Back to Journals » Psychology Research and Behavior Management » Volume 16

Regulatory Focus and Financial Satisfaction: The Sequential Mediating Roles of Construal Level and Opportunity Cost Consideration Among College Students

Authors Hu J ![]() , Zhang Q, Wang Z, Tang S

, Zhang Q, Wang Z, Tang S

Received 13 April 2023

Accepted for publication 27 June 2023

Published 12 July 2023 Volume 2023:16 Pages 2635—2645

DOI https://doi.org/10.2147/PRBM.S415053

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Igor Elman

Jianping Hu,1 Qiuyan Zhang,2,3 Zhiwen Wang,1 Song Tang4

1Laboratory for Behavioral and Regional Finance, Guangdong University of Finance, Guangzhou, People’s Republic of China; 2Mental Health Education and Counseling Center, Guangzhou College of Commerce, Guangzhou, People’s Republic of China; 3College of Education for the Future, Beijing Normal University at Zhuhai, Zhuhai, People’s Republic of China; 4School of National Finance, Guangdong University of Finance, Guangzhou, People’s Republic of China

Correspondence: Jianping Hu, Email [email protected]

Background: Recently, the importance of individual differences has been recognized in the literature of general life satisfaction and domain-specific satisfaction, however, empirical research exploring the relationship between individual differences in self-regulatory focus and financial satisfaction remains relatively sparse, and less is known about the underlying processes that may mediate this relationship. The current study addressed these gaps by investigating whether and how self-regulatory focus (promotion vs prevention) as a motivational trait is related to college students’ financial satisfaction. A model was tested in which this association was sequentially mediated by the effects of construal level and opportunity cost consideration.

Methods: A total of 552 college students (38.6% male; ages 19– 25) completed a packet of questionnaires that measured trait regulatory focus, construal level, opportunity cost consideration, and financial satisfaction.

Results: The mediation model was tested via multiple regression analyses and bootstrapping procedure. The results supported a sequential mediation model, suggesting that predominantly promotion-focused regulation is associated with information construal at a more abstract level, increasing the consideration of opportunity costs, and subsequently enhancing financial satisfaction.

Discussion: These findings can broaden our understanding of how trait regulatory focus potentially influences financial satisfaction, offering new directions towards improving college students’ financial satisfaction.

Keywords: regulatory focus, construal level, opportunity cost consideration, financial satisfaction, sequential mediation model

Introduction

With the complexity and importance of personal finance, many people are concerned about managing their own financial matters and pursuing higher financial and overall well-being.1,2 College students are no exception. College students are at the beginning of emerging adulthood, and although, on the one hand, they desire autonomy, and on the other hand, they still need their parents’ financial support for their studies.3 A recent large-scale study of 1334 college students from seven universities in China reported that approximately half of the students were not satisfied with their financial situation.4 Driven by practical concern and social attention, researchers have focused on how emerging adults, especially college students, can achieve higher satisfaction with their current financial state.2,5

Financial satisfaction refers to a person’s subjective evaluation of their current financial condition.6,7 Previous studies have focused on emerging adults’ objective financial status, eg, household income;8 financial behavior,9 eg, saving money, holding student loan debt;10 financial capacity, eg, financial literacy, financial efficacy;11 and financial socialization, eg, family financial expectations;12 in relation to their financial satisfaction. Although recently the importance of individual differences has been recognized in the literature of financial well-being, empirical research exploring the relationship between individual differences and financial satisfaction remains relatively sparse.1,2 The current study addresses this gap by testing self-regulation as a psychological characteristic that potentially affects financial satisfaction.

Trait Regulatory Focus and Financial Satisfaction

There remains a dearth of research examining the relationship between self-regulatory focus and financial satisfaction. Self-regulatory focus theory posits two distinct but coexisting foci of self-regulation, namely promotion focus and prevention focus.13,14 Although promotion- and prevention-focused motivations coexist within each person, people differ in their predominant self-regulatory focus. People with a predominant promotion focus (the net difference between promotion and prevention) are likely to strive for enhancement, growth, and advancement, adopt an approach orientation, and view difficult tasks as opportunities to demonstrate their coping abilities and achieve domain-specific and life success. People with a predominant prevention focus are likely to strive for safety and responsibility, avoid actions that could lead to negative consequences, and view difficult tasks as an obligation, or even as a barrier to ensuring security and fulfilling duties.15,16 Self-regulatory focus can be considered a stable trait or a temporary situational state.14 In the current study, we conceptualized self-regulatory focus as a relatively stable motivational system or personality trait. Self-regulatory focus has been increasingly used to explain the subjective evaluation of general life satisfaction and domain-specific satisfaction. For example, in studies on general life satisfaction, promotion-focused people reported better quality of life and greater life satisfaction than prevention-focused people.17–19 With respect to domain-specific satisfaction, promotion- versus prevention-focused people reported stronger satisfaction with their job,16 romantic relationships,20,21 and friendships.22 These studies suggest the positive role of predominance in trait promotion focus in the aforementioned relationships. It is surprising that little is known about the possible links between trait regulatory focus and financial satisfaction. To address this gap, the current study investigated whether evidence of positive association between predominant promotion focus and domain-specific satisfaction extends to the finance domain, contributing a more complete picture of the impact of self-regulatory focus on domain-specific satisfaction.

We therefore propose the following hypothesis:

Hypothesis 1: Predominant promotion focus is positively correlated with financial satisfaction.

