Back to Journals » Journal of Healthcare Leadership » Volume 18

Revisiting the Eight Basic Payment Methods in Health Care: A Contemporary Framework for Value-Based Policy and Practice in the United States

Authors Beauvais B ![]() , Ramamonjiarivelo Z, Mileski M

, Ramamonjiarivelo Z, Mileski M ![]() , Shapley R, Pradhan R

, Shapley R, Pradhan R ![]() , Priore R

, Priore R ![]()

Received 26 February 2026

Accepted for publication 14 April 2026

Published 27 May 2026 Volume 2026:18 605413

DOI https://doi.org/10.2147/JHL.S605413

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Pavani Rangachari

Brad Beauvais,1 Zo Ramamonjiarivelo,1 Michael Mileski,1 Roland Shapley,1 Rohit Pradhan,1 Richard Priore2

1School of Health Administration, Texas State University, San Marcos, TX, USA; 2Department of Social, Behavioral, and Population Sciences, Tulane University, New Orleans, LA, USA

Correspondence: Brad Beauvais, Email [email protected]

Background: Payment reform is a central policy lever for influencing cost, quality, and access in the United States health care system. Despite decades of reform activity, confusion persists regarding how modern reimbursement models differ, overlap, and redistribute financial risk, particularly as hybrid arrangements proliferate across payers. This update addresses structural payment layering, AI-enabled coding intensity, and the dominance of Medicare Advantage, developments not present at the time of Quinn’s original framework.

Objective: To update Quinn’s Eight Basic Payment Methods to reflect the 2026 reimbursement environment, using the Health Care Spending Identity to characterize risk allocation across payment methods.

Methods: Conceptual and policy-based analysis of current Medicare programs, Medicaid, and commercial reimbursement regulations, supplemented by targeted review of recent Centers for Medicare & Medicaid Services rulemaking documents and related evaluation studies.

Results: Quinn’s framework remains the stable foundation of healthcare reimbursement. Contemporary reforms—including accountable care organizations, bundled payment initiatives, Medicare Advantage risk contracting, and population-based payment models—represent hybrid combinations of these methods rather than fundamentally new payment structures. Rather than introducing new structural forms of payment, recent policy experimentation has primarily altered the degree and direction of financial risk borne by providers, payers, and patients within the established units of Quinn’s framework.

Conclusion: Policymakers and leaders should recognize that contemporary reforms are hybrid combinations of established units rather than novel inventions. Recognizing this helps clarify both the conceptual boundaries and operational mechanics of value-based payment models. Greater conceptual clarity regarding units of payment and units of accountability is necessary to design administratively feasible, transparent value-based policies that can be implemented and sustained over time.

Keywords: health care reimbursement, payment reform, value-based care, medicare policy, financial risk, risk adjustment

Introduction

Payment systems exert a powerful influence on health care delivery by shaping organizational behavior, resource allocation, and clinical priorities. Although professional norms and patient-centered values may guide individual clinical decision-making, reimbursement methods define the financial environment within which health care organizations operate, influencing staffing models, service mix, care coordination infrastructure, and investment in quality improvement.1–4

Over the past several decades, the United States has pursued repeated waves of payment reform intended to constrain cost growth, improve quality, and enhance accountability. These efforts accelerated with passage of the Patient Protection and Affordable Care Act and were further institutionalized under the Medicare Access and CHIP Reauthorization Act (MACRA).5,6 Despite sustained reform activity, health care spending remains high, quality improvement has been uneven, and administrative complexity has increased.2,7,8

A persistent challenge in payment reform discourse is the tendency to frame new initiatives as fundamentally novel, obscuring the reality that most reforms are constructed from longstanding reimbursement mechanisms.9 This framing complicates policy design, impedes stakeholder understanding, and contributes to unrealistic expectations regarding the impact of payment reform. Revisiting foundational payment concepts is therefore essential for evaluating contemporary policy initiatives.

This article builds directly on the eight basic payment methods framework originally articulated by Quinn in 2015 and updates it to reflect the current reimbursement environment, clarifying how hybrid overlays alter incentives without changing the underlying units of payment and where financial risk is ultimately reconciled.1 The goal of this study is to support a common conceptual language for characterizing payment models, enabling more transparent policy design, and providing stakeholders with a clearer basis for comparing and evaluating contemporary reforms over time.

