Back to Journals » Risk Management and Healthcare Policy » Volume 19

Does Indemnity Private Insurance Increase Healthcare Utilization? Evidence from Korea’s National Health Insurance System

Received 9 March 2026

Accepted for publication 10 June 2026

Published 30 June 2026 Volume 2026:19 607999

DOI https://doi.org/10.2147/RMHP.S607999

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Keon-Hyung Lee

Hongki Gwak1, Seong Hwan Kim2

1Department of Surgery, Jeju National University Hospital, Jeju National University College of Medicine, Jeju, South Korea; 2Department of Plastic and Reconstructive Surgery, Kangnam Sacred Heart Hospital, Hallym University College of Medicine, Seoul, South Korea

Correspondence: Seong Hwan Kim, Department of Plastic and Reconstructive Surgery, Kangnam Sacred Heart Hospital, Hallym University College of Medicine, 1 Singil-ro, Yeongdeungpo-gu, Seoul, 07441, South Korea, Tel +82-2-829-5182, Email [email protected]

Purpose: South Korea’s healthcare system is based on the National Health Insurance (NHI), and private insurance is commonly purchased to cover services not fully reimbursed by the NHI. Rising medical expenditures associated with indemnity-type private health insurance have become a growing policy concern.

Patients and Methods: In this cross-sectional study, adults aged < 65 years without chronic diseases were selected from the Korea Health Panel Survey (2019– 2020). Participants were classified into fixed-benefit or indemnity private insurance groups. Healthcare utilization and expenditures were compared, and multivariable regression models were used to evaluate factors associated with medical use and visit frequency.

Results: A total of 3,320 participants were included in the analysis. The indemnity group showed higher outpatient care use than the fixed-benefit group, with mean outpatient visits of 9.14 versus 7.46 per year. There were no significant differences in expenditures for emergency or inpatient services. In the multivariable analysis, indemnity insurance was associated with higher outpatient care use (adjusted OR, 1.503; 95% CI, 1.232– 1.834) and a higher number of outpatient visits (adjusted IRR, 1.167; 95% CI, 1.069– 1.274).

Conclusion: These findings suggest that indemnity-type private insurance is associated mainly with greater outpatient healthcare utilization and outpatient expenditures among adults without chronic diseases. The findings should be interpreted as outpatient-focused associations rather than evidence of broader system-wide cost effects.

Keywords: fixed-benefit, indemnity, private health insurance, national health insurance, medical care utilization

Introduction

Korea’s National Health Insurance (NHI) system provides universal coverage for the entire population and has substantially improved access to healthcare services. Compared with other OECD countries, Korea maintains relatively low medical fee schedules, which has contributed to high healthcare accessibility and among the highest rates of outpatient visits globally.1 However, despite universal public coverage, patients continue to face out-of-pocket payments due to copayments, deductibles, uncovered services, and non-benefit items. In this context, private health insurance (PHI) has become widely used as a supplementary financial mechanism to reduce the residual economic burden of healthcare. PHI may improve financial protection and access to care, but it may also influence healthcare-seeking behavior and increase service utilization beyond clinically necessary levels.2

The NHI is a compulsory, single-payer scheme covering virtually the entire population—approximately 51 million enrollees as of 2023, with the low-income remainder covered by the tax-financed Medical Aid program—and its total expenditure has risen steadily, from about KRW 86.6 trillion in 2020 to more than KRW 100 trillion by 2025.3 Its benefit package, however, remains comparatively shallow: incomplete coverage of some services and the relatively slow incorporation of newer, often costly drugs, devices, and procedures leave out-of-pocket payments accounting for roughly 30% of total health expenditure, which has approached 10% of gross domestic product.4–6 This residual burden underlies the widespread purchase of PHI: indemnity-type insurance has become the dominant form—often termed a “second national health insurance” and held by about 75% of the population (around 39 million people) as of 2023—whereas fixed-benefit plans represent a smaller share.7 Concerns about overutilization and rapidly rising claims have prompted repeated regulatory redesign of indemnity products—through successive product “generations,” culminating in the fifth-generation plan introduced in 2026—as well as growing government intervention to contain non-benefit overuse. From the perspective of insurance economics, the type of supplemental coverage may be as important as the presence of coverage itself. Fixed-benefit insurance pays a predetermined amount upon diagnosis, hospitalization, or treatment, leaving the insured exposed to residual costs and thereby preserving some degree of cost sensitivity. Indemnity insurance, by contrast, reimburses actual out-of-pocket expenses to a greater extent, thereby substantially reducing the marginal cost of care at the point of service. According to moral hazard theory, individuals facing lower cost-sharing may use more healthcare services than they would under higher cost-sharing. In addition, demand-side incentives created by indemnity coverage may interact with fee-for-service provider payment structures. When patients face fewer cost barriers, providers operating under fee-for-service reimbursement may have greater opportunity to recommend additional consultations, tests, or procedures. This theoretical distinction between insurance types is particularly relevant in South Korea, where indemnity-type PHI has expanded within a fee-for-service NHI system characterized by high accessibility and unrestricted patient choice.8–11

Similar concerns have been raised in other mixed public-private healthcare systems. In France, complementary private insurance covering patient cost-sharing has been associated with greater use of physician services and prescription drugs.12 In the United States, Medicare Supplement (Medigap) insurance has been linked to higher healthcare spending and greater outpatient utilization among elderly beneficiaries.13 In Australia, a mixed public–private health system, private hospital insurance has been discussed in relation to increased elective procedures and potential supplier-induced demand.14 These international findings suggest that the relationship between PHI and healthcare utilization is not unique to Korea, but may vary according to how private insurance interacts with public coverage, patient cost-sharing, and provider payment incentives.

Unlike fixed-benefit plans, indemnity-type PHI in Korea operates as a broad complementary coverage mechanism that reduces patients’ residual out-of-pocket costs under the universal NHI system, including copayments and costs for uncovered services. This institutional feature makes Korea a useful setting for examining how supplemental private coverage may alter healthcare-seeking behavior within a fee-for-service public insurance system.