The Mediating Role of Construal Level

The distal-proximal theory argues that as the preexisting characteristics of individuals, personality traits serve distal motivational functions and have their indirect effects, while information processing and decision-making processing have more proximal influences.23–25 We suspect that construal level is a proximal information processing construct that mediates the distal effects of trait regulatory focus on financial satisfaction. According to construal level theory, this concept is the degree of abstraction by which people process information.26 People differ in their construal level. Individuals with low construal level construe their environment in a concrete way, and produce subordinate representations. By contrast, individuals with high construal level construe their environment in an abstract way, and produce superordinate representations. For example, if asked to describe the act of reading, the person with low construal level might say “following lines of print”, whereas the person with high construal level might say “gaining knowledge”.

Evidence of an association between trait regulatory focus and construal level remains scarce and somewhat inconsistent. For example, in the study of Pennington and Roese,27 trait promotion focus was positively correlated with construal level for future judgments, whereas, for retrospective judgments, trait promotion focus was uncorrelated with construal level. Nevertheless, scholars have argued that considering the role of trait regulatory focus could contribute to a more comprehensive understanding of the relationship between regulatory focus and construal level.14,28 Although no studies have directly investigated the mediating role of construal level in the relationship between trait regulatory focus and financial satisfaction, there is indirect evidence concerning the first link (trait regulatory focus → construal level) that would suggest the possibility of such a mediation model. In two experiments, researchers manipulated self-regulatory goal orientation and assessed participants’ construal level. Participants who were primed with a promotion focus subsequently construed information at a higher level than those who were primed with a prevention focus.29,30

There is also indirect evidence of the second link in the proposed mediation process (construal level → financial satisfaction). Specifically, construal level has been shown to be associated with general satisfaction, which presumably includes financial satisfaction. For example, people with high versus low construal levels focused more on the positives and pro arguments in considering a course of action,31 reported less discomfort when experiencing mixed emotions and evaluated their mixed emotions more favorably,32 had a better ability to cope with mixed emotions,33 and reported higher life satisfaction.33

Research on the finance domain has shown that construal level is associated with healthy financial behaviors, which may improve financial satisfaction. For example, when saving goals were specified, people with a high construal level reported higher anticipated success, committed more to the goals, and had higher actual saving than people with a low construal level.34 In addition, a number of studies have shown that people with a higher tendency to plan for long-term goals (the core characteristic of high-level construal) had higher financial satisfaction.35–38 Thus, it is plausible that individuals with high construal level would be more satisfied with their financial situation.

Based on this review of the literature, we propose the following hypothesis:

Hypothesis 2: Predominant promotion focus is positively correlated with construal level, which in turn is positively correlated with financial satisfaction. In other words, construal level mediates the relationship between predominant regulatory focus and financial satisfaction.

The Mediating Role of Opportunity Cost Consideration

Opportunity cost consideration may serve as a proximal information processing construct that mediates the distal effects of trait regulatory focus on financial satisfaction. Green’s (1894) economic concept of opportunity cost has been applied in the research fields of psychology and marketing.39 People have unlimited wants but limited resources, requiring them to choose which wants will be fulfilled. Choosing something means forgoing something else. The opportunity cost of one option is “the evaluation placed on the most highly valued of the rejected alternatives or opportunities”.40 Opportunity cost is resource-specific. In the current study, opportunity cost consideration is defined as considering alternative uses for one’s money.

Trait regulatory focus appears to be a motivational antecedent of opportunity cost consideration. This possibility is relevant to the first link of mediation (trait regulatory focus → opportunity cost consideration). In several studies, prevention-focused (vs promotion-focused) individuals were more prone to anticipate regret41 and to experience regret,42 and were more likely to avoid regret.43 People with prevention focus might be more likely to ignore opportunity costs because there is an aversion to regret,44,45 creating an incentive to avoid information about foregone outcomes.44,46 In contrast, promotion-focused (vs prevention-focused) individuals had a higher tendency to maximize their opportunities and gains.43 The promotion-focused decision-making style that maximizes utility might help people seize opportunities and hence increase their consideration of alternative uses of their resources.

Opportunity cost consideration may also promote healthy financial behaviors. This possibility is relevant to the second link of the mediation process (opportunity cost → financial satisfaction). In the experiments of Hershfield, Goldstein, Sharpe, Fox, Yeykelis, Carstensen and Bailenson,47 participants whose attention was explicitly directed to future consequences were more likely to accept later monetary rewards over immediate ones. Individuals with a higher tendency to elaborate on potential outcomes invested more money for their retirement.48 Bartels and Urminsky49 reported that participants with a higher sense of psychological connectedness to the future self had a lower purchase intents only when the opportunity cost was chronically salient (for people with a high propensity to plan) or situationally salient (an opportunity cost cue was presented). In light of the robust relationship between healthy financial behaviors and financial satisfaction, it is reasonable to assume that opportunity cost consideration improves financial satisfaction.

Based on the literature reviewed above, we propose the following hypothesis:

Hypothesis 3: Predominant promotion focus is positively correlated with opportunity cost consideration, which in turn is positively correlated with financial satisfaction. In other words, opportunity cost consideration mediates the relationship between predominant regulatory focus and financial satisfaction.

The Relationship Between Construal Level and Opportunity Cost Consideration

As discussed above, construal level and opportunity cost consideration each contribute to financial satisfaction, and there is indirect evidence that they may each mediate the association between trait regulatory focus and financial satisfaction. However, not much is known about the relationship between these two mediators. According to construal level theory, high levels of construal drive attention to the general meaning of the action.26 In one recent experiment, participants who were manipulated to derive meanings from their choice had greater consideration of other ways to use money than control participants who were manipulated to derive pleasure from their choice.50 Taken together, it suggests that construal level may predict later consideration of opportunity cost. This further suggests the possibility that construal level and opportunity cost consideration may be sequential mediators of the association between trait regulatory focus and financial satisfaction. We thus propose the following hypothesis:

Hypothesis 4: Construal level and opportunity cost consideration sequentially mediate the relationship between predominant regulatory focus and financial satisfaction.