This analysis is primarily grounded in Medicare policy given its role as the dominant driver of payment reform innovation. However, similar hybrid payment dynamics are increasingly observed in Medicaid managed care programs and commercial insurance markets, albeit with variation in adoption timing, contractual structure, and regulatory oversight. Commercial employer-sponsored insurance often implements value-based arrangements through negotiated contracts that lag Medicare in standardization, while Medicaid programs exhibit state-level heterogeneity in model design and risk-sharing mechanisms.

Relationship to the Original Eight Payment Methods Framework

Quinn’s 2015 article introduced the eight basic payment methods as a unifying taxonomy for understanding how health care providers are paid and how financial risk is distributed between payers and providers.1 Rather than categorizing payment systems by program name or policy branding, Quinn emphasized that payment models should be understood by their unit of payment, such as per service, per episode, or per beneficiary. This conceptual shift provided clarity at a time when early value-based purchasing initiatives and episode-based demonstrations were often described as entirely new payment paradigms.

Quinn further argued that most payment reforms are hybrid arrangements, constructed from combinations of existing payment units rather than fundamentally new reimbursement structures.1 Subsequent scholarship has reinforced this observation, noting that performance measurement, reconciliation, and risk adjustment mechanisms are typically layered onto existing payment flows rather than replacing them.9,10

The present analysis extends Quinn’s framework in three important ways. First, it situates the eight payment methods within a reimbursement environment characterized by Medicare Advantage enrollment now exceeding 50% of eligible beneficiaries, mature accountable care organizations, and expanded episode-based payment programs, fundamentally altering who bears population-level risk.11–13 Second, it explicitly maps contemporary federal and commercial payment initiatives to combinations of the eight methods, clarifying how financial risk is redistributed without altering underlying payment units. Third, it examines organizational and behavioral responses that have emerged as providers increasingly operate under overlapping and sometimes competing incentive structures.