In Korea, several studies have examined the association between PHI and healthcare utilization or medical expenditure. Prior studies have suggested that supplemental PHI may increase outpatient visits, hospitalization, or medical spending, although the magnitude and direction of the association may differ according to study design, population characteristics, and methods used to address selection bias.15–17

Nevertheless, much of the existing Korean literature has treated PHI as a binary exposure—comparing individuals with and without private insurance—without distinguishing between indemnity and fixed-benefit plan types. Studies using panel-based samples, such as the Korea Health Panel, have similarly tended to pool insurance types, making it difficult to isolate the specific behavioral mechanism through which PHI influences demand. Furthermore, these studies have largely included individuals with chronic diseases, in whom underlying morbidity may strongly confound the relationship between insurance type and healthcare utilization.

To address these gaps, the present study focuses on individuals without chronic diseases and directly compares indemnity-type and fixed-benefit PHI holders. This design allows us to examine whether insurance type—rather than PHI ownership alone—is independently associated with healthcare utilization in a relatively low-baseline-risk population, where service use is less likely to be dominated by established chronic morbidity. At the same time, this design involves an important trade-off: while the exclusion of chronic disease populations may improve internal validity by reducing confounding related to underlying health status and differential underwriting, it limits the generalizability of the findings to patients with chronic illness or high healthcare needs, who may respond differently to insurance incentives.

Therefore, this study aimed to evaluate the association between PHI type and healthcare utilization among individuals without chronic diseases in Korea. In particular, we examined whether indemnity-type PHI and fixed-benefit PHI were differentially associated with outpatient and inpatient healthcare utilization, with consideration of the implications for moral hazard, demand-side incentives, and the role of supplementary private coverage within Korea’s universal NHI system.

Material and Methods

Data and Study Population

This study was a cross-sectional observational analysis using nationally representative data from the Korea Health Panel Survey (KHPS) from 2019 to 2020.18 The KHPS is a collaborative survey conducted by the Korea Institute for Health and Social Affairs and the National Health Insurance Service. The survey uses a two-stage stratified cluster sampling design to represent the Korean population and collects detailed information on socioeconomic characteristics, health status, healthcare utilization, medical expenditures, and private health insurance status. Trained surveyors visited selected households and conducted face-to-face interviews. The KHPS provides de-identified survey data for research purposes.

The analytic dataset was constructed using KHPS data from 2019–2020. When the same individual appeared in both survey years, duplicate observations were excluded so that each participant contributed only one observation to the final analytic dataset. This approach allowed us to use a broader two-year sample while maintaining independence of observations. However, because individuals were not followed longitudinally according to changes in insurance type, the analysis remained cross-sectional in nature. Although the KHPS has been conducted since 2008, the second-wave KHPS was reorganized and relaunched in 2019 using a newly constructed sampling frame. To avoid heterogeneity in survey design, sample composition, and variable structure, we did not combine the first-wave and second-wave data and instead restricted the analysis to the second-wave period. The 2019–2020 waves were the most recent data available at the time of the initial analysis; during revision, we extended the analysis to perform year-specific analyses from 2020 to 2023 to examine whether the findings persisted over time.

The primary analysis focused on adults aged <65 years who had private health insurance and no chronic diseases. Individuals aged ≥65 years were excluded because private insurance enrollment, underwriting conditions, and healthcare utilization patterns may differ substantially in older adults. Individuals with chronic diseases were excluded to reduce confounding by underlying disease burden and to examine the association between insurance type and healthcare utilization in a population with relatively low baseline medical need.

Chronic diseases were identified using KHPS survey items and included hypertension, diabetes, chronic hepatitis B or C, alcoholic hepatitis, liver cirrhosis, knee joint disease, degenerative arthritis, rheumatoid arthritis, intervertebral disc disorder, other spinal diseases, stomach cancer, colon cancer, lung cancer, breast cancer, cervical cancer, thyroid cancer, angina, myocardial infarction, cerebral hemorrhage, cerebral infarction, asthma, pulmonary tuberculosis, chronic obstructive pulmonary disease, bronchiectasis, hypothyroidism, hyperthyroidism, mood disorder, and dementia.

Participants were excluded if they had missing information on private insurance coverage, private insurance type, chronic disease status, healthcare utilization outcomes, or covariates required for multivariable analysis. Among the eligible participants for the primary analysis, 78 cases, corresponding to 2.4% of the analytic population, were excluded because of missing responses in variables used for descriptive or regression analyses. Complete-case analysis was therefore used for the final multivariable models. Although the proportion of missing data was small, the exclusion of participants with missing responses may have introduced selection bias if these individuals differed systematically in socioeconomic characteristics, insurance enrollment patterns, or healthcare-seeking behavior.

A total of 3,320 participants were included in the final primary analysis. Of these, 2,686 participants had indemnity-type private insurance and 634 had fixed-benefit private insurance.

Exposure and Outcome Variables

The primary exposure variable was the type of private health insurance, categorized as fixed-benefit insurance or indemnity insurance according to the KHPS classification. Fixed-benefit insurance was defined as private insurance that provides a predetermined payment based on diagnosis, hospitalization, or treatment. Indemnity insurance was defined as private insurance that reimburses actual out-of-pocket medical expenses within the coverage limits of the insurance contract.

The primary outcomes were healthcare utilization and medical expenditures during the study period. Healthcare utilization was assessed separately for emergency department use, inpatient care use, and outpatient care use. For each category, utilization was defined as at least one recorded use of the corresponding service. Visit frequency was assessed as the number of emergency department visits, inpatient admissions, and outpatient visits. Annual medical expenditures were analyzed separately for emergency, inpatient, outpatient, and total healthcare services.

Covariates included age, sex, marital status, educational level, household income quartile, residential area, subjective health status, regular workout, and employment status. Household income was categorized into quartiles, with Q1 representing the lowest household income group and Q4 representing the highest household income group. Age groups were used for descriptive presentation, whereas age was included as a continuous covariate in the multivariable regression models to improve model stability.