The Present Study

The present study tested a potential underlying mechanism of the relationship between trait regulatory focus and financial satisfaction. A sequential mediation model was tested in which this association was mediated by construal level and opportunity cost consideration.

Methods

Sample

A cross-sectional design with convenience sampling was used. This study was approved by the Ethics Committee of Guangdong University of Finance. Participants were recruited from two universities in Guangdong Province, China, all of whom volunteered to complete an online survey. The sample size was estimated using G-power 3.1. For linear multiple regression, the minimum required number of participants was 550, based on an α level of 0.05, power (1-β) of 0.80, effect size (f2) of 0.02, three predictors, and three covariates.7,51 There were 552 participants (38.6% male) who completed the anonymous questionnaires. The average age of participants was 19.30 (SD = 1.45).

Measures

Trait Regulatory Focus

Participants’ trait regulatory focus was assessed by the Regulatory Focus Questionnaire (RFQ; Semin, Higgins, De Montes, Estourget and Valencia52 using the Chinese translated version (Yang et al).53 The RFQ contains two subscales, with six items for promotion focus and prevention focus, respectively. A representative item in the promotion focus subscale is “I try to reach that in my life, in which I believe.” A representative item in the prevention focus subscale is “Not being careful enough has gotten me into trouble at times.” Participants rated each item on a 7-point Likert type scale from 1 (not at all true) to 7 (absolutely true). Cronbach’s α coefficients of 0.842 (promotion focus) and 0.733 (prevention focus) indicated good internal reliability for the RFQ in the present study. To test our hypotheses, following previous research,54,55 predominant regulatory focus was calculated by subtracting the mean prevention focus score from the mean promotion focus score. Higher positive scores indicate relatively greater trait promotion than prevention focus; higher negative scores indicate relatively greater trait prevention than promotion focus.

Construal Level

Participants’ construal level was measured by the Behavioral Identification Form (BIF),56 using the Chinese translated version.57 The BIF lists 25 behaviors and activities (eg, reading), with a concrete description (eg, following lines of print) and an abstract description (eg, gaining knowledge). Participants were asked to choose the description that they thought best matched the behavior. Participants’ responses (concrete answers were coded as 0, whereas abstract answers were coded as 1) were averaged to provide a BIF score. Higher BIF scores indicate higher construal levels. The Cronbach’s α coefficient for the present sample was 0.748.

Opportunity Cost Consideration

Participants’ opportunity cost consideration was measured by a three-item scale of opportunity cost consideration.58 A representative item is “I often consider other specific items that I would not be able to buy if I made a particular purchase.” The items were forward- and back-translated by two independent bilinguals. Participants indicated their degree of agreement with each item using a 7-point scale ranging from 1 (strongly disagree) to 7 (strongly agree). The mean scores were computed, with higher scores indicating greater opportunity cost consideration. The Cronbach’s α coefficient for the present sample was 0.704.

Financial Satisfaction

Participants’ financial satisfaction was measured by a five-item scale of financial satisfaction.59 A representative item is “Compared to my financial position last year, my financial position this year is ___.” Participants indicated their position using a seven-point scale ranging from 1 (much worse) to 7 (much better). The mean scores were computed, with higher scores indicating greater financial satisfaction. The Cronbach’s α coefficient for the present sample was 0.894.

Control Variables

We control for basic socio-demographic variables (age, gender and monthly living expenses). Participants were required to indicate their monthly pocket money on a five-point scale ranging from 1 (less than 500 yuan) to 5 (more than 2000 yuan).

Data Analysis

Data were analyzed using IBM SPSS version 22. First, descriptive statistics (eg, M, SD) and bivariate correlations for major variables were calculated. Because all data were collected using self-report questionnaires at one time point, Harman’s single-factor test was conducted to check for common method variance.60 Second, a linear regression was employed to test Hypothesis 1. The Model 6 in the SPSS PROCESS Macro61 was employed to test Hypotheses 2–4. The 95% confidence interval (CI) for the indirect effect was a bias-corrected estimate based on 5000 bootstrapping resamples. The mediating effect was considered to be significant at the level of p < 0.05, when the 95% CI did not include zero.

