")

Back to Journals » Risk Management and Healthcare Policy » Volume 12

Willingness to pay for Community Health Insurance among taxi drivers in Kampala City, Uganda: a contingent evaluation

Authors Basaza R, Kyasiimire EP, Namyalo PK, Kawooya A , Nnamulondo P, Alier KP

Received 22 August 2018

Accepted for publication 7 June 2019

Published 19 July 2019 Volume 2019:12 Pages 133—143

DOI https://doi.org/10.2147/RMHP.S184872

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Kent Rondeau

Robert Basaza,1,2,* Elizabeth P Kyasiimire,1,2,* Prossy K Namyalo,3 Angela Kawooya,4 Proscovia Nnamulondo,5 Kon Paul Alier6

1College of Medicine, Health and Life Science, St. Augustine International University, Kampala, Uganda; 2School of Public Health and Management, International Health Sciences University, Kampala, Uganda; 3Department of Social Sciences, Ndejje University, Kampala, Uganda; 4School of Public Health and Management, Clarke International University, Kampala, Uganda; 5College of Social Sciences, Makerere University, Kampala, Uganda; 6South Sudan Institute of Pharmacy Technicians, Juba, South Sudan

*These authors contributed equally to this work

Background: Community Health Insurance (CHI) schemes have improved the utilization of health services by reducing out-of-pocket payments (OOP). This study assessed income quintiles for taxi drivers and the minimum amount of premium a driver would be willing to pay for a CHI scheme in Kampala City, Uganda.

Methods: A cross-sectional study design using contingent evaluation was employed to gather primary data on willingness to pay (WTP). The respondents were 312 randomly and 9 purposively selected key informants. Qualitative data were analyzed using conceptual content analysis while quantitative data were analyzed using MS Excel 2016 to generate the relationship of socio-demographic variables and WTP.

Results: Close to a half (47.9%) of the respondents earn above UGX 500,000 per month (fifth quintile), followed by 24.5% earning a monthly average of UGX 300,001–500,000 and the rest (27.5%) earn less. Households in the fourth and fifth quintiles (38.4% and 20%, respectively) are more willing to join and pay for CHI. A majority of the respondents (29.9%) are willing to pay UGX, 6,001–10,000 while 22.3% are willing to pay between UGX 11,001 and UGX 20,000 and 23.2% reported willing to pay between UGX 20,001 and UGX 50,000 per person per month. Only 18.8% of the respondents recorded WTP at least UGX 5,000 and 5.8% reported being able to pay above UGX 50,000 per month (1 USD=UGX 3,500). Reasons expressed for WTP included perceived benefits such as development of health care infrastructure, risk protection, and reduced household expenditures. Reasons for not willing to pay included corruption, mistrust, inadequate information about the scheme, and low involvement of the members.

Conclusion: There is a possibility of embracing the scheme by the taxi drivers and the rest of the informal sector of Uganda if the health sector creates adequate awareness.

Keywords: Community Health Insurance, informal sector, willingness to pay, contingent valuation, Uganda

Background

Community Health Insurance and the health system

Health is a fundamental human right whose realization requires the active participation of the various stakeholders.1 However, gross inequalities within society hinder sections of people from accessing the needed health care, and this reality further impedes the countries’ attainment of universal health coverage.1 Health insurance refers to an arrangement of pooling resources so that risks are shared among different contributing individuals.2 One form of health insurance schemes is Community Health Insurance (CHI). The CHI schemes (CHIS) are run on a not-for-profit basis and mainly target the informal sector. They apply the basic principles of risk-sharing, pooling resources, and members’ participation in management.3,4 CHIS are voluntary, community-based, and initiated to improve health of the informal sector and protect them from health-related crisis by increasing their access to health services.5 Consequently, CHIS have improved the utilization of health services by reducing OOP payments, as people do not first look for money before seeking healthcare.4,5

Reviewing health systems financing is a key concern that has attracted the attention of global policy makers. The World Health Assembly resolution 58.33 of 2005 points out that everyone should be able to access health services and not subject to financial hardship in doing so.6 Unfortunately, when people from developing countries use health services, they often incur high, sometimes catastrophic costs in paying for their health care. However, evidence shows that developing countries account for 84% of the world’s population and 90% of the global disease burden but only account for 12% of the global health spending. Of the 12% global health spending by developing countries, the share of low-income countries including those in sub-Saharan Africa is only 2%. Africa accounts for 25% of the global disease burden and less than 1% of global health spending with only 2% of the global health workforce.6,7

In some countries, a mix of social health insurance-the Bismarck Model, as well as the private commercial health insurance and community-based insurance schemes is used to achieve citizen’s social health protection. Globally, the mean willingness to pay (WTP) for health insurance among the low and middle-income countries is estimated at 1.18% of the Gross Domestic Product (GDP) per capita and 1.39% of the adjusted net national income per capita. Traditionally, values in Africa such as the “brother’s keeper” were based on solidarity within families, clans, and the community for social protection including health care.8

Financing of health services in Uganda

The government of Uganda is aiming at achieving equal access to essential health care services for its population, with a focus on improving the country’s health financing systems.5,7 Currently, Uganda’s health financing system is designed to meet the Uganda National Minimum Healthcare Package. The per capita spending on health was USD 51 in 2016, which is low compared to WHO recommended minimum level of USD 84. In addition, the current health expenditure as a percentage of GDP is as low as 1.4%, against the target of 5%.9 The primary sources of health care financing are households (41.7%), donors (45%), and Government (15.3%), while private insurance constitutes a small proportion of current health expenditure (3%). Moreover, 41.7% contributed by households is majorly out-of-pocket which is far above the recommended maximum of 20% household expenditure by WHO if they are not to be pushed into impoverishment. That notwithstanding, out-of-pocket expenditure remains the major health care financing mechanism in Uganda despite the abolition of user fees in government facilities.7–10 Consequently, allocations to health in the total government budget have stagnated at around 7–8% for the last 10 years. Households, therefore, contributed 96% of the private funds to the current health expenditure in 2016. Accordingly, such levels of OOP payments suggest that healthcare financing is less equitable, leading to high chances of catastrophic expenditure on households.11

