Back to Journals » Risk Management and Healthcare Policy » Volume 19

Financial Management Innovation in Hospital Groups: An Empirical Study of Ophthalmology Specialty Care Under Consolidation

Received 28 January 2026

Accepted for publication 11 May 2026

Published 18 May 2026 Volume 2026:19 599522

DOI https://doi.org/10.2147/RMHP.S599522

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Keon-Hyung Lee

Bihui Ye,1 Xiaoqiong Pan,2 Zhengxing Wu3

1Expanding Cooperation Department, Eye Hospital, Wenzhou Medical University, Wenzhou City, Zhengjiang Province, People’s Republic of China; 2Administration Department, Community Health Service Center of Nanbaixiang Street of Ouhai District, Wenzhou City, Zhengjiang Province, People’s Republic of China; 3Department of Infectious Diseases, Wenzhou Medical University Affiliated Wenzhou Central Hospital, Wenzhou City, Zhengjiang Province, People’s Republic of China

Correspondence: Zhengxing Wu, Department of Infectious Diseases, Wenzhou Medical University Affiliated Wenzhou Central Hospital, 252 Baili East Road, Lucheng District, Wenzhou City, 325000, People’s Republic of China, Tel +86 057788882121, Email [email protected]

Objective: This study examines financial management innovation in a provincial public ophthalmology hospital group in China, focusing on associations among consolidation, shared services, digital transformation, financial performance, and operational efficiency.

Methods: We used a mixed-methods single-case design. The quantitative analysis used a campus-month panel from January 2020 to December 2024 (2 campuses x 60 months; N=120 campus-month observations), with descriptive statistics, correlation analysis, and campus fixed-effects pre-post association models with clustered standard errors. Semi-structured interviews with 28 managers and key staff were audio-recorded, transcribed, and thematically coded.

Results: Consolidation and digital transformation were associated with higher operating margins and improved process performance, but estimates should be interpreted as observational associations. In adjusted models, the post-consolidation period was associated with 2.8– 3.4 percentage points higher operating margins. Centralized procurement was associated with 18% lower average supply cost in participating categories, and RPA-supported claims processing was associated with a 35% shorter processing cycle and 94% accuracy. The absence of a financial shared service center remained associated with inefficiencies, including an average accounts payable cycle of 45 days.

Conclusion: In this single-case observational study, hospital group consolidation was associated with higher operating margins, especially when paired with selective digital transformation. The findings are hypothesis-generating and suggest that integration benefits may depend on shared service implementation and interoperable digital platforms.

Keywords: hospital consolidation, hospital shared services, robotic process automation, ophthalmology hospitals, financial performance

Introduction

The healthcare industry globally faces unprecedented challenges in balancing quality care delivery with financial sustainability. Specialty hospital groups, particularly in ophthalmology, must navigate complex financial pressures while maintaining excellence in clinical outcomes.1 The trend toward hospital consolidation has accelerated significantly, with studies showing that 68% of community hospitals were part of larger health systems by 2022, compared with 53% in 2005.2

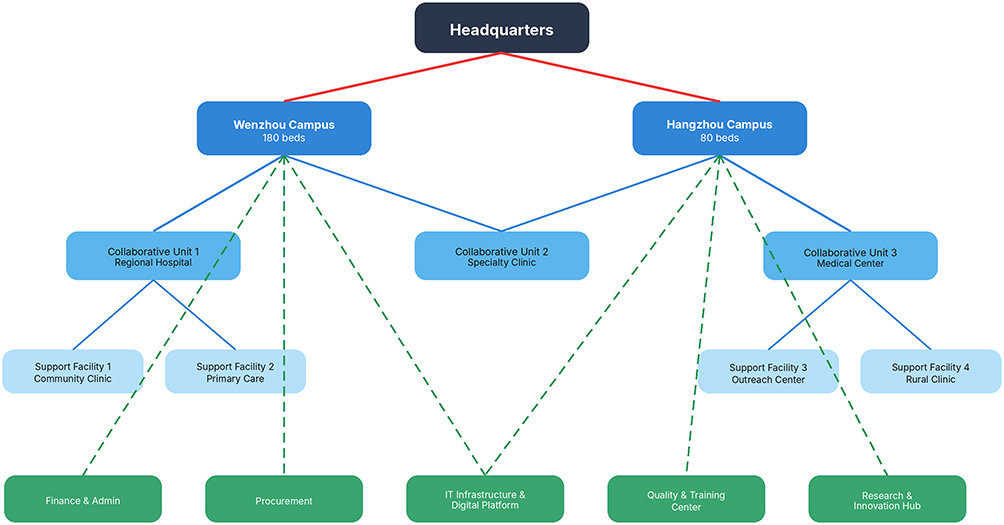

Consolidation refers specifically to the process through which previously independent or loosely affiliated healthcare resources and service capacities are systematically restructured into a unified and coordinated hospital group architecture. This involves not only organizational merger but also operational integration across financial management, procurement, information systems, and clinical protocols. The consolidation model examined here encompasses a three-tier structure comprising core hospitals, collaborative units, and support facilities—all aimed at achieving economies of scale and scope while maintaining specialty care excellence. This definition distinguishes our focus from mere corporate mergers, emphasizing instead the depth of operational and strategic alignment required to realize financial and clinical synergies in specialty care settings.3–5

Recent evidence suggests that hospital consolidation can be associated with efficiency gains through economies of scale, though the magnitude and durability of these associations remain debated.6 While some studies report cost reductions, others identify higher prices without corresponding quality improvements.7,8 The application of scale economies theory to specialty care must account for unique dynamics, such as high-cost specialized equipment, concentrated expertise, and distinct patient referral patterns.9–11 This complexity creates a critical gap in understanding how consolidation and financial innovation interact in specialty contexts.

Digital transformation has emerged as a critical enabler of financial management innovation in healthcare. Prior evidence suggests that RPA and related automation tools can improve administrative efficiency, reduce repetitive manual work, and support more timely claims management.7–9 Within China’s healthcare reform context, digital transformation is increasingly framed as a strategy to support integrated care delivery and improve financial sustainability amid systemic pressures.