Statistical Analysis

Baseline characteristics were compared between the indemnity and fixed-benefit insurance groups. Continuous variables were summarized as means with standard deviations and compared using Student’s t-test. Categorical variables were summarized as frequencies and percentages and compared using the chi-square test or Fisher’s exact test, as appropriate. Medical expenditures were analyzed using Tweedie generalized linear models with a log link because expenditure variables were right-skewed and included zero values. Multivariable logistic regression models were used to evaluate factors associated with any healthcare utilization, including inpatient care use and outpatient care use. Results were presented as odds ratios with 95% confidence intervals. Negative binomial regression models with a log link function were used to analyze visit count outcomes, including the number of inpatient admissions and outpatient visits, because these outcomes were count variables and showed overdispersion. Results were presented as incidence rate ratios with 95% confidence intervals.

The multivariable models were adjusted for age, sex, marital status, educational level, household income quartile, residential area, subjective health status, regular workout, and employment status. Household income quartile was added as a socioeconomic covariate in the revised analysis to address potential confounding by income. Detailed information on insurance premiums, benefit generosity, prior healthcare utilization, and provider accessibility was not fully available in the analytic dataset and was therefore not included in the primary models. If higher-income individuals are more likely to select indemnity plans and also use more healthcare services, omitting income-related variables may have introduced upward bias in the estimated association between indemnity insurance and healthcare utilization, although household income quartile was included as a partial adjustment.

Because this study used all eligible participants from a nationally representative survey who met the inclusion criteria, the sample size was determined by data availability rather than by an a priori sample size calculation. To address statistical power, we performed a post hoc power calculation using outpatient care use as the primary utilization outcome. Based on the observed outpatient care use rates of 82.2% in the indemnity group and 73.7% in the fixed-benefit group, with sample sizes of 2,686 and 634, respectively, the achieved power was approximately 99.8% at a two-sided alpha level of 0.05. This indicated that the final analytic sample had sufficient power to detect the observed difference in outpatient care use between the two insurance groups.

To assess the robustness of the primary findings and to address concerns regarding selection bias and generalizability, we performed an expanded-cohort sensitivity analysis. This analysis included participants who were excluded from the primary restricted cohort, including older adults and individuals with chronic diseases. Age and chronic disease status were included as additional covariates in the expanded-cohort models. This sensitivity analysis was performed to evaluate whether the association between private insurance type and healthcare utilization was consistent beyond the primary analytic population of adults aged <65 years without chronic diseases.

Because insurance choice may be endogenous, the results were interpreted as associations rather than causal effects. Individuals who anticipated greater healthcare needs or who had stronger preferences for healthcare use may have been more likely to select indemnity-type insurance. The cross-sectional design did not allow us to determine the temporal sequence between insurance enrollment and healthcare utilization.

All statistical analyses were performed using R version 4.4.1 (R Foundation for Statistical Computing, Vienna, Austria). A two-sided p-value <0.05 was considered statistically significant.

Results

Study Population

Of 14,844 survey respondents, 4,335 had missing insurance coverage data. Among the remaining 10,509 respondents, 7,583 had private health insurance. After excluding participants with chronic diseases, individuals aged ≥65 years, those with missing information on private insurance type, and those with missing analytic variables, 3,320 individuals were included in the final primary analysis.