To step up new health care financing sources, the Ugandan Ministry of Health (MOH) initiated CHIS in 1995 in an effort to address the ill effects of OOP spending on health care.2 Assessments of the schemes show that membership improves overall quality of life in relation to members’ health and ability to cope with health care costs.3 Despite earmarking CHI as a health care financing mechanism in the current second National Health Policy and the Health Sector Development Plan, the number of health insurance schemes and the persons covered have remained small and confined to one part of the country.3 The schemes currently only cover about 10% of the targeted population in their localities. There are 23 CHIS covering 150,000 in the 11 districts of western and central Uganda.11 Private commercial health insurance exists only on a very small scale covering 1.2% of the country’s population and caters only for the wealthy families and individuals. Uganda’s health sector takes CHI as a better option for the informal sector since it gives room for community participation and has relatively affordable premiums compared to commercial health insurance schemes.8,13

The proposed National Health Insurance Scheme Policy

National Health Insurance Scheme (NHIS) refers to a system of health insurance that covers a national population against the costs of health care.20 The Government of Uganda, through the Ministry of Health, is planning to introduce the NHIS for all residents. The Scheme will subsequently be composed of three sub-schemes including Social Health Insurance, CHI, and the Private Commercial Health Insurance (PCHI), which shall be implemented concurrently. The CBHI will mainly comprise the informal sector while the PCHI will complement the health insurance services.8,9

Objectives

This study’s main objective was to assess the WTP a premium for CHI among the Kampala City taxi drivers. Specifically, we looked at the income quintile levels for the taxi drivers and the minimum amount of premium a driver would be willing to pay in a CHIS in Kampala City. Such information is useful in early planning stages of the proposed NHIS where CHI is one of the components. This study-generated information that is useful in planning, designing, and promoting a CHIS for the informal sector and taxi drivers in Kampala City in particular.

Methods

The respondents and study area

Respondents were taxi drivers who operate informal minibus businesses that dominate the public urban transport services. The Operators introduced 14-seater commuter taxis to serve Kampala City and its environs following the disappearance of large-bus services in Ugandan cities. Taxis form the biggest part of the public transport means in Kampala and Uganda as a whole. Kampala Capital City Authority (KCCA) estimated that about 1,200 public taxis operate within Kampala City.12,13 As such, the estimated beneficiaries of the taxi operators are 6,000 people taking into account the average household size of 5 people.14

Study design and variables

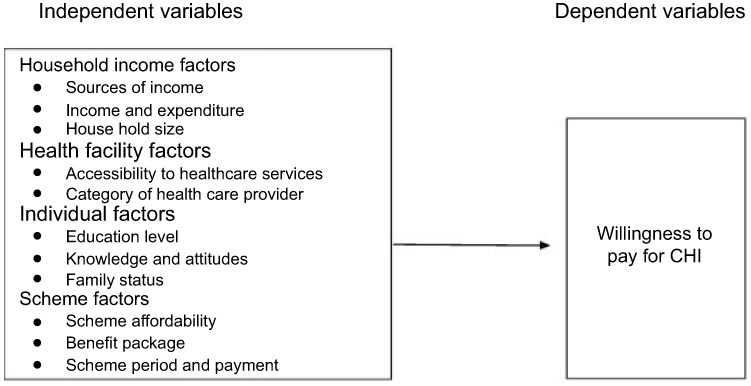

A cross-sectional design using contingent evaluation similar to the one used in a study on WTP for National Health Insurance Fund among public servants in South Sudan was used.18 Primary data were collected on WTP from randomly selected respondents. WTP for CHI was the dependent variable in this study; the independent variables were social-economic characteristics of respondents such as income quintile factors. The other independent variables included age, sex, marital status, family size, education, individual income level, alternative source of income, and household level of expenditure. Additional independent variables were health system factors, namely, frequency of health facility visits and category of health care provider (Figure 1).

|

Figure 1 Conceptual framework. Abbreviation: CHI, Community Health Insurance. |

The stated preferences for respondents to select from were willingness to contribute to the scheme a monthly premium per person of UGX: (i) below 5,000, (ii) 5,001 to 10,000, (iii) 10,001 to 20,000, (iv) 20,001 to 50,000 and (v) above 50,000. Also another stated preference was how often would respondents be willing to contribute to the scheme: (i) daily, (ii) weekly, (iii) monthly, and (iv) bi-monthly.

Sampling: The sample size n was determined using Slovin’s (1960) formula:

for a known population; n is the sample size to be determined, N is the population size 1,200 and e is the level of precision (0.05). Subsequently, the research team adjusted the obtained sample size (300) to cater for an estimated 30 (10%) non-response thus a total population size (N) of 330 for this study. The team assigned all the taxi drivers unique numbers and subsequently carried out random selection to obtain a study sample. Only taxi drivers above the age of 18 years who consented were interviewed using questionnaires administered by the researchers. The team also interviewed nine purposively selected key informants working in the Ministry of Health, KCCA, and Kampala Operational Taxi Stages Association (KOTSA) leadership in January 2018. The interviewers used English and the local language (Luganda); all the drivers could at least speak and understand either or all of the two languages used. Nine key informants were purposively selected: 2 stage managers, 2 KOTSA leaders, 2 KCCA officials, 2 MOH Officials, and 1 Health Insurance Service Provider. The team carried out key informant interviews until saturation point that is until no additional data were being found.

for a known population; n is the sample size to be determined, N is the population size 1,200 and e is the level of precision (0.05). Subsequently, the research team adjusted the obtained sample size (300) to cater for an estimated 30 (10%) non-response thus a total population size (N) of 330 for this study. The team assigned all the taxi drivers unique numbers and subsequently carried out random selection to obtain a study sample. Only taxi drivers above the age of 18 years who consented were interviewed using questionnaires administered by the researchers. The team also interviewed nine purposively selected key informants working in the Ministry of Health, KCCA, and Kampala Operational Taxi Stages Association (KOTSA) leadership in January 2018. The interviewers used English and the local language (Luganda); all the drivers could at least speak and understand either or all of the two languages used. Nine key informants were purposively selected: 2 stage managers, 2 KOTSA leaders, 2 KCCA officials, 2 MOH Officials, and 1 Health Insurance Service Provider. The team carried out key informant interviews until saturation point that is until no additional data were being found.

