")

Back to Journals » ClinicoEconomics and Outcomes Research » Volume 12

Willingness to Pay for Community-Based Health Insurance Scheme and Associated Factors Among Rural Communities in Gemmachis District, Eastern Ethiopia

Authors Kado A, Merga BT , Adem HA , Dessie Y, Geda B

Received 6 June 2020

Accepted for publication 30 September 2020

Published 23 October 2020 Volume 2020:12 Pages 609—618

DOI https://doi.org/10.2147/CEOR.S266497

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Samer Hamidi

Abishu Kado,1 Bedasa Taye Merga,2 Hassen Abdi Adem,2 Yadeta Dessie,2 Biftu Geda3

1West Hararghe Zonal Health Department, Chiro, Ethiopia; 2School of Public Health, College of Health and Medical Sciences, Haramaya University, Harar, Ethiopia; 3Colleges of Health and Medical Sciences, Arsi University, Asella, Ethiopia

Correspondence: Bedasa Taye Merga

School of Public Health, College of Health and Medical Sciences, Haramaya University, P.O.Box. 235, Harar, Ethiopia

Tel +251917723961

Email [email protected]

Background: In sub-Saharan Africa, out-of-pocket expenditures constitute approximately 40% of total healthcare expenditures, imposing huge financial burdens on the poor. To tackle the effects of out-of-pocket payment for healthcare services, Ethiopia has been focusing on implementation and expansion of a community-based health insurance (CBHI) program since 2011. This study assessed willingness to pay for CBHI scheme and associated factors among rural communities in Gemmachis district, eastern Ethiopia.

Methods: Community-based cross-sectional study was conducted among 446 randomly selected participants in Gemmachis district from April 1 to April 30, 2019. Data were collected from participants using pretested structured questionnaires through face-to-face interview. Data were entered into EpiData version 3.1 and analyzed using SPSS version 24. Bivariable and multivariable logistic regression analyses were conducted to identify factors associated with willingness to pay for CBHI.

Results: A total of 440 (98.7%) participants were involved in the study. Three in every four (74.8%) participants were willing to pay for CBHI (95% CI: 70.7%, 78.9%). Primary education (AOR=5.1, 95% CI: 2.4, 11.1), being merchant (AOR=0.23, 95% CI: 0.10, 0.51), housewife (AOR=3.8, 95% CI: 1.3, 11.0), poor (AOR=2.5, 95% CI: 1.3, 4.7), illness in the last one year (AOR=3.1, 95% CI, 1.9, 5.2), good knowledge about CBHI (AOR=2.3, 95% CI: 1.5, 3.6) and access to public health facility (AOR=2.0,95% CI: 1.1, 3.7) were all significantly associated with willingness to pay for CBHI.

Conclusion: A significant proportion of participants were willing to pay for CBHI scheme. Education, occupation, wealth status, illness in the last one year, knowledge about CBHI and access to healthcare facility were factors significantly associated with willingness to pay for CBHI. If the scheme is to serve as a means to provide access to health service, the premium for membership should be tailored and customized by individual socioeconomic factors.

Keywords: willingness to pay, community-based health insurance, associated factors, Ethiopia

Introduction

Financial constraints for healthcare services are remained challenging for most of low and middle income countries (LMICs) to provide healthcare coverage to their citizens effectively.1 About 150 million people worldwide suffer a financial shock each year, and two thirds of them get impoverished due to direct payment for healthcare services.2 The world’s 1.3 billion people with very low incomes still lack access to effective and affordable healthcare services.3

Low and middle income countries suffer the catastrophic financial burden due to out of pocket payments, which accounts 30% to 85% of the total healthcare spending.4,5 In sub-Saharan Africa (SSA), out-of-pocket expenditures constitute approximately 40% of total health expenditures, imposing huge financial burdens and limiting access to healthcare services in some of the poorest countries around the world.6 Ethiopia is one of the countries with the highest proportion (34%) of healthcare expenditures generated from households as a means of out-of-pocket payments.7

Most of the households from LMICs use various resources such as savings, borrowing, using loans or mortgages, and selling assets or livestock to cover their healthcare expenditures.8,9 Evidence from Ethiopia revealed that common financial coping mechanisms for rural families were reducing food consumption (19%), asset sales including food stock (30%) and borrowing (19%) while about 21% of rural families do not have any coping mechanism at all.10

Health insurance is among the solutions promoted in LMICs since the 1990s to improve access to healthcare services because it avoids direct payments of fees by patients and spread the financial risk among all the insured members.11–13 To mitigate the catastrophic health expenditures imposed by out-of-pocket expenditures, Ethiopia has taken the initiative of healthcare financing reform. In 2011, Ethiopia introduced the CBHI scheme in 13 pilot districts in the four major regions: Amhara, Oromia, Tigray and Southern Nations, Nationalities and Peoples (SNNPs).14 In 2015, Ethiopia also decided to expand the implementation of CBHI scheme to 80% of the districts and enroll at least 80% of households by 2020.14

However, the enrollment rate to CBHI scheme in Ethiopia is still low and varies from region to region. In 2018, the enrollment at national level was around 48%, which ranges from 36% in Oromia Region to 61% in SNNPs Region.14 Similarly, the premium of the scheme also varies across and within the regions in the country, which ranges from 34.4 Ethiopian birrs (ETB) in SNNPs Region to 132 ETB in Tigray Region.15