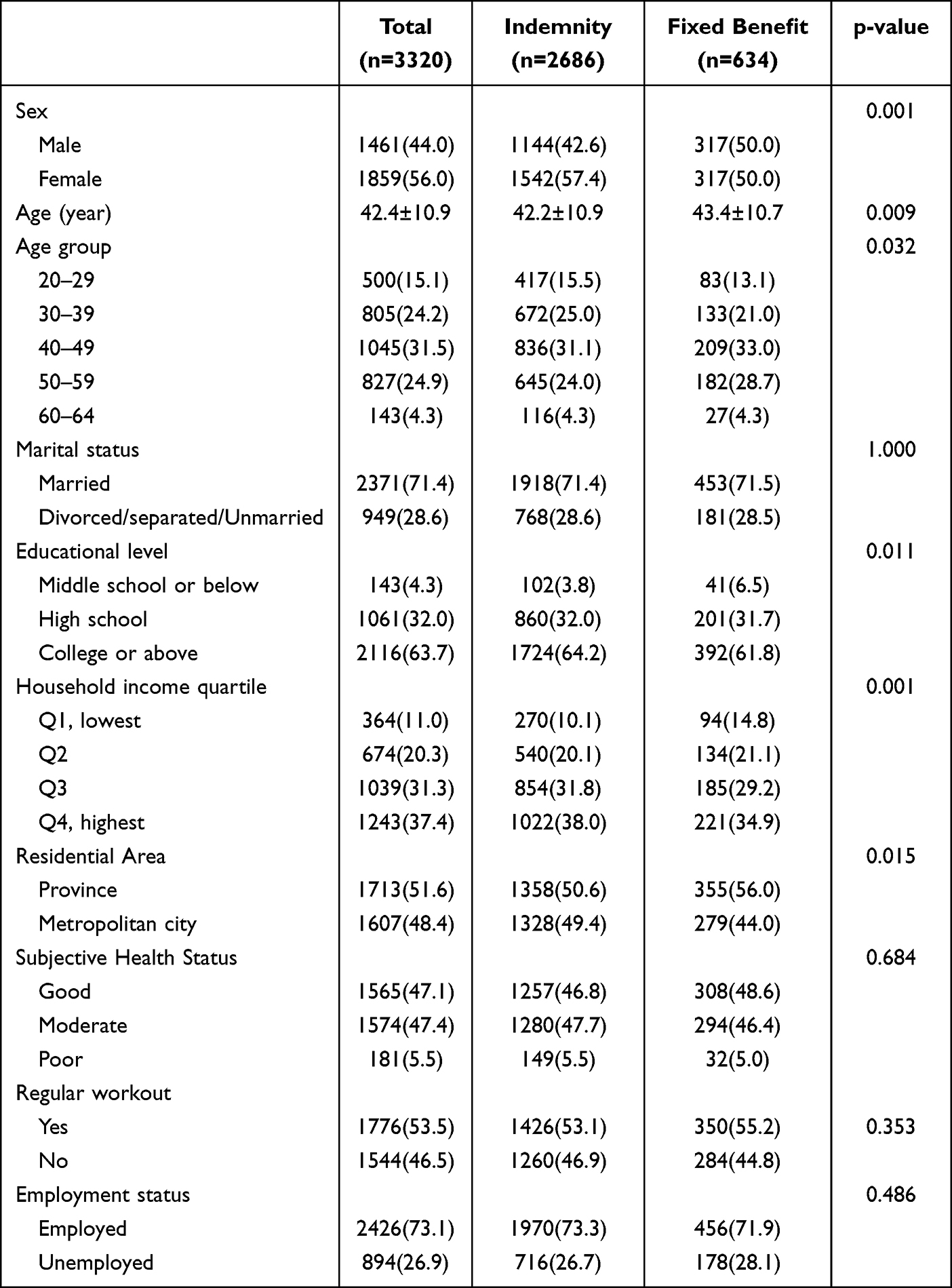

Among these participants, 2,686 individuals were enrolled in indemnity-type private insurance and 634 were enrolled in fixed-benefit private insurance (Figure 1). The indemnity group was slightly younger than the fixed-benefit group and included a higher proportion of women. Educational level, household income quartile, and residential area also differed significantly between the two groups. In contrast, marital status, subjective health status, regular workout, and employment status were not significantly different between groups (Table 1).

|

Table 1 Participant Characteristics According to Private Insurance Type |

|

Figure 1 Flow diagram of the study population. |

Healthcare Utilization and Medical Expenditures

Healthcare utilization differed primarily in outpatient care. The indemnity group had a higher proportion of outpatient care use than the fixed-benefit group (82.2% vs 73.7%). The average number of outpatient visits was also higher in the indemnity group than in the fixed-benefit group (9.14 ± 12.69 vs 7.46 ± 11.77 visits). Outpatient medical expenditures were significantly higher in the indemnity group (370.67 ± 845.73 USD) than in the fixed-benefit group (291.93 ± 712.77 USD; p=0.006). Total annual medical expenditures were also higher in the indemnity group (492.16 ± 1119.46 USD vs 392.35 ± 966.85 USD; p=0.003), largely reflecting the difference in outpatient expenditures.

In contrast, differences in emergency and inpatient expenditures were not statistically significant. Emergency department use was similar between the indemnity and fixed-benefit groups (4.4% vs 3.9%), and emergency medical expenditures did not differ significantly (3.43 ± 27.72 USD vs 3.39 ± 24.66 USD; p=0.972). Inpatient care use was numerically higher in the indemnity group than in the fixed-benefit group (8.2% vs 5.2%), but inpatient expenditures were not significantly different between groups (118.06 ± 636.17 USD vs 80.37 ± 586.77 USD; p=0.104) (Table 2).

|

Table 2 Healthcare Service Utilization and Costs by Type of Private Health Insurance |