Data analysis

Qualitative data were analyzed using conceptual content analysis and reported in quotations in appropriate sections of the results while quantitative data were entered and analyzed using MS Excel 2016 to generate relationship of socio-demographic variables and WTP.

The team pretested questionnaires with 12 respondents who were not part of the study sample. In addition, only Research Assistants experienced in data collection and fluent in written and spoken English and Luganda languages as well as having knowledge of taxi operations were selected and trained to aid data collection. One of the authors (KEP) closely supervised the entire process of data collection in order to respond to queries and ensured that the process maintained quality.

Ethics

We obtained ethical approval to conduct this study from the International Health Sciences University Faculty Research Committee. For confidentiality, the team did not write the respondents’ names on the questionnaires. In addition, the research team assured respondents of non-disclosure of the source of the information provided throughout the process of this study. Consequently, the research team sought informed consent from all respondents before data collection. Ordinarily, responses were obtained without influence from colleagues, leaders, or data collectors. The team have presented results in graphical, tabular, and narrative forms.

Results

Socio-demographic characteristics of respondents

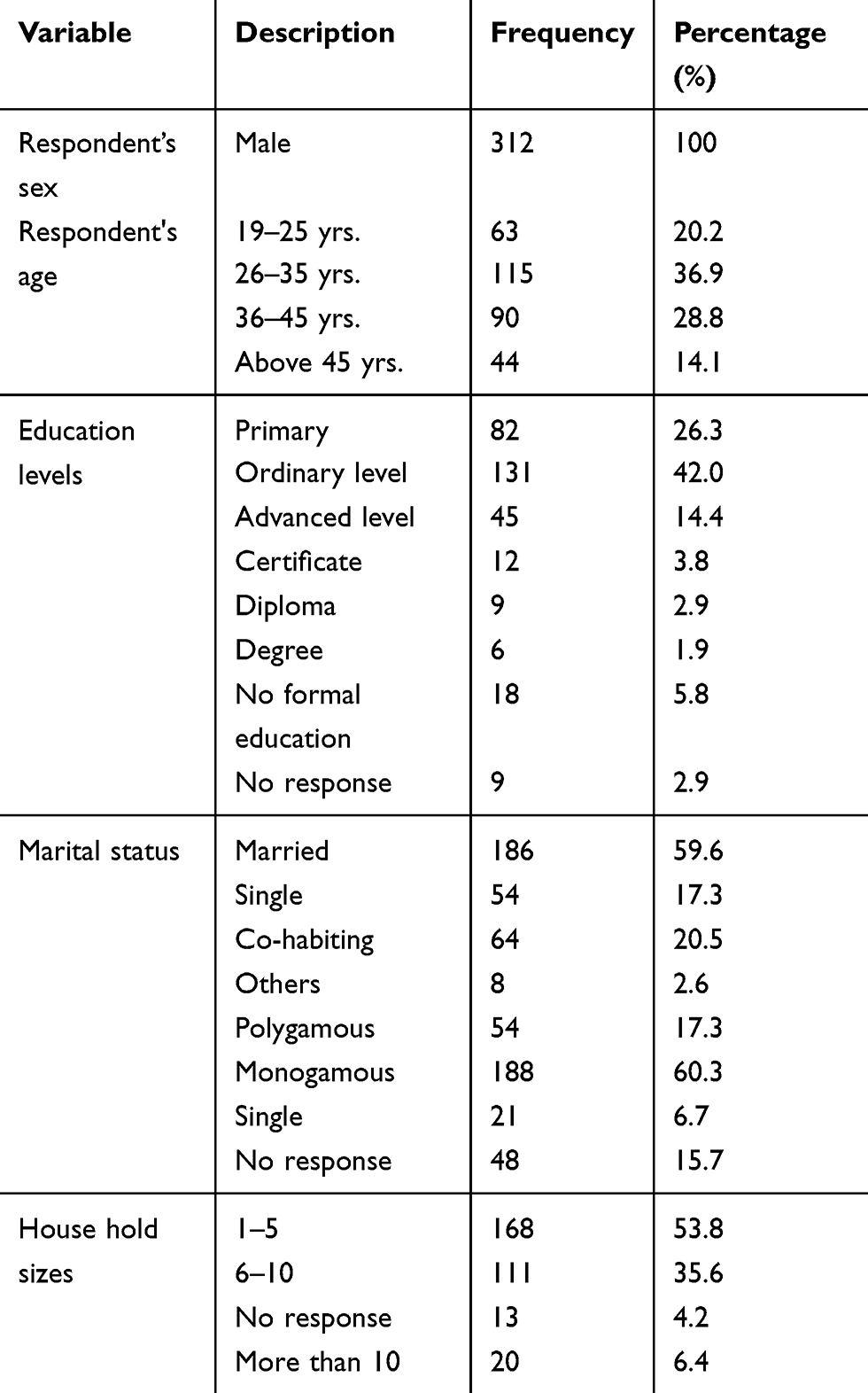

The Research Team achieved a response rate of 94.5% (312 respondents). Over a third of the respondents 115 (36.9%) were in the age group 26–35 years, less than a third 90 (28.8%) were aged between 36 and 45, and 63 (20%) in the youngest age group, 18–25 years (Table 1). Conversely, a minority of the respondents (14.1%) were older than 45 years. All respondents (100%) were male. A majority of the respondents (60.3%) said they were in monogamous marriages followed by the singles (17.3%) while the minority (6.7%) reported being polygamous. The respondents who did not disclose their marital status were 15.7%.

|

Table 1 Social demographic characteristics of respondents (N=312) |

In regard to household sizes, categorization was into 1–5, 6–10, and more than 10 in line with the country’s statistical practice of classification of family size was used. The modal household size (53.8%) consisted of 1−5 members, and this was closely followed by households of 6–10 members (35.6%) and the rest of family sizes form the remaining percentage. Most of the respondents 131 (42%) were found to have only covered 8−13 years of education (Ordinary level), which is equivalent to 11 years of formal education. This was followed by those who had covered only up to 7 years of education (primary) (26.3%). Only 14.4% had attained 12–13 years of education (Advanced level) and only 8.6% had attained more than 13 years of education (tertiary training). Only 5.8% were reported not to have attained any formal education.