The synthesis of studies conducted in different parts of the countries shows that the uptake of community-based health insurance is influenced by individual health seeking behavior,16 socio-economic status of the household, place of residences.17 Additionally, a systemic review in LMICs shows that stringent rule of some of the scheme,11 lack of adequate legal and policy framework in support of CBHI and inappropriate benefit of package are the main barriers in utilization of CBHI scheme.18 Furthermore, socio-cultural practice,19 and distance to health facility are another factor that influence uptake of community-based health insurance.20

Moreover, the government of Ethiopia aimed to achieve universal health coverage for its citizens by the end of 2035.7 To meet this, enrollment into community health insurance scheme in all rural parts of the country is considered as one strategy. To this end, it would be vital to have adequate evidence on the demand for the CBHI scheme and determinant factors among rural communities for healthcare planners and program implementers. Therefore, the willingness to pay study helps to have an insight on the possible enrollment of the community to the CBHI and the sustainability of the program.21

Despite the existence of studies on willingness to pay for CBHI in Ethiopian context, previous studies focus on piloted districts and also show huge variations in the willingness to pay and coverage achieved.22–27 The variations across and within the regions and districts in willingness to pay and coverage imply that CBHI schemes are more likely to succeed under certain socioeconomic contexts and conditions. Therefore, this study assessed the level of willingness to pay for CBHI scheme and associated factors among rural households in Gemmachis district, eastern Ethiopia.

Methods

Study Design, Setting and Period

A community-based cross-sectional study was conducted in Gemmachis district in eastern Ethiopia from April 1 to April 30, 2019. Gemmachis district is located in West Hararghe Zone of Oromia Regional State at 314 kilometers East of Addis Ababa, capital of Ethiopia. Based on the 2007 national population census projection, The district has 240,442 total population (117,336 male and 123,106 female) with 50,092 estimated households in 37 rural kebeles in 2019.28 In 2019, there were six functional primary healthcare units and 35 health posts in the district. Farming, selling of khat, and breeding of animals are common agricultural economic activity.

Population and Eligibility Criteria

All rural households in Gemmachis district and rural households in randomly selected kebeles of Gemmachis district were the source population and study population, respectively. Permanent residents of the district were included in the study. Rural household heads who were critically sick or mentally ill who were unable to respond, and those who were employed in formal sectors were excluded from the study.

Sample Size and Sampling Procedures

The sample size was calculated with Epi Info version 7.1 using a single population proportion formula to assess willingness to pay for the CBHI scheme and a double population proportion formula to identify factors associated with willingness to pay for CBHI scheme. Accordingly, the minimum sample size for the level of willingness to pay for CBHI scheme was computed with the following assumptions: confidence level of 95%, margin of error of 5%, 78.0% proportion of willingness to pay the CBHI scheme,26 and 5% non-response proportion. Accordingly, a minimum of 433 participants were required to conduct the study. Similarly, the minimum required sample size for factors associated with willingness to pay for CBHI was computed with the following assumptions: 80% power of the study, 95% confidence level, 57.1% proportion of willingness to pay for CBHI among unexposed, 70.3% proportion of willingness to pay for CBHI among exposed,29 and equal 1:1 ratio of unexposed to exposed with 5% non-response rate. Hence, a minimum of 446 participants were required to conduct the study. Then, we compared those sample sizes and considered the larger sample for the study. Accordingly, a minimum of 446 participants were required to conduct the study.

Two-stage sampling technique was used to select the participants. Gemmachis district was selected from the West Hararghe zone as the district had planned to implement the CBHI. Twelve out of 37 rural kebeles in the district were randomly selected and the minimum required sample size from each kebele was proportionally allocated based on the numbers of permanently residing households in each kebele. We prepared a sampling frame for each kebele using latest community health information system households of 2018 and actual participants in each selected kebele were selected using a systematic sampling technique.

Data Collection Tools and Measurements

Pretested structured questionnaires were used to collect data from participants through face-to-face interview. The tool contains four parts: socio-demographic and economic characteristics, healthcare related factors, knowledge about CBHI and willingness to pay for CBHI with its scenario (English Version Questionnaire).

Willingness to Pay for CBHI

Before asking about willingness to pay for CBHI, each participant was presented with a detailed standard CBHI Scenario (Scenario about willingness to pay for CBHI) after consenting. Then, the participant’s level of willingness to pay for CBHI scheme was measured by asking whether the participant was willing to pay some amount of premium (non-zero Ethiopian birr) for the CBHI scheme during data collection period,29 and the real amount of premium that they were willing to pay for CBHI scheme was assessed using Double Bounded Dichotomous Choice Variant scenario on the contingent valuation method.29

Iddir Participation

Iddir is an indigenous social association existing to help victims deal with the financial burden of catastrophic events such as burial and sickness expenses.30 Iddir participation has implications for willingness to pay for CBHI scheme, as it is an experience of having a kind of insurance since it has risk-sharing and resource pooling elements of formal health insurance, the participant was considered as participated in iddirs when s/he became a formal member of the association and not if otherwise.30

Knowledge About CBHI

It was assessed by 10 yes/no items measuring knowledge about the benefit packages and basic principles of the CBHI scheme. Mean score was computed (4.88±1.78) and knowledge about CBHI was considered as good when the participant scored above mean and poor otherwise.29

Wealth Index

It was measured by standard tool containing 38 yes/no items arranged under three domains. We observed high internal consistency among items (Cronbach’s α=0.81) and we used principal component analysis using varimax rotation to determine composite wealth indexes and wealth status of the participants.

