")

Back to Journals » Risk Management and Healthcare Policy » Volume 14

The Magnitude of Satisfaction and Associated Factors Among Household Heads Who Visited Health Facilities with Community-Based Health Insurance Scheme in Anilemo District, Hadiya Zone, Southern Ethiopia

Authors Addise T , Alemayehu T , Assefa N , Erkalo D

Received 11 November 2020

Accepted for publication 1 January 2021

Published 13 January 2021 Volume 2021:14 Pages 145—154

DOI https://doi.org/10.2147/RMHP.S290671

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Professor Marco Carotenuto

Teketel Addise,1 Tadesse Alemayehu,2 Nega Assefa,2 Desta Erkalo3

1Anilemo District Health Office, Hadiya Zone, Southern Ethiopia; 2College of Health and Medical Sciences, Haramaya University, Harar, Ethiopia; 3College of Medicine and Health Sciences, Wachemo University, Hosanna, Ethiopia

Correspondence: Desta Erkalo

College of Medicine and Health Sciences, Wachemo University, Hosanna, Ethiopia

Email [email protected]

Background: Community-based health insurance (CBHI) schemes are an emerging strategy for providing financial protection against healthcare-related poverty. In Ethiopia, CBHI is being piloted in 13 districts, but community experience and satisfaction with the scheme have yet to be studied.

Objective: To assess the magnitude of satisfaction and associated factors among household heads who visited health facilities with community-based health insurance schemes in the Anilemo district Hadiya Zone Southern Ethiopia.

Methods: A community-based cross-sectional study design was conducted for 627 household heads in the Anilemo district, from March 1– 30, 2020. Study participants were selected using stratified random sampling for kebeles and systematic sampling for study households. Data were collected by trained data collectors using a pre-tested structured questionnaire. Descriptive statistics, bivariate, and multivariate logistic regression analyses were performed. P values less than 0.05 with 95% confidence intervals were used to determine associations between independent and dependent variables.

Results: The magnitude of household heads’ satisfaction was 54.1%. Household heads age [AOR=1.70;95% CI 1.09– 2.67], households income [AOR=0.19; 95% CI 0.11– 0.35], knowledge of CBHI benefit packages [AOR=3.15; 95% CI 1.97– 5.03], agreement with laboratory services [AOR=2.25; 95% CI 1.40– 3.62], and got and agreed with prescribed drugs [AOR=2.69; 95% CI 1.66– 4.37] were significantly associated with the magnitude of household heads satisfaction with community-based health insurance.

Conclusion: About half of the household heads who visited health facilities with CBHIS were satisfied. Age, household’s income, knowledge of CBHI benefit packages, agreement with laboratory service provision, availability and agreement with prescribed drugs were significant predictors of satisfaction with CBHI. Therefore, much effort could be required to increase the magnitude of the household head’s satisfaction with the scheme.

Keywords: community-based health insurance, satisfaction, household heads

Introduction

The global community has committed to working together to achieve universal health coverage (UHC) by 2030 as part of the Sustainable Development Goals. Despite this, at least half of the world’s population still lacks access to essential health services. Consequently, a large number of people are being pushed into poverty by having made to spend much of their household budgets on health care expenses. Globally, each year around 150 million people suffer from financial disaster, and about 100 million are driven into poverty due to excessive out of pocket bills for health, from these maximum of them are from developing countries.1–4

Ethiopia is dedicated to achieving universal health coverage (UHC) – expanding high-quality health care services which might be available, affordable, accessible, and acceptable to all households.5 Due to financial risk protection is a critical component of UHC, Ethiopia has begun launching a comprehensive and sustainable financial risk protection with a health insurance scheme. The social health insurance (SHI) scheme has been all started for formal sectors, and final preparations are being made to implement the initiative entirely. In the informal area – which comprises over 85% of Ethiopians, community-based health insurance (CBHI) is being expanded.4,6,7

The overall enrollment rate inside the pilot districts reached about 52% of the target population. When we see within the country level, the current enrolment rate in 509 CBHI functional regions is 44%, of which 85% are paying members, and the remaining have subsidized membership.6

Recent reports of Ethiopia Health Insurance Agency (EHIA) indicates that there is low population coverage of 28% (in-country level) compared to the target set in HSTP, 80%, and only 77% of CBHI enrolled households are renewing their membership cards that mean 23% of them are dropped out from CBHI enrollment due to dissatisfaction with CBHI scheme. This dropout rate is also increased by 10% in the Southern region (SNNPR). Due to this, the goal of EHIA that want to make total coverage of CBHI in 2025 is in great question.6,8

Several studies showed that socio-demographic characteristics such as sex, age, marital status, educational level, occupation, family size, and household’s economic situation affect enrollee’s satisfaction with health insurance.9–12 In addition to socio-demographic factors, health service-related factors also influence enrollee’s satisfaction with CBHI. Satisfaction to CBHI is positively associated with the enrollee’s perception of proper laboratory service provision, health provider’s friendliness, weighting time, and availability of medicines.9–13 Furthermore, studies in developing countries have shown that satisfaction with the health insurance scheme is influenced by the enrollee’s knowledge of health insurance benefit packages.9–12,14 Besides, community-based health insurance (CBHI) experience-related determinants are also affected by the household head’s satisfaction with the scheme.11