WTP a premium for CHIS

The respondents were asked about their WTP a premium into a CHIS and answered thus: close to four-fifths 240 (77.9%) welcomed the CHI idea while 65 (22.1%) were not interested to pay a premium into the scheme.

Reasons for WTP for CHI

Respondents who indicated WTP a premium into the CHI scheme reported expecting some benefits from the scheme such as convenience and accessibility to affordable health care services as expressed by one of the taxi drivers “I will be sure to find medicines at a nearby facility”. Another taxi driver said “It means I will pay small amounts of money slowly; this does not break me down”. Those who were not willing to pay said they had less trust in the scheme, “those people might not cover all sicknesses especially the long term effects of driving”. Another respondent said: “they might give us Health facilities far from our residences which may not be easy to access”. Other reasons for not willing to enrol into CHI included little understanding of the scheme dynamics and preference for individual cover to group cover, one of the respondents was quoted: “I may pay my full portion and another one fails to pay yet they can get treatment; aaaha, let them start, I will join later if I see how they benefit”.

CHI and monthly income quintiles

The monthly income quintiles based on the monthly incomes reported by the Kampala taxi drivers are presented in Table 2.

|

Table 2 The WTP for community health insurance and income quintiles |

The study results indicate that close to a half (47.9%) of the respondents earn above UGX 500,000 per month (5th quintile), followed by about a quarter (24.6%) earning a monthly average of UGX 300,001–500,000 and close to a fifth (18.7%) earn UGX 200,001–300,000. Only 1.6% reported earning less than UGX 100,000. The results also indicate that households in the 4th and 5th quintiles are more willing to join and pay for CHI compared to the lower quintiles, 117 (38.4%) and 61 (20%), respectively. Nevertheless, 29 (9.5%) of the 5th quintile households are not willing to pay for the CHIS.

Average household expenditure on basic needs

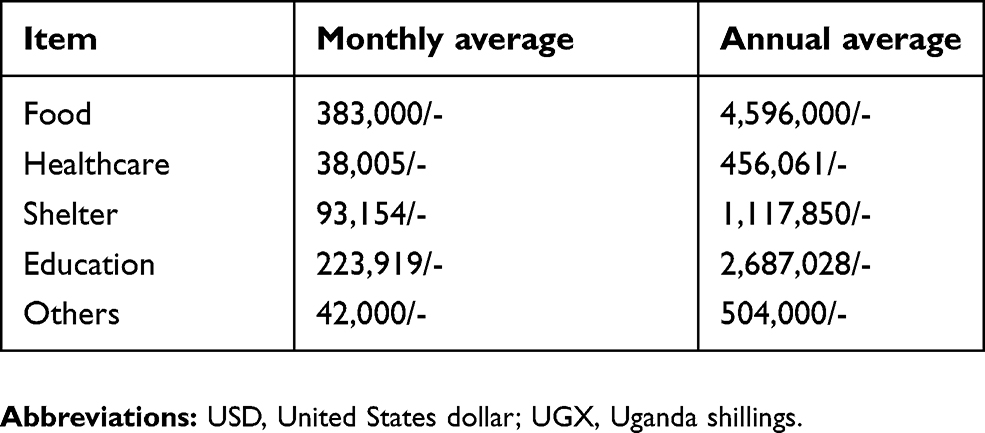

The survey collected information on average household expenditures on basic needs (Table 3).

|

Table 3 Respondent’s household monthly and annual average expenditure on basic needs in UGX |

The average monthly household expenditure on food is UGX 383,000 followed by education at UGX 223,900. Shelter monthly expenditure among the respondents’ households was reported at UGX 93,154 as compared to health care expenditure reported at averagely UGX 38,005.

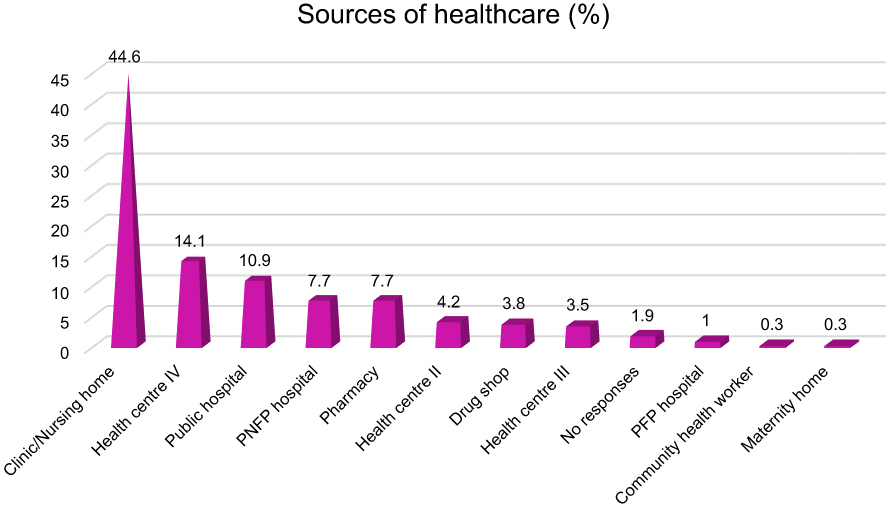

Common source of medical treatment for the households

The study respondents provided information about where their household members seek treatment when they fall sick. The results are in Figure 2.

|

Figure 2 Households health care sources.Abbreviation: WTP, willingness to pay. |

Close to a half of the respondents139 (44.6%) reported accessing health care with their families from private clinics; followed by more than a tenth 44 (14.1%) that get services from health center IVs (both government and private) and close to a tenth 34 (10.9%) from public government hospitals. Results also indicate that 24 (7.7%) of the respondents received health care services from private not for profit hospitals and the same proportion from pharmacies. Very few (0.3%) of the respondents’ households sought health care from maternity homes and community health workers within their areas. Non-governmental health service providers are more preferred to provide healthcare compared to the government health centers such as health centers IV, III, and II. One taxi driver was quoted as saying, “Church hospitals pay much attention and follow up on patients because it`s the religious people that listen much,” while another taxi driver remarked “I prefer private hospitals because they always have medicines”.