Data Quality Control

Five trained nurses collected the data, and two Bachelor of Science degree public health experts supervised the overall data collection. To maintain the data quality, the questionnaires were adapted from validated tools and published literature and Ethiopian Demographic and Health Survey.31 The questionnaire was pretested on 5% of the total sample in non-selected kebele of the district. Strict supervision of data collection and validation of collected data was carried out by supervisors and investigators.

Statistical Analysis

After checking for completeness, data were entered to EpiData version 3.1 and analyzed using SPSS version 24. Descriptive statistics such as frequency, proportion, mean, median, range and standard deviation were conducted to describe characteristics of participants, accordingly. Principal component analysis with varimax rotation was used to compute the wealth index of participants.

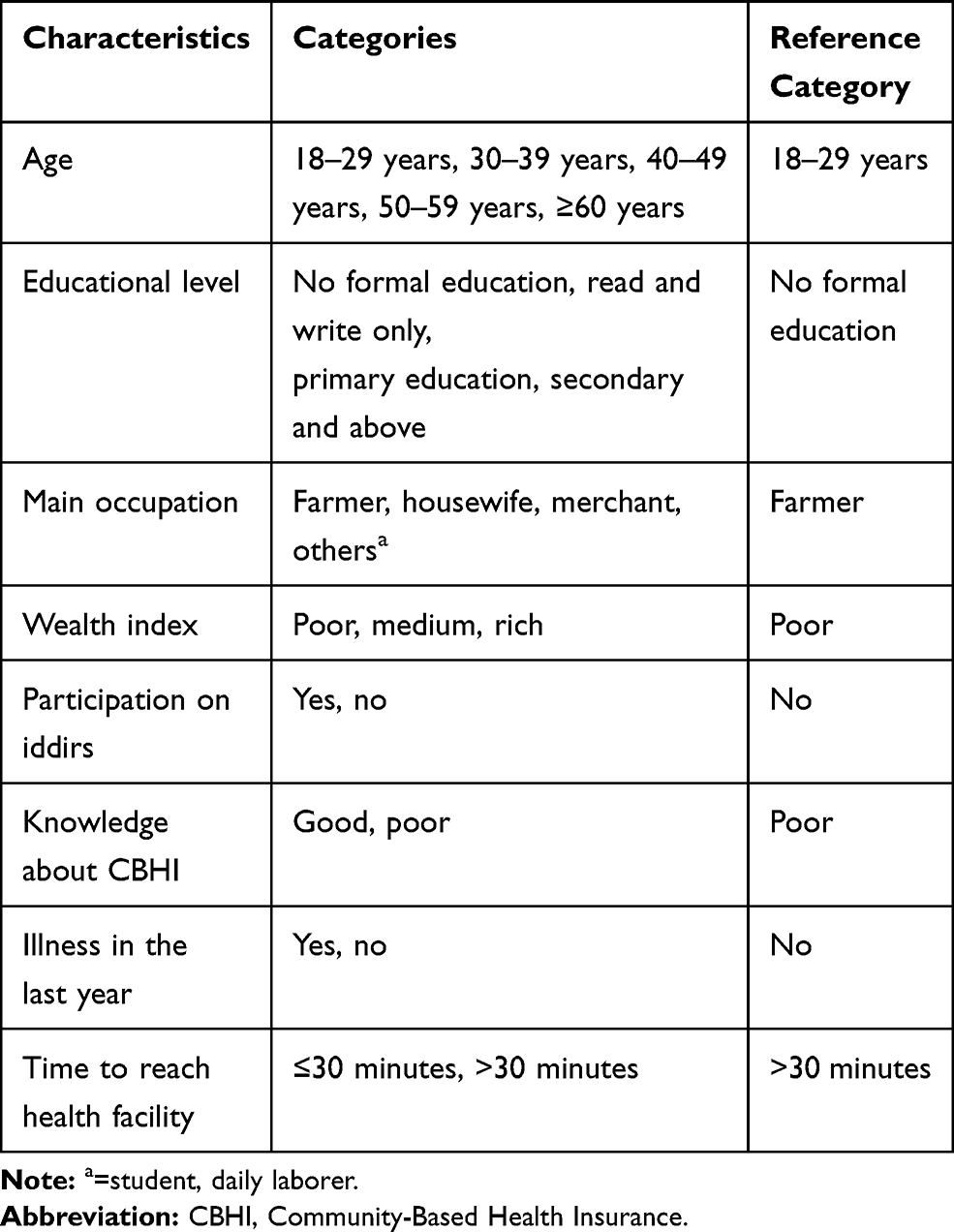

Bivariable logistic regression analysis was computed to identify statistical association between each independent and dependent variables. Variables with P-value<0.25 in bivariable analysis were considered in multivariable analysis.32,33 Multivariable logistic regression analysis was conducted to identify factors associated with willingness to pay for CBHI scheme (Table 1). Adjusted odds ratio (AOR) with 95% CI was used to report association and significance was declared at P<0.05. The model fitness was checked by Hosmer and Lemeshow goodness of fit test.

|

Table 1 Variables Selected for Multivariable Logistic Regression of Factors Associated with Willingness to Pay for CBHI Scheme Among Rural Communities in Gemmachis District, Eastern Ethiopia, 2019 (n=440) |

Ethical Statement

Institutional Health Research Ethical Review Committee of College of Health and Medical Sciences, Haramaya University approved the protocol of the study (Ref.no: IHRERC/0214/018). Written informed consent was obtained from each participant after explaining the purpose and benefits of the study. Each participant was interviewed in a separate area after being informed collected personal information would be kept confidential and not shared. We confirm that this study complies with the Declaration of Helsinki.