In the Anilemo district even though there is high (80%) coverage of households in CBHIS, there is also a high dropout rate (33%), and high enrollment complaints were reported from the district CBHI facilitating office. The community-based health insurance (CBHI) scheme has been scaled up in this study area since the end of 2016. However, the enrollee’s magnitude of satisfaction and associated factors are not yet known. Hence, whether this scheme satisfies enrollees and they have a positive perception towards the CBHI scheme is unknown so far in this study area. Up to the level of our knowledge, only two related studies were conducted in Ethiopia. The first study conducted in the Damatoyda district assessed overall satisfaction by asking only six questions. Asking only six questions to evaluate household heads satisfaction might not be enough, and both studies did not stratify urban and rural enrolls before sample size selection. Besides, the household’s wealth index assessment method is not reliable. Therefore, this study addressed these gaps to assess the knowledge gap on household heads’ magnitude of satisfaction and other associated factors with a community-based health insurance scheme.

Methods and Materials

Study Area and Period

The Community-based cross-sectional study was conducted in the Anilemo districts, Hadiya Zone, Southern Ethiopia, from March 1–30 2020. The district is located 218km south of Addis Ababa (the capital city of Ethiopia), 200km North of Hawassa (the capital city of SNNPR), and 18km East from Hosanna town (capital of Hadiya Zone). In 2019/20, according to the 2007 Ethiopia census projection, the district has an estimated total population of 98,650, of which 48,832 (49.5%) males, and 49,818 (50.5%) females.15 Regarding health infrastructure, there are 28 health posts, five health centers, eight private clinics, three drug stores, and one drug vendor in the district. All health centers have linkages with the CBHI scheme.

Sample Size Determination

To determine the study sample size, the prevalence of the dependent and independent variables associated with the outcome variable from previous literature was considered. The required sample size for this objective was determined using the formula for a single population proportion with the following assumptions: Confidence level at 95% = 1.96 Margin of error = 0.05 magnitude of satisfaction with CBHI scheme to be 54.7%9 and the design effect of 1.5 to account for the multi-stage level of sampling method, Then by adding 10% non-respondent rate resulted in the total sample required for the study to be 627.

Sampling Technique and Procedure

A multi-stage sampling technique was employed to select the study participants. We applied simple random sample selection at each stage to eliminate selection bias. First, all the kebeles (the smallest administrative levels in the country) were stratified into urban and rural kebeles. Then 1 out of 2 urban kebeles and 8 out of 26 rural Kebeles were selected using simple random sampling (by lottery method). In the second stage, households enrolled and visited health facilities with CBHI in the selected kebeles were identified using their enrollment identification numbers from the monthly report registration book (the book that was written for the financial report from health centers to woreda CBHI facilitating office were used). Then, the sample size is proportionally allocated to each kebele. Finally, the study participants were selected using systematic random sampling methods.

Data Collection Tools

Data collection questionnaires were adapted from previous similar studies after repetitive reviewing.9–13 The tool includes five sections, such as socio-demographic characteristics (9 items), the experience of household heads in the CBHI scheme (5 items), household heads knowledge of benefit packages (7 items), Health service provision related (four items), household heads overall satisfaction (9 pieces by using a five-point Likert scale from strongly disagree=1 to strongly agree=5). The scale internal reliability was checked by Cronbach’s Alpha value, which is 0.980.

Operational Definition

Health Insurance

Health insurance is a system where individuals or households pay small contributions or prepayments to get health services at the time of illness and to protect them from catastrophic health expenditures.

The Magnitude of Satisfaction

Household heads positive feeling level about the CBHI scheme. Nine items related to satisfaction on a five-point Likert scale from strongly disagree = 1 to strongly agree =5 were asked. Then, the household head was leveled, as satisfied if his/her sum responses were greater or equal to the median value of the total sum score. Otherwise, leveled as not satisfied. This scoring was taken from similar studies.9,12 (Negatively stated questions were inversely recoded).

Household Heads Knowledge of CBHIS

It assesses knowledge of the basic benefit packages of the health insurance scheme. Household heads who answered above the median score of correct answers were categorized as having good knowledge. Household heads who responded below and equaled with a median score of correct answers were categorized as having poor knowledge. This scoring method was taken from similar studies.9

Wealth Indexes

The scores which show the respondents’ household economic status. It is determined by using the respondents’ reported assets, sanitary conditions, housing conditions, dwelling construction, water source, and other vital items in the household. The total score constituted the wealth index score, which was calculated by principal component analysis, and enrolls divided into three classes: low income, medium income, and high income enrolls.

Data Quality Control

To ensure the quality of data, the questionnaire was translated from English to the local Hadiyisa language and back to English. The questionnaire was pretested at 5% CBHI enrolls in Bandalicho kebele to assess clarity, consistency, understandability, and the total time that it was taken to finish the questionnaire before the actual data collection. Then, the necessary comments and feedbacks were incorporated into the final tool to improve its quality. The training was given for both data collectors and supervisors for two days regarding the objective of the study, data collection tool, ways of data collection, and checking the completeness of the collected data. Supervisors did strict supervision. Supervisors checked for completeness, clarity, and consistency throughout the data collection period. All of the collected data were given to the supervisors daily, and any missing data were confirmed before the next day. The principal investigator did the overall supervision. Double data entry was done to make a comparison of two data cells and correct mismatches.