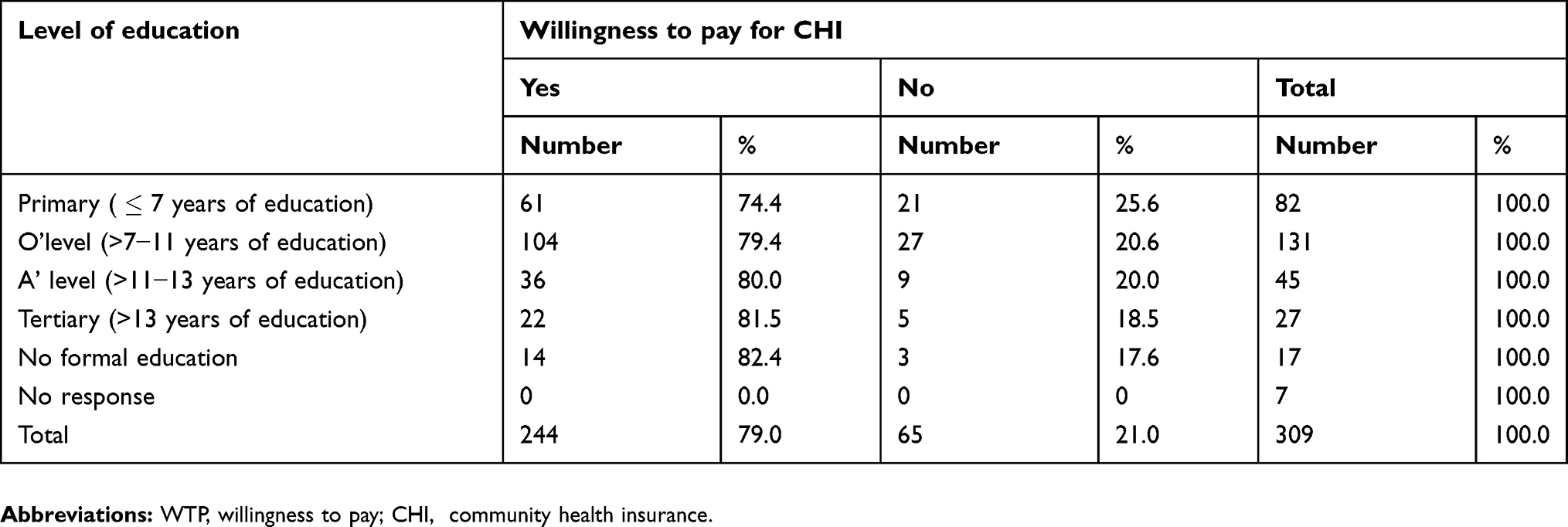

Relationship between WTP for CHI and level of education

The relationship between WTP for CHI and levels of education is presented in Table 4.

|

Table 4 Relationship between level of education and WTP for CHI |

The survey results indicate that respondents who had attained any kind of formal education (82.4%) were more willing to pay for CHI than those who had attained no formal education. However, our results further established that for respondents who had attained formal education, WTP correlated with the levels of education; thus, the higher the level of education the more the WTP for CHI. Over four-fifths (81.5%) of those who had attained tertiary education were willing to pay followed by 80% of those who had attended Advanced level and 79.4% of those who had attended up to ordinary level. Only 74.4% of those who had attended primary school were willing to pay for CHI.