Results

Socio-Demographic Characteristics

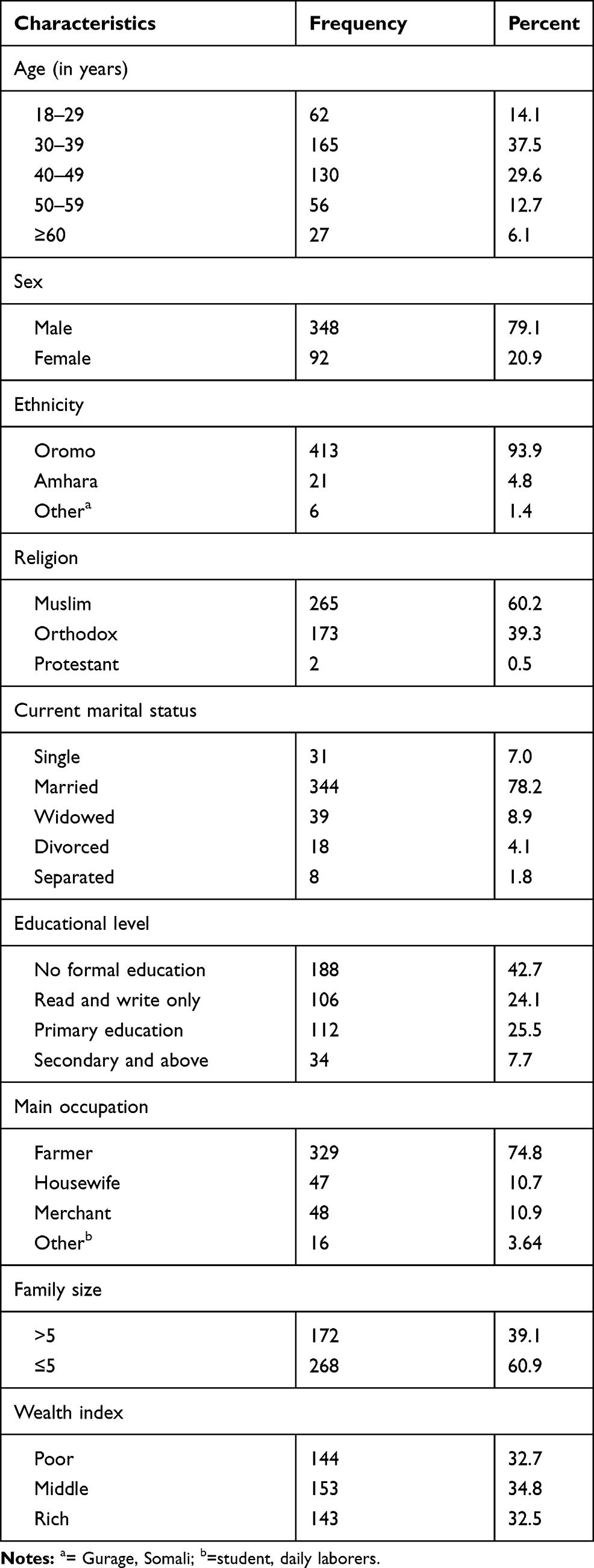

A total of 440 (98.7%) household heads participated in the study. More than one third (37.5%) of participants were in the age group of 30–39 years. The mean age ±SD of participants was 40±10.34 years. The majority, 348 (79.1%) participants were male. More than two out of five (42.7%) participants had no formal education. Nearly one-third (32.7%) of participants were poor (Table 2).

|

Table 2 Sociodemographic Characteristics of Participants in Gemmachis District, Eastern Ethiopia, 2019 (n=440) |

Knowledge About CBHI Scheme

All respondents (440) had heard about CBHI. Health extension worker, 189 (43.0%) and radio/television, 84 (19.1%) were their dominant source of information. More than three out of five, 276 (62.7%) participants had good knowledge about the benefits package and basic principles of community-based health insurance. Almost all (98.6%) of the respondents were participating in the indigenous social networking (iddir).