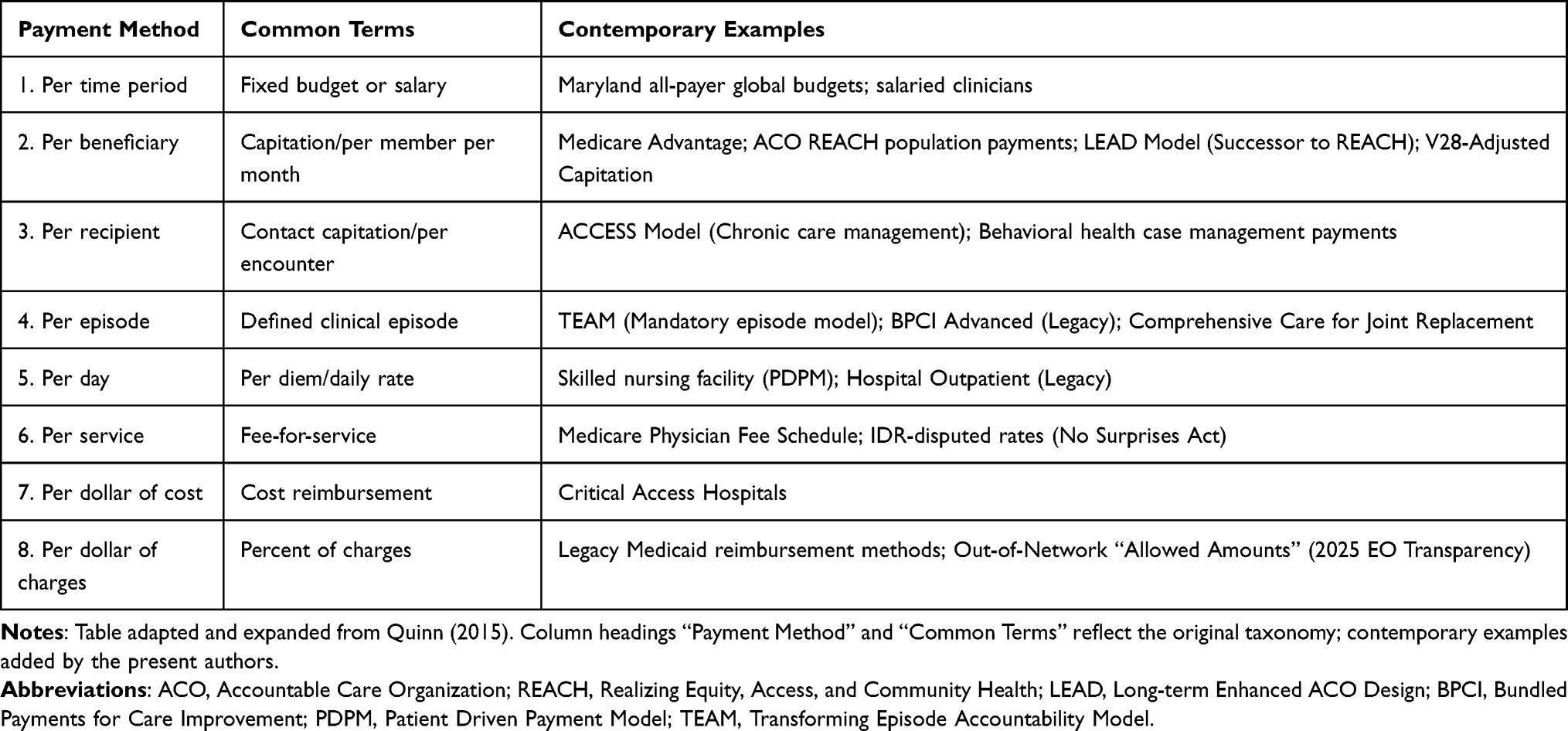

The Eight Basic Payment Methods in Health Care

The eight methods form a continuum from substantial provider financial risk (Method 1) to low provider financial risk (Method 8). As of 2026, Method 4 (per episode) continues to mark the conceptual line between epidemiologic and performance risk.1

- Payment per time period (budget or salary)

- Payment per beneficiary (capitation)

- Payment per recipient (contact capitation)

- Payment per episode (case rates or bundled payments)

- Payment per day (per diem)

- Payment per service (fee-for-service)

- Payment per dollar of cost (cost reimbursement)

- Payment per dollar of charges (percentage of charges)

Together, these eight methods span the continuum from highly prospective, population-oriented payment to highly retrospective, service-level reimbursement. Recognizing where a specific contract sits on this continuum is a prerequisite for understanding its operational implications. No payment method is neutral with respect to cost, quality, access, or efficiency. Each creates distinct incentives related to utilization, service intensity, care coordination, and cost control.1 Importantly, modern reimbursement arrangements routinely combine multiple payment methods within a single program, reinforcing Quinn’s original observation that payment reform is evolutionary rather than revolutionary.10

Table 1 summarizes the eight basic payment methods originally described by Quinn and presents them as foundational units from which contemporary reimbursement models are constructed.

|

Table 1 Eight Basic Payment Methods and Contemporary Applications |

The Health Care Spending Identity and Financial Risk

Central to this taxonomy is the Health Care Spending Identity, which provides a mathematical foundation for understanding which cost drivers a specific payment method targets:

Here ‘Population’ represents the covered lives, ‘Recipients/Population’ captures epidemiologic incidence, ‘Services/Recipients’ reflects treatment intensity, ‘Cost/Service’ captures input prices and productivity, and ‘Markup’ represents administrative load and margin.

Each of the eight payment methods corresponds to one or more risk factors within this identity. Methods 1 (per time period) and 2 (per beneficiary) target the entire population and the proportion of recipients, addressing epidemiologic risk (the risk of who gets sick). In contrast, Methods 4 through 8 focus on the cost per service and markup, placing treatment risk and the majority of financial responsibility on the payer.

This framework clarifies that risk is not a single, unified concept but is distributed across different components depending on the unit of payment. Methods 1 and 2 primarily assign risk to the Population and Recipients/Population terms, while Methods 4 through 8 concentrate risk onto Services/Recipients, Cost/Service, and Markup components, providing a practical lens for understanding how contracts redistribute responsibility for spending growth.

Evolution of Payment Reform Since 2015

Since the mid-2010s, payment reform has increasingly emphasized value-based purchasing, population accountability, and downside financial risk.2,7 However, these reforms have not replaced foundational payment units. Instead, performance measurement, reconciliation, and risk adjustment mechanisms have been progressively layered onto existing reimbursement structures.9

The policy landscape has also shifted toward mandatory participation in alternative payment models (APMs). The announced transition from ACO REACH to the LEAD (Long-term Enhanced ACO Design) Model reflects a policy shift toward more structured population-based accountability, with clearer expectations for risk-bearing and performance reporting. Simultaneously, the introduction of the TEAM (Transforming Episode Accountability Model) has made bundled payments mandatory for specific clinical episodes in many regions, further normalizing episode-based accountability as a core feature of Medicare payment.