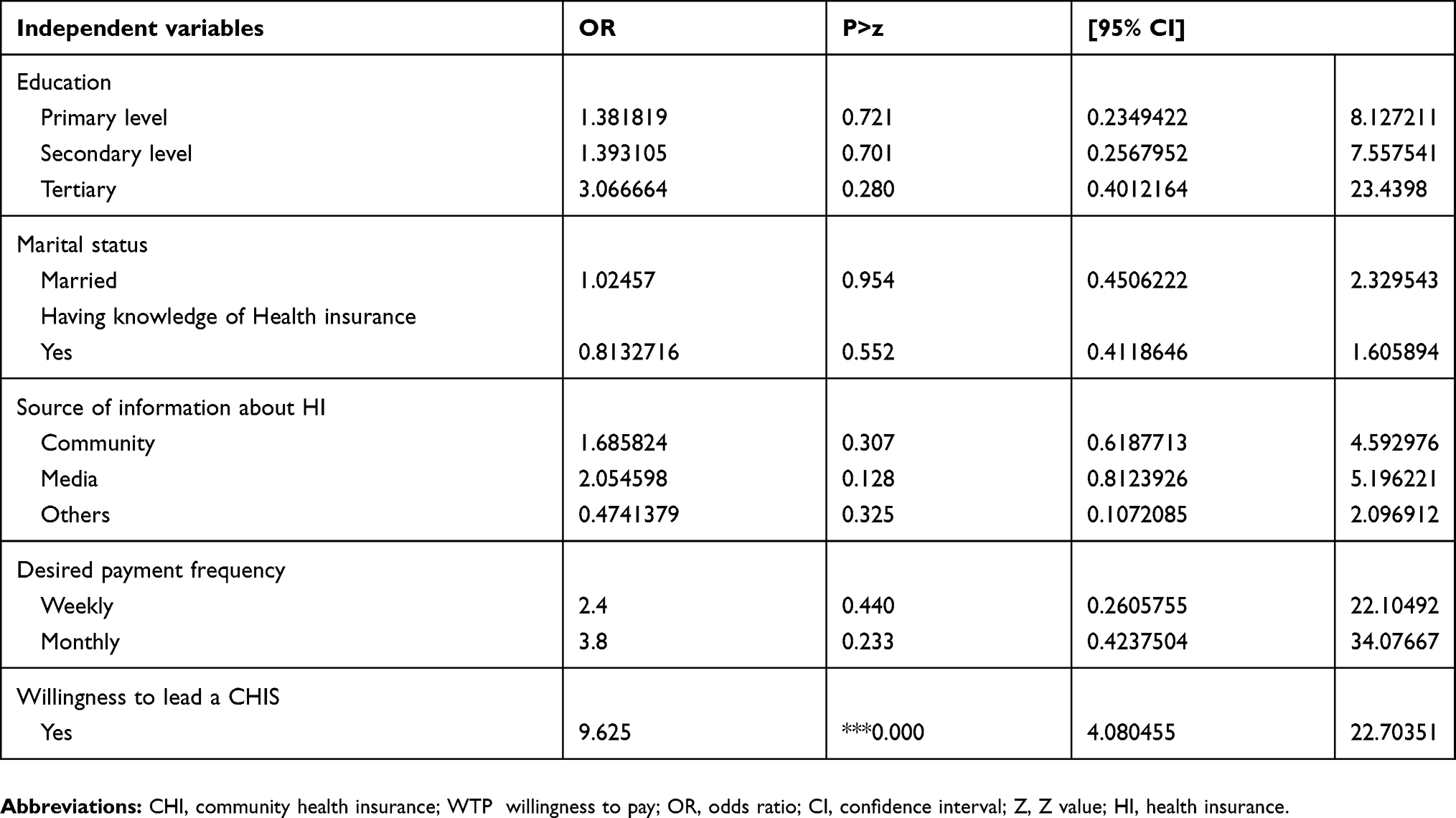

A logistic regression model was used to determine the relationship between the dependent and independent variables of WTP (Table 5).

|

Table 5 Regression analysis for WTP |

A significant relationship was realized between WTP and respondent’s willingness to take part in scheme leadership.

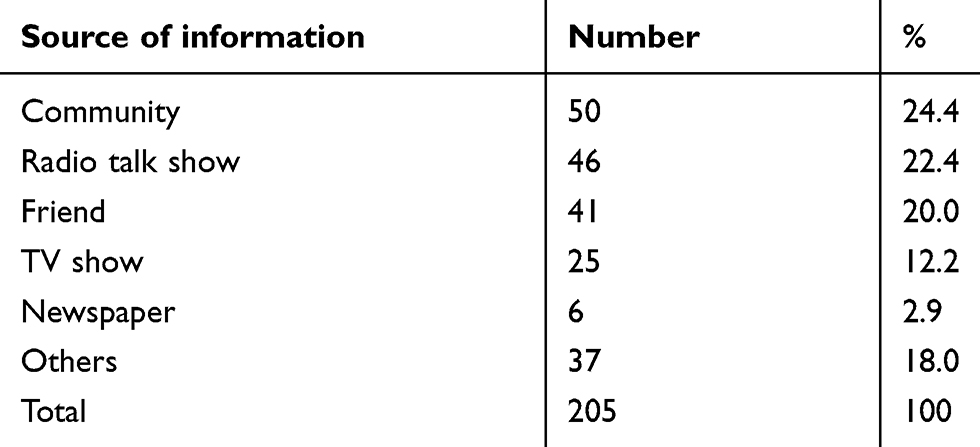

Awareness of CHI

Slightly over a half of the respondents (66.0%) indicated having an idea about health insurance schemes and 34.0% knew nothing about it. Interestingly, the most common sources of information were the media: radio, newspapers, and TV shows (37.5%). The other reported sources of information included community meetings (24.4%), friends (20.0%), school gatherings, and health workers (17.5%) (Table 6). To clearly appreciate respondent’s understanding of CHI, taxi drivers were asked to explain the concept in their own understanding. Only 56% of the respondents who reported having heard about CHI were in a position to give relevant information about health insurance such as voluntary enrolment and renewal, pooling funds, and member involvement in scheme leadership, among others. Although the media seem to have been instrumental in disseminating health insurance information, it may have not clarified the scheme concepts thus taxi drivers who had no or little time for the media had limited knowledge about the health insurance concept:

|

Table 6 Source of information about health insurance |

“It seems to be a very good idea but we lack information, so when are you coming to teach us?” (taxi driver, New Taxi Park). Another driver expressed concern for often failing to access information “We rarely get to know such information; so how can I follow up because I am so interested?” (taxi driver, Nakawa Taxi Park). “I did not know about this, I don't want to miss, please register me.” (taxi driver, Old Taxi Park). Although taxi drivers do not always access information, they acknowledge support of their leadership to get information “Please go to the office and the stage managers will call for a meeting; we want to learn.” (taxi driver, Nakawa Taxi Park).

Some of the key informants pointed out that some taxi drivers have embraced lots of changes when they are well sensitized. “They only need to be sensitized, but I believe they will embrace it,” (KOTSA Official). In addition, another key informant who is a city official mentioned that taxi drivers only lack information and mobilization to join the schemes, “Sometimes they contribute funds for their colleagues to seek medical help”. More so, some of the taxi drivers were able to relate CHI to the Motor Third Party Insurance. “Aaaahh, for us we are used, if we pay for the vehicles what about life!” (taxi driver,Old Taxi Park). This indicates that the drivers may support group enrolment into CHI.

Minimum amount of premium taxi drivers are willing to pay for CHI

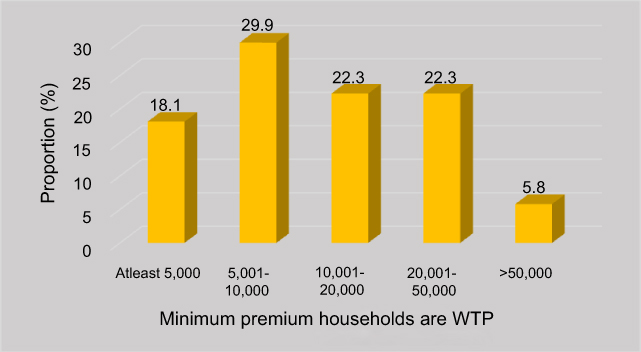

This survey further sought how much one would be willing to contribute to the scheme from respondents who reported WTP for CHIS. The findings are as presented in Figure 3.

|

Figure 3 Minimum premium households are WTP monthly. Abbreviations: WTP, willingness to pay; PFP, private for profit. |

A majority of the respondents (29.9%) were willing to pay between UGX 5,001 and UGX 10,000 per month while 50 (22.3%) were willing to pay between UGX 10,001 and UGX 20,000 and 52 (23.2%) reported WTP between UGX 20,001 and UGX 50,000. Conversely, only 42 (18.8%) of the respondents reported to be able to pay at least UGX 5,000 and 13 (5.8%) reported being able to pay above UGX 50,000 per month. “I can only determine how much to contribute when I am aware of the scheme benefits package.” (taxi driver, New Taxi Park).