Healthcare-Related Factors

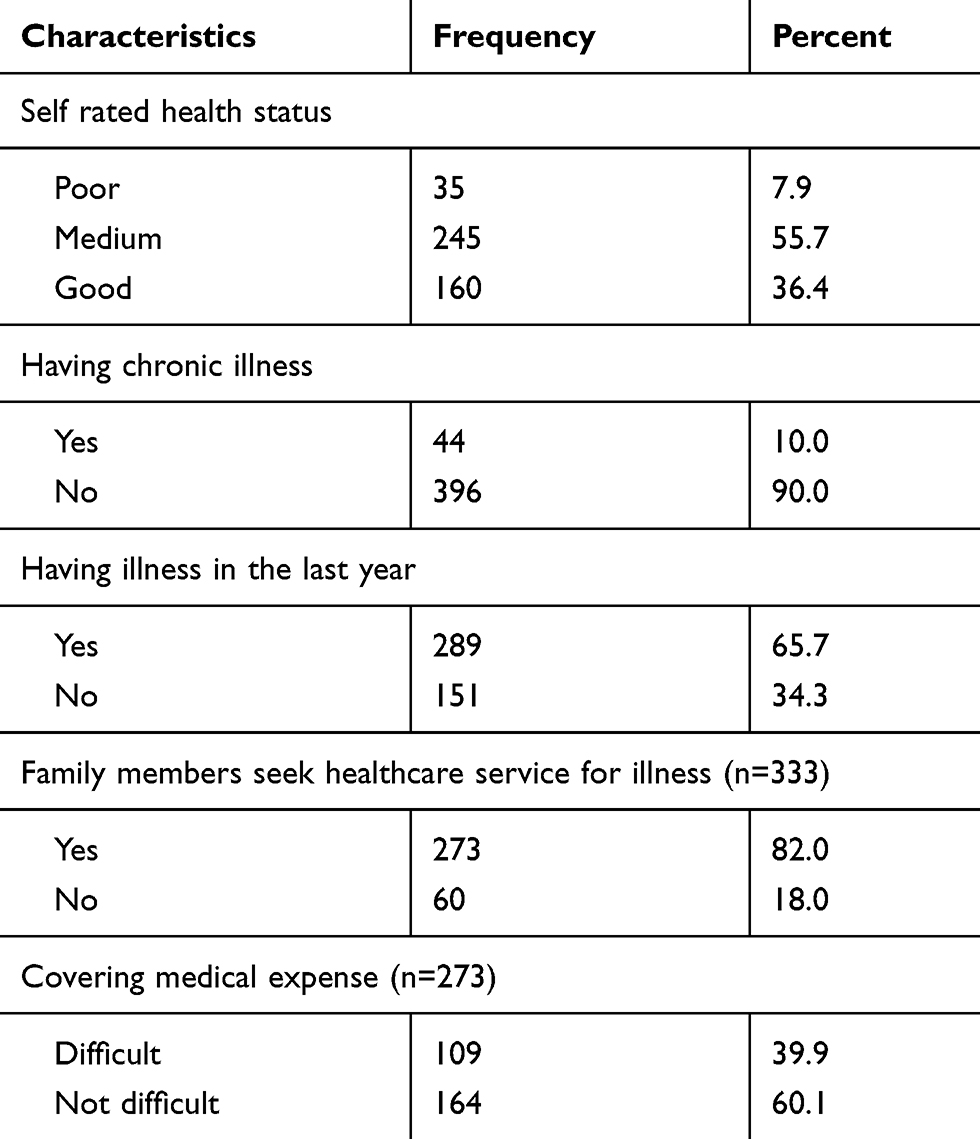

More than one-third (36.4%) of participants perceived their health status as good. Forty four (10%) participants had self-reported chronic illness while 289 (65.7%) participants had encountered illness in the last year. The majority, 373 (82%) of participants had sought medical treatment. Of total respondents who sought medical care for their illness 109 (39.9%) participants have faced difficulty in getting money to pay for medical expenses. The mean medical expense of the participants was 538.4 (±235.7 SD) Ethiopian birrs per a year. Of a total 273 respondents who have taken medical treatment, 114 (41.8%) were satisfied with the healthcare service and cost. One hundred thirty one (48%) and 91 (33.3%) participants perceived that the quality of healthcare as high and medium, respectively. The mean (foot walking) time to reach the nearby public health facility was 54±28.6 minutes (Table 3).

|

Table 3 Healthcare Characteristics of Participants in Gemmachis District, Eastern Ethiopia, 2019 (n=440) |

Willingness to Pay for CBHI Scheme

Three hundred twenty nine 74.8% of participants, showed their WTP for CBHI (95% CI: 70.7%, 78.9%). The mean amounts of money household heads willing to pay were 264 (SD±115.864) ETB per household per annual. Of 346 respondents willing to pay, 120 (34.6%) were willing to pay the initial bid amount of 250 ETB, which is the premium set by the government. Of these, 27 (7.8%) participants who were willing to pay the initial bid were also willing to pay the first higher bid of 300 ETB, and 32 (9.2%) who were willing to pay the first higher bid were also willing to pay the second higher bid amount. Of total respondents who were not willing to pay the initial bid, 82 (23.7%) were willing to pay the first lower bid of 180 ETB, 91 (26.3%) who were not willing to pay the first lower bid were willing to pay 100 ETB, and 53 (15.3%) were willing to pay the lowest bids 75 ETB. The respondents reason for not willing to pay for CBHI scheme were; poor perceived quality of healthcare 41 (9.3%), doubt management system 38 (8.6%) and lack of enough money to pay 19 (4.3%). Regarding payment of premium, all of the participants who revealed their willingness to pay prefer the premium of CBHI by annual flat rate payment.