Results

Preliminary Analyses

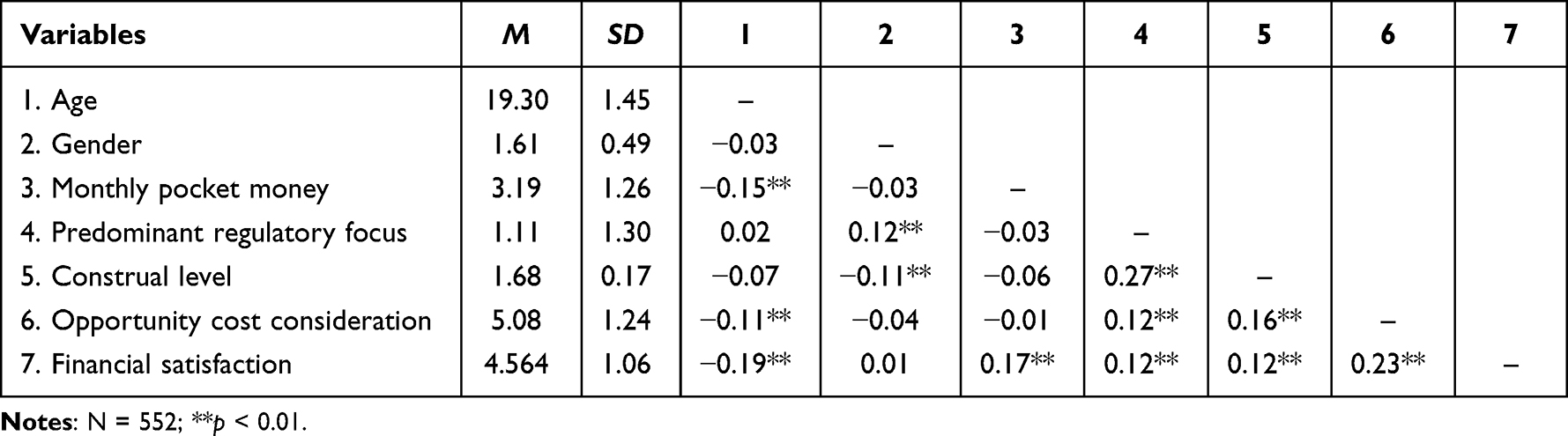

Means and standard deviations of all the variables along with their inter-correlations are presented in Table 1. Predominant regulatory focus, construal level, and opportunity cost consideration showed significant and positive correlations with financial satisfaction. Predominant regulatory focus and construal level were significantly positively associated with opportunity cost consideration. Predominant regulatory focus was significantly positively associated with construal level. In addition, monthly pocket money was significantly positively associated with financial satisfaction. Meanwhile, Harman’s single-factor test showed that the variance accounted for by the first factor was no more than 40% for all the self-report measures, indicating that the common method variance was not a concern in this study.

|

Table 1 Means and Standard Deviations of All the Variables Along with Their Correlations |

Mediation Analyses

First, significant correlations were found among predominant regulatory focus, construal level, opportunity cost consideration and financial well-being. These correlations met the statistical requirements for further analysis of the mediating effects of construal level and opportunity cost consideration.62

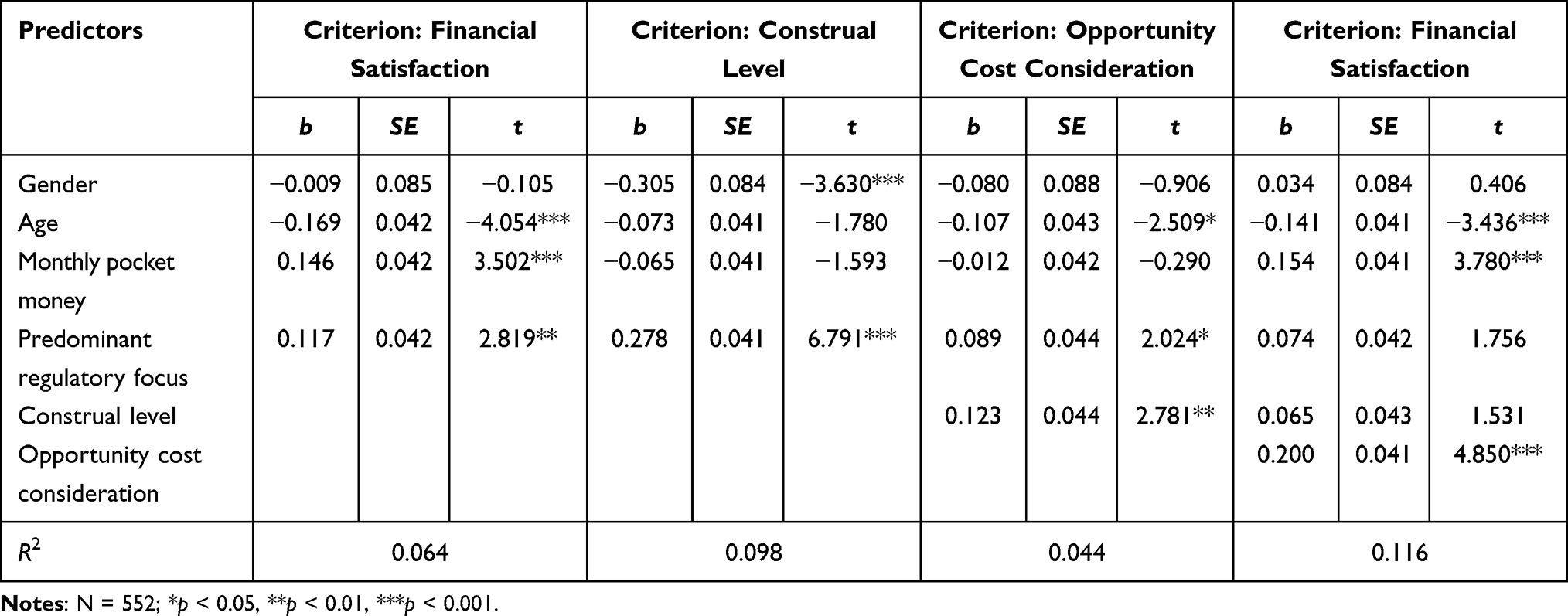

After controlling for both gender, age and monthly pocket money, the results of regression analysis (Table 2) showed that predominant regulatory focus was positively related to financial satisfaction (b = 0.117, p < 0.01). Hypothesis 1 was supported. However, when construal level and opportunity cost consideration were included in the regression equation, the direct effect of predominant regulatory focus on financial satisfaction ceased to be significant (b = 0.074, p > 0.05).

|

Table 2 Tests of Mediation in the Association Between Predominant Regulatory Focus and Financial Satisfaction |