Discussion

Factors influencing WTP for CHIS

The preference is mostly to have their family members covered since they themselves rarely get sick. Reasons expressed for WTP included perceived benefits such as development of health care infrastructure, risk protection, and reduced household expenditures. Reasons for not willing to pay include corruption and mistrust in the scheme, inadequate information about the scheme, and low involvement of the members. Accordingly, there is a possibility of embracing the scheme by the informal sector of Uganda if adequate awareness is built.

A majority of respondents (79%) who expressed WTP for CHI indicated that they rarely seek medical attention themselves but rather their other family members. “I don’t remember when I last sought treatment! But it will help my family since children get sick quite often,” taxi driver at old Taxi Park. This is associated with most of the respondents being young; 26–35 years (36.9%) and meeting the health care costs of their spouses and children. This relates to a study done in Ghana which shows that 22.6% of the uninsured and 37% of the partially insured households attributed their lack of insurance to family members not falling sick so as to require health care.15

The respondents’ incomes have a big influence on WTP. Respondents in the 4th and 5th quintiles (58%) were more willing to join CHI as compared to the lower quintiles (20%). This is attributed to a relatively higher income that meets most of their household costs. This concurs with the study done in Europe, which showed that as household incomes increased so did the health insurance coverage.16 A study in Nigeria revealed that the WTP for a CHIS was affected by a number of factors including household incomes. Wealthier households were willing to pay for the CHIS compared to others.17 Subsequently, Bawa and Jehu noted that when the price of CHI premiums is perceived to be high, the odds of enrolling decreases by 0.8.15 The same study also revealed that respondent’s levels of education and confidence in the availed schemes influenced WTP: the higher the level of education the more WTP.

Awareness about CHI

During this study, it was realized that awareness is key to enrolment into CHI because health insurance is a new phenomenon in Uganda with the first schemes launched in 2005.2 This is in line with the study by Basaza et al in South Sudan, who also found out that awareness is a significant factor that influences WTP for health insurance.18 Similarly, Biosca and Brown found out in their study on boosting health insurance in developing countries and stressing the effect on conditional transfers in Mexico that WTP for CHIS increased expressively with awareness creation.19 However, this was different from the study carried out by Bawa and Ruchita in Punjab India where 71% of the respondents reported being aware but were not subscribed to health insurance.15 A study done in Ethiopia also revealed that it requires intensive awareness creation and trust building programs in the community, particularly for those who do not have formal education, and those not insured before. The same study also found out that rural households who were aware about the basic concepts of CHI program were more willing than those not aware. Respondents with enough awareness had $0.96 more WTP than those not aware.20 This is consistent with the finding in rural Nigeria by Ayobami et al (2017) where only 21.1% of those aware about health insurance were enrolled in at least one insurance scheme.

One of the hindrances to joining the CHIS was lack of or minimum knowledge about operations of such schemes. Indeed, it is difficult for the communities to join health insurance without any prior briefing about the schemes. This relates to a study by Roth et al cited by Sayem which found that lack of knowledge about the importance of health insurance was a key determinant of health insurance product uptake. From a consumer’s perspective, enrolment options and procedures were also found to influence the adoption of CHI.19

There is a high level of scheme misuse from both the provider and beneficiaries; one respondent had this to say: “The beneficiaries can cover their relatives disguising as themselves and some doctors do only mind what they get at the end. Penalizing the culprits from both sides can help to curb down the vice.” Creating a regulatory and tracking tool amongst the insurers would help to address this. “This is because each insurer has a different person attending to their clients in one place yet one person could do it for a number of insurers in a particular place,” MOH Official.

Premium for CHIS

In CHIS, premiums are mostly charged basing on the number of enrolled household members. Apparently, the study findings show that over two-thirds of the city taxi drivers are willing to pay for CHIS. Over one-fifth (23.2%) of the respondents were willing to pay at least UGX 20,000 (USD 6.6) per month per household, which translates into USD 1.32 per individual per month. This proposed premium is within their income bracket and thus affordable. In another study carried out in Iran, it was noted that the average amount potential beneficiaries were WTP for social health insurance per person per month was USD 5.5.16 On the contrary, another study by Gustafsson-Wright in Namibia found that uninsured individuals in the Greater Windhoek Area of Namibia were willing to pay a higher premium than in our research findings: 47.50 NAD (USD 6.60) per month per individual for health insurance as compared to our finding of USD 1.32 per month per individual.19 Further still, another study done in Ethiopia established that the average premium Ethiopians were willing to pay was USD 0.64 (USD 7.7 per annum) per household per month which is lower than the amount in our study. Interestingly, this amount in the Ethiopian study was higher than the USD 0.43 monthly (annual USD 5.25) premium value designed for the households’ pilot study which catered for enrolment of up to five family members.21 Thus, the amount of premium people are willing to pay varies across countries and possibly the benefits provided by the scheme.

Study limitations

Most of the respondents would be looking forward to taking the next slots and loading vehicles for the subsequent routes. This yielded divided attention from the respondents. Nevertheless, the research team was very patient and were even always willing to return the next day and engage the respondents during the time when traffic was light.

Conclusion

The study findings give an insight about the factors likely to influence WTP for CHI among Uganda`s urban informal sector and specifically those involved in the public transport business. Highly considerable ones included awareness, level of household income, and scheme benefits. These findings may also be useful in other countries with similar settings considering design of CHI and a National Health Insurance Scheme.

Study recommendations

Arising from this study, we do make the following recommendations:

- The Ugandan Health Sector could carry out mass sensitization on CHI among the informal sector operators across the country to increase enrolment into CHIS. Consequently, this would be a platform to promote member ownership of the health insurance schemes thereby improving accessibility of health services within the community.

- Standardization of the minimum amount of premium to pay is an area that requires exploration by the health sector (MOH and Non-Governmental Organizations involved CHI). The premium amount is a key factor that determines enrolment and service packages for insurance schemes. As such, standardizing the premium would attempt to cater for all population needs and determine the service package as well as promotion of group cover rather than individual cover. This would possibly lead to increased and accelerated scheme affordability by the low-income earners.