Factors Associated with Willingness to Pay for CBHI Scheme

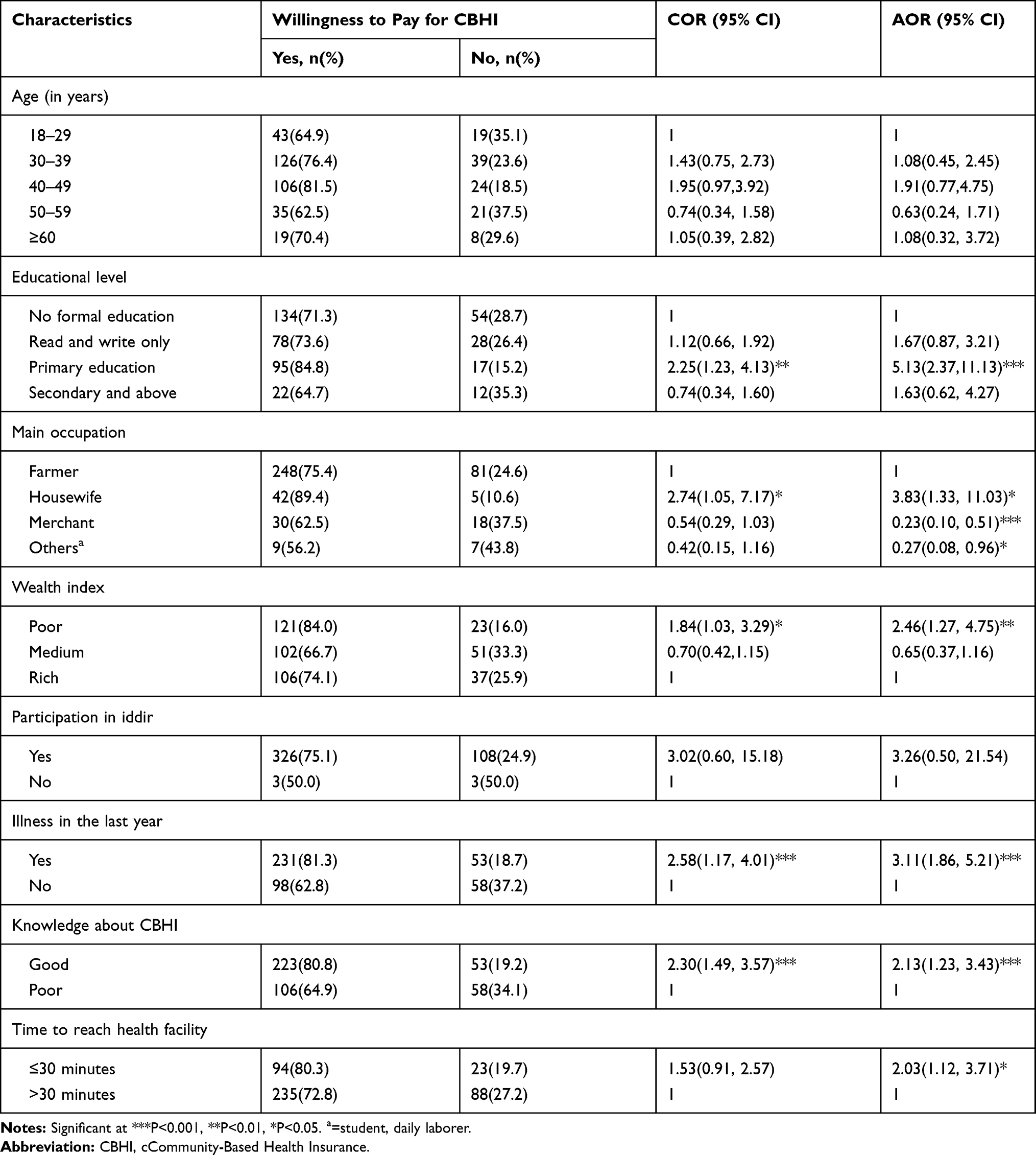

In bivariable analysis, age, educational status, occupational status, having illness in the last year, wealth index, participation on iddirs, knowledge about CBHI and time to reach nearby health facility, were associated with willingness to pay for CBHI scheme at p-value <0.05. All variables with P<0.25 in bivariable analysis were included in multivariable analysis.1,32

The odds of willingness to pay for the CBHI scheme was 5.13 times higher among household heads who had primary education compared to those who had no formal education [AOR= 5.13 (2.37, 11.13)]. The odds of willingness to pay for the CBHI scheme was 3.83 times higher among household heads who were housewives [AOR=3.83 (1.33, 11.03)] while the odds of willingness to pay for the scheme was reduced by 77% among household heads who were merchants [AOR=0.23 (0.10, 0.51)] and reduced by 73% among household heads who were students/daily laborers [AOR=0.27 (0.08, 0.96)] compared to those who were farmers, respectively. The odds of willingness to pay for the CBHI scheme was 2.46 times higher among poor compared to rich participants [AOR=2.46 (1.27, 4.75)]. The odds of willingness to pay for the CBHI scheme was 2.03 times higher when the participants took less than or equal to 30 minutes to reach nearby public health facility compared to those who took more than 30 minutes to reach nearby public health facility [AOR=2.03 (1.12, 3.71)]. The odds of willingness to pay for the CBHI scheme was 2.30 times higher among household heads who had good knowledge about CBHI compared to those who had poor knowledge about CBHI [AOR=2.30 (1.49, 3.57)]. The odds of willingness to pay for CBHI was 3.11 times higher among participants who had illness in the last year compared to those who had no illness in the last year [AOR=3.11 (1.86, 5.21)] (Table 4).

|

Table 4 Bivariable and Multivariable Logistic Regression of Factors Associated with Willingness to Pay for the CBHI Scheme Among Rural Communities in Gemmachis District, Eastern Ethiopia, 2019 (n=440) |

Discussion

Around a quarter of participants were not willing to pay for CBHI scheme. In this study, educational status, main occupation, knowledge about CBHI, wealth status, time to reach nearby public health facility and history of illness in the last one year significantly associated with willingness to pay for CBHI scheme.

This study showed that 74.8% of the respondents were willing to pay for CBHI. This is comparable with that of study conducted in rural India which was 70%.12 This finding is higher than the study finding in Wondo District, Southeast Ethiopia which was 66.5%,29 and Pakistan, which was 12.4%.34 However, this finding is lower than study done in Fogera District, Northwest Ethiopia which was 94.7%;23 Southwest Nigeria (82.4%),35 and central Nigeria (87%).36 The discrepancy might be due to differences in socioeconomic status, sample size, and study period.

