")

Back to Journals » Risk Management and Healthcare Policy » Volume 17

Urban-Rural Health Insurance Integration and China’s Rural Household Savings

Authors Yuan Z, Zhang F, Li Z , Wei H

Received 22 November 2023

Accepted for publication 5 March 2024

Published 13 March 2024 Volume 2024:17 Pages 587—601

DOI https://doi.org/10.2147/RMHP.S451278

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Jongwha Chang

Zhen Yuan,1,2 Fan Zhang,3 Zhiguang Li,1,2 Hua Wei1,2

1School of Economics and Management, Anhui University of Chinese Medicine, Hefei, Anhui, People’s Republic of China; 2Key Laboratory of Data Science & Innovative Development of Traditional Chinese Medicine, Philosophy and Social Sciences of Anhui Province, Hefei, Anhui, People’s Republic of China; 3School of Finance, Nanjing Agricultural University, Nanjing, Jiangsu, People’s Republic of China

Correspondence: Zhiguang Li; Hua Wei, Email [email protected]; [email protected]

Background: A linchpin to realizing the internal circulation (referring to the domestic cycle of production, distribution and consumption) is reducing residents’ saving rate and expanding the domestic needs. However, rural residents in China demonstrate a strong propensity to save money.

Methods: In light of practical characteristics of urban-rural health integration promoted in different places, the three-phase data (from 2014 to 2018) and the dual difference-in-differences model of the China Labor-force Dynamics Survey (CLDS) are used to empirically investigate the impact of urban-rural health insurance integration on rural household savings.

Results: Research reveals that urban-rural health integration can reduce the health risks and medical risks facing rural households, thus weakening the motivation of precautionary savings. The analysis of heterogeneity reveals that the integration of urban-rural health insurance significantly influences the savings rates of households headed by older individuals, particularly women, with lower levels of educational attainment. Besides, the single-tier health insurance system can have a more significant impact, whereas the multi-tier insurance system may not significantly affect the savings rate.

Conclusion: Based on the aforesaid research conclusions, this article believes that in order to reduce the savings rate of rural households and expand consumption, the health insurance system should be further improved.

Keywords: urban-rural health insurance integration, rural household, savings rate, health risks, medical risks

Introduction

The high savings rate has been a typical economic phenomenon prevailing in China after China’s adoption of the reform and opening-up policy. To fully tap the consumption potential of residents and to convert residents’ savings into buying behaviors hold great importance to propel sound and sustainable economic development. Compared with urban residents, China’s rural residents are faced with more risk impact and uncertainties. Therefore, rural residents have a stronger willingness of savings. In China, rural residents take up more than half of the total population, so investigating into the savings rate of China’s rural residents is of vital importance.

Some scholars have explained the high savings rate of Chinese residents from the perspective of social security, thinking that an incomplete social security system cannot effectively alleviate future expenditure risks from old-age care and medical care, so Chinese households tend to resort to precautionary savings in response to the future uncertainties.1,2 Theoretically, health insurance might bring down health risks and medical risks facing the family, thereby weakening the precautionary savings motivation and the savings rate. However, scholars have not yet reached an agreement on the correlation between health insurance and savings rate.3,4 China possesses the most extensive healthcare insurance system in the world.5 In its specific healthcare insurance reform practices, to eliminate disparities in healthcare benefits between urban and rural areas, China has gradually integrated Urban Resident Basic Medical Insurance (URBMI) with the New Rural Cooperative Medical Scheme (NRCMS) into a unified basic medical insurance system for urban and rural residents. This integration of medical insurance has enhanced the level of healthcare coverage for rural inhabitants and, theoretically, has implications for the savings rates of rural households.

Based on time differences of Chinese cities starting rural-urban health insurance integration, this paper matches the health insurance integration information of different places with the three-phase data of the China Labor-force Dynamics Survey (CLDS) in 2014, 2016 and 2018, respectively. After that, the difference-in-differences (DID) model is used to empirically study the impact of urban-rural integration on the rural household savings rate. This research can contribute to the existing literature in the following aspects. First, scholars should pay more attention to the correlation between the old-age insurance and the savings rate, but they are seldom concerned about how health insurance can influence the savings rate.6,7 This research can make up this research gap. Secondly, existing studies have revealed that the integration of healthcare insurance has unlocked residents’ medical needs, fostering the utilization of medical services,8 enhancing the health outcomes of residents,9 and reducing the degree of health inequality between urban and rural areas.10 However, there is a lack of literature discussing the impact of this healthcare insurance integration on the savings rates of rural households in China. This paper serves as a complement to the existing body of research in this area. At last, based on the precautionary savings motivation theory, we examine the mechanism of action of health insurance integration on rural household savings rate from the perspective of health risks and medical risks to deepen the understanding of relevant issues.

The rest of this paper is organized as below: Section 2 provides a literature view of health insurance and savings rate. Section 3 presents the institutional background of health insurance integration and carries out theoretical analysis. Section 4 introduces the research design. Section 5 is the empirical analysis. Section 6 provides research conclusions and discussion for this paper.

Literature Review

Scholars have extensively researched the factors influencing savings rates. Horioka and Wan investigated the impact of the dependency ratio on household savings rates.11 Wei and Zhang posited that pressures in the marriage market lead households to increase savings for housing expenses.12 Li et al explained the high savings phenomenon from the perspective of increased life expectancy.13

The theoretical basis for the correlation between health insurance and savings rate is precautionary savings motivation theory. According to life cycle theory, rational decision-makers save money when they are young so that they will have money to spend when they are old. This ensures them to arrange their spending and maximize the efficacy of their spending within the life cycle. The theory of precautionary savings motivation introduced uncertainty for analysis on the basis of the life cycle theory. The theory of precautionary savings motivation believes that, because of imperfections of the social security system, including medical care, unemployment, and old-age care, consumers tend to save their current income to guard against risks caused by their future income variations, which is a main reason for the rising savings rate.14,15 The risk-averse consumers have relatively obvious precautionary savings behaviors.16

As a risk-alleviating institutional arrangement, social security has a significant influence on the savings rate. Scholars are more conserved about the influence of the old-age insurance on the savings rate. The old-age insurance can reduce the income risk of residents after their retirement, which will alleviate preventability,6 so the old-age insurance can negatively influence the household savings. Lachowska and Myck adopted the endowment reform of Poland in 1999 as the research object, finding that a reduction in the endowment can lead to an increase of household savings.7

Health insurance exists as another social security system, but the correlation between health insurance and the savings rate has not yet received adequate attention. Even if there have been some research attempts examining this issue, the research findings are largely divided. Some believe that the health insurance can make up part of patients’ medical expenses and lower the uncertainty of their medical expenditure. As a result, their precautionary savings kept declining.3 Chou’s analysis revealed that, after the implementation of the health insurance reform, the individual savings rate in Taiwan experienced a sharp decline.17 Other scholars hold that health insurance can increase the household savings rate. Alessandra’s research revealed that public insurance usually provides poor services and requires customers to wait for a long time. While waiting for treatment provided by public insurance, customers are faced with a higher risk of accidents. So in comparison with private medical insurance, the coverage of public insurance will in turn increase residents’ savings rate.18 However, some scholars have also pointed out the uncertainty of the correlation between health insurance and household savings.19 Maynard and Qiu discussed about the correlation between medical aid and savings, and analyzed this issue by income groups. They argued that medical aid has reduced the savings rate of medium-income participants, but this does not influence the savings rate of other income participants.20

To sum up, scholars have seldom discussed about the correlation between health insurance and savings, but there has not yet been an agreement on this issue. Considering that rural-urban health integration is implemented at the municipal level gradually, this paper thus adopts the differences-in-differences (DID) approach to better recognize the causality between health insurance and savings rate, hoping to enrich research findings concerning health insurance and savings rate.

