")

Back to Journals » Risk Management and Healthcare Policy » Volume 17

Exploring Factors Influencing Family’s Enrollment in Community-Based Health Insurance in the City of Gondar Peri-Urban Community, Northwest Ethiopia: A Health Belief Model Approach

Authors Kebede MM

Received 12 January 2024

Accepted for publication 27 February 2024

Published 15 March 2024 Volume 2024:17 Pages 603—622

DOI https://doi.org/10.2147/RMHP.S454683

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Jongwha Chang

Molla Melkamu Kebede

Public Administration, University of International Business and Economics, Beijing, People’s Republic of China

Correspondence: Molla Melkamu Kebede, Email [email protected]; [email protected]

Background: A research gap exists in finding practical solutions to provide affordable and accessible health insurance coverage to improve CBHI enrollment and sustainability to people in resource-poor settings and contribute to achieving universal health coverage (UHC) in Ethiopia. This research was initiated to analyze the role of community trust in scheme management and health choice to identify significant factors based on the health belief model (HBM). This psychological framework explains and predicts health behavior by considering individual perceptions.

Methods: Cross-sectional information was gathered from 358 families, and original facts were utilized. Descriptive data and the Binary logistics in the econometric model were applied for data analysis.

Findings: The descriptive findings demonstrated that other variables were established to possess a significant consequence except for job and occupation variables. The results of the logistic regression model showed that the distance of the nearest health station from the family’s home in a minute [AOR (95% CI) =0.177 (0.015, − 0.399)], being a member of the families having an official position in local government or cultural structure [AOR (95% CI) =0.574 (0.355, 0.793)], having an experience of visiting health facilities [AOR (95% CI) =0.281 (0.166, 0.396)], and perceiving the local CBHI scheme management as trustworthy [AOR (95% CI) =0.404 (0.233, 0.575)] were positively associated with family enrollment in the CBHI scheme. On the other hand, being a member of the “rotating saving and credit association” (ROSCA) [AOR (95% CI) =− .299 (− .478, − 0.120)] was negatively associated with the family’s enrollment in the CBHI scheme.

Conclusion: Trust in CBHI scheme management, family’s experience of visiting health facilities, and distance from the nearest health station were essential factors influencing enrollment in CBHI schemes. “Rotating saving and credit association” (ROSCA) ° negatively and statistically significantly impacted the family’s CBHI enrolment status. Income level was not associated with enrollment.

Keywords: health belief model, community-based health insurance, enrollment, dropout, the city of Gondar Peri-Urban community

Introduction

Background of the Study

The necessity for medical coverage emerges from the inadequate long-term healthcare provision system in numerous developing nations, mainly because of the low ability of these countries’ administrations to gather resources.1 A survey in eighty-nine countries covering 89% of the world’s population suggested that around 150 million individuals are universally distressed by financial catastrophes yearly.2,3 At the same time, 100 million citizens are exposed to poverty annually owing to devastating health spending, according to the World Health Organization (WHO).4 It is conceivable that the lion’s share of these people inhabits limited resources surroundings such as Africa south of the Sahara (ASS) with fragile contemporary healthcare structure and, in most instances, absent any occupational health insurance project.2,4

The community-based health insurance (CBHI) project is an instrument for comprehensive health facility protection by supplying a monetary shield against healthcare costs.5 Emergent nations constitute 84% of the world’s people; among those, around 50% and more exist in Penury; furthermore, 90% of the worldwide affection load exists in such countries.5 Even though nations had coincided in the World Health Organization (WHO) Legislative meeting of 2005 to attain universal health coverage (UHC) through evolving risk-sharing operations (medical expense insurance programs) by depleting wasteful compensation (DWC), the practice of spending extravagantly for healthcare utilization motionlessly prevail undignified, less than 12%3,5,6

As 6,7 mentioned, healthiness and invulnerability are progressively identified as essential to alleviate poverty. Several below-average, low-middle-income countries are yet to be allowed to satisfy the justifiable healthcare demand of their residents or households.8 In most emergent nations, medical expenses are principally expended during illness and disbursement at the service provision place, assuredly deterring service supply.4 However, many countries need to do more to foster adequate resources to finance medical provision supplies. Consequently, they encourage CBHI to fund medical provisions.9 Since CBHI brings down the price of health care, there would be better access to modern/formal health facilities and higher utilization of healthcare services by insured individuals. Thus, CBHI provides equitable access to health facilities, irrespective of income and gender, while reducing the financial burden of illness.9 Nevertheless, it does not induce an appreciable influence on the availability of medical provisions due to insufficient members’ enrolment rate.

The federal government of Ethiopia also baited depilation of out-of-pocket spending from 37% to below 15% and destructive out-of-pocket medical costs from 3 to 2.5% by scheming and executing CBHI programs in 80% of districts. In district insurance nowadays, the district in Ethiopia is approximately 1100, while CBHI district coverage extends 827 (75%) in 2020.10 With the expanding district coverage, CBHI enrollment tendency from 2012 to 2020 manifests expanding in the long run, although it has been luxuriant from 125,142 in 2004 to 6,944,784 (1,459,123 indigents and 5,485,661 payees) in 2020. The statistics show that around 32.2 million people, 32.2% of the population, have been volunteers in the CBHI scheme and can obtain medical services in 2020. Despite the presumption that 85% of the entire population has participated in the non-formal private sector and the country owns 100 million population, CBHI enrollment participation in 2020, attributed for around 37% of the people’s non-formal private sectors, correlates to the goal of the roadmap of 80%, the achievement not encouraging.10,11

The need for medical coverage arises due to insufficient long-term healthcare infrastructure in numerous developing nations, primarily due to the limited ability of these countries’ governments to gather resources. As per a report from the EHIA in 2016, the CBHI plan faced difficulties with low membership rates and leaving the program after joining. This fluctuation of members was confirmed by statistics in the country, which showed a renewal rate of 5,694,722 (82%) for the plan and a dropout rate of 18%.10,11

In the Amhara region, the overall amount of CBHI introducing Wordas is 184 (99.9%) of the total Woredas in the regional state. In 2022, almost 3,320,864 families (82%) will be involved in the program, and 13,949,875 (61%) will be advantaged. Enrolled beneficiaries’ renewal rates in 2022 are 2,955,760 (90%), and the remaining 11% represents dropouts, as reported by the EHIA regional branch in 2023.12 In 2023, regional new participants’ enrollment was 440,198 (48.2%), Amhara region CBHI report (2023). Notably, in the urban areas, considering the six Regiopolitan cities of the region (Bahir Dar, Gondar, Dessie, Deber Markos, Debereberehan, and Kombolcha cities), 154,018 households (65% of the entire city administrations’ total) are enrolled. From 87,255 payee households (because of 37,422 direct beneficiaries), 59,501 households (68% of the 6 cities administrations) are renewed. This indicates that the enrollment rate among urban non-formal sector households is below the regional average.11,12 The performance of such schemes is confident in their viability, sustainability, membership proportion, and fluctuating membership, for instance, in the case of Ethiopia’s CBHI program.12,13

According to,12 in the City of Gondar Peri-Urban Area, there are 11 peri-urban kebeles organized within one city administration CBHI scheme, and the total average family income per year is 42,460 ETB (801$); membership is at the household level and not individuals. In 2022, Contributions vary by number of family members and range from Birr 950 (US$17.9) to Birr 1300 (US$24.5) per year per household. The federal government provides a 25% general subsidy for all members. City and regions finance a solidarity fund for indigents (an estimated 10% of the population) from their budgets. The provider payment method is fee-for-service. `Except for some ancillary service to be purchased from private facilities, public facilities are generally designated providers of services for members. The mechanism to accredit and engage providers is being worked out in the pilot phase. The average premium per year is 900 ETB (16.9$), which is 9.3% of the average total income of the family; at the time of healthcare service, there is a copayment averaged per year of 202 ETB (44% from the original yearly premium and 2.1% of the annual income of the family). In the region in 2013 EFY, the mean annual proportion premium per household increased from ETB 426 (∼US $8) to ETB 780 (∼US $14.7); in 2020, the annual share per household increased to a maximum of ETB 521 (∼US $9.8) in regions.10,13

In many emerging countries, substandard public medical service provision systems have relied on health insurance schemes to attain universal health insurance.14 Ethiopia still needs to execute a health insurance program; despite the scheme’s development to over 827 districts in the country, encompassing the study district of the peri-urban area of Gondar city in the Amhara region, CBHI enrollment progress could be better.12 In 2022, only 61% of eligible households in the City of Gondar Peri-Urban community were enrolled in the CBHI program, with a low renewal rate posing challenges to its sustainability.