Data Processing and Analysis

The collected data were checked for completeness, cleaned, coded manually, and entered into Epi-Data version 3.1, and exported to SPSS version 22 statistical package for analysis. The family wealth index was done by using the principal component analysis (PCA) method by considering locally available household assets and categorized them into three (low, medium, and high). Seven items were also used to measure knowledge of household heads on CBHI benefit packages by using yes=1 and no =0 questions these questions are: 1, CBHI is a good way of helping clients to health expenditure 2. CBHI covers only care from public health institutions, 3. CBHI covers only care within the country, 4. CBHI covers outpatient services in public hospitals and health centers, 5. CBHI covers inpatient services in public hospitals and health centers, 6. CBHI does not cover the transportation fee, 7. CBHI does not cover medical care for cosmetic value. After summing up their responses, they recorded a minimum score of 2, a maximum score of 7, and by using spss, we got a median score of 5. By using the median score, we dichotomized enrolls either have good knowledge or have poor knowledge. The outcome variable was completed by asking nine questions by using five points Likert scale (from strongly disagree=1 up to strongly agree=5). These nine questions are 1) local CBHI is trustworthy, 2) satisfied with the collection process of insurance card, 3) satisfied with time to make use of the CBHI program after registration, 4) satisfied with the schedule for paying a premium, 5) satisfied with the information provided, 6) satisfied with permitted insurance, 7) satisfied with CBHI benefit packages, 8) want to stay enrolled and, 9) After adding all nine responses, we got a total satisfaction score for each individual ranging from 10–45. From this total satisfaction by using SPSS we got a median value=41. By using this median value (41) as a cutoff point, we have a dichotomized dependent variable either satisfied (total satisfaction ≥41) or not satisfied (total satisfaction <41). A binary logistic regression model was used to identify factors associated with the level of household head’s satisfaction with the CBHI scheme. All variables with a p-value <0.25 in bivariate analyses were included in the final model of multivariate analyses to control all possible confounders. The multi co-linearity test was checked to see the correlation between independent variables by using standard error. The goodness of fit test was checked by Hosmer-Lemeshow’s test was found to insignificant (p-value=0.06), an omnibus test was significant (p-value=0.00), which indicates the model was fitted. Adjusted odds ratio (AOR) along with 95% CI was estimated to identify factors associated with the magnitude of household heads satisfaction with the CBHI scheme by using multivariable logistic regression analysis. Finally, variables whose p<0.05 in multivariable logistic regression were considered as the cutoff point for statistical significance.

Ethical Consideration

Ethical clearance was obtained from Haramaya University, College of Health and Medical Sciences, the Institutional Health Research Ethics Review Committee (IHRERC). The study was conducted in accordance with the Declaration of Helsinki. A formal letter of permission and support were written to the Anilemo district health office. Then, the Anilemo district health office has written a cooperation letter for all kebeles in which the study was carried out. All the study participants were informed about the purpose of the study and their right to refuse. Then, written and signed informed, voluntary consent was obtained from all study participants before data collection.

Results

Socio-Demographic Characteristics of Household Heads Who Visited Health Facilities with CBHIS