In addition, predominant regulatory focus was positively correlated with construal level (b = 0.278, p < 0.001) and opportunity cost consideration (b = 0.089, p < 0.05); construal level was positively correlated with opportunity cost consideration (b = 0.123, p < 0.01), but not significantly related to financial satisfaction (b = 0.065, p > 0.05); and opportunity cost consideration was positively associated with financial satisfaction (b = 0.200, p < 0.001). Figure 1 shows the path of standardized regression coefficients of the sequential mediation model.

|

Figure 1 Effect of predominant regulatory focus on financial satisfaction sequentially via construal level and opportunity cost consideration. Notes: Solid lines indicate statistically significant associations, whereas dashed lines indicate non-significant associations. *p<0.05, **p<0.01, ***p<0.001. |

Mediation analysis was conducted using Model 6 of the PROCESS macro in SPSS.61 Construal level and opportunity cost consideration exerted a full sequential mediating role in the association between predominant regulatory focus and financial satisfaction (Table 3). To be specific, firstly, neither the “predominant regulatory focus→construal level→financial satisfaction” pathway (indirect effect = 0.018, 95% CI = −0.010 to 0.044) nor the “predominant regulatory focus→opportunity cost consideration→financial satisfaction” pathway (indirect effect = 0.018, 95% CI = −0.004 to 0.045) was significant. Hence, construal level and opportunity cost consideration did not individually mediate the link between predominant regulatory focus and financial satisfaction. Thus, Hypothesis 2 and Hypothesis 3 were not supported. Secondly, the sequential pathway of “predominant regulatory focus→construal level→opportunity cost consideration→financial satisfaction” was significant (indirect effect = 0.007, 95% CI = 0.001 to 0.015). Thus, construal level and opportunity cost consideration sequentially mediated the link between predominant regulatory focus and financial satisfaction, supporting Hypothesis 4.

|

Table 3 Total, Direct, and Indirect Effects of Predominant Regulatory Focus on Financial Satisfaction |

Discussion

The main objective of this study was to investigate the psychological basis for the link between trait regulatory focus and financial satisfaction among college students. We tested construal level and opportunity cost consideration as individual and sequential mediators of this association. When tested individually, neither construal level nor opportunity cost consideration mediated the link between trait regulatory focus and financial satisfaction. However, construal level and opportunity cost consideration were sequential mediators of this association.

The research contributes to the financial satisfaction literature by identifying trait regulatory focus, construal level and opportunity cost consideration as hitherto under-studied but important antecedents of financial satisfaction. The results suggest that opportunity cost consideration may be a driver of the subjective evaluation of one’s financial situation. Because the consideration of opportunity cost is thought to occur before final decision-making,39,63 it makes sense that opportunity cost consideration would play a more proximal role in shaping evaluation than motivational factors (ie, trait regulatory focus) or information processing style (ie, construal level) would do. This sequential mediation model helps us to better understand the ways in which trait regulatory focus and construal level, as distal influences on financial satisfaction, can exert their impact on opportunity cost consideration as a proximal influence.

Further, evidence of a positive link between opportunity cost consideration and financial satisfaction in the current study can be applied to understanding the relationship between opportunity cost consideration and consumer well-being. Previous research showed that opportunity cost consideration increased sensitivity to the value of outside options, thus reducing the likelihood of buying the focal purchases.58 This may diminish people’s short-run satisfaction from consumption. However, greater consideration of alternative uses of one’s money may enhance financial satisfaction in the long run. Heightened focus on alternative uses for one’s money may encourage people to prioritize some purchases over others, making the best use of their money.64 Indeed, research suggests that opportunity cost consideration is positively associated with several healthy financial behaviors, such as budgeting, saving money, and delaying discounting,47,48 all of which may contribute to people’s long-run financial satisfaction. In our own study of college students, this positive link between opportunity cost consideration and financial satisfaction suggests that considering the opportunity cost and making the best use of their limited money may be one of the effective way to manage the conflict between autonomy and financial dependence, then achieving a higher level of financial satisfaction.

Our findings also contribute to the literature on the antecedents of opportunity cost consideration. While this literature has primarily focused on the impact of dispositional differences in spending attitudes, such as being a tightwad65 and having a propensity to plan,58,66 researchers have recently suggested to examine how motivational factors and information processing style affect the consideration of alternative use of the resource, see a review.39 We extend this literature by demonstrating that trait regulatory focus and construal level affect opportunity cost consideration, in isolation and in concert.

In addition, these findings lend further credence to the notion that the accessibility of alternative uses of a resource is an important driver of opportunity cost consideration.58 The direct positive link between trait regulatory focus and opportunity cost consideration suggests that with the goal orientation of utility maximization, people with high promotion focus may be motivated to search for opportunities and focus their attention on them.43 This may make it easier to access the alternatives, thus enabling them to give greater consideration to opportunity cost. In addition, the beneficial role of trait regulatory focus on opportunity cost consideration may partly be due to the adoption of high-level construal. Specifically, people with high promotion focus may be more likely to construe information at an abstract, high level. It has been suggested that high construal level is associated with a more flexible and creative information processing style55 and with more attention to the “big picture”.67 These characteristics may promote awareness of future consequences, the accessibility of an alternative, and consideration of opportunity cost. That is, regulatory focus is a psychological tool that may not per se be associated with opportunity cost consideration, but needs to be used to have a beneficial effect on opportunity cost consideration.