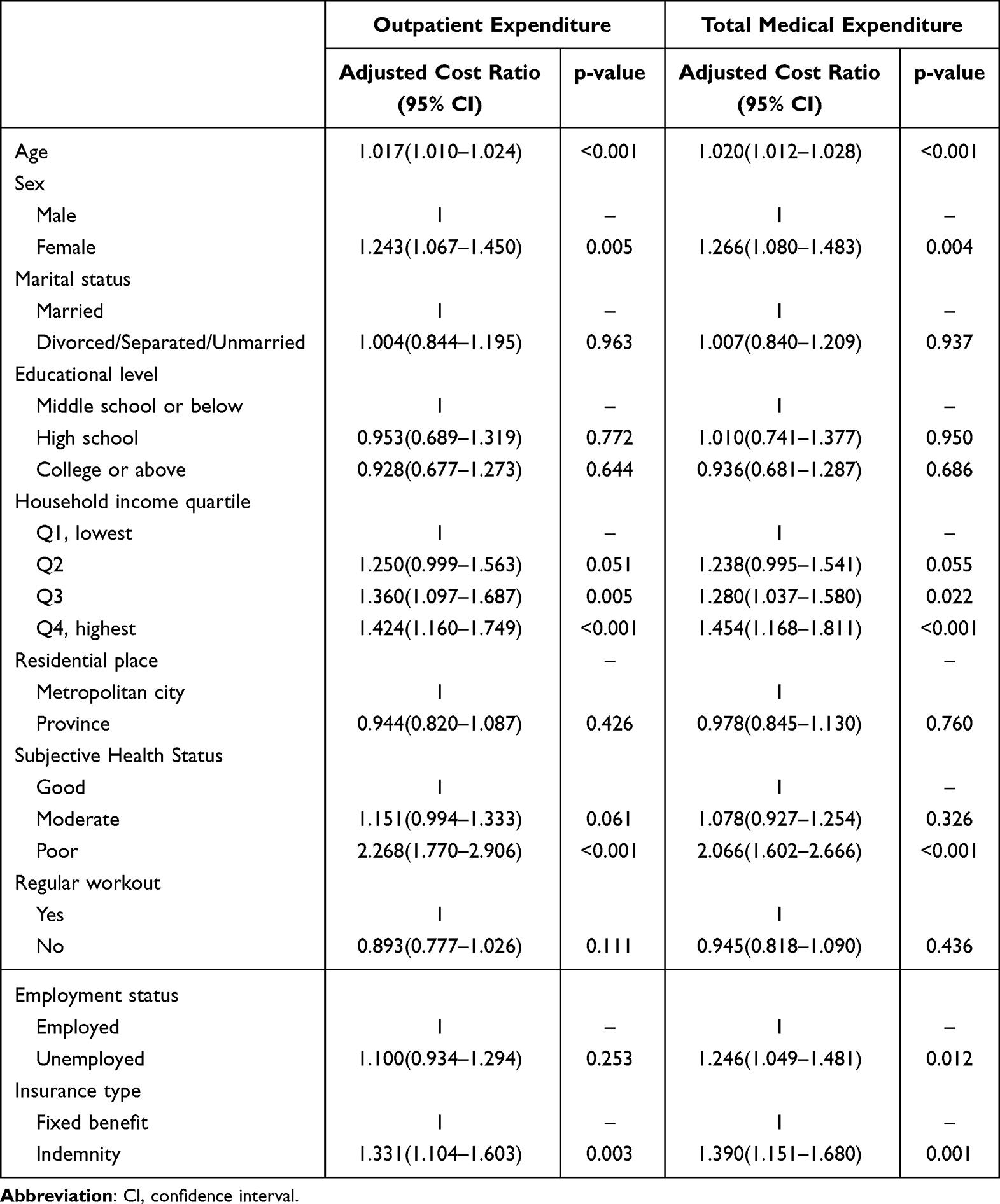

In the multivariable expenditure analysis, indemnity-type insurance was independently associated with higher outpatient medical expenditures compared with fixed-benefit insurance (adjusted cost ratio, 1.331; 95% CI, 1.104–1.603; p=0.003). Indemnity-type insurance was also associated with higher total medical expenditures (adjusted cost ratio, 1.390; 95% CI, 1.151–1.680; p=0.001) (Table 3). In additional analyses, indemnity-type insurance was not significantly associated with emergency or inpatient medical expenditures after adjustment for the same covariates.

|

Table 3 Multivariable Analysis of Outpatient and Total Medical Expenditures |

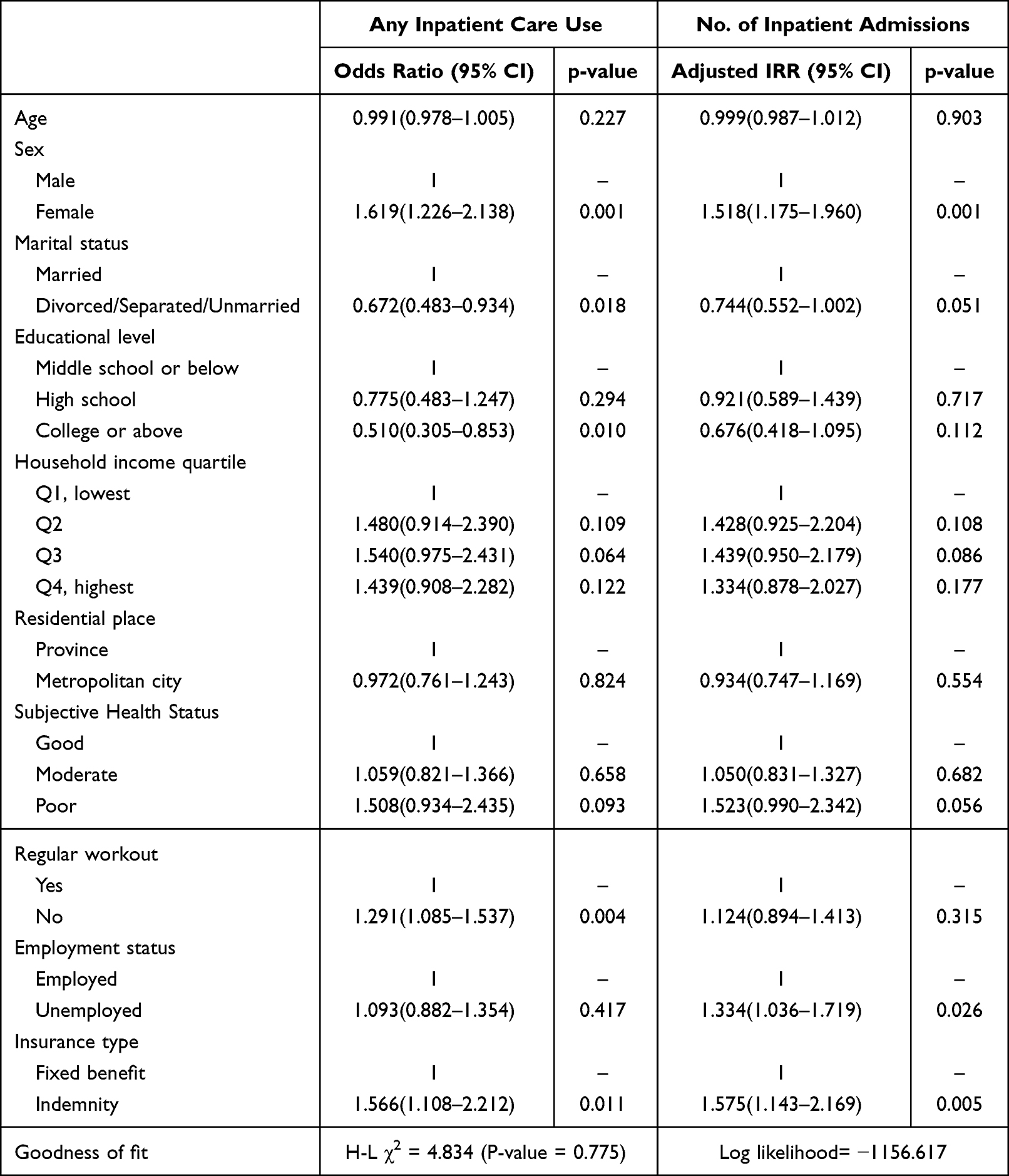

Multivariable Analysis of Inpatient Care Utilization

In the multivariable analysis, indemnity-type insurance was associated with any inpatient care use compared with fixed-benefit insurance. However, given that inpatient care use was relatively uncommon in this population (8.2% in the indemnity group), the absolute contribution of inpatient services to overall healthcare utilization was smaller than that observed for outpatient care. Indemnity-type insurance was associated with higher odds of inpatient care use (adjusted OR, 1.566; 95% CI, 1.108–2.212; p=0.011) and a higher number of inpatient admissions (adjusted IRR, 1.575; 95% CI, 1.143–2.169; p=0.005). Other factors associated with inpatient care use included sex, marital status, educational level, employment status, and regular workout status (Table 4).