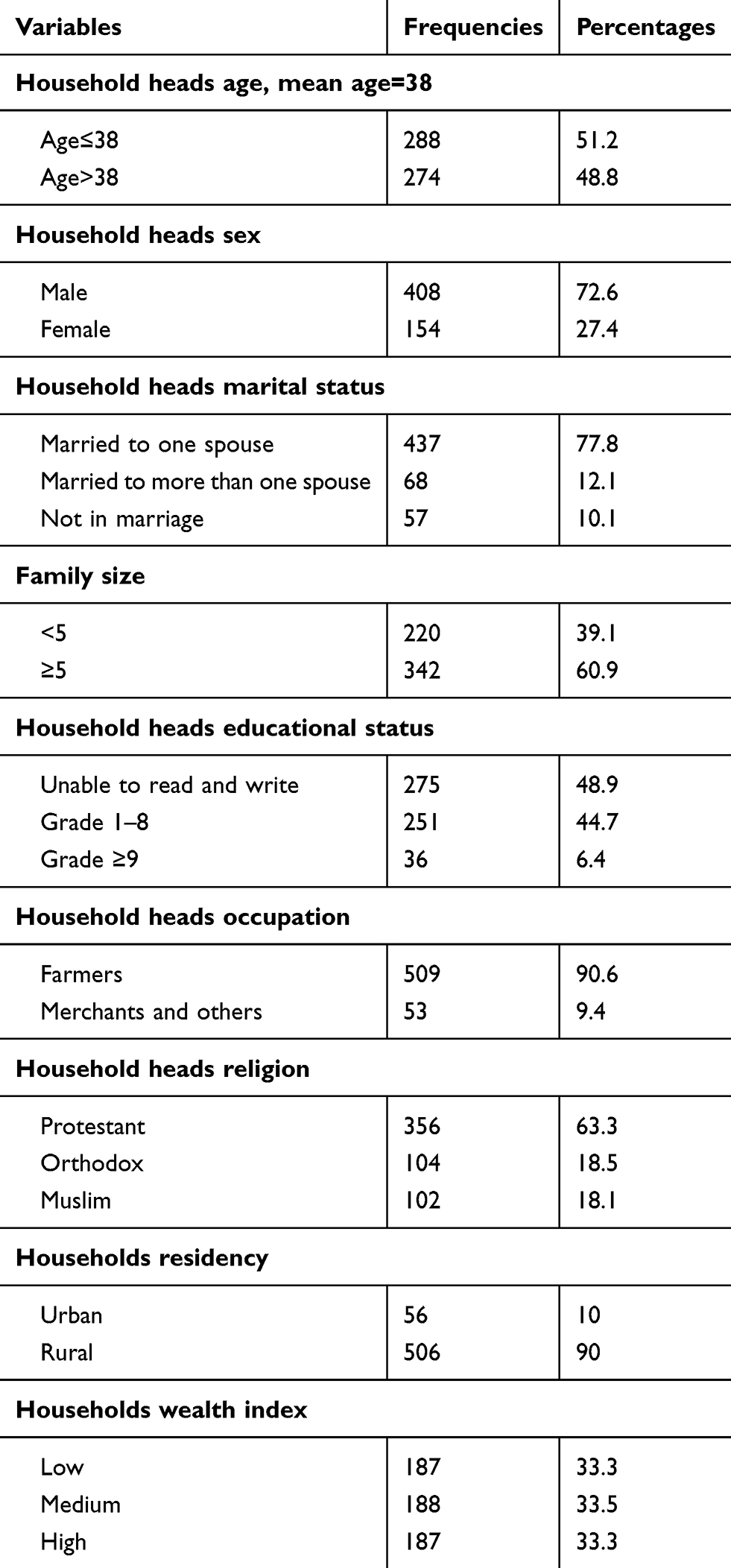

Five hundred sixty-two household heads had participated in this study, yielding a response rate of 90%. Of these, 408 (72.6%) were male. The mean age of participants was 38 years. The majority of respondents (77.8%) were married to one spouse. More than half 342 (60.9%) of the household heads had greater than five family members. Regarding education, 275 (48.9%) of participants did not attend formal education. Nearly 90% of the study participants were farmers by their occupation. Related to the family wealth index 187 (33.3%) of households income was high (Table 1).

|

Table 1 Distribution of Socio-Demographic Characteristics of Household Heads Who Visited Health Facilities with CBHIS in Anilemo District, Hadiya Zone, Southern Ethiopia, 2020 |

Experience of Household Heads Who Visited Health Facilities with CBHI Scheme

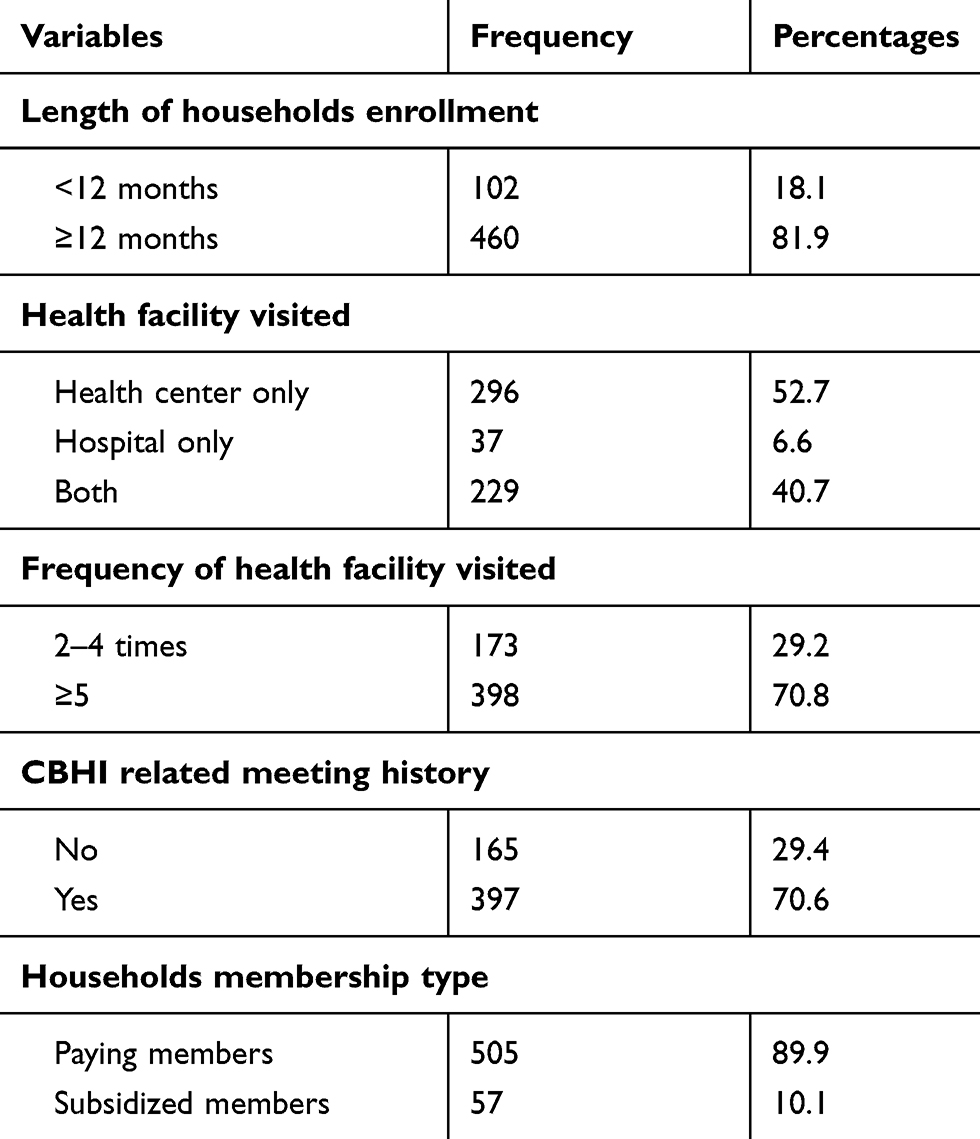

This study included household heads that had at least one family member that had fallen sick and visited health facilities at least two times since enrolled in CBHIS. Accordingly, the majority (54.4%) of the respondents visited only health centers, and 70.8% visited more than five times since enrolled in the CBHI scheme. Of the total participants, 89.9% are paying members, and the rest is subsidized members (Table 2).