To sum up, the achievement of CBHI depends on diverse components, for instance, society participation, low-cost premiums, service bundle design, and supplier payment procedures. Even though it has possible advantages, CBHI has encountered problems regarding sustainability, coverage, and quality of care, and enrollment still needs to be appreciated in some constituencies. In Amhara Region, CBHI enrollment has exceeded, but sustainability and quality of care still need to be questioned. Objectively, the study intends to examine the association between families, institutions, and trust factors and the decision of the family to join a CBHI in the City of Gondar Peri-Urban community. Specifically, the aim is to identify and analyze the specific determinants influencing households’ registration, explore the institutional variables that mediate households’ decision to participate in the CBHI program and assess the impact of households’ trust in scheme management and modern care on their decision to register in the CBHI program in the study area based on Health Belief Model approach.

Literature Review

Definition and Concept of Health Insurance

Health insurance is a way to distribute the financial risk associated with the variation of individuals’ healthcare expenditures by pooling costs over time through prepayment and over people by risk pooling.15 CBHI is a non-profit scheme organized to improve financial access to healthcare services and to protect its members against the financial risks associated with illness.16 It operates based on solidarity and mutual aid values with its institutional arrangements designed to maximize its critical functions of revenue collection, risk pooling, and purchasing of health care services. FMoH, (2008). In low-income countries, health insurance can be introduced for broader segments of the population through government subsidization of the premium to the poor and low-income informal sector workers, allowing more rapid coverage expansion and more direct targeting of the poor households to robust health financing system.16

One of the ways that poor communities manage health risks, in combination with publicly financed healthcare services, is through community-based health insurance schemes (CBHISs). They are designed to be simple and affordable and to draw on resources of social solidarity and cohesion to overcome problems of small risk pools, moral hazard, fraud, exclusion, and cost escalation.15 In theory, all CHI schemes share the following five characteristics: (1) Community-based social dynamics and risk pooling, where the schemes are organized by and for individuals who share common characteristics (geographical, occupational, ethnic, religious, gender, and so on); (2) Solidarity, where risk sharing is as inclusive as possible within a given community and membership premiums are independent of individual health risks (3) Participatory decision-making and management, (4) Non-profits character and (5) Voluntary affiliation,16,17 CBHI beneficiaries are associated with or involved in managing community-based schemes, at least in the choice of the health services they cover. It is voluntary, formed based on mutual aid, and covers a variety of benefit packages.1,14 As of,15 CBHIs face constraints related to their small size, limited access to management and technical insurance skills, and the quality and accessibility of local healthcare service providers. CBHIs often fail due to weaknesses in management, financing, or a combination. In addition, the poorest groups are unlikely to become members of CBHIs because they are generally unable to afford the premiums.17

Theoretical Foundation Regarding Health Insurance

According to,18 studies on insurance requirements utilize anticipated utility theory to describe entities’ determination regardless of whether to insure. This Hypothesis declares that health insurance is necessary for risk avoidance and the wish to avoid the financial result of ill Health. This hypothesis suggests that the greater an individual’s aversion to risk, the greater the insurance they will purchase.

According to,19 State-dependent admittance reasons that insurance absorption relies on an individual or family’s contemporary Health and socioeconomic condition and the anticipated discharge or satisfaction from insurance, successively perhaps regarded as the execution of insurance coverage and the accessibility quality of health care. Prospect theory addresses the insurance circumstance and discusses that individual decision-making is according to exacting premium costs versus health risks and the related gain or loss expectation.20,21

This proposition proposes that the higher an individual’s reluctance to take risks, the more insurance they will procure. As suggested by the endowment effect and status quo bias,21 the determination to insure individuals can be intricate for people, especially in regions where insurance is a strange notion and the illiteracy rate is maximum. People will exclusively access insurance if they trust that the advantages of insurance are equivalent to or exceed the cost of not being insured. Social capital is pivotal in the CBHI context. The non-formal climate of confidence factors equivalently or exceeds significantly in describing the desire for insurance. The trust in the insurer or the particular insurance yield can be inclined to an insurance confidence. Harmony in the community or faith in the administration will positively impact individuals’ determination to register in CBHI. Institutional factors such as the technical positioning developed by the scheme management also affect an individual’s appreciation of the program’s advantages.22

“The Impact of OPP Expenses on Low-Income Households’ Decision to Join CBHI in Ethiopia”?

Admissions to medical provision and achieving Universal Health Coverage (UHC) are among the principal universal SDG programs and an essential issue for emerging countries, including Ethiopia.23,24 Country’s Gross medical spending in 2017/18, USD in billions 3.1, out of this government portion or allotment, % 32.0, from OOP % 30.6 from extraneous funding, % 35.2 some other private funding % 2.0, Government medical spending, the portion of GDP 1.2%, and Government medical spending as a portion of total government expenditure, is 8.1%. The odds of total public sector health expenditure against the country’s government expenditure remain low.24

In Ethiopia, to prevail over the vast number of households’ excessive dependence on direct out-of-pocket (OOP) spending for health care and insufficient medical service provision utilization, OOP spending comprised 35% of the contemporary medical expenditure by 2018, which decreased from 47% in 2011. The initiation of CBHI has earned a crucial financial shield from ruinous health spending in Ethiopia,24,25 where health insurance coverage was 32% in 2020. This performance was below the investigation in Tanzania, 49%, and Rwanda, 85%, which may be accredited to dissimilarities in execution strategies, insurance contribution, and the package of benefits.25

When examining the influence of out-of-pocket (OPP) expenses on the decisions to join Community-Based Health Insurance (CBHI) at national and regional levels, comparing and contrasting the out-of-pocket expenditure patterns is essential. OPP expenses are crucial in shaping individuals’ and families’ decisions to enroll in CBHI programs. The Health Belief Model (HBM) posits that people are more likely to engage in health-related behaviors, such as enrolling in health insurance, if they perceive the benefits to outweigh the costs. In the context of CBHI, out-of-pocket expenses refer to the financial burden individuals and households bear for healthcare services not covered by the insurance scheme.

At the national level in Ethiopia, out-of-pocket healthcare expenditures, at 33% in 2020, have been a significant concern. The country has been working towards achieving universal health coverage and reducing the reliance on out-of-pocket payments. According to a study by,26 out-of-pocket payments accounted for a substantial portion of healthcare financing in Ethiopia, with many households facing financial hardships due to healthcare expenses. This high financial burden can deter individuals and families from enrolling in CBHI programs, as they may perceive the costs to outweigh the potential benefits.26,27

In the specific context of the City of Gondar Peri-Urban community in Northwest Ethiopia, regional variations in out-of-pocket expenditures may exist. For example, a study by28 examined the determinants of out-of-pocket health expenditures in the Amhara region, where Gondar is located. The findings indicated that households in rural areas and those with lower socioeconomic status had higher out-of-pocket health expenditures. These disparities in out-of-pocket expenses can influence households’ decisions to enroll in CBHI, as higher expenses may make the insurance program more attractive to mitigate the financial burden.29

Testing the Health Belief Model (HBM) in Ethiopia

The theory most appropriate to be tested through this study is the Health Belief Model (HBM). The HBM extensively utilizes hypothetical configurations in health behavior investigations, which describe why individuals take particular measures to safeguard, shield, perceive, or investigate disease.30 It proposes that communities’ healthcare conduct is impacted by their assumptions regarding the following determinants: “perceived susceptibility”, “perceived severity”, “perceived benefits”, “perceived barriers”, “cues to action”, and “self-efficacy”.31 “Perceived susceptibility” concerns the ideology that one is Susceptible to progressing a health problem. In the circumstances of this investigation, it could be households’ discernment about their susceptibility to disease and their necessity for medical insurance. “Perceived benefits” refer to the belief that taking action (such as enrolling in CBHI) will lead to positive outcomes, such as better healthcare provision and financial shield availability.30,31 “Cues to action” refer to external determinants that motivate individuals to adopt the decision, such as media campaigns, social influence, or personal experiences with illness. “Self-efficacy” concerns the assumption in one’s capability to enact a particular behavior successfully.31,32

Based on the HBM, the Research Has Tested the Following Hypotheses

H1: Households’ enrollment in CBHI is positively associated with their “perceived susceptibility” to disease and their “perceived severity” of health problems. H2: Households’ enrollment in CBHI is positively correlated with their “perceived benefits” of enrolling in the scheme (such as better availability to healthcare provisions and financial safeguards) and negatively associated with perceived barriers (such as lack of information or affordability) and H3: According to the Health Belief Model,32 households’ enrollment in CBHI is positively associated with cues to action, such as media campaigns or personal experiences with illness, and their self-efficacy in making informed decisions about enrolling in the scheme. Additionally, the analysis has included institutional variables to explore potential impacts on households’ enrollment in CBHI.