|

Table 4 Multivariate Analysis of Factors for Inpatient Care Utilization |

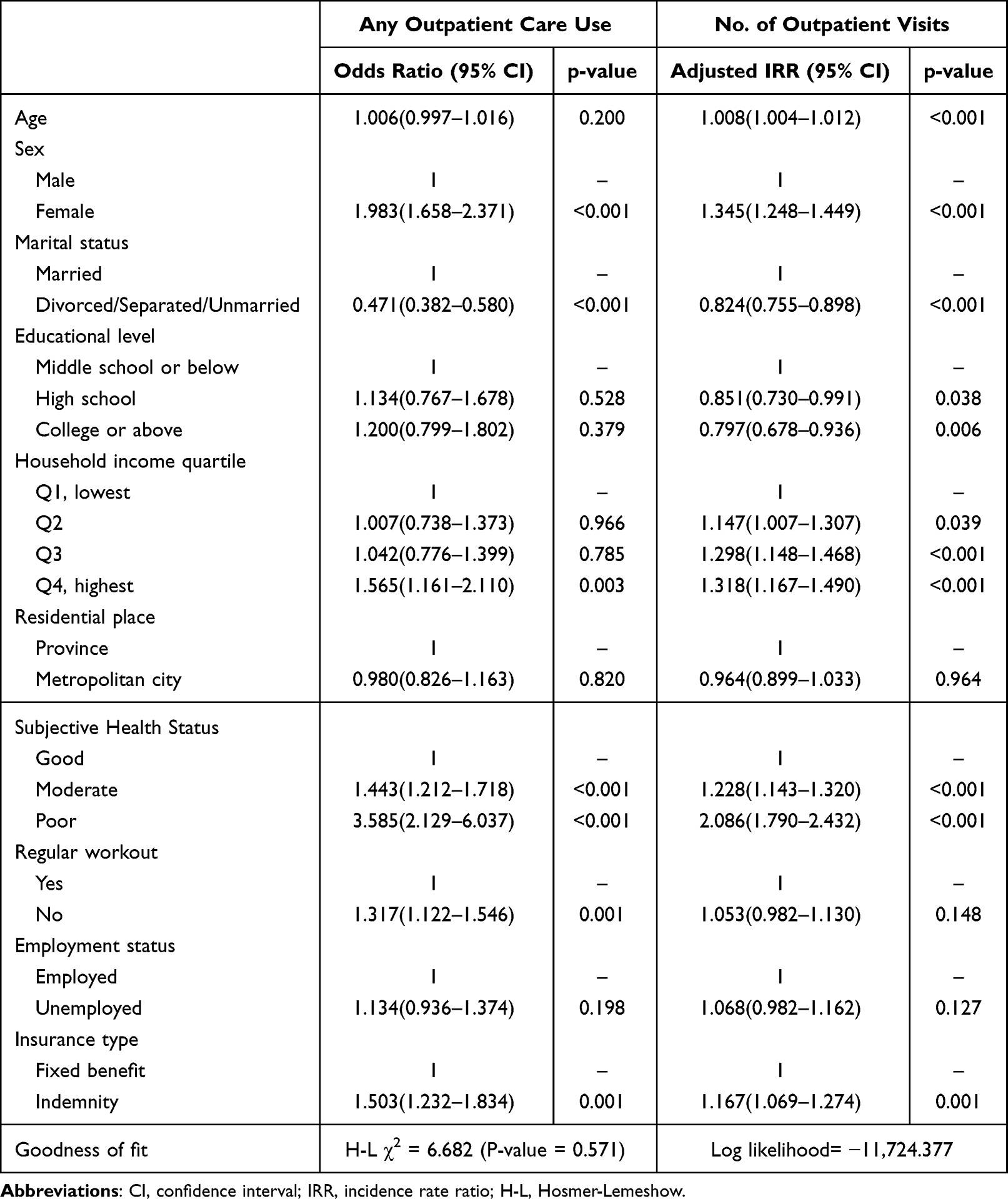

Multivariable Analysis of Outpatient Care Utilization

The strongest and most consistent associations were observed for outpatient care. In the multivariable analysis, indemnity-type insurance was associated with higher odds of outpatient care use compared with fixed-benefit insurance (adjusted OR, 1.503; 95% CI, 1.232–1.834; p=0.001). Indemnity-type insurance was also associated with a higher number of outpatient visits (adjusted IRR, 1.167; 95% CI, 1.069–1.274; p=0.001). These findings indicate that the association between insurance type and healthcare utilization was driven mainly by outpatient service use. Other variables associated with outpatient care use included age, sex, marital status, educational level, household income quartile, and subjective health status. Regular workout status was associated with outpatient care use in the logistic regression model but not in the negative binomial model (Table 5).

|

Table 5 Multivariate Analysis of Factors for Outpatient Care Utilization |

Expanded-Cohort Sensitivity Analysis

The association between indemnity-type insurance and healthcare utilization remained statistically significant in the expanded cohort. Indemnity-type insurance was associated with any inpatient care use (adjusted OR, 1.281; 95% CI, 1.088–1.506; p=0.003) and with the number of inpatient admissions (adjusted IRR, 1.310; 95% CI, 1.142–1.502; p<0.001) (Supplementary Table S1).

Similarly, indemnity-type insurance remained associated with outpatient care use in the expanded cohort. Indemnity-type insurance was associated with any outpatient care use (adjusted OR, 1.221; 95% CI, 1.018–1.466; p=0.032) and with the number of outpatient visits (adjusted IRR, 1.074; 95% CI, 1.017–1.134; p=0.011) (Supplementary Table S2). These sensitivity analyses supported the robustness of the primary findings, although the associations remained observational and should not be interpreted as causal effects.