Institutional Background and Theoretical Analysis

Institutional Background

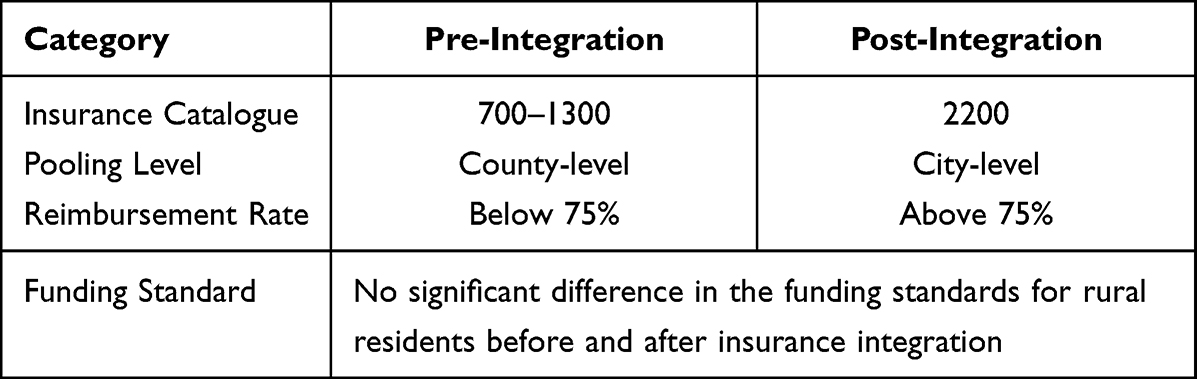

To satisfy residents’ basic health demands, China has made lots of explorations after 1998, having established a basic health insurance system consisting of urban employees’ health insurance (health insurance for urban workers), new-type rural cooperative health insurance and health insurance for urban dwellers. By the end of 2011, participants of the three health insurance systems have taken up 97% of the total national permanent residents, which means that a full coverage of health insurance has been basically realized. As a basis for insurance participation, health insurance for urban workers and new-type cooperative health care artificially divide the insurance participants, which has reinforced the census register segmentation and its affiliated social security system. Consequently, there have been significant differences between the urban and rural health insurance system in terms of the coverage scope, funding level and style, overall planning hierarchy and compensation style. Since the health insurance system separating the urban and rural areas ran counter to the principles of justice and fairness, integration thus became a necessity.

China’s health integration process can mainly be divided into two stages. Before 2016, some cities took the initiative to integrate the health insurance for urban dwellers with the new-type rural cooperative health insurance. In January 2016, the State Council issued the Opinions on Integrating Urban and Rural Residents’ Basic Health Insurance System (National Development and Reform Commission [2016] No. 3 Document) to obviously speed up urban-rural health insurance integration. The whole urban-rural health insurance integration consisted of six aspects. In other words, the urban-rural residents; basic health insurance after integration can cover all other urban and rural residents apart from urban workers. Since the implementation of integration, urban and rural areas have adopted the same funding standards, same urban-rural coverage and payment standards, same catalog of medicines and services covered by health insurance, same management methods for designated urban and rural residents’ health insurance institutions, and same health insurance fund management systems. Table 1 illustrates the changes in healthcare benefits for rural residents before and after the integration of medical insurance. In this paper, we sorted around 300 documents related to municipal health insurance. After sorting these data, we found that, before and in 2016, there were just a few cities taking the initiative to seek urban-rural health insurance integration. Two years after the Central Government’s promulgation of the urban-rural health insurance integration, the number of cities seeking urban-rural health insurance integration increased to 172. By the year 2020, a majority of cities had finished the health insurance integration. Based on the progressive promulgation of health insurance integration in different cities, we can study policy effects of urban-rural health insurance integrating using the progressive Differences-in-Differences method under the research framework of “natural experiment”.

|

Table 1 Changes in Healthcare Insurance Benefits |

In practice, integration models can be divided into three kinds, including “one system and single tier”, “one system and two tiers” and “one system and three tiers”. The single-tier system implements funding and payment standards which are totally the same. The two-tier system divides grown-up residents’ funding and corresponding payment into two tiers. The high-tier funding and payment is similar to the previous medical insurance for urban residents; the low-tier funding and payment is similar to the previous new-type cooperative medical system. Urban residents can choose the high-tier funding and payment system, while rural counterparts have the freedom to choose the high-tier or low-tier system. So the two-tier system has maintained the relatively independent funding and payment level of the previous health insurance for urban residents and the previous new-type cooperative medical system, which is only a funding balance between different new-type cooperative systems of the past. The three-tier system divides the funding and payment of grown-up residents into three tiers. At present, regions adopting the three-tier system are lacking. Before and in 2016, cities adopting urban-rural health insurance integration mostly turned to the two-tier system. After 2016, cities seeking health insurance integration generally chose single-tier system. In this paper, we unified the two-tier system and the three-tier system into the multi-tier system.

Theoretical Analysis

During the health insurance integration process, we should stick to three principles. First, the reimbursement scope and coverage of health insurance for urban and rural residents should be consistent. Second, the health insurance treatment for urban and rural residents should not be reduced. Third, the individual payment should not be increased under the bearing capacity of finance. This means that, compared with the new-type rural cooperative system, urban-rural integration can provide more comprehensive medical coverage and better health insurance for rural residents without increasing the actual payment. For example, health insurance items covered by health insurance for urban residents are about twice as many as those covered by the new-type rural cooperative medical system. After urban-rural health insurance integration, rural and urban residents are entitled to the same catalog of items covered by health insurance. This means that the health insurance reimbursement scope for rural residents has been expanded. The new-type rural cooperative medical system follows the county-level overall planning. Seeking medical treatment beyond the county requires directly settling medical expenses incurred outside of a patient’s hometown. Under the condition, seeking medical treatment and reimbursement can both be a challenge. On the contrary, the urban-rural residents’ basic medical insurance follows the municipal overall planning, thus allowing rural residents to seek medical care within the city which they belong to. This has greatly enriched the options of medical treatment. Besides, urban-rural health insurance integration has strengthened the subsidization for rural residents, and improved the reimbursement percentage of hospitalization and outpatient services.

Before urban-rural health insurance integration, the new-type rural cooperative insurance, although having realized full coverage of rural residents, still featured a low hierarchy, a narrow scope of catalog and a low percentage of reimbursement. Because of these defects, the new-type rural cooperative could not provide adequate health insurance for rural residents. Some residents hold that the new-type rural cooperative medical system has failed to significantly bring down medical expenses covered by themselves,21 nor has it effectively curbed the occurrence of disease-triggered poverty.22 So evidence is lacking to conclude that the new-type rural cooperative medical system has comprehensively boosted rural residents’ health and effectively alleviate risks. In the face of uncertainties brought by health insurance and medical risks, rural residents tend to save up money, which indicates a strong motivation of precautionary savings. Health insurance integration has improved the health insurance level for rural residents to demonstrate significant health performance.9 Therefore, after medical insurance integration, health risks and health risks facing rural residents have both dramatically declined. The precautionary savings motivation of rural residents will thus be dampened, leading to a decline in their savings rate. To sum up discussions above, we argue that medical insurance integration can significantly reduce rural households’ savings rate.