From a practical perspective, ophthalmology practices face specific financial challenges including declining reimbursement rates, high capital requirements for advanced surgical equipment, and the need to balance insurance-covered procedures with elective services.12 The average ophthalmology ambulatory surgery center generates substantial annual revenue and remains highly sensitive to throughput, payer mix, and equipment utilization, highlighting both the opportunity and pressure for efficient financial management.13–15

This study addresses three primary research questions: (1) How is hospital group consolidation associated with financial performance and operational efficiency in specialty ophthalmology care? (2) What role do shared service centers and centralized financial management appear to play in realizing these associations? (3) How might digital transformation, particularly RPA and integrated platforms, strengthen financial management within multi-site specialty hospital groups?

Our research makes three distinct contributions to the literature. First, it provides empirical evidence on financial management outcomes within a consolidated specialty care context, addressing a gap in research that has predominantly focused on general acute care hospitals. Second, it examines the interplay between consolidation strategies and digital transformation initiatives. Third, it presents a detailed case study of a three-tier hospital group structure within the Chinese healthcare policy landscape, offering practice-oriented insights for administrators navigating similar integration pathways.

Research Design

Research Object and Context

This study examines a provincial public ophthalmology specialty hospital system in China that exemplifies the complexities of modern healthcare consolidation. The institution was originally established in Wenzhou in 1998 as a specialized eye care facility, responding to the region’s growing demand for advanced ophthalmology services. In 2010, recognizing the need to expand access and leverage economies of scale, the organization established a second major campus in Hangzhou, creating a dual-campus structure that would later evolve into a comprehensive three-tier hospital group. This three-tier structure consists of (1) core hospital campuses providing comprehensive specialty care, (2) collaborative units offering focused services through partnership agreements, and (3) support facilities providing auxiliary and community-based care, as shown in Figure 1. The organizational evolution reflects broader trends in Chinese healthcare reform, particularly the government’s emphasis on developing regional medical consortiums to improve care coordination and resource utilization. The current infrastructure comprises 260 total beds distributed across the two main campuses, with Wenzhou maintaining 180 beds and Hangzhou operating 80 beds. Despite the significant increase in the service volume of ophthalmology outpatient clinics and day surgeries, a considerable number of beds are maintained for the following reasons: (1) Patients with complex ophthalmic diseases (such as severe retinal detachment, complex eye trauma, and those undergoing ophthalmic surgeries with comorbid systemic diseases) still require multi - day hospitalization and peri - operative management; (2) As a regional ophthalmic diagnosis and treatment center, it is necessary to admit patients with difficult and severe conditions referred by collaborating units; (3) Inpatient services are an important platform for the standardized training of ophthalmology specialists and clinical scientific research; (4) Maintaining an appropriate number of beds is beneficial for coping with public health emergencies and fluctuations in service demand, ensuring the resilience of the system. This bed distribution reflects both historical development patterns and strategic decisions about service concentration. The Wenzhou campus, as the original facility, serves as the primary center for complex surgical procedures and medical education, while the Hangzhou campus focuses on expanding geographic access and developing subspecialty services. The operational scale achieved in 2024 demonstrates the system’s maturity: 1.2788 million outpatient visits, 90,200 surgical procedures performed, and 53,600 inpatient discharges. These volume metrics position the hospital group among the leading ophthalmology centers in China, comparable to other major specialty institutions in Beijing and Shanghai. The institutional and regulatory context significantly shapes the hospital group’s financial management approach. As a provincial-level public institution, the hospital operates within China’s dual-track healthcare system, balancing public service obligations with market-oriented reforms. The implementation of Diagnosis-Related Group (DRG) payment systems and provincial-level centralized procurement initiatives has fundamentally altered revenue structures and cost management strategies. The hospital must navigate complex relationships with multiple stakeholders including provincial health commissions, municipal governments, insurance funds, and affiliated medical institutions. This regulatory complexity creates both constraints and opportunities for financial innovation, particularly in areas such as shared service development and digital transformation initiatives.

|

Figure 1 Three-tier organizational structure of the provincial ophthalmology hospital group. The dark navy node represents the headquarters, blue nodes represent core hospital campuses, light-blue nodes represent collaborative units and support facilities, and green nodes represent group-level administrative and technical support functions. Solid red lines indicate governance relationships from the headquarters to the core campuses; solid blue lines indicate operational referral or service relationships; green dashed lines indicate shared-service, administrative, or technical support linkages. |