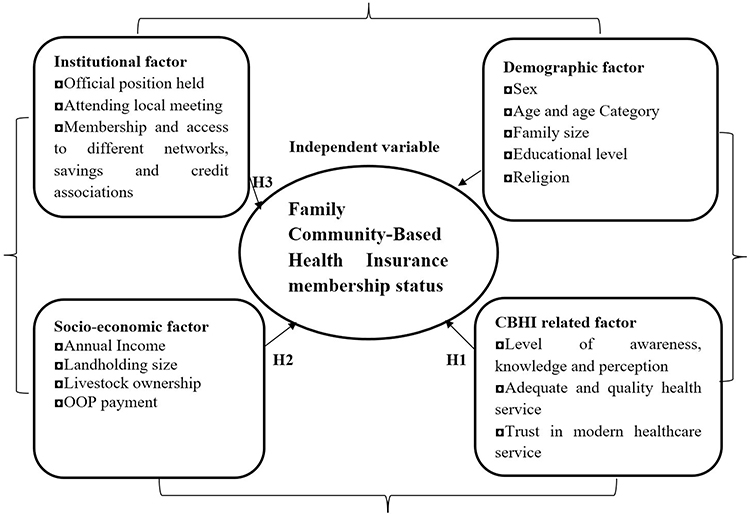

Conceptual Framework

Figure 1 of the conceptual framework illustrates that the dependent variable of this study is “Households’ CBHI enrollment status” In contrast, the independent variables are categorized into four groups: demographic variables, socioeconomic variables, institutional variables, and CBHI-related variables. Demographic variables encompass factors such as sex, family size, age category, educational level, and religion, which may influence households’ decision to enroll in CBHI based on cultural beliefs and values. Socioeconomic variables include annual income, landholding size, livestock ownership, and out-of-pocket (OOP) payments, which may impact households’ decision to enroll in CBHI based on their financial situation and resource access.

|

Figure 1 Conceptual framework. Note: Author’s own Formulation (2023). |

Institutional variables include the official position, attendance of local meetings, membership access to networks like saving and credit associations, and distance to health facilities. These variables may influence households’ decision to enroll in CBHI based on their trust in the scheme management and community participation. CBHI-related variables include awareness, knowledge, and perception of CBHI, adequate and quality health service, and trust in modern healthcare services.

The relationship between the HBM factors and the independent variables is examined in this study. Each independent variable, including demographic variables, socioeconomic variables, institutional variables, and CBHI-related variables, can be associated with the factors of the HBM. For instance, demographic variables such as age, gender, and education level may influence households’ perceptions of susceptibility to illness and severity of health problems. Socioeconomic variables such as income and occupation may affect households’ perceived benefits and barriers to enrolling in CBHI.33,34 CBHI-related variables, such as the cost of premiums and the coverage of services, may also influence households’ perceived benefits and barriers to enrolling in CBHI.35 Institutional variables, such as the availability of health facilities and the quality of healthcare services, may influence households’ cues to action and self-efficacy in making informed decisions about enrolling in CBHI.33,34

Method and Methodology

Design and Approach-

A community-based cross-sectional study was conducted among 358 peri-urban communities (143 enrolled and 215 not enrolled) in Gondar City, northwest Ethiopia, from January 2, 2023, to April 14, 2023. Gondar metropolitan city is 749 km from Addis Ababa, Ethiopia’s capital. The district’s total population was estimated to be 483,224 (246,444 males and 236,779 females), founded in 1636. The city has 25 urban and 11 rural kebeles (the lowest administrative units in the country), ten health centers, 25 health posts, one general and one referral hospital, 15 private clinics, and 22 drug stores. The CBHI was introduced in the city as a full-scale scheme in 2019. In 2022, from 68,695 eligible households, 45,173 (65.8%) households were members of the CBHI scheme. This investigation is focused on 11 rural kebeles insurance community participation is very low compared to urban kebeles. The study has used a “Health Belief Model” approach to examine the determinants impacting household enrollment in CBHI. It used a mixed-methods approach to collect household data, encompassing qualitative and quantitative data-gathering methods.

Study Population and Sampling Procedures

A multi-stage sampling method was applied to select sample respondents; the purposive selection method was used to choose from 11 rural Kebeles (the smallest administrative unit) in the City of Gondar Peri-Urban community. Three rural kebeles were chosen randomly (Lozamariam, Belajig, and Weleka) and were selected first using a simple random sampling technique (lottery method). Then, the households in each selected Kebele were stratified into enrolled and non-enrolled categories; based on this, 358 sample households were determined using the formula given by,36,37 from a total of 2687 population (households) found in the selected kebeles at 5% error and 95% confidence level. Yemane forwards the procedure as follows:  , Where n is the minimum sample size to be drawn, e is the desired level of precision, ie, 5%, and N is the population size, ie, the total population size found in the selected three (3) kebeles. Therefore, the proportionate sample size was taken from each Kebele. Finally, 358 valuable responses from sample respondents will be used for data analysis. Use a purposive selection method within each Kebele to choose the specific households to be included in the study; this selection ensured a representative sample of both enrolled and non-enrolled households, train 12 study assistants (enumerators) on administering the structured questionnaire to selected respondents visit each selected household and conduct the interview using the structured questionnaire. It is essential to ensure that the chosen households represent the diversity and characteristics of the City of Gondar Peri-Urban community.

, Where n is the minimum sample size to be drawn, e is the desired level of precision, ie, 5%, and N is the population size, ie, the total population size found in the selected three (3) kebeles. Therefore, the proportionate sample size was taken from each Kebele. Finally, 358 valuable responses from sample respondents will be used for data analysis. Use a purposive selection method within each Kebele to choose the specific households to be included in the study; this selection ensured a representative sample of both enrolled and non-enrolled households, train 12 study assistants (enumerators) on administering the structured questionnaire to selected respondents visit each selected household and conduct the interview using the structured questionnaire. It is essential to ensure that the chosen households represent the diversity and characteristics of the City of Gondar Peri-Urban community.

Source of Data and Method of Data Collection

Study assistants who were trained implemented information gatherings by administering the structured questionnaire to eligible households, recruiting human participants, and distributing questionnaires to obtain valuable data from 358 enrolled and unenrolled respondents from January 2, 2023, to April 14, 2023. Participants provided verbal informed consent that the ethical committee confirmed. Questionnaires gathered numerical information from answerers and qualitative evidence, employing thorough examination with institutional managers and healthcare providers for triangulation. The questionnaire was developed based on the Health Belief Model factors, dependent household enrollment status variables, and independent variables.

Data Analysis

Data analysis used percentages, frequencies, mean, and standard deviation for socioeconomic and demographic variables. A t–test was employed to examine the distinction between household enrollment decisions with continuous independent variables. A chi-square test was also utilized to identify the relationship between household enrollment decisions and dummy independent variables. Furthermore, binary logistic regression analysis was undertaken to determine significant factors impacting families’ enrollment status.38,39

The econometric model specification focused on the discreet choice of joining or not joining the CBHI program. A logit model was employed to determine households’ enrollment assumption and the impact of socioeconomic, demographic, institutional, and CBHI scheme-related characteristics on this decision. The binary logistic regression (logit model) was used to analyze the enrollment function of the study, and the STATA 17 software package was utilized for estimation.

A binary logistic regression model was suitable for analyzing the factors influencing household enrollment in the CBHI scheme in the City of Gondar Peri-Urban community. The dependent variable was the binary response variable indicating household enrollment status (1 for enrolled, 0 for not enrolled). In contrast, the independent variables included various socioeconomic and institutional factors that may influence enrollment decisions.

The logistic regression model can be specified as follows:

Logit (Enrollment) = β0 + β1Education + β2Sex + β3Age + β4Family Size + β5Landholding Size + β6Livestock Ownership + β7Annual Income + β8Distance from Health Facilities + β9Service Quality + β10Access to Social Networks + β11Membership in Different Government Officials and Organizations + β12Distance to the Nearest Health Centre + β13Adequate and Quality Health Care Service + β14Trust in Modern Health Care + β15Trustworthiness of CBHI Scheme Management

Where:

- Enrollment is the binary response variable indicating whether the household is enrolled in the CBHI scheme (1 for enrolled, 0 for not enrolled)

- Education, Sex, Age, Family Size, Landholding Size, Livestock Ownership, Annual Income, Distance from Health Facilities, Service Quality, Access to Social Networks, Membership in Different Government Officials and Organizations, Distance to the Nearest Health Centre, Adequate and Quality Health Care Service, Trust in Modern Health Care, and Trustworthiness of CBHI Scheme Management are the independent variables that may influence households’ enrollment decisions.