The mean amounts of money household heads were willing to pay were 264 (SD±115.864) ETB or 7.76 (SD± 3.41) US$ per household per annual. This is lower than that of Iran which was US$ 2.77 per month (US$33.24 annually),37 and Ghana which was monthly US$ 3.03 (US$ 36.36 annually) in a rural community.38 The discrepancy might be due to differences in socioeconomic status, and health insurance experiences.

Household heads with Primary education (grade 1–8) were more likely to pay for CBHI than those with no formal education. This is supported by findings from previous studies done in Namibia,39 Ghana,38 and Burkina Faso.40 This could be because educated individuals might easily understand the benefits of participating in the health insurance scheme and better health seeking behavior.

Household heads that had good knowledge of CBHI were more willing to pay for CBHI than their counterparts. This finding is in line with that of studies done in, Ethiopia,22,24,41 and Pakistan.34 Continues education and bringing basic knowledge about the benefits of the scheme increases the likely of willing to pay and enrollment.42

Regarding the occupational status; merchant household heads were more willing to pay for CBHI compared to farmers. This result is supported with study done in Northeast Ethiopia,41 and Edo state of Nigeria.43 This might be due to merchant household heads having more exposure to media to understand the benefits of CBHI. Housewife respondents were more willing to pay for CBHI compared to farmers whereas others (student, daily laborers) were less likely to be willing to pay for CBHI as compared to farmers. This could be because housewives might feel more responsibility about the health of their family and thus be more willing to pay for CBHI to secure the financial uncertainty of future health expenses. Studies from Ghana, Senegal and Mali44 indicate that female-headed households are more likely to enroll into CBHI than male.

Households with poor wealth status were more likely willing to pay for CBHI than rich household heads. This finding was somewhat similar with cross-sectional studies conducted in different parts of Ethiopia.25,42,45 This could because of the relative pro-poor nature of the CBHI that may in part be attributed to the relatively low premium.42 Another justification is that the poor households prefer to join CBHI because they could not afford the expensive out of pocket payment.46 Household heads who had reported any illness history in the past year were more willing to pay for CBHI than households with no history of illness in the past year. This finding is in line with study from India,47 and Bangladesh.48 This might be due to the risk-averse individuals are more likely to pay for CBHI.

Furthermore, household at close distance from nearby health facility (less than or equal to 30 minutes) were more willing to pay for community-based health insurance than those reach the nearby health facility in more than 30 minutes. This finding is in line with the finding of the study conducted in Mali and Senegal,44 and rural China.1 This might be due to the fact that health facility’s accessibility is quite related with the health seeking behavior and the demand for CBHI.49,50

By using contingent valuation method, one have to be aware that the existence of nay-saying or yea saying that can affect the accuracy of the result.51 Therefore in this study, the reason for refusing to pay was elicited to rule out protest no answer and the number was minimal. Yea-saying can be identified if the respondent answered yes to all bid options and the percentage was low in this study.

Strength and Limitation of the Study

Regarding the strengths, the study used Double-Bounded Dichotomous choice variant of the contingent valuation method which helps to reduce response bias. This study may provide factual insight to stakeholders in the scheme, and ultimately help in organizing and managing the scheme for better acceptability to the communities.

Even though this study used the large sample size with high response rate, due to the nature of the WTP, the study may not show the actual amount of money the households can pay for a proposed scheme based on their own choice. Some households, who have a better understanding of the benefit packages and interest in implementation of the scheme in the district, may overestimate their premium contributions and the opposite may also be true.

Conclusions

This study revealed that the majority of the rural household heads in the study area were willing to pay for community-based health insurance scheme. Primary education, merchant, housewife, poor wealth status, good knowledge about CBHI, having illness in the last year and distance from health facility were factors associated with willingness to pay for community-based health insurance.

In order to make the CBHI scheme more attractive to all citizens with different socioeconomic status, at least in the short term, the premium for membership should be customized by individual socioeconomic factors. Strengthening awareness creation at community level about the benefit package and principle of the scheme would increase their demand for the CBHI scheme.

Furthermore, we recommend the prospective researchers to explore the different methods of payment through qualitative research on reasons of stated willingness to pay for the CBHI scheme.

Abbreviations

AOR, adjusted odds ratio; CBHI, Community-Based Health Insurance; CI, confidence interval; COR, crude odds ratio; LMIC, low and middle income countries; OOP, out of pocket payments; SSA, sub-Saharan Africa; WHO, World Health Organization; WTP, willingness to pay.

Data Sharing Statement

Data that support the findings are available from the correspondence author on reasonable request.

Acknowledgments

The authors would like to thank Haramaya University college of Health and Medical Sciences for providing opportunity and intellectual and technical support throughout the study. We are also grateful to Gemmachis district health office, study participants, data collectors, and supervisors for their valuable roles in the success of this study.

Author Contributions

All authors contributed to conception and design of the study, acquisition of data, data analysis and interpretation, drafting and revising the manuscript, have agreed on the journal to which the article will be submitted, gave their final approval for submission and the version to be published, and agreed to be accountable for all aspects of the work.

Funding

No external funding was received.

Disclosure

The authors declared that they have no competing interests.