Year-Specific Analysis from 2020 to 2023

To examine whether the main findings persisted over time, we performed additional year-specific analyses using KHPS data from 2020 to 2023. The proportion of indemnity-type insurance among eligible private insurance holders increased steadily from 80.4% in 2020 to 87.2% in 2023 (Figure 2). Across all survey years, individuals with indemnity-type insurance had higher mean outpatient visits, outpatient expenditures, and total medical expenditures than those with fixed-benefit insurance. In adjusted analyses, indemnity-type insurance was generally associated with a higher number of outpatient visits, although statistical significance varied by year (Supplementary Table S3). The expenditure analyses showed a more consistent pattern: indemnity-type insurance was significantly associated with higher outpatient expenditures in each year from 2020 to 2023. Similar associations were observed for total medical expenditures (Supplementary Table S4). These results suggest that the association between indemnity-type insurance and greater outpatient-focused medical spending was not limited to the main 2020 analytic period, but persisted through 2023.

|

Figure 2 Yearly trends in the proportion of indemnity-type private insurance and total medical expenditures from 2020 to 2023. |

Discussion

In this cross-sectional analysis using nationally representative data from Korea, indemnity-type private insurance was associated with greater healthcare utilization compared with fixed-benefit insurance.8,9,16 However, the findings were not uniform across all types of healthcare services. The most consistent differences were observed in outpatient care: individuals with indemnity-type insurance had higher outpatient care use, more outpatient visits, and higher outpatient medical expenditures. In contrast, emergency and inpatient expenditures did not differ significantly between the two groups in the primary cohort, although year-specific analyses indicated a significant association with inpatient expenditures in the later years (2021–2023; Supplementary Table S4). These findings suggest that the association between indemnity-type insurance and healthcare utilization was primarily outpatient-focused rather than reflecting a broad increase in all categories of medical care.

This outpatient-focused pattern is important for interpreting the results. Outpatient services in Korea are highly accessible, relatively inexpensive at the point of care, and generally available without strong gatekeeping restrictions. In such a setting, indemnity-type insurance may further reduce patients’ perceived cost burden and lower the marginal cost of additional visits. This mechanism is consistent with moral hazard theory and demand-side incentives in insurance economics, whereby lower cost-sharing may be associated with greater healthcare use.10,11 However, the present findings suggest a selective utilization pattern, not a uniform increase across all care settings. Therefore, the results should be interpreted as evidence of differential outpatient utilization associated with insurance design, not as evidence of broad system-wide cost escalation.

The distinction between indemnity and fixed-benefit insurance may help explain these findings. Fixed-benefit insurance provides a predetermined payment based on diagnosis, hospitalization, or treatment, and therefore does not necessarily reduce the marginal cost of each additional medical encounter. Indemnity insurance, by contrast, reimburses actual out-of-pocket expenses within the limits of the insurance contract. This reimbursement structure may make additional outpatient consultations, tests, or procedures less financially burdensome to patients. In a fee-for-service system, demand-side incentives may also interact with provider-side incentives, because providers may have greater opportunity to recommend additional services when patients face fewer direct cost barriers.16,17 These mechanisms may be particularly relevant in the Korean healthcare system, where patients have broad freedom to choose providers and access medical institutions.

Our findings are broadly consistent with international evidence from mixed public-private healthcare systems. Studies from countries with complementary or supplementary private insurance have reported that reduced cost-sharing may be associated with increased use of physician services, prescription drugs, or elective procedures.10–12 However, the magnitude and type of utilization associated with private insurance vary across institutional contexts. For example, in systems where private insurance mainly covers cost-sharing for outpatient services, increased outpatient use may be more apparent, whereas effects on inpatient or emergency care may be less consistent. The present study adds to this literature by showing that, within Korea’s universal NHI system, differences by private insurance type were most evident in outpatient utilization.

The expanded-cohort sensitivity analysis supported the robustness of the main findings. When older adults and individuals with chronic diseases were included, indemnity-type insurance remained significantly associated with inpatient and outpatient utilization after adjustment for age, chronic disease status, household income quartile, and other covariates. Nevertheless, this sensitivity analysis does not eliminate the possibility of selection bias or unmeasured confounding. Rather, it suggests that the observed association was not entirely driven by the primary restriction to adults aged <65 years without chronic diseases. Consistent with this, year-specific analyses from 2020 to 2023 showed that the association between indemnity-type insurance and higher outpatient and total medical expenditures was maintained across survey years, supporting the temporal robustness of the main finding (Supplementary Tables S3 and S4).

Several limitations should be considered when interpreting these findings. First, because this study used a cross-sectional design, the observed associations should not be interpreted as causal effects of indemnity-type insurance. Reverse causation is possible: individuals who anticipate greater healthcare needs, have stronger preferences for medical care, or are more likely to seek healthcare may be more likely to purchase indemnity-type insurance. Therefore, insurance choice may be endogenous, and self-selection into indemnity plans may have contributed to the observed associations.

Second, although the primary analysis was restricted to adults aged <65 years without chronic diseases to reduce confounding by underlying disease burden, this restriction may limit external validity. Individuals with chronic diseases and older adults may have different healthcare needs, insurance enrollment restrictions, premium burdens, and responses to insurance incentives. The expanded-cohort sensitivity analysis partially addressed this concern, but it cannot fully resolve differences in baseline risk or insurance selection patterns between groups.

Third, residual confounding may remain. In the revised analysis, household income quartile was added as a socioeconomic covariate. However, detailed information on insurance premiums, benefit generosity, prior healthcare utilization, and provider accessibility was not fully available in the analytic dataset. These factors may be associated with both insurance type and healthcare use. For example, individuals purchasing more generous indemnity plans may differ from fixed-benefit policyholders in income, health-seeking behavior, risk preferences, or access to healthcare providers. Omission of these variables may have influenced the estimated associations.