|

Table 2 Experience of Household Heads Who Visited Health Facilities with CBHI Scheme in Anilemo District, Hadiya Zone Southern Ethiopia, 2020 |

Household Heads Knowledge of CBHI Benefit Packages Who Visited Health Facilities with CBHIS

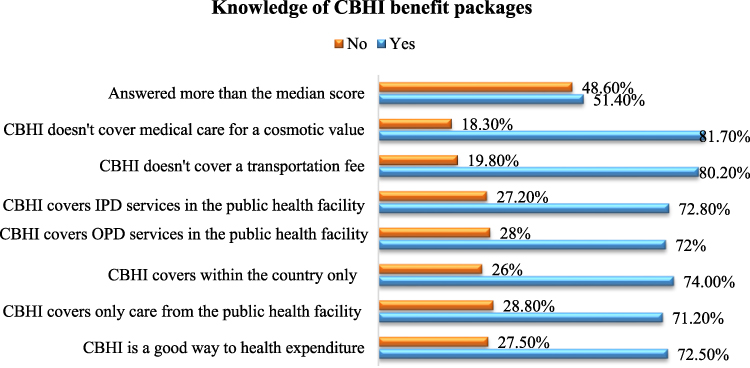

Seven items were used to measure a household’s knowledge of the CBHI benefit packages. From a total of seven items, respondents have a minimum score of 2, a maximum score of 7, and a median score of 5. Households were labeled as having good knowledge if answered more than the median score of the CBHI benefit package questions. Otherwise, households were labeled as have poor knowledge. Accordingly, 289 (51.4%) household heads had good knowledge of the CBHI benefit package (Figure 1).

|

Figure 1 Knowledge of CBHI benefit packages who visited health facilities with CBHIS in Anilemo district, Hadiya Zone, Southern Ethiopia, 2020. |

Health Service Provision Related Factors of Household Heads Who Visited Health Facilities with CBHI Scheme

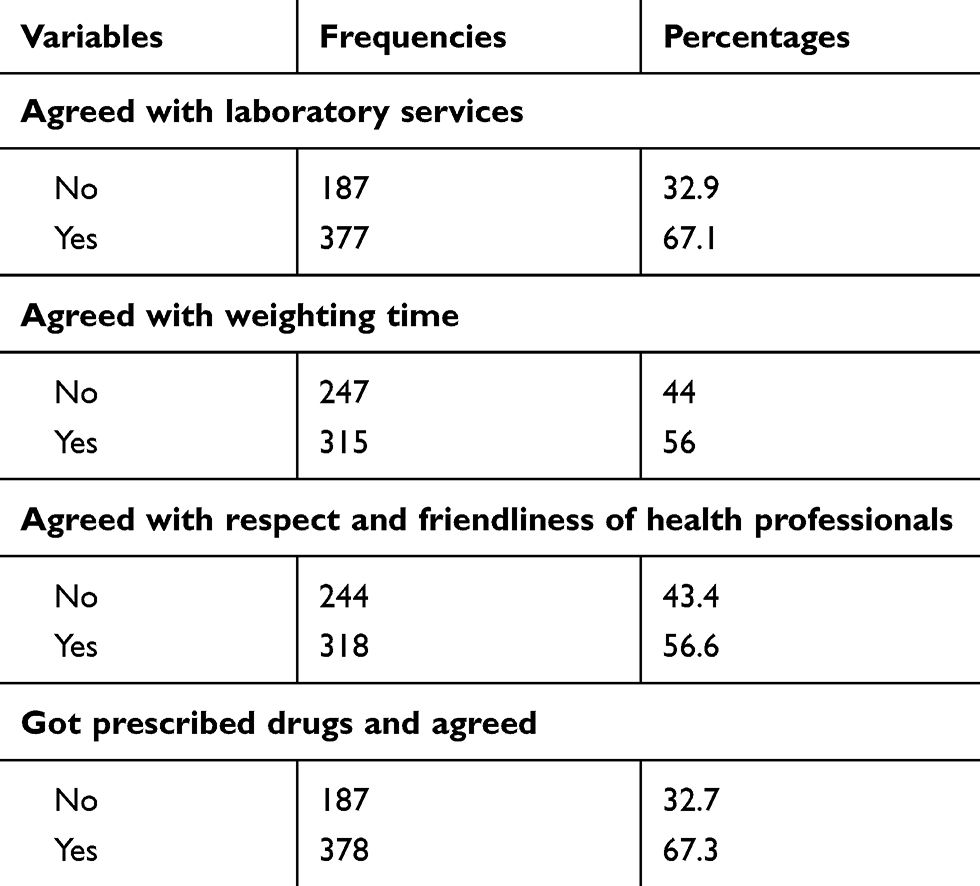

The majority of (67.1%) the participants mentioned that they agreed with laboratory services received, and about 56% of them agreed that they got immediate care when visiting health facilities. However, nearly half of (43.4%) the participants believed that they did not get respect from the health care providers and 378 (67.3%) of household heads received the correct prescribed drugs and agreed with that (Table 3).

