in urban Ethiopia. Ann Global Health. 2023;89(1):84. doi:10.5334/aogh.4240

26. Amilaku EM, Fentaye FW, Mekonen AM, Bayked EM. Willingness to pay for social health insurance among public civil servants: a cross-sectional study in Dessie City Administration, North-East Ethiopia. Front Public Health. 2022;10:920502. doi:10.3389/fpubh.2022.920502

27. Zweifel P, Breyer F, Kifmann M. Health Economics. Springer Science & Business Media; 2009 Jul 14.

28. Buchmueller TC, Couffinhal A. The role of social solidarity in the financing of health care. Int J Health Serv. 2004;34(3):469–490.

29. Douwes R, Stuttaford M, London L. Social solidarity, human rights, and collective action: considerations in the implementation of the National Health Insurance in South Africa. Health Hum Rights. 2018;20(2):185.

30. Harris B, Nxumalo N, Ataguba JE, Govender V, Chersich M, Goudge J. Social solidarity and civil servants’ willingness for financial cross-subsidization in South Africa: implications for health financing reform. J Public Health Policy. 2011;32:S162–S183. doi:10.1057/jphp.2011.23

31. Health Finance and Governance Project. Ethiopia scales up community-based health insurance. Addis Ababa: HFG; 2015.

32. Amhara National Regional State. Amhara Region community based health insurance implementation Directive no 08/2024. Bahir Dar: ANRS; 2024.

33. Abt Associates. Ethiopia’s community-based health insurance: a step on the road to universal health coverage; 2015 [cited December 15, 2021]. Available from: https://pdf.usaid.gov/pdf_docs/PA00KDXT.pdf.

34. Ethiopian Health Insurance Agency. CBHI members’ registration and contribution (2011–2020 G.C): CBHI trend bulletin. Addis Ababa: EHIA; 2020.

35. Segahu ZA. The contribution of community-based health insurance (CBHI) in improving access and utilization of healthcare services: the case of Adea District, East Shoa Zone, Oromia Region, Ethiopia [dissertation]. Addis Ababa: St. Mary’s University; 2018.

36. Federal Democratic Republic of Ethiopia. Social health insurance scheme. Federal Negarit Gazeta, Council of Ministers Regulation 271/2012. Addis Ababa: FDRE; 2012.

37. SIAPS. Ethiopian national health insurance scale-up assessment on medicines financing, use, and benefit management. Arlington (VA): Systems for Improved Access to Pharmaceuticals and Services; 2016.

38. Ali EE. Health Care Financing in Ethiopia: implications on access to essential medicines. Value Health Reg Issues. 2014;4(1):37–40. doi:10.1016/j.vhri.2014.06.005

39. Federal Ministry of Health. Health and Health Related Indicators for 2004 EC (2021/22 GC). Addis Ababa: FMoH; 2012.

40. Bayked EM, Toleha HN, Chekole BB, Workneh BD, Kahissay MH. Willingness to pay for social health insurance in Ethiopia: a systematic review and meta-analysis. Front Public Health. 2023;11:1089019. doi:10.3389/fpubh.2023.1089019

41. Federal Ministry of Health. Health and Health Related Indicators for 2014 EFY (2012 GC). Addis Ababa: FMoH; 2022a.

42. Obse A, Ryan M, Heidenreich S, Normand C, Hailemariam D. Eliciting preferences for social health insurance in Ethiopia: a discrete choice experiment. Health Policy Plann. 2016;31(10):1423–1432. doi:10.1093/heapol/czw084

43. Alemayehu YK, Dessie E, Medhin G, et al. The impact of community-based health insurance on health service utilization and financial risk protection in Ethiopia. BMC Health Serv Res. 2023;23(1):67. doi:10.1186/s12913-022-09019-6

44. Degefa MB, Woldehanna BT, Mebratie AD. Effect of community-based health insurance on catastrophic health expenditure among chronic disease patients in Asella referral hospital, Southeast Ethiopia: a comparative cross-sectional study. BMC Health Serv Res. 2023;23(1):188. doi:10.1186/s12913-023-09181-5

45. Mebratie AD, Sparrow R, Yilma Z, Abebaw D, Alemu G, Bedi AS. The impact of Ethiopia’s pilot community based health insurance scheme on healthcare utilization and cost of care. Soc Sci Med. 2019;220:112–119. doi:10.1016/j.socscimed.2018.11.003

46. Shrestha MV, Manandhar N, Dhimal M, Joshi SK. Awareness on social health insurance scheme among Locals in Bhaktapur Municipality. J Nepal Health Res Counc. 2020;18(3):422–425. doi:10.33314/jnhrc.v18i3.2471

47. Sendekie AK, Gebremichael AH, Tadesse MW. Enrollment and clients’ satisfaction with a community-based health insurance scheme: a community-based survey in Northwest Ethiopia. BMC Health Serv Res. 2024;24(1):70. doi:10.1186/s12913-024-10570-7

48. Kokebie MA, Abdo ZA, Mohamed S, Leulseged B. Willingness to pay for social health insurance and its associated factors among public servants in Addis Ababa, Ethiopia: a cross-sectional study. BMC Health Serv Res. 2022;22(1):909. doi:10.1186/s12913-022-08304-8

49. Ethiopian Federal Ministry of Health. Health Sector Transformation Plan II (2020/21–2024/25). Addis Ababa: Federal Democratic Republic of Ethiopia; 2020.

50. Kelecha M. Oromo protests, repression, and political change in Ethiopia, 2014–2020. Northeast African Studies. 2021;21(2):183–226. doi:10.14321/nortafristud.21.2.183v

51. Salemot MA, Matshanda NT. The causes and consequences of the 2018 failed peace agreement between the Oromo Liberation Front and the Ethiopian government. J Contemporary African Studies. 2023;41(4):441–458. doi:10.1080/02589001.2023.2193364

52. Wolde HM, Tekle MG, Alemayehu YK, Gebre EG, Teklu AM. Attrition of health extension workers in Ethiopia: trends, regional variations and determinants–a mixed methods study of 15 years of experience. BMC Health Serv Res. 2023;23(1):1444. doi:10.1186/s12913-023-10292-2

53. Hanson K, Brikci N, Erlangga D, Cashin C, Gatome-Munyua A. Mapping research on Primary Health Care financing in Ethiopia. Financing PHC in Ethiopia BRIEF 1. Lancet Glob Health Comm. 2023.

54. HSFR. Piloting community-based health insurance in Ethiopia: the way forward. Addis Ababa: Health Sector Financing Reform Project; 2008.

55. Birhanu Z, Sudhakar M, Jemal M, et al. Households willingness to join and pay for community-based health insurance: implications for designing community-based health insurance based on economic Status in Ethiopia. PLoS One. 2025;20(3):e0320218. doi:10.1371/journal.pone.0320218

56. Federal Ministry of Health, Ethiopia. Health Care Financing Strategy 2022–2031. Addis Ababa: Ministry of Health; 2022.

© 2025 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2025 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.