The present study has important practical implications. Our sequential mediation model identified opportunity cost consideration as the more proximal mediator. Interventions should be tailored to help college students bring opportunity cost to bear on consumption decisions. Experimental studies have shown that opportunity costs can be brought to mind by directing people’s attention to alternative uses of money beyond the options at hand,50 even outside the purchase context.65 However, the heightened consideration of opportunity cost encourages people to choose products that are less expensive, and thus less durable and less environmentally friendly.50 This consumer behavior can have a negative impact on consumption utility. The seeming tendency of sacrificing quality for quantity points to the danger of understanding opportunity cost in narrow and concrete ways. Given the positive association between construal level and opportunity cost consideration, interventions should be aimed at cultivating abstract construal in the long run. For example, individuals can be encouraged to consider opportunity costs within broader contexts and longer periods. This could help them to develop a bigger picture of possible alternatives and further to link the alternatives to their core values and beliefs. Interventions could promote both satisfactory consumption experiences in the short run and improved financial well-being in the long run.

Despite the relevant theoretical and practical contributions of the present research, it is not without limitations. First, the cross-sectional design does not allow us to draw conclusions regarding causality or directionality. Reciprocal relationships between construal level, opportunity cost consideration and financial satisfaction are possible. For example, individuals who used to consider opportunity cost and make trade-offs may be more likely to develop and adopt a high level of construal. College students who are satisfied with their financial situation may come to perceive trade-offs as more valuable. Thus, it is necessary to use experimental or longitudinal designs to achieve an understanding of the influence of inter-related contributors to financial satisfaction. Second, the self-reported nature of our measures may cause potential bias due to social desirability, selective memory bias, and common method variance. Even though Harman’s single-factor test suggested that the common method variance was not a concern in this study, future studies could address this limitation by using multi-method and multi-informant data collection strategies. Third, there might be other mediators (eg, the tendency toward regret, the tendency toward maximization, healthy financial behaviors) and moderators (eg, children’s poverty, perceived scarcity) in the relationship between trait regulatory focus and financial satisfaction. Therefore, future studies could examine other factors that mediate and/or moderate the association. Last but not least, convenience sampling may have limited the ability to generalize beyond highly similar groups. Future studies could validate the findings with random sampling to reach a more diverse sample.

Conclusions

Despite the above limitations, this is the first study to investigate the sequential mediating roles of construal level and opportunity cost consideration in the link between trait regulatory focus and financial satisfaction. Findings suggest that people with predominant promotion focus may be more likely to construe information at an abstract, high level, which continues to increase the consideration of alternative uses of their money, and ultimately achieves higher levels of financial satisfaction. These findings add a new understanding of the mechanisms underlying the pathway between motivational traits and financial satisfaction and provide novel insights for improving college students’ financial satisfaction.

Data Sharing Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.

Ethics Approval

The research was approved by the ethics committee of Guangdong University of Finance.

Consent to Participate

Informed consent was obtained from all adult participants included in the study.

Funding

This study was supported by Humanities and Social Science Youth Foundation of the Ministry of Education of China (21YJC190006), the 13th “Five-Year” Plan of Philosophy and Social Science of Guangdong Province (GD19YXL02), and National Natural Science Foundation of China (31800933, 71874038 and 72003047).

Disclosure

The authors declare that there is no conflict of interest in this work.

References

1. Hashmi F, Aftab H, Martins JM, et al. The role of self-esteem, optimism, deliberative thinking and self-control in shaping the financial behavior and financial well-being of young adults. PLoS One. 2021;16(9):e0256649. doi:10.1371/journal.pone.0256649

2. Iannello P, Sorgente A, Lanz M, Antonietti A. Financial well-being and its relationship with subjective and psychological well-being among emerging adults: testing the moderating effect of individual differences. J Happiness Stud. 2021;22(3):1385–1411. doi:10.1007/s10902-020-00277-x

3. Shim S, Serido J, Tang C, Card N. Socialization processes and pathways to healthy financial development for emerging young adults. J Appl Dev Psychol. 2015;38:29–38. doi:10.1016/j.appdev.2015.01.002

4. Huang W, Liao X, Li F, Yao P. Does enrolling in finance-related majors improve financial habits? A case study of China’s college students. Asia Pac Educ Rev. 2023;1–14. doi:10.1007/s12564-023-09856-y

5. Sorgente A, Lanz M. Emerging adults’ financial well-being: a scoping review. Adolesc Res Rev. 2017;2(4):255–292. doi:10.1007/s40894-016-0052-x

6. Ng W, Diener E. What matters to the rich and the poor? Subjective well-being, financial satisfaction, and postmaterialist needs across the world. J Pers Soc Psychol. 2014;107(2):326. doi:10.1037/a0036856

7. Hu J, Quan L, Wu Y, et al. Financial self-efficacy and general life satisfaction: the sequential mediating role of high standards tendency and investment satisfaction. Front Psychol. 2021;12:545508. doi:10.3389/fpsyg.2021.545508

8. Shim S, Xiao JJ, Barber BL, Lyons AC. Pathways to life success: a conceptual model of financial well-being for young adults. J Appl Dev Psychol. 2009;30(6):708–723. doi:10.1016/j.appdev.2009.02.003

9. Montalto CP, Phillips EL, McDaniel A, Baker AR. College student financial wellness: student loans and beyond. J Fam Econ Issues. 2019;40(1):3–21. doi:10.1007/s10834-018-9593-4

10. Damian LE, Negru-Subtirica O, Domocus IM, Friedlmeier M. Healthy financial behaviors and financial satisfaction in emerging adulthood: a parental socialization perspective. Emerg Adulthood. 2020;8(6):548–554. doi:10.1177/2167696819841952

11. Sabri MF, Wahab R, Mahdzan NS, Magli AS, Abd Rahim H. Mediating effect of financial behaviour on the relationship between perceived financial wellbeing and its factors among low-income young adults in Malaysia. Front Psychol. 2022;13. doi:10.3389/fpsyg.2022.858630

12. Utkarsh PA, Ashta A, Spiegelman E, Sutan A. Catch them young: impact of financial socialization, financial literacy and attitude towards money on financial well‐being of young adults. Int J Consum Stud. 2020;44(6):531–541. doi:10.1111/ijcs.12583

13. Higgins ET. Beyond pleasure and pain. Am Psychol. 1997;52(12):1280. doi:10.1037/0003-066X.52.12.1280

14. Higgins ET. Promotion and prevention: regulatory focus as a motivational principle. Adv Exp Soc Psychol. 1998;30:1–46.