|

Table 3 Health Service Provision Related Factors of Household Heads Who Visited Health Facilities with CBHI Scheme in Anilemo District, Hadiya Zone, Southern Ethiopia, 2020 |

The Overall Magnitude of Satisfaction Among Household Heads Who Visited Health Facilities with the CBHI Scheme

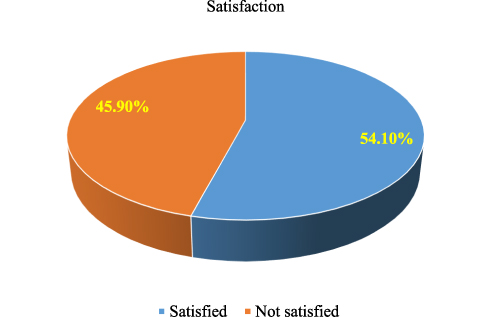

The median score for household heads satisfaction on the CBHI scheme was 41.00. About 304 (54.1%) respondents scored above the median satisfaction score (they are satisfied), and the remaining 258 (45.9%) scored below the median satisfaction score (Figure 2).

|

Figure 2 The magnitude of household heads satisfaction with CBHI scheme in Anilemo district, Hadiya Zone, Southern Ethiopia, 2020. |

Factors Associated with the Magnitude of Household Heads Satisfaction Who Visited Health Facilities with a Community-Based Health Insurance Scheme