Research Design

Data Sources

The data used in this study is derived from two sources: household microdata is obtained from the China Labor-force Dynamics Survey (CLDS) for the years 2014, 2016, and 2018. CLDS, a large-scale interdisciplinary longitudinal survey, is conducted by the Center for Social Science at Sun Yat-sen University. This dataset employs a multi-stage, multi-level, and labor force scale-proportional probability sampling method. The sample covers 29 provinces and cities across China, encompassing 401 villages and urban communities, 14,214 households, and 23,594 individuals, ensuring national representativeness. Data of the aforesaid three years can cover the most important stages of health insurance integration in China. The data published by the CLDS in 2014 and 2015, respectively include the name of the municipal cities of respondents, while the data published in 2018 did not include the name of the municipal cities. So we match the data of the year 2018 with the data of the year 2016 by community coding to identify the information of the municipal city of respondents in 2018. This allows the information of municipal health insurance integration and the three-phase data of CLDS to be matched by the name of cities. We manually summarize the urban-rural medical integration information and the urban economic development data through open network channels.

The Empirical Models

According to the progressive promotion of urban-rural integration at the municipal level, we use the progressive Differences-in-Differences method to study the influence of urban-rural health insurance integration on rural household savings rate. This research model can be specified as below:

Where, i represents the family chosen for research, j denotes the prefecture-level city where the family is located, and t denotes the year. Y stands for the explained variable, namely the rural household savings rate; Treatjt stands for the core explaining variable, which is used to suggest whether the prefecture-level city has implemented health insurance integration one year before the prefecture-level city; X stands for the control variable influencing the domestic savings rate; λj denotes the dummy variable of the prefecture-level city, which is used to control the urban effect; δt denotes the dummy variable of the year, which can be used to control the time effect; εijt is an error item.

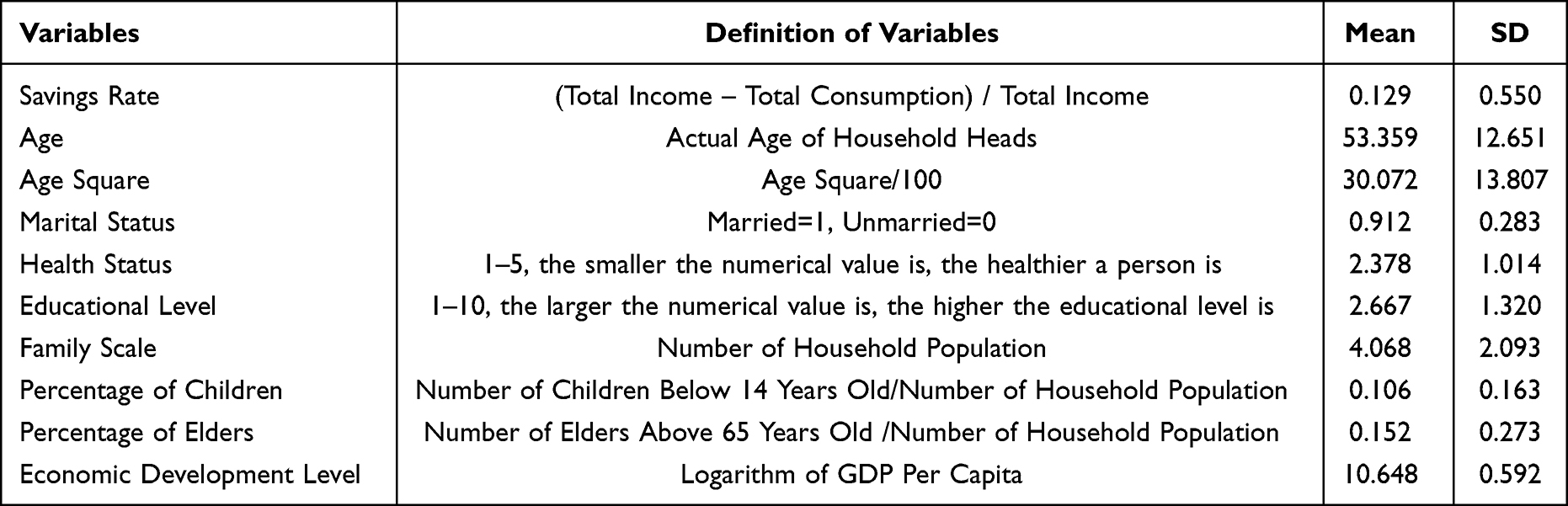

Variable Selection and Descriptive Statistics

Dependent Variable

The explained variable of this paper is the household savings rate which can be given by diving (gross household income – gross household consumption) with gross household income.

Independent Variable

The core explaining variable of this paper is the health insurance integration treatment variable. The data on household income and consumption in CLDS is based on the data from the previous year of the survey, so when assigning variables to health insurance integration, they are assigned based on the data from the previous year of the survey. If the municipal city where the rural household is located carried out the health insurance integration the year before, then the core explaining variable would take the value 1; otherwise, the core explaining variable would take the value 0.

Control Variable

Control variables of this paper include the household head characteristic variables, household characteristic variables, and city characteristic variable. The household head characteristic variables include the age, age square, marital status, and education background. The household characteristic variables include the family scale, percentage of children, and percentage of elders. The city characteristic variable includes the economic development level.

Sample selection was conducted in accordance with the research requirements. First, due to the presence of numerous outliers in the savings rate, this study excluded samples with total household income less than or equal to zero, and savings rates less than −1.5 or greater than 1. Secondly, as the primary focus of this study is on rural household savings, urban household samples were also eliminated. Finally, samples with unidentifiable city-level information were removed. The final dataset comprises a three-wave unbalanced panel consisting of 17,451 samples. Detailed definitions and descriptive statistics of the aforementioned variables are presented in Table 2.

|

Table 2 Descriptive Statistics of Variables |

From Table 2, it can be seen that the health status of sample households is 2.378 on average, with 2 indicating being relatively healthy and 3 indicating generally healthy. The sample household heads are relatively healthy. The educational level of household heads is 2.667 on average, with 2 representing graduating from primary schools and 3 representing graduating from middle schools. Therefore, the educational level of a majority of household heads is shorter than 9 years, which suggests a relatively low educational level among household heads. On average, children take up around 0.106 of the total, and elders take up 0.1522. This means the rural household structure is characterized by low fertility and aging.