15. Shah J, Higgins ET. Expectancy× value effects: regulatory focus as determinant of magnitude and direction. J Pers Soc Psychol. 1997;73(3):447. doi:10.1037/0022-3514.73.3.447

16. Zhao XR, Namasivayam K. The relationship of chronic regulatory focus to work–family conflict and job satisfaction. Int J Hosp Manag. 2012;31(2):458–467. doi:10.1016/j.ijhm.2011.07.004

17. Li R, Liu H, Yao M, Chen Y. Regulatory focus and subjective well-being: the mediating role of coping styles and the moderating role of gender. J Psychol. 2019;153(7):714–731. doi:10.1080/00223980.2019.1601066

18. Manczak EM, Zapata-Gietl C, McAdams DP. Regulatory focus in the life story: prevention and promotion as expressed in three layers of personality. J Pers Soc Psychol. 2014;106(1):169. doi:10.1037/a0034951

19. Wu CW, Chen WW. Mediating role of regulatory focus in the relation between filial piety and youths’ life satisfaction and psychological distress. Asian J Soc Psychol. 2021;24(4):499–510. doi:10.1111/ajsp.12447

20. An U, Park HG, Han DE, Kim Y-H. Emotional suppression and psychological well-being in marriage: the role of regulatory focus and spousal behavior. Int J Environ Res Public Health. 2022;19(2):973. doi:10.3390/ijerph19020973

21. Winterheld HA, Simpson JA. Seeking security or growth: a regulatory focus perspective on motivations in romantic relationships. J Pers Soc Psychol. 2011;101(5):935. doi:10.1037/a0025012

22. Gao Q, Bian R, R-d L, He Y, Oei T-P. Conflict resolution in Chinese adolescents’ friendship: links with regulatory focus and friendship satisfaction. J Psychol. 2017;151(3):268–281. doi:10.1080/00223980.2016.1270887

23. Hoyle RH. Personality and self‐regulation: trait and information‐processing perspectives. J Pers. 2006;74(6):1507–1526. doi:10.1111/j.1467-6494.2006.00418.x

24. Steinbach AL, Gamache DL, Johnson RE. Don’t get it misconstrued: executive construal-level shifts and flexibility in the upper echelons. Acad Manage Rev. 2019;44(4):871–895. doi:10.5465/amr.2017.0273

25. Kanfer R. Motivation theory and industrial and organizational psychology. In: Dunnette MD, Hough LM, editors. Handbook of Industrial and Organizational Psychology. Vol. 2. Consulting Psychologists Press; 1990:75–171.

26. Trope Y, Liberman N. Construal-level theory of psychological distance. Psychol Rev. 2010;117(2):440. doi:10.1037/a0018963

27. Pennington GL, Roese NJ. Regulatory focus and temporal distance. J Exp Soc Psychol. 2003;39(6):563–576. doi:10.1016/S0022-1031(03)00058-1

28. Wiebenga JH, Fennis BM. The road traveled, the road ahead, or simply on the road? When progress framing affects motivation in goal pursuit. J Consum Psychol. 2014;24(1):49–62. doi:10.1016/j.jcps.2013.06.002

29. Lee AY, Keller PA, Sternthal B. Value from regulatory construal fit: the persuasive impact of fit between consumer goals and message concreteness. J Consum Res. 2010;36(5):735–747. doi:10.1086/605591

30. Pandey A, Tripathi S. To go or to let it go: a regulatory focus perspective on bundle consumption. J Serv Res. 2022;10946705211067101. doi:10.1177/10946705211067101

31. Eyal T, Liberman N, Trope Y, Walther E. The pros and cons of temporally near and distant action. J Pers Soc Psychol. 2004;86(6):781. doi:10.1037/0022-3514.86.6.781

32. Hong J, Lee AY. Feeling mixed but not torn: the moderating role of construal level in mixed emotions appeals. J Consum Res. 2010;37(3):456–472. doi:10.1086/653492

33. Sun W, Zheng Z, Jiang Y, Tian L, Fang P. Does goal conflict necessarily undermine wellbeing? A moderated mediating effect of mixed emotion and construal level. Front Psychol. 2021;1921. doi:10.3389/fpsyg.2021.653512

34. Ülkümen G, Cheema A. Framing goals to influence personal savings: the role of specificity and construal level. J Mark Res. 2011;48(6):958–969. doi:10.1509/jmr.09.0516

35. Ali A, Rahman MSA, Bakar A. Financial satisfaction and the influence of financial literacy in Malaysia. Soc Indic Res. 2015;120(1):137–156. doi:10.1007/s11205-014-0583-0

36. Lee JM, Lee J, Kim KT. Consumer financial well-being: knowledge is not enough. J Fam Econ Issues. 2020;41(2):218–228. doi:10.1007/s10834-019-09649-9

37. O’Neill B, Xiao JJ, Ensle K. Propensity to plan: a key to health and wealth. J Financ Couns Plan. 2016;29(3):42–50. doi:10.1037/a0036856

38. Xiao JJ, O’Neill B. Propensity to plan, financial capability, and financial satisfaction. Int J Consum Stud. 2018;42(5):501–512. doi:10.1111/ijcs.12461