Data Sources and Variables

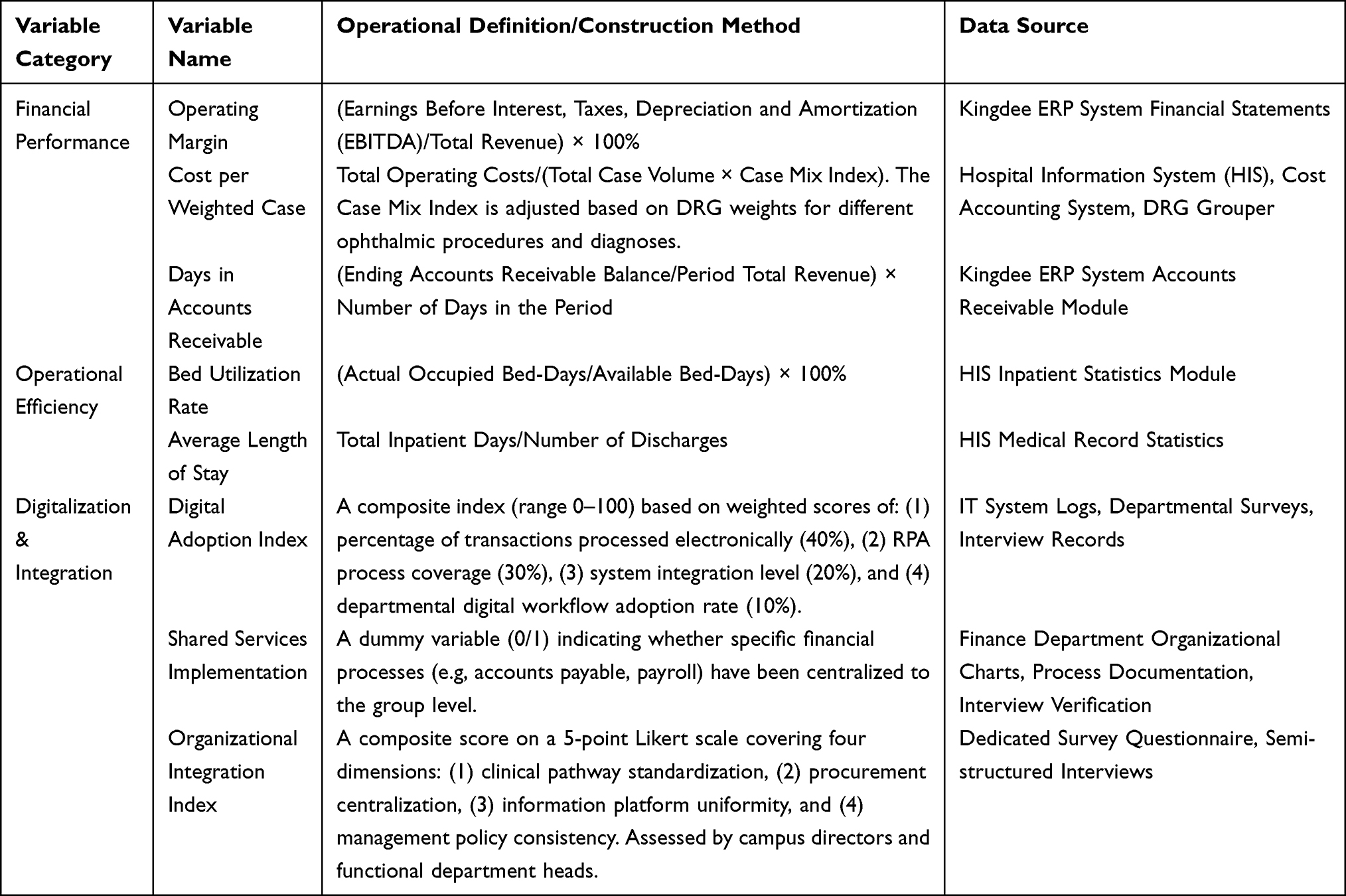

The research employs a comprehensive multi-source data collection strategy designed to capture both quantitative performance metrics and qualitative insights into financial management processes. Primary quantitative data were extracted from the hospital information system, ERP platform, cost accounting system, and administrative finance records. The analytic panel contains 120 campus-month observations from two main campuses over 60 consecutive months. Qualitative data were derived from 28 semi-structured interviews with managers, finance staff, procurement personnel, and clinical department leaders, supplemented by internal process documents and field observations. Table 1 summarizes the operational definitions, construction methods, and data sources of the key variables used in the analysis.

|

Table 1 Definitions, Construction, and Sources of Key Variables |

In the panel dataset used in this study, missing values mainly occur in monthly operational indicators and a small number of financial process fields. Missingness was low (<4.5% across all modeled variables) and was concentrated in isolated months rather than systematic blocks. We used mean imputation only for descriptive continuity in a limited number of monthly fields and retained complete-case estimation for the regression models. Because mean imputation can attenuate variance and introduce bias, this decision is treated as a methodological limitation and is revisited in the Discussion.

Research Methods

The methodological approach integrates quantitative and qualitative techniques to provide a comprehensive understanding of financial management innovation in the hospital group context. The quantitative component should be interpreted as a campus fixed-effects pre-post association analysis rather than a classical difference-in-differences design, because both campuses entered the group-wide intervention environment during the same period and no untreated control campus was available. Accordingly, all estimates are framed as within-system temporal associations rather than causal treatment effects.

In the regression analysis, the core explanatory variable “integration” is operationalized as a post-restructuring indicator that equals 1 after the group completed the major consolidation milestone and 0 beforehand. The models additionally include patient volume, case-mix complexity, payer-mix composition, and campus and month fixed effects. Standard errors are clustered at the campus level to account for serial correlation and heteroscedasticity. Given the modest panel size (N=120 campus-month observations), the subgroup analyses are treated as exploratory, and severely underpowered payer-based splits were not retained in the revised main table.

The qualitative research component employs semi-structured interviews and observational studies to capture nuanced aspects of financial management processes that quantitative metrics alone cannot fully explain. Interview guides covered procurement integration, digital workflow redesign, budgeting practices, and perceived barriers to shared-service implementation. All interviewees provided verbal informed consent before participation, and transcripts were de-identified prior to analysis.

The analytical integration of quantitative and qualitative data follows an explanatory sequential design where quantitative findings inform qualitative inquiry directions, and qualitative insights help interpret quantitative patterns. The thematic analysis of the interview transcripts adopted a method that combined deductive coding based on a theoretical framework with inductive coding for identifying emerging themes. The coding process was systematically organized and analyzed using NVivo software and completed by two independent coders. (Modification note: The confidence interval of the Kappa statistic and its calculation basis are supplemented). The inter-coder reliability was 0.82 (Cohen’s kappa, 95% CI: 0.76–0.88). This estimate was calculated based on a randomly selected sample of 150 coded segments (accounting for 15% of the total number of coded segments). The validity of the study was enhanced through triangulation among different data sources by comparing statistical patterns, participants’ views, and observational evidence.

This mixed-methods approach enables examination of both “what” questions addressed through quantitative metrics and “how” and “why” questions explored through qualitative investigation.

This study was conducted in accordance with the declaration of Helsinki and reviewed by the Ethics Committee of the Eye Hospital of Wenzhou Medical University and was determined to be exempt from full ethics review because the quantitative component used de-identified administrative records and the qualitative interviews involved non-sensitive professional perspectives. Verbal informed consent was obtained from all interview participants before recording and transcription.

Empirical Results

The empirical analysis of this study focuses on intervention components with direct and observable associations with financial and operational performance, namely centralized procurement and selected digital transformation initiatives. Given the observational design, all quantitative findings are reported as adjusted associations rather than causal effects.