- β0 is the intercept term, and β1 to β15 are the coefficients of the independent variables.

The logistic regression model estimates the log odds of households’ enrollment in the CBHI scheme based on the independent variables. The coefficients represent the change in log odds of enrollment associated with a one-unit change in the corresponding independent variable, holding all other variables constant.

To test the hypotheses, the logistic regression model can estimate the association between the independent variables and households’ enrollment decisions. Hypothesis 1 can be tested by examining the coefficients of perceived susceptibility to illness and perceived severity of health problems. Hypothesis 2 can be tested by examining the coefficients of perceived benefits and perceived barriers to enrolling in the scheme. Hypothesis 3 can be tested by examining the coefficients of cues to action and self-efficacy in making informed decisions about enrolling in the scheme. The significance and direction of the coefficients can indicate whether the hypotheses are supported or not.

Variables

Dependent Variable

The dependent variable measured rural households’ enrolment status in the CBHI scheme, which has a binary response: 1 if the household is enrolled and 0 if not.

Independent Variables

The following variables are involved: demographic variables sex, age, family size of the household, proportion of family size between 14 to 64 years old, proportion of families above 64 years old, and household head education condition level.

The socioeconomic variables consist of the size of the cultivated land of the household, number of animals in the household (TLU), distance of the nearest health station from the household home (in minutes), and participation in different local meetings (1=yes). Additionally, the income level of households converted into natural legalism is considered.

Institutional factors include household graduation in HEP and certification (1=yes), participation in and use of different credit packages (1=yes), membership in the local Funeral Association (LFA) (1=yes), membership in ROSCA for any member of the household (1=yes), any member of the household holding an official position in local government or cultural structure, frequency of visiting health facilities by the household for the last year, and perception of trustworthiness of the local CBHI scheme management (1=yes).

CBHI-related factors include the health choice of the household head (1=Modern Healthcare), perception of the quality of healthcare services (HCS) from public health facilities (1=neutral), and perception of the quality of HCS from public health facilities (1=poor). The gender of the household leader (male or female) was expected to influence enrollment decisions, with female-headed households more likely to enroll. Age was also considered, with older household heads expected to be more likely to enroll. Family size, education level, annual income, landholding size, and livestock ownership were hypothesized to affect enrollment positively. Membership in different organizations and attendance at local meetings were expected to influence enrollment positively.

The level of awareness and knowledge about the CBHI scheme was investigated, and it was expected that higher awareness would lead to a higher likelihood of enrollment. Membership and access to social networks, such as savings and credit associations, were expected to affect enrollment positively. In contrast, distance to the nearest health center was expected to have a negative relationship. Perceptions of adequate and quality health care service, trust in modern health care, and trustworthiness of the CBHI scheme management also influenced enrollment decisions. Positive perceptions and trust were expected to increase the likelihood of enrollment.

Results and Discussions

Enrolment Status by Socioeconomic Factors

Job Occupation of Sample Households

From the total sample households, 271(75.75%) are farmers, 31(8.66%) are engaged in off-farm activities, 38(10.61%) are traders, 6(1.68%) are daily laborers, and 12(3.35%) are involved in other activities. from a member of the CBHI scheme 77.62% are farmers, 2.1% are in off-farm activities, 14.68% are traders, 2.1% are daily laborers, and 3.5% are from other activities. In comparison, 74.42%, 13.02%, 7.91%, 1.4%, and 3.25% of the not-enrolled households are farmers from off-farm activities, traders, and daily laborers engaged in other activities.

The Landholding Size of Household Heads

From the survey results (Table 1), the typical extent of land ownership of enrolled and not-enrolled households is 1.311 and 0.964 acres, accordingly, and the standard deviation of the land ownership extent of enrolled along with not-enrolled families is 0.8245 and 0.9688 acres consequently. The average amount indicates that registered households’ mean land ownership extent is greater than that of not-enrolled homes. The t-score (t=3.5193; P=0.0005) shows a statistically meaningful contrast between the average land ownership and enrolled and not-enrolled households. This inference suggests that representative families with high land ownership extent are likelier to enroll in the CBHI scheme.

|

Table 1 Enrolled and Non-Enrolled Households by Socioeconomic Factors |

Livestock Ownership

As per the study results (Table 1), the mean extent of livestock of the representative enrolled along with not-enrolled households was 4.463 and 3.541 TLU tropical livestock,40 accordingly, and the standard deviation of the cattle holding extent of enrolled along with not-enrolled households was 3.613 and 2.72 TLU accordingly. The t-score (t=2.5974; P=0.01) indicates a statistically meaningful contrast between the average cattle-ownership extent of enrolled and not-enrolled households concerning their livestock-holding time. This assumption suggested that representative families with higher cattle extent were likelier to enroll in the CBHI scheme, like landholding results.

Yearly Income of Sample Residences

As you see in Table 1, the yearly earnings of the sampled residences are computed by ETB and discovered by the investigator. Consequently, the average annual earnings of the enrolled and non-enrolled households are 42,460.23 and 33,751.79 ETB, and the Standard Deviation (St. Dev.) of the yearly Income of enrolled and not enrolled households was 19,963.22 and 17,977.05 ETB; therefore, the average Income indicates a difference in annual Income between enrolled and not enrolled households. The t-score (t=4.2044; P=0.00) also shows a statistically meaningful contrast between the average yearly income of enrolled and not enrolled households concerning their income amounts.

Enrolment Status by Institutional Factors and Participation in Different Social and Development Programs

Frequency of Visiting Health Facilities

Based on the findings of the investigation (Table 2), the mean frequentness of visiting health facilities of the sampled enrolled along with not enrolled households is 2.412 and 0.837, accordingly, and the Standard Deviation (St. Dev.) of visiting health facilities of enrolled along with not enrolled households is 1.224 and 0.994, respectively. The t-score (t=12.835; P=0.00) shows a statistically meaningful contrast between the average value of enrolled and unenrolled residents concerning their experience of visiting health facilities. This conclusion suggested that sampled residents with a greater frequency of visiting health facilities are more likely to enroll in the CBHI scheme to meet their health problems with an affordable premium payment, and 35.66% of households are enrolled since the premium is below OOP payment. Remoteness is presumed to exist among the significant explanatory variables that residence leaders could consider if they decide to enroll in the CBHI program.

|

Table 2 Enrolment Status by Institutional Factors (Distance and Frequency of Visit) |

The remoteness between the residence house and the nearby health post on foot is asked in the minute. A categorical specification is adopted to see the role of space on a household’s enrolment and categorized near as a distance below 30 minutes, not far as a distance between 30 to 60 minutes, and far as a distance above 60 minutes.

As indicated in Table 3 below, the t-score (t=8.78; p= 0.00) of the sampled residences demonstrates that there is a statistically meaningful contrast in the distance betwixt enrolled and not enrolled residences’ homes to the nearby health station, and it has a substantial effect on CBHI scheme enrolment decision of households. Table 3 shows that more are enrolled as households reside in the nearest and at a moderate distance to health facilities. At the same time, high not enrolled is experienced as the household lives distant from medical stations.

|

Table 3 Distance to the Nearest Health Station |

Official Positions Held

Table 4 below indicates that out of the total sample households, 47(13.13%) of the enrolled and not enrolled households have an official position, and 41(28.07%) and 6(2.79%) are registered and not enrolled households, respectively. The representative residences’ chi-square score (2=50.437; p= 0.000) indicates a statistically meaningful contrast in the official position of enrolled and not enrolled households.

|

Table 4 Enrolment Status by Official Position & Participation in Local Meetings |

Participation of Respondents in Different Local Meetings

This variable determines the role of household heads’ involvement in various local and CBHI scheme-related conferences/gatherings.

Table 4 above indicates that out of the total sample households, 196(54.75%) of the enrolled and not enrolled families were participating in local meetings, and out of the 98(68.53%) and 98(45.58%) sample households were enrolled and not enrolled households accordingly. The chi-square score (x2=18.2581; p= 0.000) of the sampled households indicates a statistically meaningful contrast in the participation of registered and not enrolled households. This belief shows that families with experience participating in such meetings are likelier to enroll in the CBHI program compared to those who do not participate.