39. Haghpour B, Sahabeh E, Halvari H. Opportunity cost in consumer behavior: definitions, operationalizations, and ambiguities. Int J Consum Stud. 2022;46(5):1942–1959. doi:10.1111/ijcs.12842

40. Buchanan J. Opportunity cost. In: Durlauf SN, Blume LE, editors. The New Palgrave Dictionary of Economics.

41. Leder S, Florack A, Keller J. Self-regulation and protective health behaviour: how regulatory focus and anticipated regret are related to vaccination decisions. Psychol Health. 2015;30(2):165–188. doi:10.1080/08870446.2014.954574

42. Pierro A, Leder S, Mannetti L, Higgins ET, Kruglanski AW, Aiello A. Regulatory mode effects on counterfactual thinking and regret. J Exp Soc Psychol. 2008;44(2):321–329. doi:10.1016/j.jesp.2007.06.002

43. Lim J, Hahn M. Regulatory focus and decision rules: are prevention-focused consumers regret minimizers? J Bus Res. 2020;120:343–350. doi:10.1016/j.jbusres.2019.11.066

44. Gabillon E. When choosing is painful: anticipated regret and psychological opportunity cost. J Econ Behav Organ. 2020;178:644–659. doi:10.1016/j.jebo.2020.08.010

45. Hoskin RE. Opportunity cost and behavior. J Account Res. 1983;21(1):78–95. doi:10.2307/2490937

46. Golman R, Hagmann D, Loewenstein G. Information avoidance. J Econ Lit. 2017;55(1):96–135. doi:10.1257/jel.20151245

47. Hershfield HE, Goldstein DG, Sharpe WF, et al. Increasing saving behavior through age-progressed renderings of the future self. J Mark Res. 2011;48(SPL):S23–S37. doi:10.1509/jmkr.48.SPL.S23

48. Nenkov GY, Inman JJ, Hulland J. Considering the future: the conceptualization and measurement of elaboration on potential outcomes. J Consum Res. 2008;35(1):126–141. doi:10.1086/525504

49. Bartels DM, Urminsky O. To know and to care: how awareness and valuation of the future jointly shape consumer spending. J Consum Res. 2015;41(6):1469–1485. doi:10.1086/680670

50. Mead NL, Williams LE. The pursuit of meaning and the preference for less expensive options. J Consum Res. 2022. doi:10.1093/jcr/ucac019

51. Faul F, Erdfelder E, Buchner A, Lang A-G. Statistical power analyses using G* Power 3.1: tests for correlation and regression analyses. Behav Res Methods. 2009;41(4):1149–1160. doi:10.3758/BRM.41.4.1149

52. Semin GR, Higgins T, De Montes LG, Estourget Y, Valencia JF. Linguistic signatures of regulatory focus: how abstraction fits promotion more than prevention. J Pers Soc Psychol. 2005;89(1):36. doi:10.1037/0022-3514.89.1.36

53. Yang W, Li Q, Guo M, Fan Q, He Y. The effects of power on human behavior: the perspective of regulatory focus. Acta Psychol Sin. 2017;49(3):404. doi:10.3724/SP.J.1041.2017.00404

54. Pham MT, Avnet T. Contingent reliance on the affect heuristic as a function of regulatory focus. Organ Behav Hum Decis Process. 2009;108(2):267–278. doi:10.1016/j.obhdp.2008.10.001

55. Förster J, Higgins ET, Werth L. How threat from stereotype disconfirmation triggers self-defense. Soc Cogn. 2004;22(1: Special issue):54–74. doi:10.1521/soco.22.1.54.30982

56. Vallacher RR, Wegner DM. Levels of personal agency: individual variation in action identification. J Pers Soc Psychol. 1989;57(4):660. doi:10.1037/0022-3514.57.4.660

57. Xu J, Jiang Z, Dhar R. Mental representation and perceived similarity: how abstract mindset aids choice from large assortments. J Mark Res. 2013;50(4):548–559. doi:10.1509/jmr.10.0390

58. Spiller SA. Opportunity cost consideration. J Consum Res. 2011;38(4):595–610. doi:10.1086/660045

59. Sharma E, Alter AL. Financial deprivation prompts consumers to seek scarce goods. J Consum Res. 2012;39(3):545–560. doi:10.1086/664038

60. Podsakoff PM, Organ DW. Self-reports in organizational research: problems and prospects. J Manage. 1986;12(4):531–544. doi:10.1177/014920638601200

61. Hayes AF. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. Guilford Publications; 2017.

62. Wen Z, Ye B. Analyses of mediating effects: the development of methods and models. Adv Psychol Sci. 2014;22(5):731. doi:10.3724/SP.J.1042.2014.00731

63. Parkin M. Opportunity cost: a reexamination. J Econ Educ. 2016;47(1):12–22. doi:10.1080/00220485.2015.1106361

64. Fernbach PM, Kan C, Lynch JG Jr. Squeezed: coping with constraint through efficiency and prioritization. J Consum Res. 2015;41(5):1204–1227. doi:10.1086/679118

65. Frederick S, Novemsky N, Wang J, Dhar R, Nowlis S. Opportunity cost neglect. J Consum Res. 2009;36(4):553–561. doi:10.1086/599764

66. Lynch JG Jr, Netemeyer RG, Spiller SA, Zammit A. A generalizable scale of propensity to plan: the long and the short of planning for time and for money. J Consum Res. 2010;37(1):108–128. doi:10.1086/649907

67. Venus M, Johnson RE, Zhang S, Wang X-H, Lanaj K. Seeing the big picture: a within-person examination of leader construal level and vision communication. J Manage. 2019;45(7):2666–2684. doi:10.1177/0149206318761576

© 2023 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2023 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.