Descriptive Statistics and Correlation Analysis

This section presents the descriptive statistical profile and correlations of the hospital group’s operational and financial performance based on administrative data, with results summarized in Table 2 and Table 3.

|

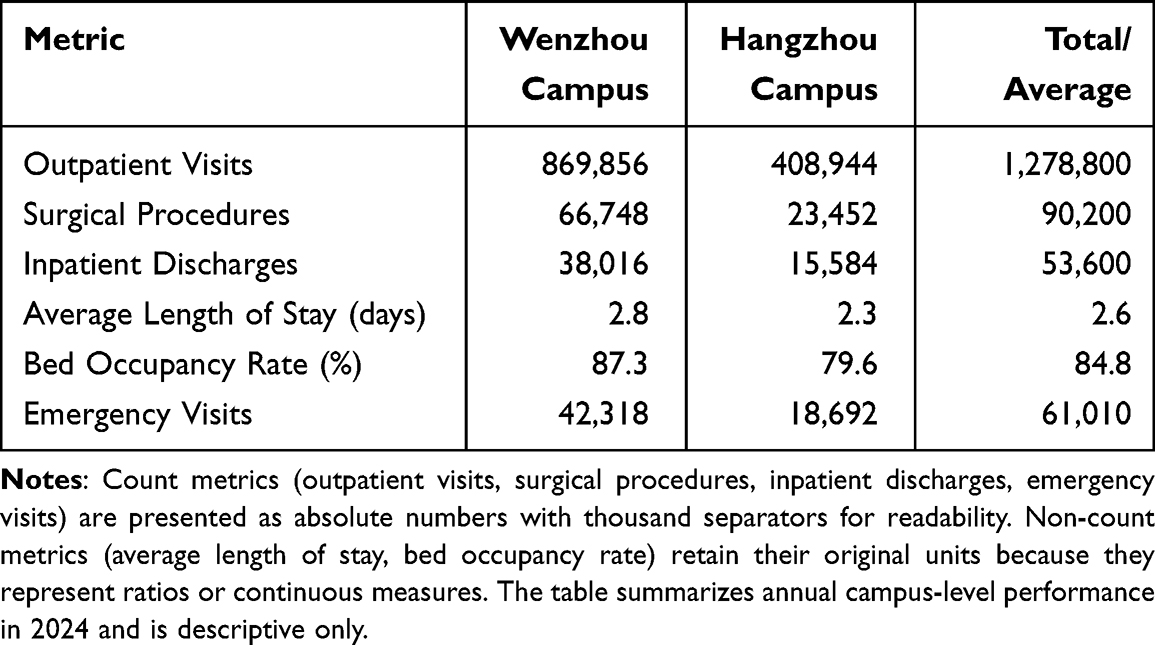

Table 2 2024 Operational Performance Indicators (Unit of Analysis: Campus-Year; Count Metrics in Absolute Numbers) |

|

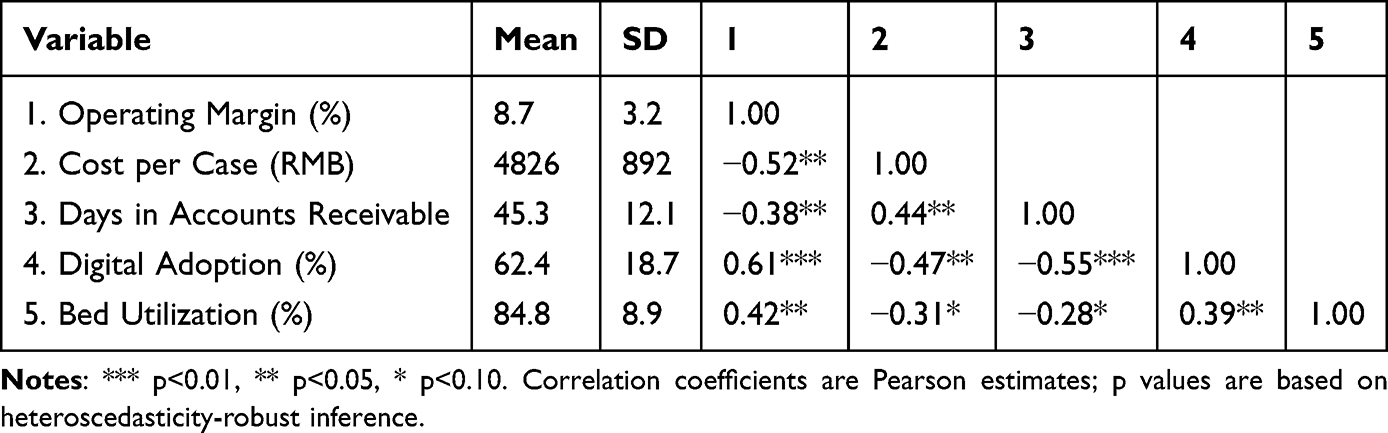

Table 3 Descriptive Statistics and Correlation Matrix (Unit of Analysis: Campus-Month) |

The descriptive analysis reveals substantial variation in operational and financial performance metrics across the hospital group’s facilities and over time. Table 2 presents the 2024 operational performance indicators, demonstrating the scale achieved through the consolidated structure. The combined outpatient volume of 1.2788 million visits represents a 15% increase from 2022 levels, with the Wenzhou campus accounting for 68% of total visits and Hangzhou contributing 32%. Surgical volumes show even greater concentration, with Wenzhou performing 74% of the 90,200 total procedures, reflecting its role as the primary referral center for complex cases. The distribution of surgical types indicates specialization patterns: cataract surgeries comprise 52% of total volume, followed by refractive procedures (18%), vitreoretinal surgeries (15%), glaucoma interventions (10%), and other procedures (5%).

Financial performance metrics displayed in Table 3 reveal both achievements and ongoing constraints in the current management structure. The correlation matrix shows that operating margin was negatively correlated with cost per case (r = −0.52, p < 0.05) and days in accounts receivable (r = −0.38, p < 0.05). Digital adoption was positively correlated with operating margin (r = 0.61, p < 0.01) and negatively correlated with days in accounts receivable (r = −0.55, p < 0.01).

The temporal analysis reveals important trends in financial management evolution. Operating margins improved from 5.2% in 2020 to 8.7% in 2024, driven primarily by revenue growth outpacing cost increases. Revenue per outpatient visit increased by 18% over the period while cost per visit rose only 11%, indicating improved operational efficiency. However, this aggregate improvement masks significant variation: margins for insurance-covered procedures declined by 2.3 percentage points due to reimbursement pressures, while margins for self-pay services increased by 4.8 percentage points. This divergence highlights the importance of service mix management and the financial vulnerability created by reimbursement dependencies.

Regression Results: Associations Between Consolidation and Financial Performance

This section estimates the adjusted association between group integration measures and financial performance after controlling for observed time-varying covariates and fixed campus characteristics.