Empirical Analysis

Benchmark Regression Results

Table 3 is the benchmark regression results. From Column (1) of Table 3, it can be seen that, before control variables are added, the urban-rural health insurance integration treatment variable coefficient is −0.047, which is significant at the significance level of 1%. This indicates that health insurance integration has brought down the savings rate. Column (2) of Table 3 displays regression results after characteristic variables of household heads, family characteristic variables and city characteristic variables are added. The health insurance integration treatment variable coefficient is −0.045, which is significant on the significance level of 5%. The core explaining variables of these two columns of results are not significantly different in terms of their coefficient and significance. Results stated above that, compared with regions having adopted health insurance integration, regions having adopted it can pronouncedly reduce the savings rate of rural households.

|

Table 3 Benchmark Regression Results |

According to Column (2) of Table 3, this paper further analyzes the influence of control variables on the savings rate. The age coefficient is negatively significant at the significance level of 1%. The age square coefficient is positive and significant at the significance level of 1%. This implies a U-shaped relationship between the household savings rate and the age of the household head. However, life cycle theory believes that rational decision-makers should save some money when they are young and then use the money thus saved when they are old. This can maximize the utilization of money within the life cycle. So age and savings rate should feature an inverted U-shaped correlation.23 Foreign scholars observe that age and savings rate of people in Western developed countries feature an obvious inverted U-shaped correlation.24

On the contrary, the counter-life-cycle phenomenon has been prevailing among the savings rate of Chinese families.1,25 A possible reason is that the middle-aged household heads are expected to bring up their offspring and support elders. Consequently, their household savings rate is relatively low among middle-aged household heads.26 The health status coefficient of these middle-aged household heads is −0.054, which is significant on the significance level of 1%. This suggests that the poorer the health status of household heads is, the lower their household savings rate will be. A potential reason is that poorer health can cause higher medical expenses, which will in turn reduce the savings rate. The educational level coefficient is positive and significant on the significance level of 1%. This provides solid evidence for the conclusion that the higher the educational level of household heads is, the higher the household savings rate will be. The higher the educational level is, the higher their income will be. Most of their income is converted into savings, which leads to an increase of the savings rate. The coefficient of the number of children is significantly negative on the significance level of 5%. The coefficient of the percentage of elders is significantly negative on the significance level of 1%. Based on that, we can conclude that the number of children and the number of elders can both significantly reduce the rural household rate. This is probably because that families are faced with an increasing amount of unexpected expenditure, which can lower the savings rate.

Robust Test

Replace the Explained Variable

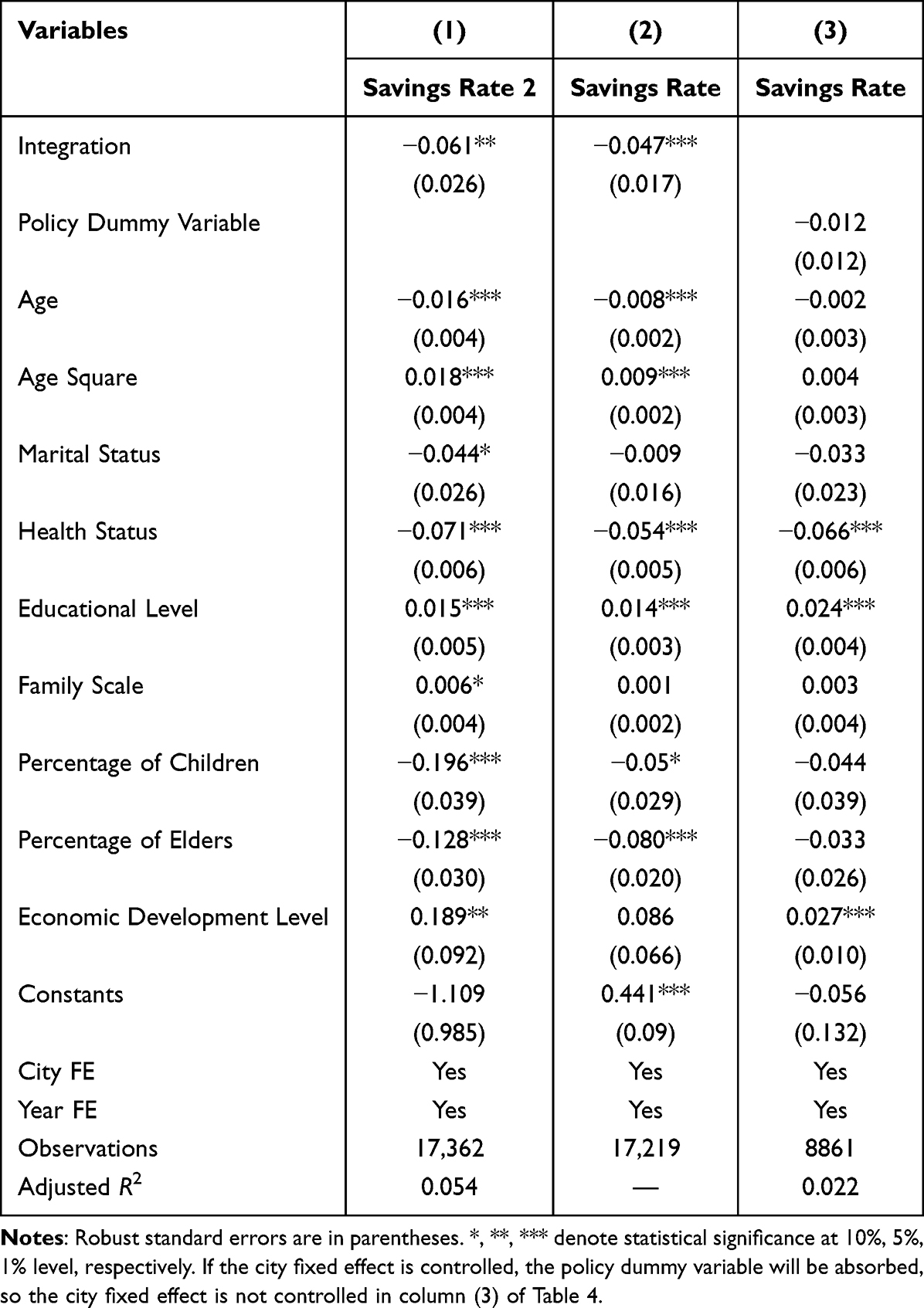

We adopt the definition of household savings rate by Chamon and Prasad, that is, replacing the regression of explained variables with the logarithmic value obtained by dividing the total household income with the total household consumption. The logarithmic value can effectively avoid the influence of extreme value on results.1 According to Column (1) of Table 4, the coefficient of urban-rural integration treatment variable is negative and is significant on the significance level of 5%. This means that after the explained variable is replaced, the conclusions obtained by benchmark regressions remain the same.

|

Table 4 Robust Test |

Replace the Measurement Model

In this paper, the lower and upper limit of the rural household savings rate are set to be −1.5 and 1, respectively. Therefore, the savings rate is a bounded variable. To prevent estimated results from any bias, Tobit model is used for re-estimation of the coefficient. According to Column (2) of Table 4, the coefficient of the health insurance integration treated variable is significantly negative at the significance level of 1%. The result suggests that, after the measurement model is replaced, the estimated results are still stable.

Counterfactual Hypothesis Test

Counter-facts are constructed to test whether there are significant differences between the experiment group and the control group before the implementation of policies. Specifically, the year 2014 and 2016 are adopted as the inspection periods, when urban-rural health insurance integration was not carried out. Prefecture-level cities which pursued health insurance integration in 2018 took the value of 1. Prefecture-level cities which did not seek urban-rural integration in 2014, 2016, and 2018 are defined as the contrast group, which take the value, 0. Theoretically, in 2014 and 2016 before urban-rural health insurance integration, the rural household savings rate of the experiment group and the control group is not significantly different. The policy dummy variable, D, is substituted into equation (1) to replace the urban-rural health insurance integration treated variable for regression. The results are shown in Column (3) of Table 4. It can be seen that the coefficient of the policy dummy variable failed to pass the significance test, which suggested that the counterfactual hypothesis passed the test.