Enrolment Status of CBHI Scheme Related Factors Knowledge About the Scheme

As shown in Table 5 below, 87.43% of enrolled and not enrolled residents in the survey locality have information about the CBHI program. For the amount and time of premium payment, 138(96.50%) and 79(36.74%) of enrolled and not-enrolled households, respectively, are aware of the price; this indicates an awareness difference.

|

Table 5 Enrolment and Knowledge About the Scheme |

From the survey results (Table 6), the average awareness level of enrolled and not enrolled households is 4.236 and 3.215, respectively, and the standard deviation of the awareness level of enrolled and unenrolled households is 0.567 and 0.717, respectively. Hence, the mean value indicates that the average awareness of enrolled households is more considerable than that of not-enrolled households. Moreover, the t-score (t= 15.348; P=0.0000) shows a statistically meaningful contrast betwixt enrolled and not-enrolled households’ mean awareness of the CBHI scheme enrolment. Therefore, the level of understanding highly affects households’ enrolment decisions.

|

Table 6 Enrolment Status by Awareness Level |

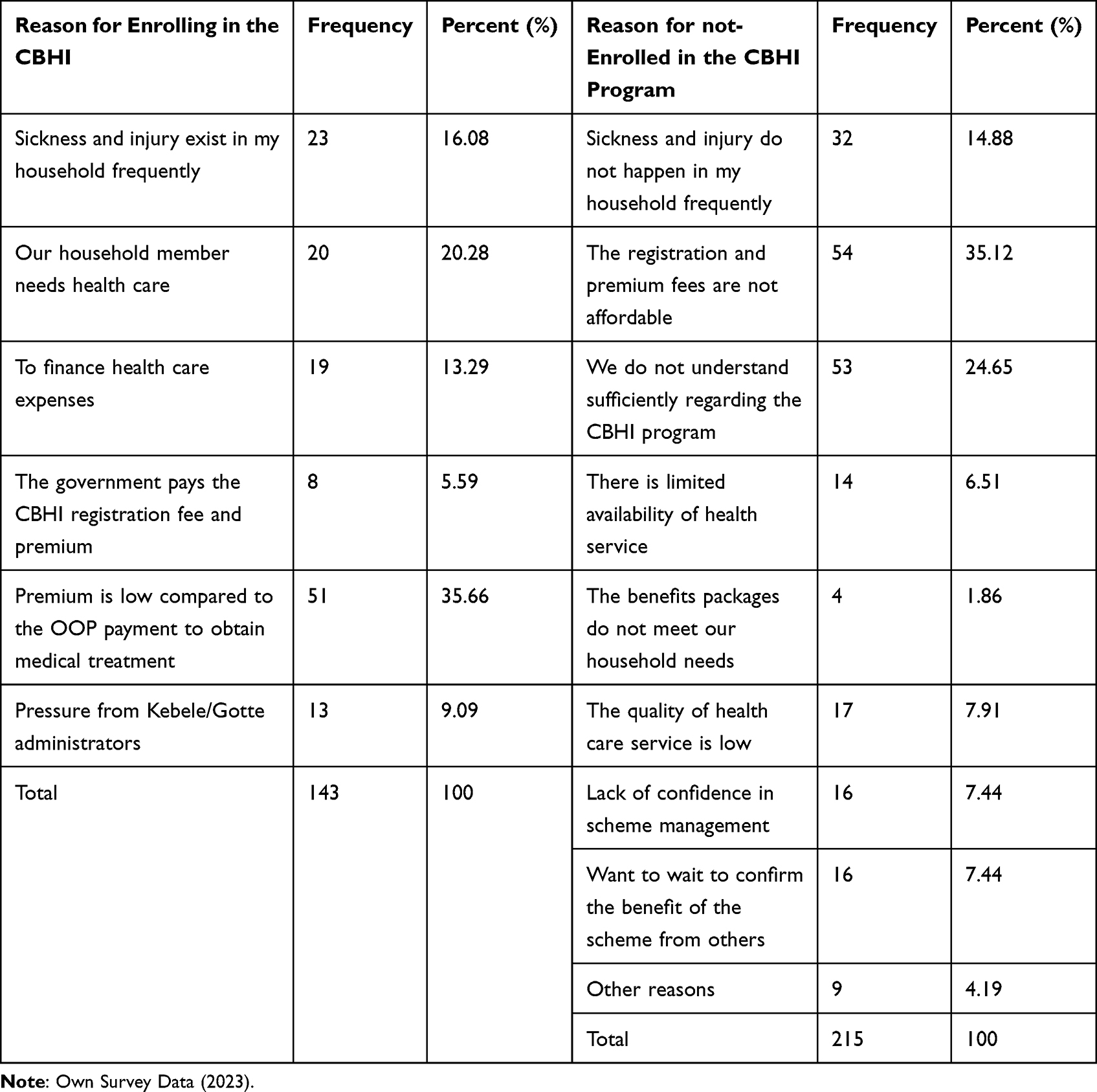

Reasons for Enrolment

Table 7 below shows why households were not enrolled in the CBHI program. As the survey results show, 54(35.12%) respondents did not enroll because the registration and premium fees were not affordable. For 53(34.65%) not-enrolled households, adequate knowledge about the CBHI scheme was needed. 51(35.66%) respondents confirm that the premium is low compared to OPP expenses, which is the reason for their enrollment.

|

Table 7 Motives for Enrolment Status of Sample Households |

In addition to this, for 32(14.88%), 17(7.91%), 16(7.44%), and 16(7.44%), the motive for not- being enrolled in the program was non-occurrence of sickness and injury in their household accordingly, the low quality of health care service, lack of confidence in program administration, and the need to get time to know and confirm the benefit of the scheme from member households respectively.

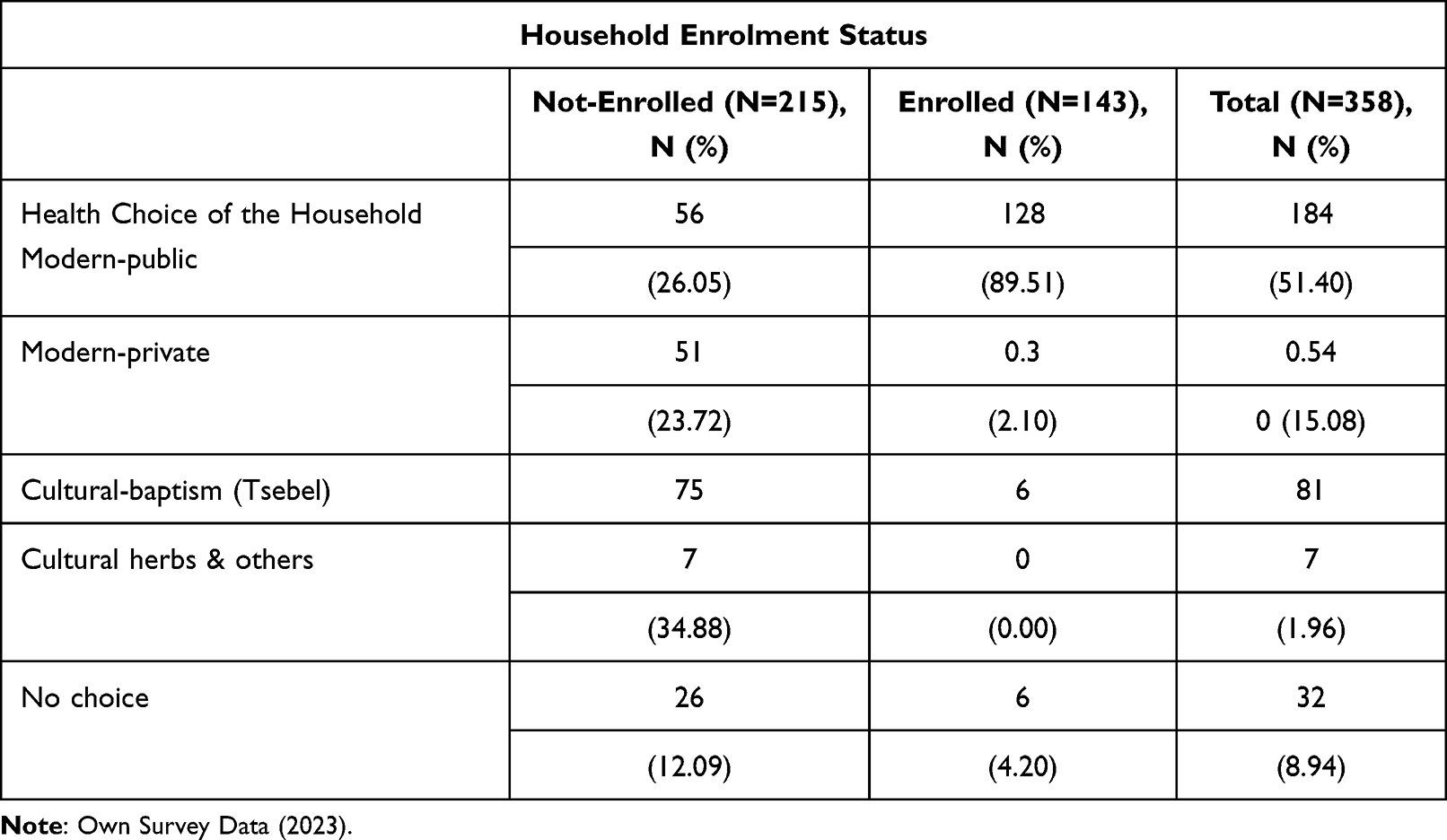

Health Choice of Sample Households

From the total sample households, 238(66.48%) chose modern health care service, whereas the rest 120(33.52%) chose either cultural treatment or did not use any health care treatments.