Abbreviation list

CBHIS, Community-Based Health Insurance Scheme; CHI, Community Health Insurance; CHIS, Community Health Insurance Schemes; CBHFA, Community-Based Health Financing Association; GDP, Gross Domestic Product; KCCA, Kampala Capital City Authority; KI, Key informant; KOTSA, Kampala Operational Taxi Stages Association; MOH, Ministry of Health; NHA, National Health Accounts; NGO, Nongovernmental organization; NHIS, National Health Insurance Scheme; OOP, Out of pocket; PNFP, Private Not for Profit; UCBHFA, Uganda Community-Based Health Financing Association; UGX, Uganda Shilling; USD, United States dollar; WHO, World Health Organisation; WTP, Willingness To Pay.

Ethics approval and consent to participate

We obtained ethical approval to conduct this study from the International Health Sciences University (now named Clarke International University) School of Public Health and Management Research and Ethics Committee. We also obtained signed consent from all respondents after assuring them that all the data would remain anonymous.

Availability of data and materials

The data are available and can be provided on request.

Acknowledgments

We would like to thank the staff of Kampala Capital City Authority, Ministry of Health Uganda, Kampala Operational Taxi Stages Association, and the taxi drivers who were involved in this study. We are also grateful to International Health Sciences University and St. Augustine International University for setting the stage for the study. The contribution of Brendan Kwesiga of WHO Uganda country office on statistical analysis is highly acknowledged. The study was funded from the authors own resources and did not receive any external assistance.

Author contributions

All authors contributed to data analysis, drafting or revising the article, gave final approval of the version to be published, and agree to be accountable for all aspects of the work.

Disclosure

The authors report no conflicts of interests in this work.

References

1. Kutzin J. Health Insurance for the Formal Sector in Africa: but. World Health Organisation. 1997. doi:10.2471/BLT.12.113985

2. Basaza RK, Criel B, Van Der Stuyft P. Low enrolment in Ugandan Community Health Insurance schemes: underlying causes and policy implications. BMC Health Serv Res. 2007;7:105. doi:10.1186/1472-6963-7-105

3. Mebratie AD, Sparrow R, Alemu G, Bedi AS. Enrollment in Ethiopia’s community based.Health Insurance on household economic welfare. Working paper No. 568. A systematic review; 2013. DOI: 10.1016/j.worlddev.2015.04.011.

4. Panda P, Dror I, Koehlemoos TP, et al. What factors affect voluntary and community based health insurance programmes in low and middle-income countries? EPPI-Centre Social Sci Res Unit. 2013. doi:10.1371/journal.pone.0160479

5. WHO : Health Systems Financing - The path to universal coverage. Geneva World Health Organization; 2010. Available from: https://www.who.int/whr/2010/en/.

6. East African Community: Situational Analysis and Feasibility Study of Options for Harmonization of Social Health Protection Systems Towards Universal Health Coverage in the East African Community Partner States; Arusha East African Community. 2014. Available from: http://eacgermany.org/wp-content/uploads/2014/10/EAC%20SHP%20Study.pdf.

7. Ministry of Finance, Planning and Economic Development: State of Uganda Population Report; Kampala; 2017. Available from: http://npcsec.go.ug/wp-content/uploads/2013/06/SUPRE-REPORT-2017.pdf.

8. Basaza RK, Criel B, Van Der Stuyft P. Community health insurance amidst abolition of user fees in Uganda: the view from policy makers and health service managers. 2010. BMC Health Services Research. doi:10.1186/1472-6963-10-33

9. Ministry of Health: National Health Accounts report 2015/16. 2017. Available from: http://library.health.go.ug/publications/health-insurance/national-health-accounts-fy-201415-201516.

10. UCBHFA, Uganda Community Based Health Financing Association report on Community based health financing in Uganda. PHR plus and USAID/GOU; 2014. Available from: https://www.shu.org.ug/index.php/resources/annual-reports/23-shu-annual-report2014/file.

11. UCBHFA, Uganda Community Based Health Financing Association report on Community based health financing in Uganda. PHR plus and USAID/GOU; 2010. Available from: http://www.phrplus.org/Pubs/Tech060_fin.pdf.

12. Robert Mwanje: ‘KCCA to conduct fresh taxi census’ Daily monitor Tuesday July 26th 2011. Available from: https://www.monitor.co.ug/News/National/688334-1207708-a76p7yz/index.html.

13. Uganda Bureau of statistics: National Population and Housing Census. 2014. Available from: https://www.ubos.org/wp-content/uploads/publications/03_20182014_National_Census_Main_Report.pdf.

14. Carmen Denavas-Walt Bernadette DP, Smith J Income, Poverty, and Health Insurance Coverage in the United States; 2006. Available from: https://www.census.gov/newsroom/press-releases/2018/income-poverty.html.

15. Bawa SK. Awareness and willingness to pay for health insurance: an empirical study with reference to Punjab, India. International Journal of Humanities and Social Sciences.2011;1. Accessed February 12 2019. doi:10.1002/14651858.CD005619.pub3

16. Sayem Ahmed MEH. Willingness-to-pay for community-based health insurance among informal workers in Urban Bangladesh. Plos One. 2016. doi:10.1371/journal.pone.0148211

17. Adebayo EF, Uthman OA, Wiysonge CS, Stern EA, Lamont KT, Ataguba JE. A systematic review of factors that affect uptake of community-based health insurance in low-income and middle-income countries. BMC Health Serv Res. 2015;15:543. doi:10.1186/s12913-015-1179-3

18. Basaza R, Kon P, Kirabira P, Lako R. Willingness to pay for National Health Insurance Fund among public servants in Juba City, South Sudan: a contingent evaluation. 2017. International Journal for Equity in Health. doi:10.1186/s12939-017-0650-7

19. Biosca & Brown. Boosting health insurance coverage in developing countries: do conditional cash transfer programmes matter in Mexico? Health Policy and Planning. 2015; 30(2): 155–162. doi:10.1093/heapol/czt109

20. Mogessie EM, Bekele G. Households‟ Willingness to Pay for Community Based Health Insurance Scheme: In Kewiot and Efratana Gedem Districts of Amhara Region. Business and Economic Research. Ethiopia; 2017.

21. Abebe Sorsa Badacho: Household satisfaction with a community based health insurance scheme in Ethiopia. BMC Res Notes. 2018. doi:10.1186/s13104-016-2226-9

© 2019 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2019 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.