MACRA institutionalized performance-based payment through the Merit-based Incentive Payment System (MIPS), which functions largely as an overlay on fee-for-service reimbursement rather than a replacement for it, illustrating how policy reforms often modify incentives while leaving payment units unchanged.6,14

Accountable care organizations have matured through multiple programmatic iterations, including the Medicare Shared Saving Program, culminating in models such as ACO REACH that incorporate population-based payments, prospective risk adjustment, and explicit equity benchmarks.11,12 Episode-based payment has persisted through voluntary and mandatory demonstrations, including Bundled Payments for Care Improvement Advanced and joint replacement bundles.15–17

Medicare Advantage has emerged as the dominant form of Medicare coverage, enrolling a majority of Medicare beneficiaries nationwide.13,18 Provider payment within Medicare Advantage is privately negotiated and frequently combines capitation, quality bonuses, and service-based reimbursement, reinforcing the hybrid nature of contemporary payment systems.13,19 As of early 2026, the transition to the V28 Risk Adjustment Model is 100% complete, necessitating a significant recalibration of benchmarks for ACOs and Medicare Advantage plans.

However, participation in advanced alternative payment models has grown more slowly than originally anticipated, reflecting provider concerns regarding financial risk exposure, administrative burden, and measure validity.2,14 As a result, the dominant trajectory of reform has been to layer performance-based incentives and risk-sharing arrangements onto existing units of payment, rather than to replace those units with fundamentally new payment structures.

Mapping Contemporary Payment Models to the Eight Basic Payment Methods

Modern payment reforms are most clearly understood as structured recombinations of Quinn’s eight foundational payment methods rather than as fundamentally new reimbursement architectures.1,9 As illustrated by recent Medicare ACO initiatives, and Medicare Advantage contracting, contemporary reforms combine these units in different proportion rather than introducing entirely novel payment mechanisms. Therefore, even though contemporary initiatives are frequently described as “value-based”, “population-based”, or “advanced alternative payment models”, these descriptors often obscure the fact that the underlying transactional mechanics of payment continue to rely on one or more of the eight basic methods.9,10

A central analytic distinction—often underemphasized in policy discourse—is the difference between the unit of payment and the unit of accountability. The unit of payment determines how claims are processed and revenue is generated (eg, per service, per episode, per beneficiary). The unit of accountability determines where financial risk ultimately resides within the Health Care Spending Identity. Many contemporary reforms shift accountability for spending, utilization, or population health outcomes while retaining existing claims-based payment infrastructure.4,11–16 As a result, the apparent novelty of reform frequently reflects changes in reconciliation mechanics, benchmark construction, or risk adjustment rather than the creation of new payment units.