The percentage contrast between enrolled and not enrolled households signifies that the health choice of the sample household highly affects the enrolment status of the respondents (Table 8).

|

Table 8 Sample Households’ Healthcare Care Choice |

Synopsis of Statistical Analysis Findings for Factors That Explain

To gain a comprehensive understanding of the “demographic”, “socioeconomic”, and “institutional” participation in different social networks and variables related to the CBHI scheme, which differentiates the enrolled from the non-enrolled group, chi-square, and t-score tests have been conducted. The descriptive result in the above discussion indicates that except sex, other explanatory variables are established to have a significant influence on household enrolment status.

Test of the Overall Goodness of Fit is Investigated Utilizing the Hosmer-Lemeshow Method

The goodness of the model is mirrored in a non-significant p-score. The Hosmer-Lemeshow test p-score is 0.2193, which is insignificant. This conviction suggests that the overall goodness of fit of the model is good. That means the model fits the data well. We can use the regression result for policy recommendations based on these tests. Table 9 illustrates the outcomes of the binary logistic regression model estimation of determinants significantly determining the households’ enrolment condition decision. The model was mirrored to be significant at a 1% importance level. The logit model examination highlights allowing for the organized influence of variables between enrolled and not-enrolled households in the research locality. The focus is on examining the factors collectively instead of individually. Out of all the elements, seven were noteworthy, while the rest were inadequate in clarifying the fluctuations in the reliant part.

|

Table 9 Logistic Regression Analysis for CBHI Family’s Enrollment in CBHI in the City of Gondar Peri-Urban community, Northwest Ethiopia |

The study found significant associations based on the binary logistic regression model results. Regarding Demographic factors, the sex of the household head [AOR (95% CI) =0.186 (−.0.966, 0.468)], the odds of enrollment were significantly lower for households with a male head compared to female leads; Age of the household head [AOR (95% CI) =0.002 (−.009, 0.013)], the odds of enrollment decreased with increasing age of the household head, consequently was no significant association between family size and enrollment.

Concerning Socioeconomic factors, Cultivated land size of the household [AOR (95% CI) =0.088 (−.067, 0.243)], Larger cultivated land size was associated with higher odds of enrollment, Number of animals having the household in TLU [AOR (95% CI) =0.020 (−.025, 0.066)], Owning more animals was associated with higher odds of enrollment, and Income level of households converted into natural logarithm [AOR (95% CI) =0.070 (−.010, 0.238)], higher income levels were associated with higher odds of enrollment.

Institutional factors: distance of the nearest health station from household home in a minute [AOR (95% CI) =0.177 (0.015, −0.399)], the longer the distance, the lower the odds of enrollment. Participating in different local meetings [AOR (95% CI) =0.177 (0.015, 0.399)] was associated with higher odds of enrollment. Members of the household who have an official position in local government or cultural structure [AOR (95% CI) =0.574 (0.355, 0.793)] were associated with higher odds of enrollment. Having your household had an experience of visiting health facilities [AOR (95% CI) =0.281 (0.166, 0.396)] was associated with higher odds of enrollment. The local CBHI scheme management is trustworthy [AOR (95% CI) =0.404 (0.233, 0.575)] and was associated with higher odds of enrollment.

Regarding Health belief factors, Health choice of the household Head Modern Healthcare [AOR (95% CI) =−.217 (−.530, 0.096)], a preference for modern healthcare was associated with lower odds of enrollment. So, some variables, such as family size of the household [AOR (95% CI) =−.006 (−.064, 0.053)], income level of households converted into natural logarithm [AOR (95% CI) =0.070 (−.010, 0.238)], and quality of HCS from public health facilities as the respondents’ perception neutral, [AOR (95% CI) =−.030 (−.221, 0.160)], and quality of HCS from public health facilities as the respondents’ perception poor [AOR (95% CI) =−.070 (−.284, 0.143)], perceptions of healthcare quality, did not show significant associations with enrollment in the CBHI program. These findings provide insights into the specific determinants influencing households’ registration in the CBHI program in the City of Gondar Peri-Urban community, highlighting the importance of demographic, socioeconomic, institutional, and health beliefs in shaping enrollment decisions.

Interpretation of the Model Results

The logistic regression model demonstrated that households’ enrollment in the CBHI scheme was positively correlated with the proximity of the nearest health station to their home in minutes [AOR (95% CI) =0.177 (0.015, −0.399)], membership of the household head in local government or cultural structure [AOR (95% CI) =0.574 (0.355, 0.793)], experience of visiting health facilities [AOR (95% CI) =0.281 (0.166, 0.396)], and perception of the local CBHI scheme management as trustworthy [AOR (95% CI) =0.404 (0.233, 0.575)]. Conversely, membership in the “rotating saving and credit association” (ROSCA) [AOR (95% CI) =−.299 (−.478, −0.120)] was negatively associated with households’ enrollment in the CBHI scheme.

The study’s hypothesis received partial support. The logistic regression model did not support H1, which suggested that households’ enrollment in CBHI is positively linked to their perceived susceptibility to illness and the severity of health problems. H2, which proposed that households’ enrollment in CBHI is positively associated with perceived benefits (eg, improved access to healthcare services and financial protection) and negatively related to perceived barriers (eg, lack of information or affordability), was partially supported as the proximity of the nearest health station to the household home in minutes was positively associated with households’ enrollment. However, the income level of households converted into natural logarithm was not linked to households’ enrollment. H3, which posited that households’ enrollment in CBHI is positively connected to cues to action (eg, media campaigns or personal experiences with illness) and their self-efficacy in making informed decisions about enrolling in the scheme, was partially supported by the finding that visiting health facilities was positively associated with households’ enrollment.

Education Level of Household Head

Education enhances an individual’s capacity to analyze details from any given source. The model results reflected in Table 9 show that the academic standard of households holds statistical significance at a 10% significance amount and positively impacts the dependent variable. This deduction indicates that families with at least primary education are more inclined to sign up for the scheme than those uneducated. According to the model result, literate heads of households increase the odds of enrollment in the CBHI scheme by 18.54% compared to illiterate ones. This finding aligns with,41,42 demonstrating that education contributes positively to health insurance enrollment and holds statistical significance. According to,42 the education level of the head of the household impacted the utilization of health services and overall mortality within households.

However, this discovery disagrees with the findings of,43 purporting that while the level of education contributes positively to household enrollment status, its statistical significance is dismissed.

Official Positions Held, Attending Local Meetings/Gathering/ and Membership and Access Different Networks, Saving and Credit Packages

Concerning the variables examined, it was discovered that households with a household leader or any member occupying an official government position, participating in community gatherings, or belonging to a community group called “ROSCA” were statistically significant at the 1%, 5%, and 1% levels of significance, accordingly. However, variables related to financial status or social connections did not impact enrollment. Having an official or community leadership role increased CBHI enrollment by approximately 57.43%. This is because these individuals had access to information about the scheme and could educate and sensitize the community about its benefits, a finding that is consistent with prior research. Participation in local gatherings increased the likelihood of household enrollment by 17.69%. However, membership in “ROSCA” had an adverse effect, decreasing the chance of registration by 29.9%. However, the study on willingness to enroll for CBHI in Simada District, Ethiopia, found that borrowing money for medical services was a significant factor associated with willingness to enroll in the health insurance scheme. Participants who had borrowed money for medical services were more likely to be willing to enroll in community-based health insurance compared to those who had not borrowed money.44

Distance to the nearest health facility was also a significant factor in households’ decisions to enroll in the CBHI scheme, with an inverse relationship observed. As the distance from a household’s residence to the nearest health station increased, the likelihood of enrollment decreased by 1.28%. This indicates that proximity to health facilities motivates community members to enroll in the scheme. This finding is consistent with44 that the distance from health facilities significantly influenced the willingness to enroll in community-based health insurance. Participants who lived less than 5 kilometers from health facilities had a higher likelihood of being willing to enroll in the health insurance scheme compared to those who lived farther away.