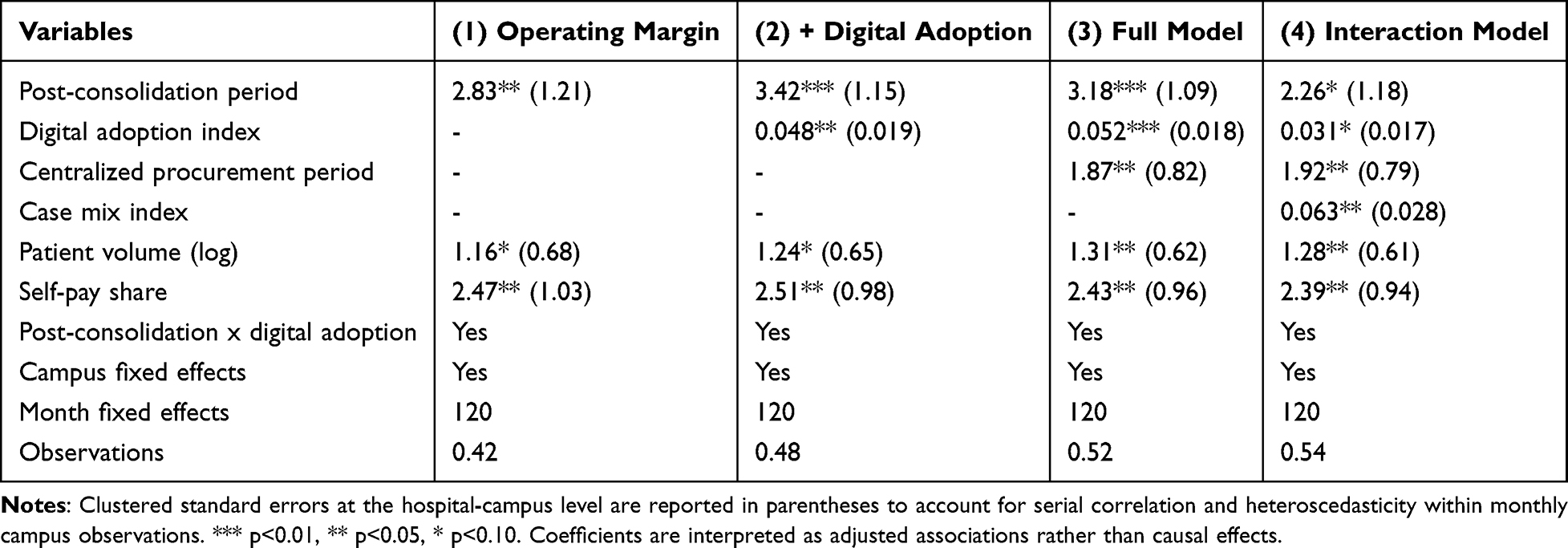

The regression analysis examines how hospital group characteristics and management practices are associated with financial outcomes. Table 4 presents results from multiple model specifications, progressively adding control variables and interaction terms. In the baseline model (Column 1), the post-consolidation period is associated with a 2.83 percentage point higher operating margin (SE 1.21; approximate 95% CI 0.46 to 5.20). This association increases to 3.42 percentage points in Column 2 after accounting for digital adoption (SE 1.15; approximate 95% CI 1.17 to 5.67), and remains 3.18 percentage points in the full model (SE 1.09; approximate 95% CI 1.04 to 5.32). These estimates are directionally consistent but should be interpreted as associations within a single system rather than as transportable causal effects.

|

Table 4 Regression Results: Association of Consolidation with Financial Performance (Unit of Analysis: Campus-Month) |

The analysis of cost efficiency reveals nuanced patterns. Centralized procurement, implemented in July 2021, was associated with an 18% lower average supply cost for participating categories relative to the pre-implementation baseline period (January 2020 to June 2021). This percentage change reflects the difference between the mean monthly cost per equivalent procurement unit in the 18 months after implementation and the corresponding 18-month baseline period. The largest relative reductions were observed for high-volume consumables (22%) and pharmaceutical products (19%).

The interaction term in Column 4 indicates that consolidation and digital transformation may be jointly associated with financial performance, although the estimate is imprecise and should be interpreted cautiously. The coefficient of 0.063 (95% CI 0.008 to 0.118) implies that a campus with a digital adoption index of 75, approximately one standard deviation above the mean, would be expected to have an additional 4.7 percentage point post-consolidation margin association relative to a campus at the sample mean of 50. Because this estimate is derived from a small observational panel, it should be viewed as exploratory.