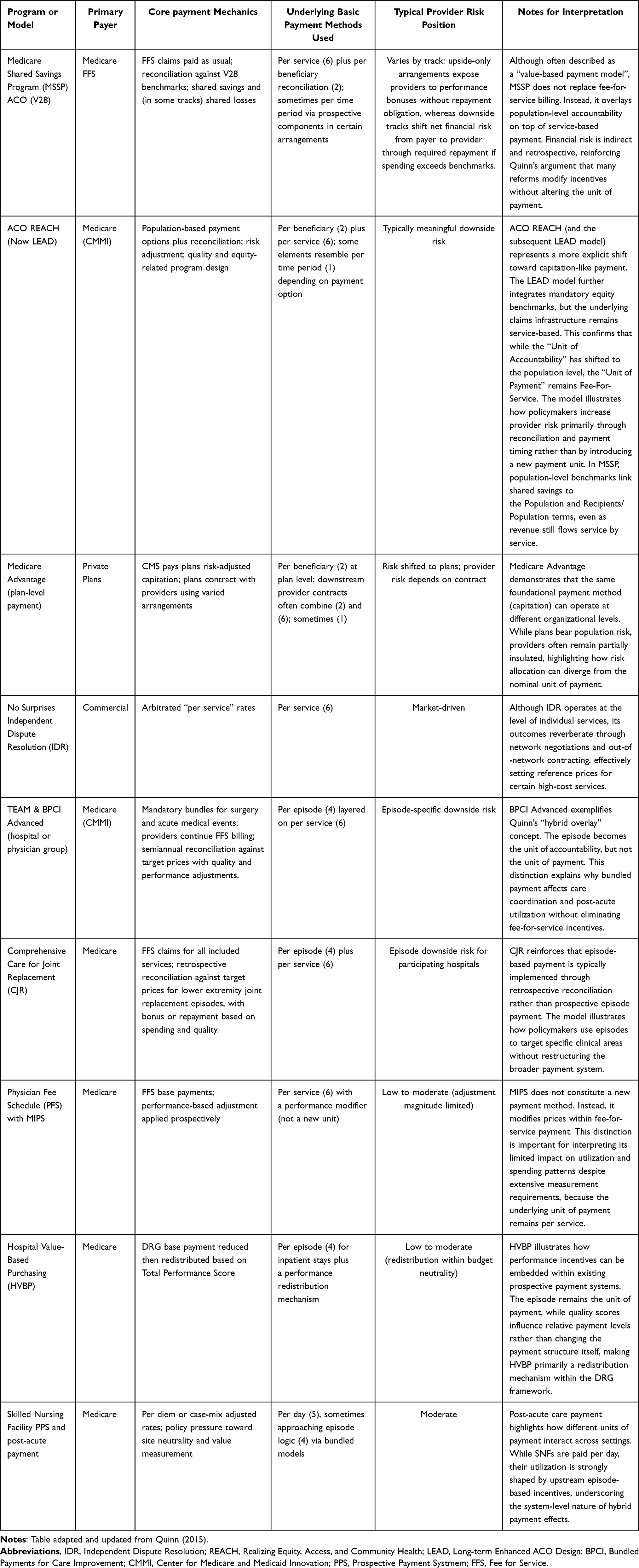

Table 2 maps prominent contemporary payment programs—including the Medicare Shared Savings Program (MSSP), ACO REACH and its successor LEAD, Medicare Advantage, bundled payment initiatives such as BPCI Advanced and TEAM, performance adjustment systems such as MIPS and Hospital Value-Based Purchasing, Independent Dispute Resolution (IDR) under the No Surprises Act, and post-acute prospective payment systems—to Quinn’s eight basic payment methods.11–19 The table identifies (1) the primary payer, (2) core payment mechanics, (3) the underlying basic payment methods in operation, (4) the typical provider risk position, and (5) interpretive notes clarifying whether the model alters the unit of payment, the unit of accountability, or both.

|

Table 2 Mapping Contemporary Payment Programs to the Eight Basic Payment Methods |

Several patterns emerge from this mapping. First, many accountable care organization models retain fee-for-service (Method 6) as the unit of payment while introducing per-beneficiary (Method 2) accountability through benchmark reconciliation and shared savings or losses.4,11,12,16 This structure extends provider exposure to Population and Recipients/Population terms within the Spending Identity, even though revenue continues to flow service by service. Downside risk tracks explicitly shift net financial risk from payer to provider when aggregate spending exceeds benchmark levels.

Second, bundled payment models such as BPCI Advanced, CJR, and TEAM use per episode (Method 4) as the unit of accountability while continuing to rely on per-service claims processing (Method 6).17–19 Providers therefore assume episode-specific treatment and utilization risk—particularly affecting Services/Recipients and Cost/Service components of the Spending Identity—without eliminating fee-for-service billing mechanics.

Third, Medicare Advantage demonstrates vertical layering of payment methods. At the federal-plan interface, CMS pays risk-adjusted capitation (Method 2).13,15 At the plan-provider interface, contracts frequently combine capitation, salary, bundled payments, and fee-for-service arrangements.13,19 This multi-level structure illustrates how population risk may be transferred to plans while provider-level exposure varies according to negotiated contract design.

Fourth, performance-based systems such as MIPS and Hospital Value-Based Purchasing modify prices within existing units rather than creating new units.7,10 These programs function as redistribution or adjustment mechanisms layered onto per-service or per-episode payment, which helps explain their modest but measurable impact on utilization and spending.7,8

Finally, IDR under the No Surprises Act operates at the per-service level (Method 6), yet arbitrated rates influence broader contracting dynamics and effective Cost/Service pricing.20 Post-acute prospective payment systems such as skilled nursing facility per diem reimbursement (Method 5) interact with upstream bundled or accountable care incentives, illustrating cross-setting hybridization.