The CBHI enrollment decision of households is negatively impacted by the distance to the nearest health facility, a significant variable at a 1% significance level. As anticipated, space is one of the factors that influence enrollment decisions. The model output reveals that for every increase in distance between a household’s residence and the closest health station, the likelihood of enrollment decreases by 1.28%. This suggests that the closer the health facility is to the community, the more motivated community members are to enroll in the scheme. This finding is consistent with44,45 research, which indicates that individuals living near a health facility play a significant role in CBHI enrollment. However, it contradicts the46 study, which found that households’ enrollment increases with increased travel time.

Frequency of Visiting Health Facilities

According to the findings of the survey (as presented in Table 9), it can be observed that out of the households that enrolled in the CBHI scheme, 39.94% were able to access modern medical posts in the past year, while 8.39% were not able to do so. Conversely, among the households that did not enroll in the scheme, 51.16% were unable to access modern medical posts in the past year. Additionally, the model output indicates that the frequency of visits to a health facility is a significant factor at a 1% significance level. Households that stay with health posts more frequently are more likely to enroll in the CBHI scheme than those that do not visit often. This variable is associated with a 28.08% increase in the probability of enrollment.

Trustworthiness of the Scheme Management

The community’s role in scheme management significantly impacts the household’s enrolment status in the CBHI scheme. The model output in Table 9 also signifies that the trustworthiness of local scheme management is statistically considerable at a 1% significance level, which has about a 40.41% increment in the probability of households’ enrolment decision in the study area. The result shows that if the community participates and is aware of the scheme management, they trust it and play a positive role in increasing enrolment status. This finding is compatible with,43,46 which aims to raise awareness and understanding of the social health insurance program, its benefits, and the enrollment process. This intervention aimed to address the lack of information as a potential barrier to enrollment.

Limitations

Limited Demographic Variation: The study primarily focused on households within a specific demographic, potentially limiting the generalizability of the findings to broader populations.

Scope of Variables: While the study examined various demographic, socioeconomic, and institutional factors, other relevant variables, such as cultural beliefs and perceptions, were omitted, which could have provided further insights into enrollment decisions.

Self-Reported Data: The reliance on self-reported data may introduce biases or inaccuracies, impacting the reliability of the results.

Cross-Sectional Design: The study’s cross-sectional nature limits the ability to establish causality between variables, warranting further longitudinal research to validate the findings.

Contextual Specificity: Findings may be influenced by the specific context of the study area, and caution should be exercised when extrapolating results to different settings or regions.

Conclusions

Demographic factors such as sex, age, and family size significantly influence rural households’ enrollment status in the CBHI scheme.

Socioeconomic variables like education level, yearly income, land ownership extent, and livestock ownership are crucial in determining households’ enrollment status.

Institutional factors significantly impact households’ enrollment decisions, including distance to the nearest health facility, frequency of visiting health facilities, holding official positions, and participation in local meetings.

Variables related to health beliefs, such as the health choice of households and the trustworthiness of scheme management, also affect enrollment.

Education level, trustworthiness of scheme management, frequency of visiting health facilities, official positions held, and participation in local meetings positively influence rural household enrollment status.

Conversely, distance from the nearest health facility and membership in ROSCA negatively impact households’ CBHI enrollment position.

Awareness levels regarding the importance and utilization of health facilities could be better among enrolled and non-enrolled households, indicating a need for improved access and quality of medical facilities to encourage enrollment.

Local gatherings and trust in scheme management significantly increase enrollment rates, highlighting the importance of community involvement and confidence in program administration.

Overall, the study underscores the multifaceted factors influencing households’ enrollment in the CBHI scheme and emphasizes the need for targeted interventions to address barriers and promote enrollment in rural communities.

Recommendations

Prioritize Community Awareness: The government should focus on raising community awareness to increase enrollment in the CBHI scheme. This can be achieved through various activities such as organizing awareness campaigns, promoting community participation in meetings, and expanding access to education, especially adult education. Enhanced Education Initiatives: implement educational programs targeting households with lower levels of education to increase awareness and understanding of the CBHI scheme, thereby encouraging enrollment.

Empower Local Administrations: Local administrations should be empowered to lead and manage CBHI programs effectively, especially at the grassroots level. This includes providing necessary resources and training to local administrators to ensure the successful implementation of the scheme.

Strengthen Community Involvement: Community involvement in scheme management should be strengthened to build trust and increase enrollment rates. This can be done by encouraging the active participation of community members in decision-making processes related to the CBHI scheme. Community Engagement to Foster community engagement through local meetings and gatherings to disseminate information about the CBHI scheme, its benefits, and the enrollment process, thereby increasing trust and participation.

Improve Supply Side: Efforts should be made to improve the supply side of healthcare services to enhance enrollment and retention in the CBHI scheme. This includes ensuring adequate and standardized health facilities within reasonable distances to households. Improved Accessibility Ensure better accessibility to healthcare facilities by reducing the distance between households and the nearest health stations, positively impacting enrollment rates.

Scheme Management Trustworthiness mainly strengthens transparency and accountability in CBHI scheme management to enhance trust among potential enrollees, thus increasing enrollment rates.

Promotion of Official Positions: Encourage households to participate in official positions within local government or cultural structures, as this has been associated with higher enrollment rates, possibly due to increased awareness and advocacy within the community.

By implementing these recommendations, household enrollment in the CBHI scheme is expected to increase, leading to improved access to healthcare services and financial protection for communities in rural areas.

Abbreviations

CBHI, Community-Based Health Insurance; EHIA, Ethiopian Health Insurance Agency; EFY, Ethiopian Fiscal Year; ETB, Ethiopian Birr; FMoH, Federal Minister of Health; GDP, Gross Domestic Product; OOP, Out of Pocket; SSA, Sub-Saharan Africa; USD, United States Dollar; WHO, World Health Organization.

Data Sharing Statement

The data is available from the corresponding author upon request.

Approval of Ethics and Participation Consent

The study was conducted under the Declaration of Helsinki after obtaining ethical clearance from the Central Gondar Health Department (reference number: ማጎጠ 1/19/1952 date 2023-04-26. An information sheet was developed to provide participants with clear information on the research topic, objectives, confidentiality of responses, and study benefits. Verbal consent was obtained from all participants before data collection, as the Ethiopian ethics guideline permitted non-sensitive topics with no risk to participants. Participants were informed of their right to withdraw from the study at any time, and only those who voluntarily agreed to participate were included. The review committee approved the procedure, and confidentiality was maintained by using codes instead of personal identifiers in data collection tools. All paper-based and computer-based data were stored in secure locations and accessed only by the research team. Data sharing will be conducted under ethical and legal rules.

Acknowledgments

The author thanks Dr. Xu Mengmeng for her unreserved support throughout the research process. I am also grateful to the heads and experts of the central Gondar health departments, data collectors, and supervisors for their valuable roles in the success of this study.

Disclosure

The author affirms no conflicts of interest in this work.

References

1. Preker AS, editor. Public Ends, Private Means: Strategic Purchasing of Health Services. World Bank Publications; 2007.

2. Xu K, Evans DB, Carrin G, Aguilar-Rivera AM, Musgrove P, Evans T. Protecting households from catastrophic health spending. Health Affairs. 2007;26(4):972–983. doi:10.1377/hlthaff.26.4.972

3. Muniandy RK, Lansing MG. Implementing urbanization in Malaysian healthcare services. Borneo J Med Sci. 2020;14(2):53. doi:10.51200/bjms.v14i2.1967

4. World Health Organization. editor.. World Health Statistics 2008. World Health Organization; 2008.

5. Chen C, Pan J. The effect of the health poverty alleviation project on financial risk protection for rural residents: evidence from Chishui City, China. Int J Equity Health. 2019;18(1):1–6. doi:10.1186/s12939-019-0982-6

6. WHO. World Health Report: Health Systems Financing: The Path to Universal Coverage. Geneva;2010:15–50.

7. Taddesse G, Atnafu DD, Ketemaw A, Alemu Y. Determinants of enrollment decision in the community-based health insurance, north west Ethiopia: a case-control study. Global Health. 2020;16(1):4. doi:10.1186/s12992-019-0535-1

8. Ibukun OA, Olatona FA, Oridota ES, Okafor IP, Onajole AT. Knowledge and uptake of community-based health insurance scheme among residents of Olowora, Lagos. J Clinical Sci. 2013;10(2):2013.