Robustness Checks and Exploratory Heterogeneity Analysis

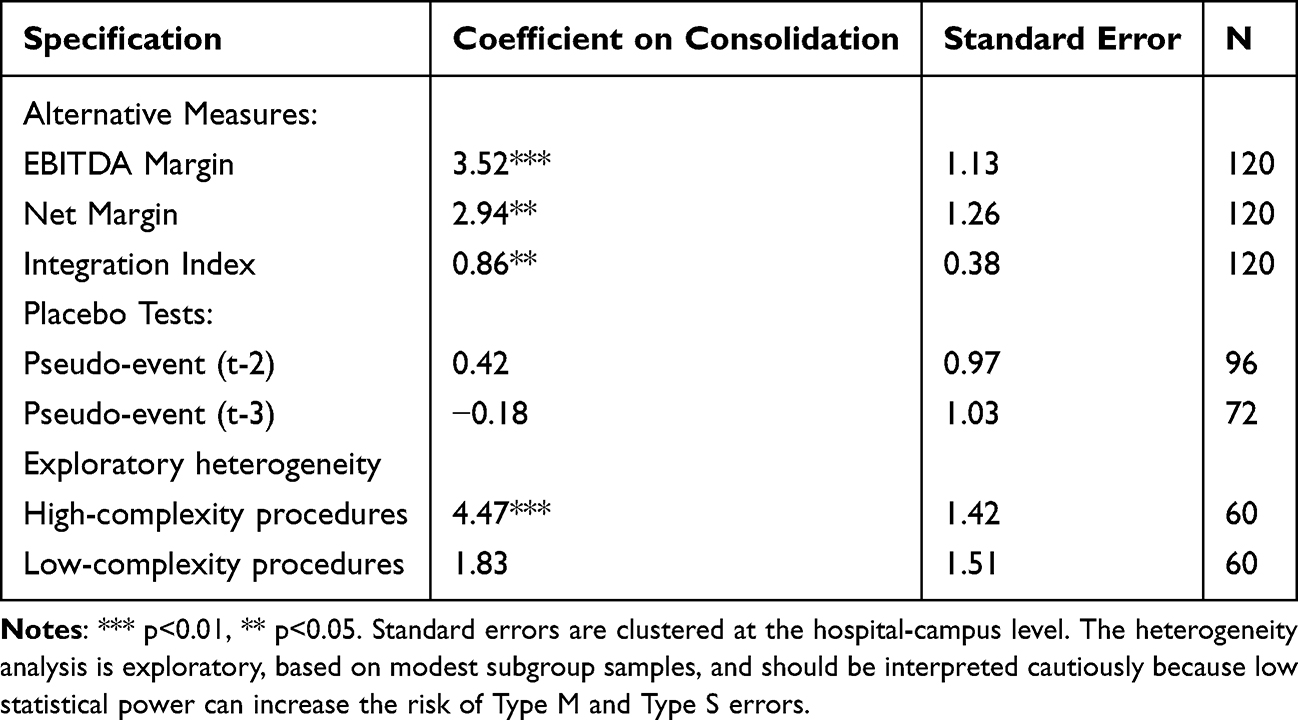

To examine the stability of the main findings, we conducted a series of robustness checks summarized in Table 5. Alternative outcome definitions yielded similar coefficient magnitudes: using EBITDA margin instead of operating margin produced a consolidation coefficient of 3.52 (SE 1.13), and using net margin produced a coefficient of 2.94 (SE 1.26). Placebo tests based on pseudo-event timing were not statistically significant. We retained only one pre-specified heterogeneity comparison based on procedure complexity, because payer-based subgroup splits were underpowered and produced unstable estimates in the original version.

|

Table 5 Robustness Tests and Exploratory Heterogeneity Analysis (Unit of Analysis: Campus-Month) |

The exploratory heterogeneity analysis suggests a possible tendency toward larger positive associations in high-complexity service areas than in low-complexity areas, but this pattern requires confirmation in larger multi-center samples. The complexity split was retained because it aligns with the study’s clinical and economic rationale: advanced ophthalmic procedures involve higher fixed capital intensity, greater coordination requirements, and more scope for standardization benefits. Even so, the subgroup sample sizes are modest (n=60 in each subgroup), and the estimates should be interpreted with caution because Type M and Type S errors remain possible in small samples.

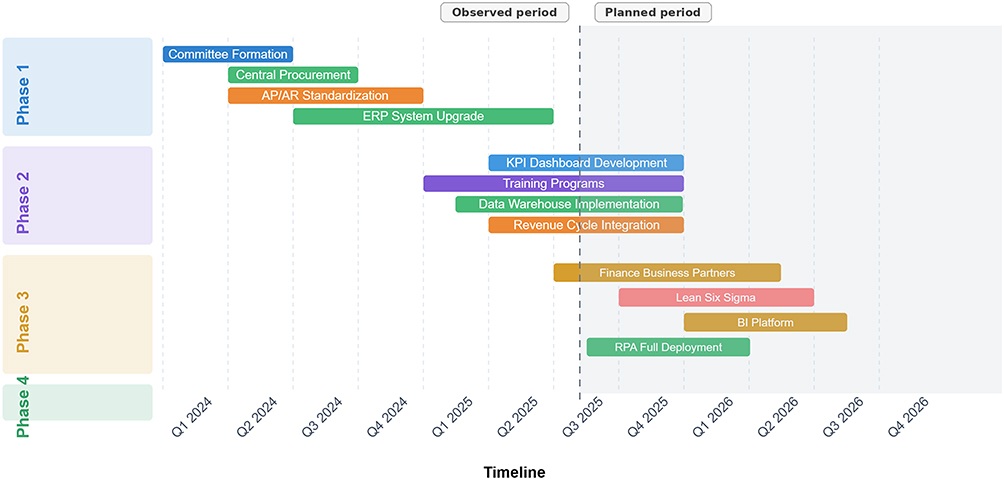

Case Analysis: Digital Transformation and Process Innovation

The qualitative case analysis provides detailed insight into successful and constrained transformation initiatives, as referenced in Figure 2, which presents the hospital group’s financial shared-services and digital transformation roadmap. The centralized procurement case illustrates how targeted integration can be associated with substantial operational benefits even without a fully implemented shared-service center. By consolidating purchasing across both campuses and leveraging combined volumes, the hospital group was associated with lower supply costs and improved supply-chain reliability. Standardization of product specifications reduced SKU counts by 35%, simplifying inventory management and lowering carrying costs. Vendor consolidation from 287 to 142 suppliers strengthened negotiating leverage and reduced transaction complexity. The implementation process faced initial resistance from clinical departments accustomed to product-specific preferences, but structured physician engagement and evidence-based product review ultimately achieved 91% clinician satisfaction with standardized products.

|

Figure 2 Financial shared-services and digital transformation roadmap. The horizontal bars indicate the implementation period of each initiative by quarter. The left labels denote implementation phases. The vertical dashed line separates the observed period from the planned period, and the grey shaded area represents planned later-stage implementation rather than completed activities. Bar colours distinguish initiative categories: blue indicates governance or dashboard development, green indicates procurement, ERP, data warehouse, or RPA-related digital infrastructure, Orange indicates standardization or revenue-cycle integration, purple indicates training programmes, gold indicates finance business partner or BI platform development, and red indicates Lean Six Sigma process improvement. |

The RPA deployment in claims processing represents a particularly successful digital transformation initiative. Before automation, the claims process required an average of 4.2 FTEs and took 8 to 12 days from submission to payment posting. The phased RPA solution now processes 78% of claims automatically. Processing time declined to 3 to 5 days, and accuracy improved from 87% to 94%. The freed capacity allowed redeployment of staff to more complex claims requiring human judgment and payer communication. The system now processes routine claims overnight, enabling next-day submission for services rendered on the previous day. Exception-handling protocols flag unusual claims for manual review, preserving quality while maximizing automation. The associated financial changes included a reduction in days sales outstanding from 52 to 45 days, a decline in claim denial rates from 8.2% to 5.1%, and estimated annual labor savings of RMB 1.8 million.