By explicitly mapping contemporary programs to the eight foundational payment methods, Table 2 clarifies that most reforms modify where risk is reconciled rather than how revenue is transacted.1,9,14 This distinction is analytically important. It explains why administrative complexity has increased—multiple units of accountability now operate simultaneously within the same organizations—while the fundamental taxonomy of payment remains unchanged.

Viewed through the lens of the Health Care Spending Identity, contemporary payment reform primarily redistributes risk across epidemiologic, utilization, and price variables rather than introducing new economic primitives. The eight-method framework therefore continues to provide a parsimonious and durable structure for interpreting the evolution of U.S. health care reimbursement.

Financial Risk, Incentives, and Behavioral Responses

As payment reforms shift financial risk toward providers, organizations have responded by investing in care management infrastructure, data analytics, utilization controls, and population health capabilities, while simultaneously consolidating to gain contracting leverage and spread fixed costs.2,9 While these investments may improve efficiency and coordination, they also introduce incentives for risk selection, coding intensity, and organizational consolidation.18,19,21 Consequently, these shifts may increase market concentration, enhance pricing leverage, and widen disparities between organizations with advanced risk-management infrastructure and those without such capacity, raising concerns about long-term affordability and equity.

Risk adjustment systems are intended to mitigate selection bias but frequently increase administrative burden and create opportunities for gaming.19,22 Provider consolidation has accelerated as organizations seek scale to manage financial risk and negotiate favorable contracts, raising concerns regarding competition, affordability, and access to care.21,23 Because risk adjustment primarily operates on the Population and Recipients/Population components of the entity, even small documentation changes can shift substantial revenue.

Policy and Practice Implications

For policymakers, clarity regarding units of payment remains essential for designing reforms that align incentives with desired outcomes.1 Layering multiple payment methods without acknowledging their interactions increases complexity, obscures accountability, and complicates performance evaluation.2,7 Contemporary reform efforts increasingly rely on overlays—performance adjustment, reconciliation, risk scoring, and regulatory mandates—that modify financial incentives without altering foundational payment units. As a result, policymakers must distinguish between changes in the unit of payment and changes in the mechanisms used to adjust or redistribute payment.

Recent developments illustrate how operational and technological shifts can influence financial performance even when the underlying payment method remains unchanged. As financial risk has shifted toward providers, organizations have deployed advanced analytics and documentation systems to manage exposure. By 2026, generative AI-enabled chart preparation and clinical documentation support tools have contributed to measurable increases in coding intensity by more systematically identifying and documenting comorbidities and social risk factors that were previously underreported. While improved documentation may enhance clinical accuracy and risk adjustment precision, it also influences benchmark calculations in population-based and episode-based payment models. In response to observed increases in risk scores, CMS has finalized a 2% Coding Intensity Factor for certain high-needs and population-based models to stabilize spending benchmarks and mitigate technology-driven inflation in risk-adjusted payments. Ongoing policy debate centers on how to distinguish appropriate documentation improvement from opportunistic upcoding in environments increasingly shaped by algorithmic support tools. These developments demonstrate that financial outcomes in hybrid payment systems are shaped not only by formal payment design, but also by documentation practices and technology-enabled revenue cycle strategies.

Similarly, implementation of the No Surprises Act and expanded use of Independent Dispute Resolution have altered pricing dynamics in out-of-network settings. In some cases, payment determinations exceed the qualifying payment amount, introducing additional financial variability and contributing to a substantial administrative backlog of disputed claims for both payers and providers. Although IDR does not change the underlying unit of payment, it affects realized reimbursement levels and introduces additional uncertainty into contractual relationships. This reinforces the broader argument that payment reform now operates through administrative adjudication processes and regulatory overlays layered onto existing payment structures.

Method 8 (payment per dollar of charges) has also been increasingly constrained by recent federal transparency requirements. The February 2025 Executive Order on price transparency mandates disclosure of negotiated allowed amounts in addition to gross charges, reducing the informational asymmetry historically associated with chargemaster-based pricing. By requiring publication of payer-specific contracted rates, policymakers have weakened the strategic relevance of charge-based reimbursement by enabling benchmarking of contracted prices against posted charges. Although charge-based payment mechanisms persist in certain legacy arrangements, their policy and operational utility continues to diminish as negotiated rate transparency increases comparability, oversight, and scrutiny.24–27

For healthcare organizations and clinicians, understanding foundational payment mechanisms remains critical for strategic participation in value-based arrangements.1,3 As hybrid overlays multiply, leaders must differentiate between the unit of payment, the unit of accountability, and the operational levers that influence financial performance. Investments in care coordination, data analytics, documentation infrastructure, and compliance functions increasingly determine organizational success under risk-bearing contracts. Multidisciplinary care teams play an essential role in navigating these complex incentive environments while preserving patient-centered care and clinical integrity.