9. Demissie B, Negeri KG. Effect of community-based health insurance on utilization of outpatient health care services in Southern Ethiopia: a comparative cross-sectional study. Risk Manag Health Policy. 2020;13:141–153. doi:10.2147/RMHP.S215836

10. EHIA CBHI Trend Bulletin. CBHI members’ registration and contribution 2011–2020 G.C; 2020. Available from: http://www.ehia.gov.et/.

11. Ethiopian Health Insurance Agency (EHIA). Evaluation of Community-Based Health Insurance Pilot Schemes in Ethiopia: Final Report. Ethiopia: Addis Ababa; 2020.

12. Amhara region CBHI report. Amhara region community-based health insurance annual report, June 2022, Bahir Dar Ethiopia; 2022.

13. Toleha HN, Bayked EM. Dropout rate and associated factors of community-based health insurance beneficiaries in Ethiopia: a systematic review and meta-analysis. BMC Public Health. 2023;23(1):2425. doi:10.1186/s12889-023-17351-7

14. Preker AS, Scheffler RM, Bassett MC, editors.. Private Voluntary Health Insurance in Development: Friend or Foe? Washington, D.C: The World Bank; 2007.

15. Khan JAM, Ahmed S. Impact of educational intervention on willingness-to-pay for health insurance: a study of informal sector workers in urban Bangladesh. Health Econ Rev. 2013;3(1):12. doi:10.1186/2191-1991-3-12

16. Desai S, Sinha T, Mahal A, Cousens S. Understanding CBHI hospitalization patterns: a comparison of insured and uninsured women in Gujarat, India. BMC Health Serv Res. 2014;14(1):1–4. doi:10.1186/1472-6963-14-320

17. Soors W, Devadasan N, Durairaj V, Criel B Community health insurance and universal coverage: multiple paths, many rivers to cross. AMA; 2010. 39–79.

18. Ortona G, Scacciati F. ”Endowment effect”, status quo bias and contingent valuation. Rivista Intern Di Sci Soc. 2003;2003:397–407.

19. Meeker D, Thompson C, Strylewicz G, Knight TK, Doctor JN. Use of insurance against a small loss as an incentive strategy. Decision Analy. 2015;12(3):122–129. doi:10.1287/deca.2015.0314

20. Kahneman D, Tversky A. Prospect theory: an analysis of decision under risk. Econometrica. 1979;47(2):263–292. doi:10.2307/1914185

21. Kunreuther H, Pauly M. Insurance Decision-Making and Market Behavior. Hanover, MA: Now Publishers; 2006.

22. Mekonen KD, Tedla WT. Paradoxical consequences of CBHI scheme in rural Ethiopia: enrollees’ perceived preferential treatment to paying clients and concomitant problems. Cogent Soc Sci. 2022;8(1):2057635. doi:10.1080/23311886.2022.2057635

23. Glassman A, Giedion U, Smith PC. The health benefits package: bringing universal health coverage from rhetoric to reality. In: Glassman A, Giedion U, Smith PC, editors. What’s in, What’s Out? Designing Benefits for Universal Health Coverage. Washington, DC: Center for Global Development; 2017.1.

24. Hailu A, Eregata GT, Stenberg K, Norheim OF. Is universal health coverage affordable? Estimated costs and fiscal space analysis for the Ethiopian essential health services package. Health Syst Reform. 2021;7(1). doi:10.1080/23288604.2020.1870061

25. Kiros M, Dessie E, Jbaily A, et al. The burden of household out-of-pocket health expenditures in Ethiopia: estimates from a nationally representative survey. Health Policy Plann. 2020;35(8):1003–1010. doi:10.1093/heapol/czaa044

26. David B, Evans GC Distribution of health payments and catastrophic expenditures Methodology. FER/EIP discuss. Pap; 2005. Available from: http://whqlibdoc.who.int/hq/2005/EIP_HSF_DP_05.2.pdf.

27. Mekuria GA, Ali EE. The financial burden of out-of-pocket payments on medicines among households in Ethiopia: analysis of trends and contributing factors. BMC Public Health. 2023;23(1):1–12. doi:10.1186/s12889-023-15751-3

28. Yitayal M, Berhane Y, Worku A. Health care financing in Ethiopia: implications on access and utilization of health services. Ethiop J Health Dev. 2019;33(1):3–8.

29. Gebreegziabher E, Kebede A, Gebrehiwot T, Grierson PF. The impact of community-based health insurance on out-of-pocket payments in Ethiopia: evidence from a longitudinal study. PLoS One. 2021;16(4):e0249959. doi:10.1371/journal.pone.0249959

30. Champion VL, Skinner CS. The health belief model. In: Glanz K, Rimer BK, Viswanath K, editors. Health Behavior and Health Education: Theory, Research, and Practice.

31. Rosenstock IM. The health belief model and preventive health behavior. Health Educ Monogr. 1974;2(4):354–386. doi:10.1177/109019817400200405

32. Rosenstock IM, Strecher VJ, Becker MH. The health belief model and hiv risk behavior change. In: Peterson J, DiClemente R, editors. Preventing AIDS: Theory and Practice of Behavioral Interventions. New York: Plenum; 1994.1.

33. Panda P, Dror I, Koehlmoos TP, et al. What Factors Affect Uptake of Voluntary and Community-Based Health Insurance Schemes in Low- and Middle-Income Countries? A Systematic Review by EPPI-Centre. Social Science Research Unit, Institute of Education, University of London;2024.

34. Acharya D, Devkota B, Kreps GL. Does perceived susceptibility and severity of health problems drive household enrolment in health insurance? A case study from Nepal. Int J Health Plann Manag. 2022;37(2):839–853. doi:10.1002/hpm.3377

35. Merga BT, Balis B, Bekele H, et al. Health insurance coverage in Ethiopia: financial protection in the Era of sustainable development goals (SDGs). Health Econ Rev. 2022;12(1):43. doi:10.1186/s13561-022-00389-5

36. Adam AM. Sample size determination in survey research. J Sci Res Rep. 2020;26(5):90–97. doi:10.9734/jsrr/2020/v26i530263

37. Yamane T. Statistics: An Introductory Analysis.

38. Gujarati DN. Basic Econometrics.

39. Wilson JR, Lorenz KA. Standard binary logistic regression model. In: Modeling Binary Correlated Responses Using SAS, SPSS and R. ICSA Book Series in Statistics. Vol. 9. Cham: Springer; 2015. 1. doi:10.1007/978-3-319-23805-0_3

40. Njuki J, Poole J, Johnson N, et al. Gender, Livestock and Livelihood Indicators. Nairobi, Kenya: International Livestock Research Institute; 2011.

41. EHIA. Evaluation of Community-Based Health Insurance Pilot Schemes in Ethiopia: Final Report. Ethiopia: Addis Ababa; 2015.

42. Hounton S, Byass P, Kouyate B. Assessing the effectiveness of community-based health insurance in rural Burkina Faso. BMC Health Serv Res. 2012;12(1):1–9.

43. Basaza R, Criel B, Van der Stuyft P. Low enrolment in Ugandan Community Health Insurance Schemes: underlying causes and policy implications. BMC Health Serv Res. 2007;7:1–12. doi:10.1186/1472-6963-7-105

44. Yinges Yitayew M, Hussien Adem M, Tibebu NS; Nigusie Selomon Tibebu. Willingness to enroll for community-based health insurance and associated factors in Simada District, north-west, Ethiopia, 2020: a community-based cross-sectional study. Risk Manag Healthcare Pol. 2020;13:3031–3038. doi:10.2147/RMHP.S280685

45. Hong W, Nancy P. Community-based health insurance: an evolutionary approach to achieving universal coverage in low-income countries. J Life Sci. 2012;6:320–329.

46. Capuno JJ, Kraft AD, Quimbo S, Cr T Jr, Wagstaff A. Effects of price, information, and transactions cost interventions to raise voluntary enrollment in a social health insurance scheme: a randomized experiment in the Philippines. Health Eco. 2016;25(6):650–662.

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2024 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.