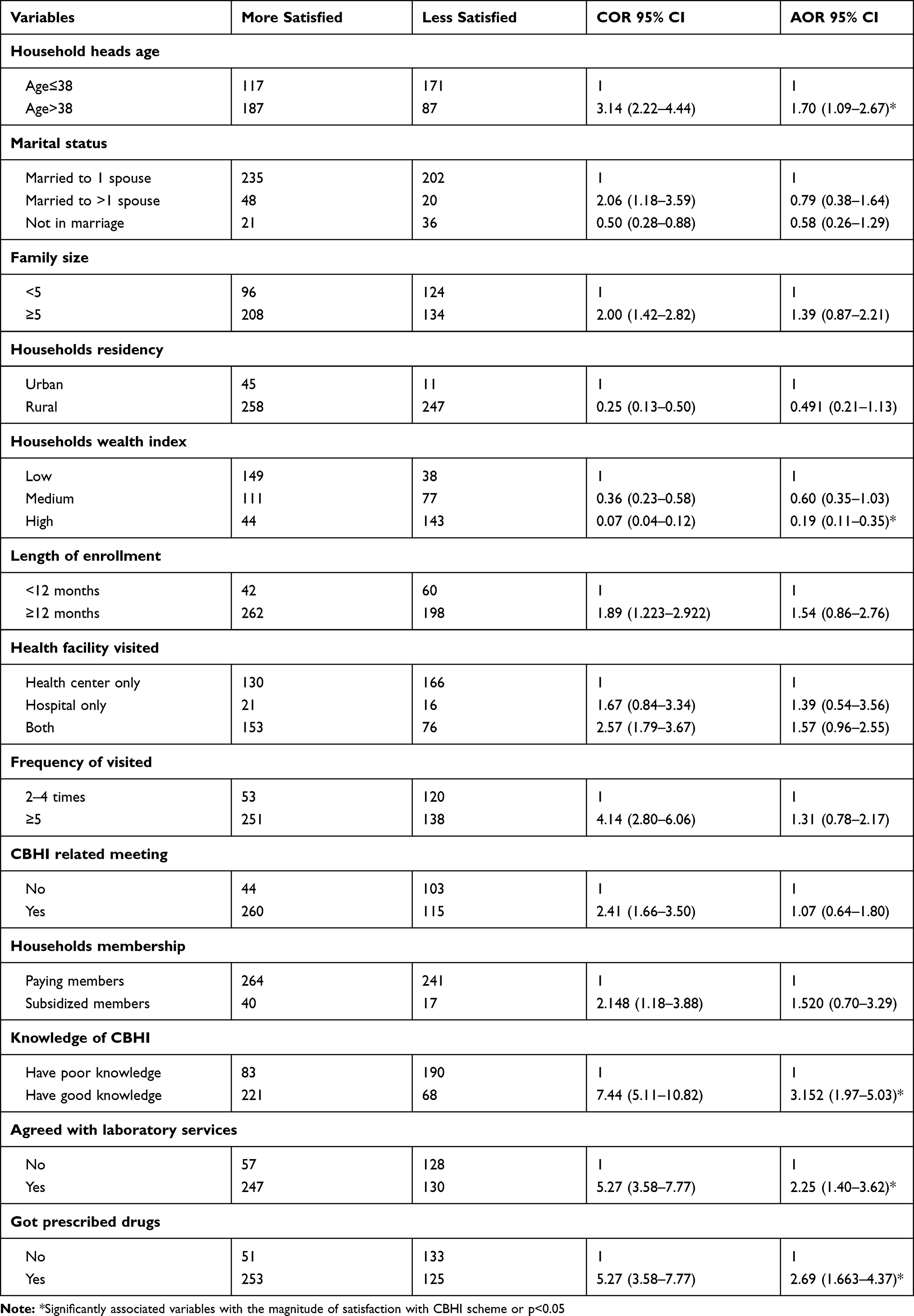

In bivariable analysis variables with p <0.25 included in the final model. Then: age, households’ wealth index, general knowledge of CBHI benefit packages, agreed with lab services, and agreed with prescribed drugs were factors significantly associated with outcome variable in multivariable analysis. The odds of household head satisfaction were 1.70 times higher for elder enrolls than younger enrolls [AOR=1.70; 95% CI 1.09–2.67]. For those household heads who had high household wealth, the odds of household head satisfaction decreased by 81% compared with those household heads who had low household wealth [AOR=0.19; 95% CI 0.11–0.35]. The odds of household head satisfaction were 3.15 times higher for those who had good knowledge about CBHI benefit packages compared to those who had poor knowledge [AOR=3.15; 95% CI 1.97–5.03]. Similarly, the odds of household heads satisfaction were 2.69 and 2.25 times higher for those enroll who agreed with prescribed drugs and laboratory services when compared to those enrolls who disagreed on these services [AOR=2.69; 95% CI 1.66–4.37] and [AOR=2.25; 95% CI 1.40–3.62] respectively (Table 4).

|

Table 4 Multivariable Logistic Regression Analysis Results on Factors Associated with the Magnitude of Household Heads Satisfaction Who Visited Health Facilities with CBHIS in Anilemo District, Hadiya Zone, Southern Ethiopia, 2020 |

Discussion

In this study, the magnitude of satisfaction with the CBHI scheme was found to be 54.1%. This is in line with the different studies done in the Sheko district (Ethiopia),9 Istanbul city (Turkey),12 and Nigeria.16 However, it is higher in comparison to two studies conducted in Nigeria.13,14 It is probably because of the look at settings, socio-demographic characteristics of the respondents, and study duration variations.

However, the magnitude of satisfaction in this study is lower than the study conducted in the Damatowyda district of Southern Ethiopia.11 The possible reason might be the definition of satisfaction; in the former study, the satisfaction scored based on the percentage of maximum scale (taking the percent strongly agree and agree). Calculating household heads satisfaction based on the percentage of maximum scale might overestimate the proportion of household’s satisfaction to CBHIS. In addition to these, it measures the overall satisfaction score by asking only six questions; it might be difficult to express enroll satisfaction by asking a few questions. When we ask more questions we may probe more problems on CBHI enrollment.

In this study, older participants (age>38) were more likely satisfied than younger (age≤38) participants. The finding of this study is supported by the studies conducted in Ethiopia, Nigeria, and Turkey.11–13 This might be attributed to more frequent illness in older people; when age increases, the probability of getting sick increases; thus, they use health services more frequently without paying from their pocket for every service they received.

Enrolls who had high household wealth less likely to be satisfied than low-wealthy household heads. This finding is similar to the studies done in Nigeria, Bangladesh, and Ethiopia.10,11,13 This might be due to a high expectation of wealthy people for more quality health services than they are practically had. They have the trends of using private sectors. Public health sectors are not as qualified as private sectors in this study area. On the other hand, poor households might not use the private sector. So, their expectation is lower than wealthy enrolls.

Participants with good knowledge about CBHI benefit packages were more likely satisfied than participants with poor knowledge. These findings were in line with studies conducted in Ethiopia, Nigeria, and Uganda.9–11,13,14,16 This might be that enrollee’s satisfaction gets better only if they understand how the health insurance scheme works, and know CBHI benefits packages. Those who know more about CBHI benefit packages may benefit more from it and might be more satisfied. And also, another study conducted in Senegal showed that inadequate knowledge of CBHI benefit packages is often associated with dropout.17

Those who got prescribed drugs and agreed with that drugs were more likely satisfied than those who did not get and disagreed with prescribed drugs. This finding is consistent with the study conducted in Bangladesh.10 This might be due to enrolled who did not get prescribed drugs in a public health facility were enforced to pay additional costs for private pharmacies, which might be the causes of disagreement and less satisfaction with the CBHI scheme.

Participants who agreed with the laboratory services they received were more likely satisfied when compared with counterparts. This finding is consistent with former studies conducted in Ethiopia, Uganda, and Bangladesh.9–11,18 This might be linked to the quality of health services (availability of reagents, lab services, good professionals, and equipment) after enrollment determines household heads’ satisfaction with the CBHI scheme.

Strength and Limitation of the Study

The study was community-based, includes both urban and rural kebeles, to generalize for the study area. Despite this strength, it is a cross-sectional survey; causality cannot be inferred from these studies.

Conclusions

The study showed that more than half of household heads’ were satisfied with the CBHI scheme in the Anilemo district. Household head’s age, household wealth, knowledge of CBHI benefit packages, agreement with laboratory service provision, availability of prescribed drugs, and agreement with that were independent factors of household heads’ satisfaction. Therefore, different strategies were required to improve enrolls knowledge of CBHI benefit packages through education, information campaign, and strengthening community participation in the district. And also, a further comparative study should be done on the magnitude of household heads satisfaction who visited a health facility should be done on CBHI enrolls and non-enrolls.