However, the case analysis also reveals substantial implementation challenges, particularly in achieving cross-campus integration without a unified shared-service platform. The absence of a financial shared service center creates duplicate transaction processing across campuses, inconsistent application of financial policies, limited workload balancing during peak periods, and fewer opportunities for staff specialization. Interview participants consistently identified these issues as major barriers to realizing the full potential of consolidation. One finance manager noted that “we often find ourselves recreating the wheel at each campus, unable to leverage learnings and best practices effectively”. The current structure maintains separate accounts payable teams at each campus, resulting in average payment cycles of 45 days compared with approximately 30-day benchmarks at institutions with centralized processing.

Discussion

Our research contributes to the literature in several ways. First, it provides empirical evidence on financial management innovation in a specialty care context, addressing a gap in research that has predominantly focused on general acute care hospitals. Second, it examines how consolidation and digital transformation appear to operate together within a specialty system. Third, it presents a detailed case study of a three-tier hospital group structure, providing practice-oriented insights for healthcare administrators navigating similar transformations.

Our findings both confirm and extend previous research on hospital consolidation and financial management innovation. Consistent with recent studies showing mixed results from hospital mergers, we find that consolidation alone does not guarantee financial improvement.16 The 2.8–3.4 percentage point operating-margin association observed here falls within the range reported in recent syntheses, though the specialty care context adds important nuance.17 Unlike studies of general acute care hospitals that often identify minimal or mixed quality associations with consolidation, our analysis suggests that specialty-focused integration may reduce some coordination frictions while also introducing new administrative bottlenecks when financial systems remain fragmented.18–20

Our analysis of the absent shared-service center provides empirical support for theoretical arguments that operational integration is crucial for translating structural consolidation into sustained administrative efficiency. Studies of shared-services implementation in other sectors and health systems emphasize standardization, specialization, and transaction visibility as core mechanisms.21,22 In our case, procurement and selected digital workflows were associated with measurable improvements, whereas decentralized finance processing remained a persistent source of drag.

Qualitative insights from interviews help explain the mechanisms and constraints underlying these quantitative patterns. For example, the persistently long accounts payable cycle appears linked not simply to volume growth but to duplicated approval chains, inconsistent coding practices, and limited cross-campus workload sharing. These observations reinforce the interpretation that structural merger alone is insufficient and that process redesign mediates whether positive financial associations are realized.

The exploratory heterogeneity analysis suggests a potential trend toward larger positive associations in high-complexity service areas, though this pattern requires confirmation in larger samples. A plausible explanation is that advanced specialty care has higher fixed-cost intensity and therefore greater room for coordination and scale-related efficiencies. At the same time, the subgroup estimates are based on modest sample sizes and should not be overinterpreted.

Based on our empirical findings and international experience, we propose a provisional framework for financial management innovation in specialty hospital groups. The framework should be viewed as a hypothesis-generating model derived from a single institutional case rather than a universal prescription.

The organizational integration pathway begins with governance structures that balance autonomy with standardization. The case hospital’s experience suggests that successful integration requires clear decision rights, harmonized coding and budgeting rules, and transparent accountability for cross-campus processes.

Digital enablement appears to proceed through three overlapping stages: automation of existing processes, integration across systems, and intelligence augmentation through analytics. The RPA claims-processing case supports the feasibility of the first stage, whereas the slower progress in ERP and shared-service integration illustrates the implementation demands of the second stage.

Capability development represents the often-overlooked human dimension of financial transformation. Our findings suggest that finance departments with more analytically trained staff may adapt more quickly to standardized workflows and data-driven management, although this proposition also requires validation in larger samples.

The study’s findings carry implications for healthcare executives leading specialty hospital groups, but these implications should be interpreted cautiously. First, the results emphasize that operational integration is at least as important as formal organizational merger. Second, the observed relationship between consolidation and digital adoption suggests that technology investment may be most valuable when paired with process standardization rather than pursued as a stand-alone initiative.

The association between consolidation and digital transformation also suggests that technology investment should not necessarily be deferred during integration. However, because this study does not identify causal effects, the sequencing implications are best understood as practical hypotheses for future evaluation rather than definitive prescriptions.

The findings invite reflection on policy and practice beyond the single case. For policymakers and health-system planners, the results suggest that structural consolidation may not translate into administrative efficiency unless supported by interoperable data systems, standardized workflows, and governance mechanisms that enable shared services. These propositions should be tested in broader comparative settings before they inform generalized policy mandates.

As a case study of a large-scale, high-volume provincial specialty center, our findings are necessarily contextual. The magnitude of the reported associations, particularly the procurement and digital workflow gains, may not generalize to smaller hospitals, non-specialty settings, or systems operating under different payment incentives.

The specialty care focus of our study also highlights important considerations for healthcare system design. While general hospital consolidation often raises concerns about access and care continuity, specialty service concentration can improve both quality and efficiency by enabling expertise development and equipment utilization optimization.23 Policy makers should distinguish between consolidation types, potentially supporting specialty service regionalization while maintaining distributed primary care access. The success of our case hospital’s three-tier structure, balancing centralized specialty services with distributed access points, provides a potential model for other regions seeking to optimize specialty care delivery.24

Finally, our findings contribute to evolving discussions about healthcare financial sustainability in the face of demographic transitions and technological advancement. The aging population drives increased demand for ophthalmology services, with age-related conditions such as cataracts, glaucoma, and macular degeneration becoming increasingly prevalent. Our analysis suggests that consolidated specialty providers with strong digital capabilities are better positioned to meet this growing demand efficiently. The 15% increase in outpatient volumes achieved while improving margins demonstrates that efficiency and access need not be opposing goals when appropriate organizational and technological infrastructure exists.

This study has several limitations that suggest directions for future work. First, as a single-case study within a specific Chinese provincial context, the generalizability of findings is limited. Second, the quantitative analysis relies on a relatively small campus-month panel and lacks an external control group, so the estimates should not be interpreted causally. Third, some descriptive variables required limited mean imputation, which may attenuate variance. Fourth, the exploratory subgroup analysis remains underpowered even after revision. Future research should use multi-center data, larger panels, and prospectively specified subgroup analyses to test whether the associations reported here replicate in other specialty hospital systems.