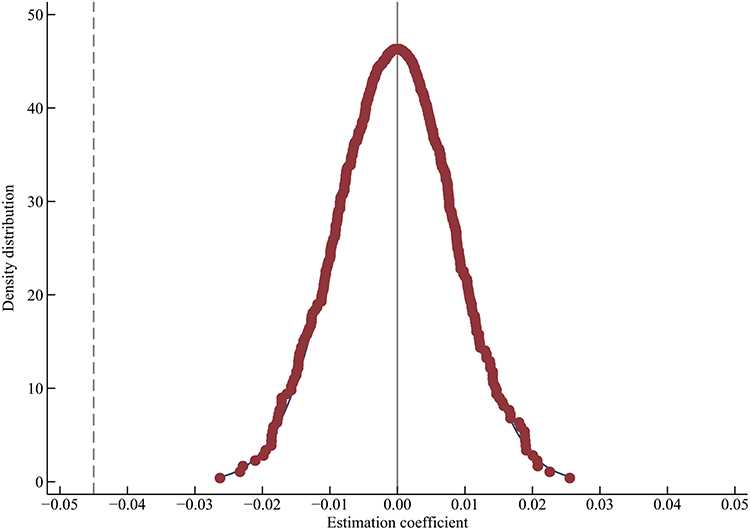

Placebo Test

To avoid the potential influence of random factors on benchmark results, we follow the practice of Liu and Lu.27 First, we randomly distribute the treated variables of the health insurance integration policy. After 500 times of repeated sampling and regression, we obtain the coefficient nuclear density distribution in Figure 1.

|

Figure 1 Placebo test. |

Theoretically, the experiment group and the control group were randomly distributed. The treated variable will not significantly influence the result variables. From Figure 1, it can be seen that the density distribution graph of the estimation coefficient randomly sampled features a normal distribution with the average value as 0. The estimation coefficient of random sampling is larger than the actual coefficient of benchmark regression. This suggests significant placebo test effects. Therefore, the benchmark regression results are not driven by factors not observed.

Mechanism Test

Motivation theory of precautionary savings believes that families tend to cope with risks of uncertainties with precautionary savings. Urban-rural health insurance integration has improved the medical care level, thus helping better the medical service utilization and health status of rural residents. Therefore, urban-rural health insurance integration can theoretically weaken the motivation of precautionary savings to exert an influence on the household savings rate.

Health Risk Mechanism

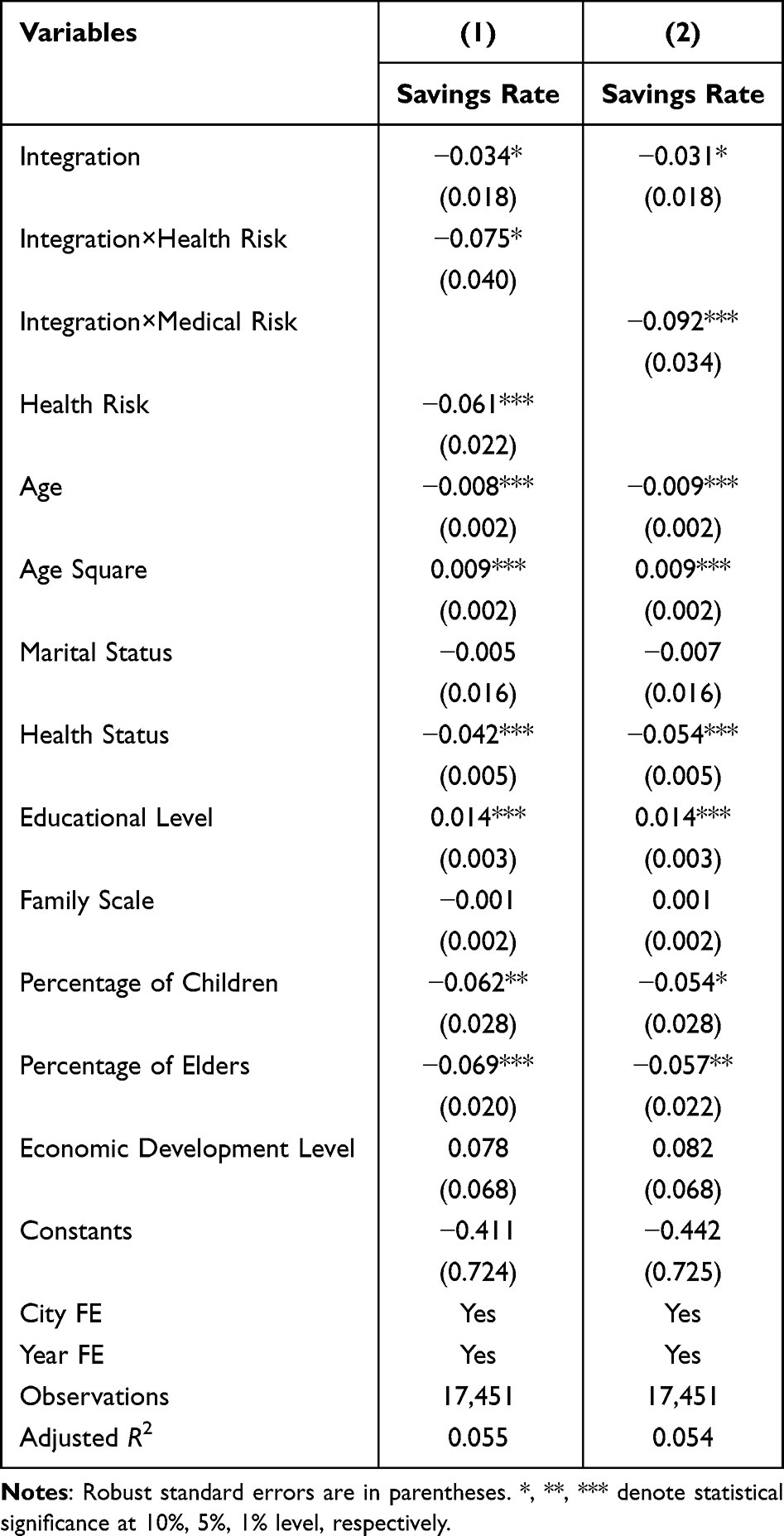

In this paper, we use the number of family members in poor health to measure the health risk facing a family. The higher the number of family members in poor health is, the higher the health risk will be facing the family. In order to verify that urban-rural health insurance integration can lower the household savings rate through alleviation of the health risk, we create an interaction item between the treated item of health insurance integration and the health risk. It can be observed from Column (1) of Table 5 that the interaction item coefficient between the medical health treated variable and the health risk is −0.075, which is significant at the significance level of 10%. This means that medical health integration has a stronger influence on the savings rate of families with a high health risk. Therefore, health insurance integration can influence the household savings rate of rural households by alleviating the health risk.

|

Table 5 Health Insurance Integration and Precautionary Savings |

Medical Risk Mechanism

Generally, the elder the individuals is, the higher the medical risk is. In this paper, we use the percentage of elders above 65 years old to measure the medical risk. A higher percentage of elders is usually associated with a higher health risk. To confirm that medical health integration leads to alleviation of medical risk and then a drop in the household savings rate, we make the interaction item between the treated variable of urban-rural health care integration and the medical risk. Column (2) of Table 5 shows that the interaction coefficient between the two variables is significantly negative at the significance level of 1%. This suggests that urban-rural health care integration can affect more the savings rate of families with a high medical risk. So it is apt to say that urban-rural health insurance integration can affect the household savings rate by bringing down the medical risk.