Limitations of the Framework

While the eight-method taxonomy captures the essential structure of payment systems, it does not fully account for nonpayment influences such as regulatory mandates, professional norms, or market power. Many of the examples in this analysis are drawn from Medicare demonstrations and models, which may diffuse only partially or slowly into Medicaid and commercial markets. The framework also assumes rational organizational response to financial incentives; however, behavioral economics and organizational culture factors may mediate or dampen predicted responses, suggesting that incentive-based analyses should be complemented by qualitative and contextual perspectives.

Conclusion

Quinn’s original framework remains a durable and comprehensive tool for understanding health care reimbursement.1 What has changed over the past decade is not the foundational taxonomy of provider payment, but the scale, layering, and interaction of hybrid accountability mechanisms operating simultaneously within health care organizations. Accountable care organizations, mandatory episode models, Medicare Advantage enrollment exceeding 50% of eligible beneficiaries, performance-based redistribution systems, and increasingly sophisticated risk adjustment have intensified provider exposure to financial risk while leaving the underlying units of payment largely intact.

Contemporary reform has therefore been characterized less by structural replacement than by cumulative overlay. Reconciliation mechanics, benchmark recalibration, coding intensity controls, equity adjustments, and performance redistribution systems have been layered onto per-service, per-episode, and per-beneficiary payment units. Through the lens of the Health Care Spending Identity, these reforms redistribute risk across Population, Recipients/Population, Services/Recipients, and Cost/Service variables without introducing new economic primitives. The unit of payment often remains unchanged, even as the unit of accountability expands.

Whether this cumulative reform trajectory will plateau remains uncertain. As hybrid overlays multiply, administrative burden, reconciliation complexity, reporting fragmentation, and compliance costs increase. At some threshold, marginal layering may generate diminishing returns, producing reform fatigue and limited incremental improvement in cost or quality performance. Future reform may therefore shift toward simplification, consolidation of models, or harmonization of benchmarks rather than continued proliferation of structurally similar programs.

Price transparency initiatives highlight this tension. Although policymakers seek clearer disclosure of negotiated “allowed amounts”, heterogeneous payment arrangements—combining per-service claims, retrospective reconciliation, quality redistribution, and population-based accountability—obscure the true transactional price of care. The multiplicity of payment overlays may inadvertently complicate the transparency objectives reform intends to advance.

Revisiting Quinn’s framework in this contemporary environment clarifies that current challenges stem less from conceptual inadequacy and more from cumulative interaction effects among overlapping incentives layered onto unchanged payment units. By distinguishing clearly between unit of payment and unit of accountability and by situating reforms within the Spending Identity, policymakers and health care leaders can better evaluate incentive alignment, anticipate behavioral responses, and design reimbursement systems that balance accountability with administrative feasibility and long-term sustainability.

Acknowledgments

Artificial intelligence assistance disclosure: The authors used ChatGPT (OpenAI, GPT-5 architecture) for limited editorial support during manuscript preparation, including refinement of language clarity, organization of sections, and stylistic improvement. The AI tool was not used to generate original conceptual arguments, conduct analysis, or determine conclusions. All substantive intellectual content, policy analysis, framework development, and final manuscript revisions were performed solely by the authors, who take full responsibility for the content of the manuscript.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Quinn K. The 8 basic payment methods in health care. Ann Internal Med. 2015;163(4):300–10. doi:10.7326/M14-2784

2. Berwick DM, Nolan TW, Whittington J. The triple aim: care, health, and cost. Health Affairs. 2008;27(3):759–769. doi:10.1377/hlthaff.27.3.759

3. Miller HD. From volume to value: better ways to pay for health care. Health Affairs. 2009;28(5):1418–1428. doi:10.1377/hlthaff.28.5.1418

4. McWilliams JM, Hatfield LA, Chernew ME, Landon BE, Schwartz AL. Early performance of accountable care organizations in medicare. N Engl J Med. 2016;374(24):2357–2366. doi:10.1056/NEJMsa1600142

5. Patient Protection and Affordable Care Act, Pub L No. 111-148 (2010). Available from: https://www.congress.gov/111/plaws/publ148/PLAW-111publ148.pdf.