Fourth, although the study used a two-year KHPS sample and excluded duplicate individuals to maintain independence of observations, the analysis remained cross-sectional. The study could not evaluate within-person changes in healthcare utilization before and after enrollment in indemnity-type insurance, nor could it capture longer-term behavioral responses to changes in insurance coverage. Future longitudinal studies using repeated measures of insurance status, premiums, benefit design, and healthcare utilization are needed to better assess dynamic utilization responses and strengthen causal inference.

Despite these limitations, this study has several strengths. It used nationally representative survey data and directly compared two types of private health insurance rather than simply comparing insured versus uninsured individuals. The analysis also focused on a generally healthy population, which may help clarify the association between insurance design and healthcare utilization. In addition, the expanded-cohort sensitivity analysis suggested that the direction of the association was consistent beyond the primary restricted cohort.

From a policy perspective, the findings suggest that indemnity-type private insurance may be associated with selective increases in outpatient utilization within Korea’s mixed public-private healthcare system.19,20 The results do not establish broad system-wide cost escalation or direct financial risk to the NHI. However, they indicate that insurance design may influence outpatient care-seeking behavior in a highly accessible fee-for-service environment. Policy discussions should consider not only coverage expansion and financial protection, but also the ways in which reimbursement structure, cost-sharing mechanisms, and provider incentives may shape outpatient utilization.

Conclusions

Indemnity-type private health insurance was associated with higher outpatient healthcare utilization and outpatient medical expenditures compared with fixed-benefit insurance among adults aged <65 years without chronic diseases. However, no significant differences were observed in emergency or inpatient expenditures in the primary cohort, and the findings do not establish broader system-wide cost effects. These results suggest that the association between indemnity-type insurance and healthcare utilization is primarily outpatient-focused. Policymakers should consider how private insurance design, particularly reimbursement-based coverage, may influence outpatient care-seeking behavior within Korea’s highly accessible National Health Insurance system. Although the association remained consistent across survey years from 2020 to 2023, further longitudinal studies using within-person designs are needed to confirm whether these outpatient-focused differences persist over time and whether changes in private insurance design or cost-sharing policy may help moderate outpatient utilization within Korea’s NHI system.

Ethical Statement

This study was approved by the Institutional Review Boards of Kangnam Sacred Heart (IRB No. 2023-12-013). However, informed consent was waived by the institutional review board because this study utilized publicly available, fully anonymized data and did not involve primary data collection or direct human participant recruitment.

Acknowledgments

This study was supported by Jeju National University Hospital.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Lee C, Lee HJ, Park S. Comparative study on medical fees: caesarean section, cataract, and appendectomy surgeries among OECD countries. J Korean Med Assoc. 2013;56(6):523–14. doi:10.5124/jkma.2013.56.6.523

2. Kwon S. Thirty years of national health insurance in South Korea: lessons for achieving universal health care coverage. Health Policy Plan. 2009;24(1):63–71. doi:10.1093/heapol/czn037

3. National Health Insurance Service. National Health Insurance Statistical Yearbook. Wonju: National Health Insurance Service; 2024.

4. Jung HW, Kwon YD, Noh JW. How public and private health insurance coverage mitigates catastrophic health expenditures in Republic of Korea. BMC Health Serv Res. 2022;22(1):1042. doi:10.1186/s12913-022-08405-4

5. Kim E, Kwon S. The effect of catastrophic health expenditure on exit from poverty among the poor in South Korea. Int J Health Plann Manag. 2021;36(2):482–497. doi:10.1002/hpm.3097

6. OECD. Health at a Glance 2023: OECD Indicators. Paris: OECD Publishing; 2023.

7. Financial Supervisory Service. Status of Indemnity (Silson) Medical Insurance Enrollment and Benefit Payments, 2023. Seoul: Financial Supervisory Service; 2024.

8. Kang S, You CH, Kwon YD, Oh EH. Effects of supplementary private health insurance on physician visits in Korea. J Formos Med Assoc. 2009;108(12):912–920. doi:10.1016/S0929-6646(10)60003-4

9. Jeon B, Kwon S. Effect of private health insurance on health care utilization in a universal public insurance system: a case of South Korea. Health Policy. 2013;113(1–2):69–76. doi:10.1016/j.healthpol.2013.05.007

10. Ko H. Moral hazard effects of supplemental private health insurance in Korea. Soc Sci Med. 2020;265:113325. doi:10.1016/j.socscimed.2020.113325

11. Pauly MV. The economics of moral hazard: comment. Am Econ Rev. 1968;58(3):531–537.

12. Buchmueller TC, Couffinhal A, Grignon M, Perronnin M. Access to physician services: does supplemental insurance matter? Evidence from France. Health Econ. 2004;13(7):669–687. doi:10.1002/hec.879

13. Lemieux J, Chovan T, Heath K. Medigap coverage and Medicare spending: a second look. Health Aff. 2008;27(2):469–477. doi:10.1377/hlthaff.27.2.469

14. Segal L. Why it is time to review the role of private health insurance in Australia. Aust Health Rev. 2004;27(1):3–15. doi:10.1071/AH042710003

15. Kwon KN, Chung W. Effects of private health insurance on medical expenditure and health service utilization in South Korea: a quantile regression analysis. BMC Health Serv Res. 2023;23(1):1219. doi:10.1186/s12913-023-10251-x

16. Kim JH, Kim JH, Yoo KB, Park EC. Association between chronic disease and catastrophic health expenditure in Korea. BMC Health Serv Res. 2015;15:26. doi:10.1186/s12913-014-0675-1

17. Lee M, Yoon K, Choi M. Private health insurance and catastrophic health expenditures of households with cancer patients in South Korea. Eur J Cancer Care. 2018;27(5):e12867. doi:10.1111/ecc.12867

18. Korea Health Panel Survey. Korea Health Panel Survey official website. Available from: https://www.khp.re.kr:444/eng/main.do.

19. Korea Insurance Research Institute. Indemnity health insurance loss ratio statistics. Available from: https://www.kiri.or.kr.

20. Shin DW. How to reach agreement on appropriate reimbursement level through the insurer-run hospitals. Public Health Aff. 2019;3(1):155–164. doi:10.29339/pha.3.1.155

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.