Abbreviations

CBHI, Community Based Health Insurance; CBHIS, Community Based Health Insurance Scheme; CSA, Central statistical agency; EDHS, Ethiopian Demographic and Health Survey; ETB, Ethiopian Birr; EFY, Ethiopian Fiscal Year; EHIA, Ethiopia Health Insurance Agency; FMOH, Federal Ministry of Health; HH, Households; HHH, Household Heads; HF, Health facility; HI, Health insurance; HSTP, Health sector transformation plan; IPD, Inpatient Department; OPD, Out Patient Department; OOP, Out of pocket; PHCU, Primary health care unit; SHI, Social Health Insurance; SNNP, Southern Nations, Nationalities and People; UHC, Universal health coverage; USAID, United States aid international development; USD, United States Dollar; WHA, World health assembly; WHO, World Health Organization.

Data Access

All relevant data are within the paper.

Acknowledgments

We would like to express our special thanks to Haramaya University, for technical support to conduct this research. We also acknowledge data collectors, supervisors, participants, and the Anilemo district health office for their respective contributions.

Author Contributions

All authors made substantial contribution to the work reported, whether that is in the conception, study design, execution, acquisition of data, analysis, and interpretation and took part in drafting, revising, or critically reviewing the article; gave final approval of the version to be published; have agreed on the journal to which the article has been submitted, and agree to be accountable for all aspects of the work. All authors have read and approved the final manuscript.

Funding

There was no funding for this research. The University did not provide funds.

Disclosure

The authors declare that they have no conflicts of interest.

References

1. Kutzin J. Health financing for universal coverage and health system performance: concepts and implications for policy. Bull World Health Organ. 2013;91:602–611. doi:10.2471/BLT.12.113985

2. Dieleman JL, Sadat N, Chang AY; Global Burden of Disease Health Financing Collaborator Network. Trends in future health financing and coverage: future health spending and universal health coverage in 188 countries. Lancet. 2018;391:1783–1798. doi:10.1016/S0140-6736(18)30697-4.

3. Asante A, Price J, Hayen A, Jan S, Wiseman V. Equity in health care financing in low- and middle-income countries: a systematic review of evidence from studies using benefit and financing incidence analyses. PLoS One. 2016;11(4):1–20. doi:10.1371/journal.pone.0152866

4. United Nations. Transforming our world: the 2030 agenda for sustainable development. In: A New Era in Global Health; 2018. doi:10.1891/9780826190123.ap02

5. Federal Democratic Republic of Ethiopia Ministry of Health. Ethiopian health accounts household health service utilization and expenditure survey 2015/2016; 2017.

6. EHIA. Evaluation of community-based health insurance pilot schemes in Ethiopia: final report; May 2015:21. Available from: https://www.hfgproject.org/evaluation-cbhi-pilots-ethiopia-final-report/.

7. Solomon F, Hailu Z, Tesfaye DA. Ethiopia’s community-based health insurance: a step on the road to universal health coverage. Health Financ Gov. 2011.

8. World Health Organization (WHO). Ethiopian Health Sector Transformation Plan. 2015/16–2019/20. Fed Democr Repub Ethiop Minist Health. 2015.

9. Kebede KM, Geberetsadik SM. Household satisfaction with community-based health insurance scheme and associated factors in piloted Sheko district; Southwest Ethiopia. PLoS One. 2019. doi:10.1371/journal.pone.0216411

10. Sarker AR, Sultana M, Ahmed S, Mahumud RA, Morton A, Khan JAM. Clients’ experience and satisfaction of utilizing healthcare services in a community based health insurance program in Bangladesh. Int J Environ Res Public Health. 2018;15(8):1637. doi:10.3390/ijerph15081637

11. Badacho AS, Tushune K, Ejigu Y, Berheto TM. Household satisfaction with a community-based health insurance scheme in Ethiopia. BMC Res Notes. 2016;9(1). doi:10.1186/s13104-016-2226-9

12. Jadoo SAA, Puteh SEW, Ahmed Z, Jawdat A. Level of patients’ satisfaction toward national health insurance in Istanbul City (Turkey). World Appl Sci J. 2012. doi:10.1186/1471-2458-12-s2-a5

13. Mohammed S, Sambo MN, Dong H. Understanding client satisfaction with a health insurance scheme in Nigeria: factors and enrollees experiences. Health Res Policy Syst. 2011;9(1):20. doi:10.1186/1478-4505-9-20

14. Mustapha Kurfi M, Hussaini Aliero I, Author C. A study on clients’ satisfaction on the national health insurance scheme among staff of Usmanu Danfodiyo University Sokoto. IOSR J Econ Financ. 2017.

15. Central Statistics Authority CSA. Ethiopia population & housing census report 2007. Mortality; 2007.

16. Aliyu A Knowledge, attitude, perception and clients’ satisfaction with National Health Insurance Scheme Services(NHIS) at general hospital Minna, Niger State-Nigeria; 2012.

17. Mladovsky P. Why do people drop out of community-based health insurance? Findings from an exploratory household survey in Senegal. Soc Sci Med. 2014;107:78–88. doi:10.1016/j.socscimed.2014.02.008

18. Nshakira-Rukundo E, Mussa EC, Nshakira N, Gerber N, von Braun J. Determinants of enrolment and renewing of community-based health insurance in households with under-5 children in rural South-Western Uganda. Int J Health Policy Manag. 2019;8(10):593–606. doi:10.15171/ijhpm.2019.49

© 2021 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2021 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.