6. Medicare Access and CHIP Reauthorization Act of 2015, Pub L No. 114-10 (2015). Available from https://www.congress.gov/114/plaws/publ10/PLAW-114publ10.pdf.

7. Ryan AM, Krinsky S, Maurer KA, Dimick JB. Changes in hospital quality associated with hospital value-based purchasing. N Engl J Med. 2017;376(24):2358–2366. doi:10.1056/NEJMsa1613412

8. Figueroa JF, Tsugawa Y, Zheng J, Orav EJ, Jha AK. Association between the value-based purchasing pay for performance program and patient mortality in US hospitals: observational study. BMJ. 2016;353:i2214. doi:10.1136/bmj.i2214

9. Damberg CL, Sorbero ME, Lovejoy SL, Martsolf GR, Raaen L. Measuring success in health care value-based purchasing programs. RAND Health Quarterly. 2014;4(3):1–19.

10. Centers for Medicare & Medicaid Services. Quality payment program: MIPS and advanced alternative payment models. Available from: https://qpp.cms.gov.

11. Centers for Medicare & Medicaid Services. Accountable care organization REACH model overview. Available from: https://innovation.cms.gov/innovation-models/aco-reach.

12. Centers for Medicare & Medicaid Services. ACO REACH model financial operating guide. Available from: https://innovation.cms.gov/media/document/aco-reach-financial-operating-guide.

13. Medicare Payment Advisory Commission. Report to the congress: medicare payment policy. Washington, DC; 2025. Available from: https://www.medpac.gov/document/march-2025-report-to-the-congress-medicare-payment-policy.

14. Medicare Payment Advisory Commission. Medicare advantage coding intensity and risk adjustment. Washington, DC; 2024. Available from: https://www.medpac.gov/document/march-2024-report-to-the-congress-medicare-payment-policy.

15. Medicare Payment Advisory Commission. Status report on the medicare advantage program. Washington, DC; 2026. Available from: https://www.medpac.gov/document/january-2026-medicare-advantage-status-report.

16. Congressional Budget Office. Medicare accountable care organizations. Washington, DC; 2024. Available from: https://www.cbo.gov/publication/aco-medicare-2024.

17. Centers for Medicare & Medicaid Services. Bundled payments for care improvement advanced model overview. Available from: https://innovation.cms.gov/innovation-models/bpci-advanced.

18. Shashikumar SA, Gulseren B, Berlin NL, et al. Association of hospital participation in bundled payments for care improvement advanced with medicare spending and hospital incentive payments. JAMA. 2022;328(16):1456–1465. doi:10.1001/jama.2022.18529

19. Liao JM, Huang Q, Wang E, et al. Performance of physician groups and hospitals participating in bundled payments for care improvement. JAMA Health Forum. 2022;3(6):e221245. doi:10.1001/jamahealthforum.2022.1245

20. Centers for Medicare & Medicaid Services. No Surprises act: overview of federal surprise billing protections. Available from: https://www.cms.gov/nosurprises.

21. Wadhera RK, Yeh RW, Maddox KEJ. The hospital readmissions reduction program — time for a reboot. N Engl J Med. 2019;380(24):2289–2291. doi:10.1056/NEJMp1901225

22. Centers for Medicare & Medicaid Services. Medicare advantage enrollment dashboard. Available from: https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/mcradvpartdenroldata.

23. McWilliams JM. Cost containment and the tale of care coordination. N Engl J Med. 2016;375(23):2218–2220. doi:10.1056/NEJMp1610821

24. Whaley C, Schneider Chafen J, Pinkard S, et al. Association between availability of health service prices and payments for these services. JAMA. 2014;312(16):1670–1676. doi:10.1001/jama.2014.13373

25. Jiang J, Makary MA, Bai G. Comparison of US hospital cash prices and commercial negotiated prices for 70 services. JAMA Network Open. 2021;4(12):e2140526. doi:10.1001/jamanetworkopen.2021.40526

26. Kong E, Ji Y. Provision of hospital price information after increases in financial penalties for failure to comply with a US federal hospital price transparency rule. JAMA Network Open. 2023;6(6):e2320694. doi:10.1001/jamanetworkopen.2023.20694

27. Centers for Medicare & Medicaid Services. Hospital price transparency overview. Available from: https://www.cms.gov/hospital-price-transparency.

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2026 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.