Heterogeneity Analysis

Heterogeneity Analysis Based on the Age of the Household Head

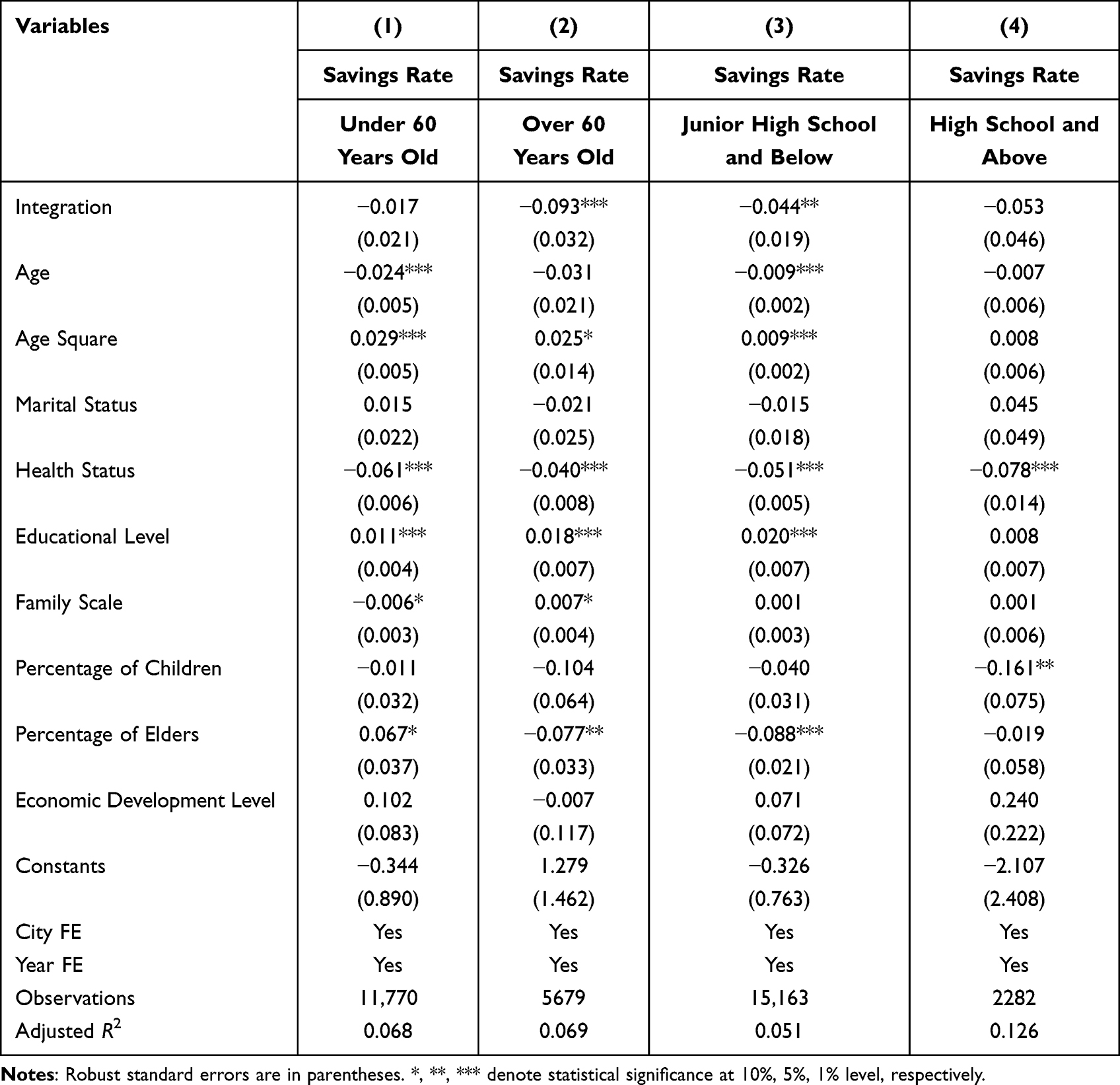

To examine whether the influence of urban-rural medical insurance integration on the rural household savings rate differs because of rural household heads’ age differences, we divide rural household heads into two age groups, including the low age group and the high age, with 60 years old as the division. Then, the age groups are all substituted into equation (1) for regression. According to Column (1) of Table 6, the urban-rural health insurance integration treated variable coefficient is negative but not significant. This means that urban-rural health insurance integration cannot significantly reduce the savings rate of rural households whose rural household head’ age is below 60 years old. Column (2) of Table 6 suggests that the coefficient of the urban-rural health insurance integrated treated coefficient is −0.093, which is significant at the significance level of 1%. This means that urban-rural health insurance integration has significantly brought down the savings rate of rural households whose household heads are above the age of 60.

|

Table 6 Heterogeneity Analysis |

Heterogeneity Analysis Based on the Educational Level of the Household Heads

Next, we put households whose household heads complete the middle school or lower into one group, and households whose household heads complete the senior high school or above into the other group. Doing so can help take a look into whether the influence of urban-rural health insurance integration varies because of the difference of rural household heads’ educational level. Then, these two groups are substituted into equation (1) for regression, respectively. The urban-rural health insurance integration treated variable coefficient is −0.044, which is significant at the significance level of 5%. Therefore, urban-rural health insurance integration can significantly reduce the savings rate of rural households whose households heads hold a low educational level. Results presented in Column (4) of Table 6 show that the health insurance integration treated variable coefficient is negative, but it fails to pass the significance test. This means that health insurance integration cannot significantly reduce the savings rate of rural households whose household heads hold a high educational level.