Conclusion

This single-case observational study, limited by sample size, selective mean imputation, and the absence of an external control group, finds that hospital group consolidation was associated with higher operating margins, particularly when paired with digital transformation. The results also suggest that targeted integration in procurement and claims processing may support administrative efficiency, whereas incomplete shared-service implementation may constrain broader gains.

For hospital managers, the findings support three cautious priorities: establishing shared financial service functions, sequencing digital investments with workflow standardization, and strengthening cross-campus governance for data and process integration. For researchers and policymakers, the present study should be treated as hypothesis-generating evidence that requires validation in larger comparative designs before stronger generalizations are made.

Data Sharing Statement

All data generated or analysed during this study are included in this article. Further enquiries can be directed to the corresponding author.

Ethics Approval and Consent to Participate

This study was conducted in accordance with the Declaration of Helsinki. The study protocol was reviewed by the Ethics Committee of the Eye Hospital of Wenzhou Medical University and was determined to be exempt from full ethics review because the quantitative component used de-identified administrative records and the qualitative interviews involved non-sensitive professional perspectives. Verbal informed consent was obtained from all interview participants before audio recording and transcription.

Consent for Publication

Not applicable. This manuscript does not contain any identifiable individual-level data, images, or personal information.

Funding

This work was funded by Wenzhou Science and Technology Plan Project (SC20250027).

Disclosure

The authors declare that they have no competing interests in this work.

References

1. Smith JF, Hintze BC, Anderson ST, Tailor PD, Xu TT, Starr MR. Trends in ophthalmology practice consolidation: 2015-2022. Ophthalmology. 2023;130(8):812–12. doi:10.1016/j.ophtha.2023.05.006

2. Figueroa JF, Lam MB, Orav EJ, Joynt Maddox KE. Consolidation among cardiologists across U.S. practices over time. J Am Coll Cardiol. 2020;76(5):590–593. doi:10.1016/j.jacc.2020.04.081

3. Yang X, Chen Y, Li C, Hao M. Effects of medical consortium policy on health services: an interrupted time-series analysis in Sanming, China. Front Public Health. 2024;12:1322949. doi:10.3389/fpubh.2024.1322949

4. Meng Q, Fang H, Liu X, et al. Consolidating the social health insurance schemes in China: towards an equitable and efficient health system. Lancet. 2015;386(10002):1484–1492. doi:10.1016/S0140-6736(15)00342-6

5. Dranove D, Lindrooth R. Hospital consolidation and costs: another look at the evidence. J Health Econ. 2003;22(6):1983–1997. doi:10.1016/j.jhealeco.2003.05.001

6. Harrison TD. Consolidation and closures: an empirical analysis of exits from the hospital industry. Health Econ. 2023;32(2):407–429.

7. Topol EJ. High-performance medicine: the convergence of human and artificial intelligence. Nat Med. 2019;25(1):44–56. doi:10.1038/s41591-018-0300-7

8. Research P. Robotic process automation in healthcare market report 2023-2032. Market Research Report. 2023. Available from: https://www.precedenceresearch.com/robotic-process-automation-in-healthcare-market.

9. Sahni N, Wessel M, Christensen C. Administrative simplification: how to save a quarter-trillion dollars in US healthcare. McKinsey & Company Healthcare Insights. 2021.

10. Bernet PM, Singh S. Economies of scale in the production of public health services: an analysis of local health districts. Am J Public Health. 2015;105(S2):S260–S267. doi:10.2105/AJPH.2014.302350

11. Braun RT, Lelli GJ, Pandey A, Zhang M, Winebrake JP, Casalino LP. Association of private equity firm acquisition of ophthalmology practices with medicare spending and use of ophthalmology services. Ophthalmology. 2024;131(3):360–369. doi:10.1016/j.ophtha.2023.09.029

12. Corcoran KJ. Macroeconomic landscape of refractive surgery in the United States. Curr Opin Ophthalmol. 2015;26(4):249–254. doi:10.1097/ICU.0000000000000159

13. Li Y, Chen Y, Ma B, et al. Configurations associated with the efficiency of the ophthalmology departments in public hospitals of Central South China. PLoS One. 2024;19(12):e0315218. doi:10.1371/journal.pone.0315218

14. American Society of Cataract and Refractive Surgery. ASC operating margins and financial performance metrics 2023. ASCRS Industry Survey. 2023.

15. Health VMG. 2023 multi-specialty ASC benchmarking study: ophthalmology performance metrics. Healthcare Valuation Report. 2023.

16. Schwartz K, Lopez E, Rae M, Neuman T. What we know about provider consolidation. Kaiser Family Foundation Issue Brief. 2023.

17. Cooper Z, Craig SV, Gaynor M, Van Reenen J. The price ain’t right? Hospital prices and health spending on the privately insured. Q J Econ. 2019;134(1):51–107. doi:10.1093/qje/qjy020

18. Mariani M, Sisti LG, Isonne C, et al. Impact of hospital mergers: a systematic review focusing on healthcare quality measures. Eur J Public Health. 2022;32(2):191–199. doi:10.1093/eurpub/ckac002

19. Kohl S, Schoenfelder J, Fügener A, Brunner JO. The use of Data Envelopment Analysis (DEA) in healthcare with a focus on hospitals. Health Care Manag Sci. 2019;22(2):245–261. doi:10.1007/s10729-018-9436-8

20. Wu YX, Li YP. Effect of medical insurance package payment in compact county medical community on patient flows. J Nanjing Med Univ. 2023;23:144–149.

21. Tseng P, Kaplan RS, Richman BD, Shah MA, Schulman KA. Administrative costs associated with physician billing and insurance-related activities at an academic health care system. JAMA. 2018;319(7):691–697. doi:10.1001/jama.2017.19148

22. Burns LR, Pauly MV. Transformation of the health care industry: curb your enthusiasm? Milbank Q. 2018;96(1):57–109. doi:10.1111/1468-0009.12312

23. Li X, Krumholz HM, Yip W, et al. Quality of primary health care in China: challenges and recommendations. Lancet. 2020;395(10239):1802–1812. doi:10.1016/S0140-6736(20)30122-7

24. Centers for Medicare & Medicaid Services. Medicare program; CY 2022 payment policies under the physician fee schedule and other changes to Part B payment policies; Medicare shared savings program requirements; provider enrollment regulation updates; and provider and supplier prepayment and post-payment medical review requirements. Fed Regist. 2021;86(221):64996–66031.

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.