Heterogeneity Analysis Based on the Gender of the Household Head

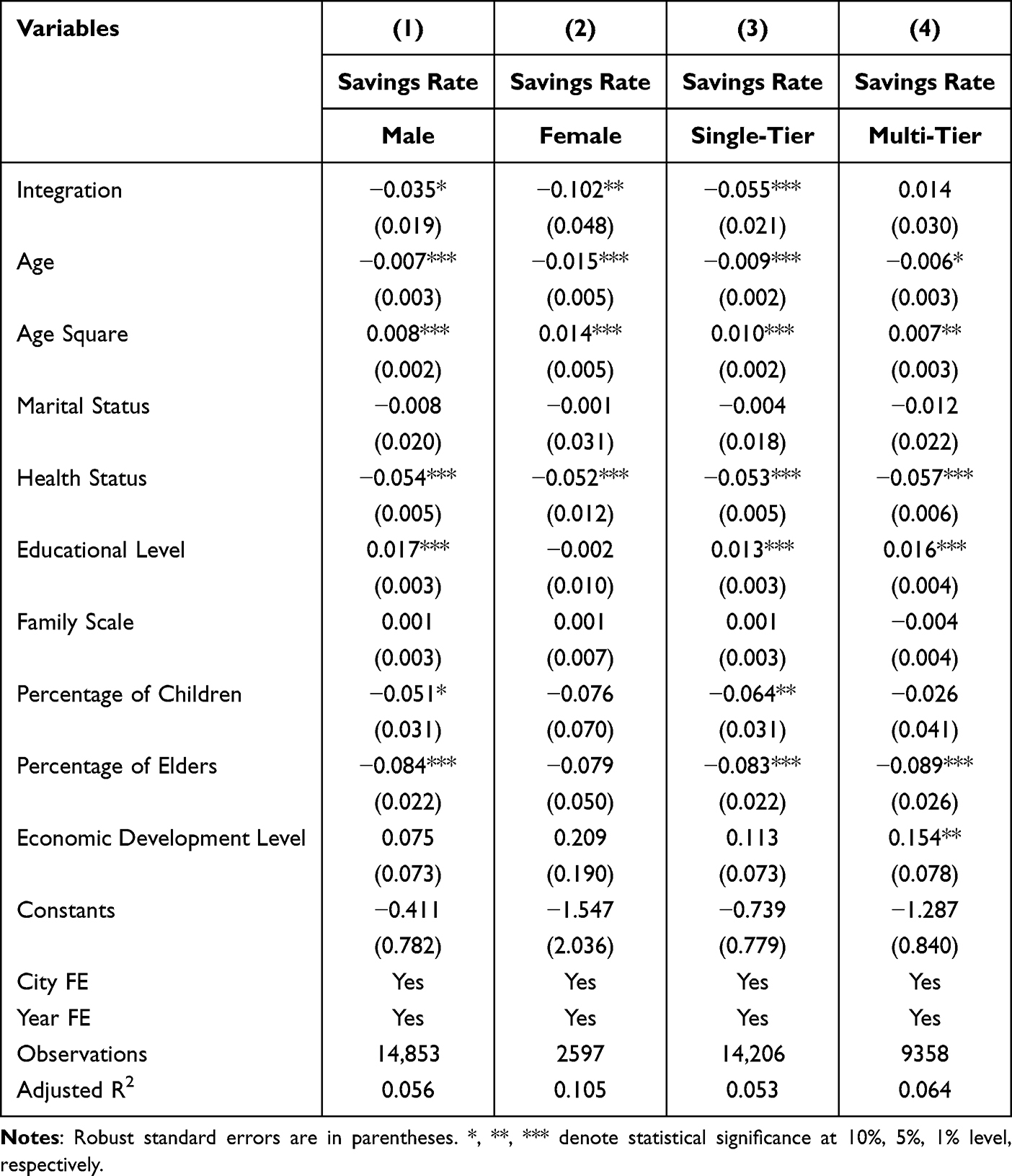

To examine whether the impact of medical insurance integration on the savings rates of rural households varies by the gender of the household head, this study divides the sample into male-headed and female-headed households, and then regresses them separately using equation (1). As shown in column (1) of Table 7, the coefficient for the medical insurance integration treatment variable is −0.035 and significant at the 10% level; the results in column (2) of Table 7 indicate that the coefficient for the medical insurance integration treatment variable is −0.102 and significant at the 5% level. These results suggest that the impact of medical insurance integration on the savings rates is more pronounced in households headed by women.

|

Table 7 Heterogeneity Analysis |

To sum up, the influence of urban-rural household integration on the rural household savings rate is heterogeneous in terms of the household heads’ age, educational level, and gender of the household head. A possible reason is that, compared with rural households whose household heads are younger in age, higher in educational level and male head of household, rural households with rural households whose household heads are older, lower in educational level and female head of household are faced with more uncertainties. Urban-rural health insurance integration has improved the income level of households of this kind, and weakened their precautionary savings motivation, thereby bringing down the savings rate of rural households of this type.

Heterogeneity Analysis Based on the Integration Model

We further examine the influence of two health insurance integration models on the rural household savings rate. In order to study effects of the “single-tier” integration model, we eliminate cities adopting the “multi-tier” system as the experimental group, and cities not adopting health insurance integration as the control group for regression. Results of Column (3) of Table 7 suggest that the health insurance integration treated variable coefficient is −0.055, which is significant at the significance level of 1%. This means that implementing the “single-tier” system health insurance integration model can significantly reduce the rural household savings rate.

To investigate effects of the “multi-tier” system integration model, we eliminate cities implementing the “first-tier” system but maintain cities maintaining the “multi-tier” system. Cities not carrying out health insurance integration are defined as the control group for regression. Results in Column (4) of Table 7 show that the health insurance integration treated variable coefficient is not statistically significant, which means that the health insurance integration model implementing the “multi-tier” system has not influenced the rural household savings rate.

A main reason behind the aforesaid results is that, though the grading system allows rural residents to freely choose their insurance tier, chances are low for rural residents to choose a high-tier insurance. There are no substantial differences between the low-tier system and the former new-type rural cooperative medical care system. Health insurance integration has actually failed to effectively improve rural residents’ treatment level. Nor has it influenced the savings rate of rural households.

Conclusions and Discussion

A high savings rate is an obvious phenomenon in the process of China’s economic development, because rural residents show a strong savings propensity. Reducing the savings rate and expanding consumption are of vital importance to realize the domestic cycle. The social insurance system is a critical factor affecting residents’ savings. Theoretically, health insurance integration can improve the medical care level of rural households, thus weakening their precautionary savings motivation and influencing their domestic savings. Based on the step-by-step progression of health insurance integration, we match the health insurance integration information manually collected from different places with three phases of data of CLDS collected in 2014, 2016 and 2018, respectively. Empirical research reveals the influence of health insurance integration on the rural household savings rate.

The findings from this study provide crucial insights into the impacts of medical insurance integration on rural households in China. Firstly, the integration of medical insurance has successfully reduced the health and medical risks faced by rural families. This reduction has weakened the motive for precautionary savings, resulting in a decline in the savings rate. Given the widespread implementation of medical insurance integration across Chinese cities, there is a need for continuous improvement in the basic medical insurance system for urban and rural residents. This includes establishing a dynamic financing mechanism that aligns with economic development levels, expanding the medical insurance catalog, and increasing public fiscal subsidies for medical insurance payments where financially feasible. Special attention should be given to channeling medical public finance and healthcare resources towards vulnerable rural groups and optimizing the design of the supporting systems for basic medical insurance for urban and rural residents.

Secondly, the study highlights the heterogeneous impact of medical insurance integration on savings rates. The integration has a more pronounced effect on households with older heads and lower education levels, likely due to these groups facing higher health and medical risks, which the integration effectively reduces. This suggests the need for a targeted allocation of medical and health resources towards such demographics.

Thirdly, the more substantial impact of the single-tier model on household savings rates suggests that simplified and unified policies could be more effective in achieving the desired economic impacts. In contrast, the multi-tier system’s negligible effect on savings rates may point to the complexity or inefficiency in its implementation or design. Consequently, regions employing a multi-tier system are advised to diligently pursue the consolidation into a single-tier framework, in accordance with the policy mandate that urban and rural areas align under uniform funding standards, identical coverage and payment criteria, a consistent catalog of health insurance-covered medicines and services, standardized management approaches for designated health insurance institutions for urban and rural residents, and unified health insurance fund management systems.

Overall, these findings have important implications for policy-making in the realm of healthcare insurance. The current phase of medical insurance integration, primarily involving the integration of Urban Resident Basic Medical Insurance (URBMI) and the New Rural Cooperative Medical Scheme (NRCMS), represents only a stage in the broader reform of the medical insurance system. The ultimate goal is to establish a completely unified medical insurance system for urban and rural areas, integrating urban employee medical insurance, URBMI, and NRCMS into a single social basic medical insurance system (“three-insurance integration”). Achieving “three-insurance integration” would maximally reduce the disparities in medical insurance benefits between urban and rural areas, enhance the healthcare security for rural residents, and impact their economic behaviors. Encouraging regions with the capability to actively explore effective models and feasible paths for “three-insurance integration” can provide valuable experiences for other cities planning similar reforms.

Abbreviations

CLDS, China Labor-force Dynamics Survey; DID, Difference-in-differences.

Data Sharing Statement

Please contact Zhiguang Li for data requests.

Ethics Approval and Consent to Participate

Not applicable. The CLDS is a publicly available dataset that has been anonymized and de-identified prior to its release. This dataset is considered secondary data, with no direct interaction between our research team and the subjects of the survey. The anonymization process undertaken by the CLDS ensures that individual respondents cannot be identified, thereby mitigating privacy and confidentiality concerns. Given these characteristics, our study falls within the scope of research activities that do not typically require IRB review.

Author Contributions

All authors made a significant contribution to the work reported, whether that is in the conception, study design, execution, acquisition of data, analysis and interpretation, or in all these areas; took part in drafting, revising or critically reviewing the article; gave final approval of the version to be published; have agreed on the journal to which the article has been submitted; and agree to be accountable for all aspects of the work.

Funding

This study benefited from research grants of Collaborative Innovation Program of Anhui Provincial Education Department (Grant No. GXXT-2022-095), Excellent Youth Research Program of Anhui Provincial Education Department (Grant No. 2023AH030071) and Youth Talent Program of Anhui University of Chinese Medicine (Grant No. 2021qnyc12;No. 2023rcyb015).

Disclosure

The authors declare that they have no competing interests.

References

1. Chamon MD, Prasad ES. Why are saving rates of urban households in China rising? Am Econ J-Macroecon. 2010;2(1):93–130. doi:10.1257/mac.2.1.93

2. Chamon M, Liu K, Prasad E. Income uncertainty and household savings in China. J Dev Econ. 2013;105:164–177. doi:10.1016/j.jdeveco.2013.07.014

3. Gruber J, Yelowitz A. Public health insurance and private savings. J Polit Econ. 1999;107(6):1249–1274. doi:10.1086/250096

4. Alessie R, Angelini V, van Santen P. Pension wealth and household savings in Europe: evidence from SHARELIFE. Eur Econ Rev. 2013;63:308–328. doi:10.1016/j.euroecorev.2013.04.009

5. Zuo F, Zhai SG. The influence of china’s covid-19 treatment policy on the sustainability of its social health insurance system. Risk Manag Healthc P. 2021;14:4243–4252. doi:10.2147/Rmhp.S322040

6. Engelhardt GV, Kumar A. Pensions and household wealth accumulation. J Hum Resour. 2011;46(1):203–236.

7. Lachowska M, Myck M. The effect of public pension wealth on saving and expenditure. Am Econ J-Econ Polic. 2018;10(3):284–308. doi:10.1257/pol.20150154

8. Huang X, Wu BX. Impact of urban-rural health insurance integration on health care: evidence from rural China. China Econ Rev. 2020;64. doi:10.1016/j.chieco.2020.101543

9. Zhou Q, He Q, Eggleston K, Liu GG. Urban-rural health insurance integration in China: impact on health care utilization, financial risk protection, and health status. Appl Econ. 2022;54(22):2491–2509. doi:10.1080/00036846.2021.1998323

10. Yang D, Acharya Y, Liu XT. Social health insurance consolidation and urban-rural inequality in utilization and financial risk protection in China. Soc Sci Med. 2022;308. doi:10.1016/j.socscimed.2022.115200

11. Horioka CY, Wan JM. The determinants of household saving in China: a dynamic panel analysis of provincial data. J Money Credit Bank. 2007;39(8):2077–2096. doi:10.1111/j.1538-4616.2007.00099.x

12. Wei SJ, Zhang XB. The competitive saving motive: evidence from rising sex ratios and savings rates in China. J Polit Econ. 2011;119(3):511–564. doi:10.1086/660887

13. Li HB, Zhang H, Zhang JS. Effects of longevity and dependency rates on saving and growth: evidence from a panel of cross countries. J Dev Econ. 2007;84(1):138–154. doi:10.1016/j.jdeveco.2006.10.002

14. Hubbard RG, Skinner J, Zeldes SP. Precautionary saving and social insurance. J Polit Econ. 1995;103(2):360–399. doi:10.1086/261987

15. Blanchard O, Giavazzi F. Rebalancing growth in China: a three-handed approach. China World Econ. 2006;14(4):1–20. doi:10.1111/j.1749-124X.2006.00027.x

16. Dynan KE. How prudent are consumers? J Polit Econ. 1993;101(6):1104–1113. doi:10.1086/261916

17. Chou S-Y, Liu J-T, Hammitt JK. National health insurance and precautionary saving: evidence from Taiwan. J Public Econ. 2003;87(9–10):1873–1894. doi:10.1016/s0047-2727(01)00205-5

18. Guariglia A, Rossi M. Private medical insurance and saving: evidence from the British household panel survey. J Health Econ. 2004;23(4):761–783. doi:10.1016/j.jhealeco.2003.11.002

19. Starr-McCluer M. Health insurance and precautionary savings. Am Econ Rev. 1996;86(1):285–295.

20. Maynard A, Qiu JP. Public insurance and private savings: who is affected and by how much? J Appl Economet. 2009;24(2):282–308. doi:10.1002/jae.1039

21. Lei XY, Lin WC. The new cooperative medical scheme in rural China: does more coverage mean more service and better health? Health Econ. 2009;18(S2):25–46. doi:10.1002/hec.1501

22. Yip W, Hsiao WC. Non-evidence-based policy: how effective is China’s new cooperative medical scheme in reducing medical impoverishment? Soc Sci Med. 2009;68(2):201–209. doi:10.1016/j.socscimed.2008.09.066

23. Bosworth B, Burtless G, Sabelhaus J, Poterba JM, Summers LH. The decline in saving: evidence from household surveys. Brook Pap Econ Act. 1991;22(1):183–256. doi:10.2307/2534640

24. Attanasio OP. Cohort analysis of saving behavior by US households. J Hum Resour. 1998;33(3):575. doi:10.3386/w4454

25. Ge SQ, Yang DT, Zhang JS. Population policies, demographic structural changes, and the Chinese household saving puzzle. Eur Econ Rev. 2018;101:181–209. doi:10.1016/j.euroecorev.2017.09.008

26. Wan G, Shi Q, Tang S. Saving behavior in a transition economy: an empirical case study of rural China. J Econ Res. 2003;5:3–12+91. (In Chinese).

27. Liu Q, Lu Y. Firm investment and exporting: evidence from China’s value-added tax reform. J Int Econ. 2015;97(2):392–403. doi:10.1016/j.jinteco.2015.07.003

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.