References

1. Zhang L, Wang H, Wang L, Hsiao W. Social capital and farmer’s willingness-to-join a newly established community-based health insurance in rural China. Health Policy (New York). 2006;76(2):233–242. doi:10.1016/j.healthpol.2005.06.001

2. Reshmi B, Nair NS, Sabu K, Unnikrishnan B. Awareness, attitude and their correlates towards health insurance in an urban south Indian population. Manag Health. 2012;16(1).

3. Purohit B. Community based health Insurance in India: prospects and challenges. Health. 2014;2014.

4. World Health Organization. The World Health Report-Financing for Universal Coverage. Geneva: World Health Organization; 2010:23–25.

5. Njagi P, Arsenijevic J, Groot W. Understanding variations in catastrophic health expenditure, its underlying determinants and impoverishment in sub-Saharan African countries: a scoping review. Syst Rev. 2018;7(1):136. doi:10.1186/s13643-018-0799-1

6. Leive A, Xu K. Coping with out-of-pocket health payments: empirical evidence from 15 African countries. Bull World Health Organ. 2008;86:849–856C. doi:10.2471/BLT.07.049403

7. FDRE MoH. Health Sector Transformation Plan. Addis Ababa, Ethiopia; 2015:184.

8. Alam K, Mahal A. Economic impacts of health shocks on households in low and middle income countries: a review of the literature. Global Health. 2014;10(1):21. doi:10.1186/1744-8603-10-21

9. Kruk ME, Goldmann E, Galea S. Borrowing and selling to pay for health care in low-and middle-income countries. Health Aff. 2009;28(4):1056–1066. doi:10.1377/hlthaff.28.4.1056

10. Yilma Z, Mebratie A, Sparrow R, et al. Coping with shocks in rural Ethiopia. J Dev Stud. 2014;50(7):1009–1024. doi:10.1080/00220388.2014.909028

11. Adebayo EF, Uthman OA, Wiysonge CS, Stern EA, Lamont KT, Ataguba JE. A systematic review of factors that affect uptake of community-based health insurance inlow-income andmiddle-income countries. BMC Health Serv Res. 2015;15(1):543. doi:10.1186/s12913-015-1179-3

12. Dror DM, Chakraborty A, Majumdar A, Panda P, Koren R. Impact of community-based health insurance in rural India on self-medication & financial protection of the insured. Indian J Med Res. 2016;143(6):809. doi:10.4103/0971-5916.192075

13. Woldemichael A, Shimeles A. Measuring the Impact of Micro-Health Insurance on Healthcare Utilization: A Bayesian Potential Outcomes Approach. African Development Bank Group; 2015.

14. Ethiopian Health Insurance Agency. Evaluation of Community-Based Health Insurance Pilot Schemes in Ethiopia: Final Report; 2015.

15. Ethiopian Health Insurance Agency. Evaluation of Community-based Health Insurance Pilot Schemes in Ethiopia; 2015.

16. Shiferaw S. Assessment of Factors Affecting Uptake of Community Based Health Insurance Among Sabata Hawas Woreda Community, Oromiya Region. Addis Ababa: Public Health; 2017.

17. Mebratie AD, Sparrow R, Yilma Z, Abebaw D, Alemu G, Bedi A. Impact of Ethiopian pilot community-based health insurance scheme on health-care utilisation: a household panel data analysis. Lancet. 2013;381:S92. doi:10.1016/S0140-6736(13)61346-X

18. Mirach TH, Demissie GD, Biks GA. Determinants of community-based health insurance implementation in west Gojjam zone, Northwest Ethiopia: a community based cross sectional study design. BMC Health Serv Res. 2019;19(1):544. doi:10.1186/s12913-019-4363-z

19. Mukangendo M, Nzayirambaho M, Hitimana R, Yamuragiye AJ. Factors contributing to low adherence to community-based health insurance in Rural Nyanza District, Southern Rwanda. J Environ Res Public Health. 2018;2018.

20. Dixon J. Determinants of Health Insurance Enrolment in Ghana’s Upper West Region. The University of Western Ontario (Thesis). 2014.

21. Phillips K, Homan R, Luft H, et al. Costs and financing of public goods: the case of poison control centres.

22. Mamo E, Bekele G. Households¡¯ Willingness to pay for community based health insurance scheme: in Kewiot and EfratanaGedem Districts of Amhara Region, Ethiopia. Bus Econ Res. 2017;7(2):212–233. doi:10.5296/ber.v7i2.11513

23. Kebede A. Willingness to pay for community based health insurance among households in the rural community of Fogera District, north West Ethiopia. Int J Econ Finance Manag Sci. 2014;2(4):263–269. doi:10.11648/j.ijefm.20140204.15

24. Minyihun A, Gebregziabher MG, Gelaw YA. Willingness to pay for community-based health insurance and associated factors among rural households of Bugna District, Northeast Ethiopia. BMC Res Notes. 2019;12(1):55. doi:10.1186/s13104-019-4091-9

25. Entele BR, Emodi NV. Health insurance technology in Ethiopia: willingness to pay and its implication for health care financing. Am J Public Health Res. 2016;4(3):98–106.

26. Haile M, Ololo S, Megersa B. Willingness to join community-based health insurance among rural households of Debub Bench District, Bench Maji Zone, Southwest Ethiopia. BMC Public Health. 2014;14(1):591. doi:10.1186/1471-2458-14-591

27. Kibret GD, Leshargie CT, Wagnew F, Alebel A. Willingness to join community based health insurance and its determinants in East Gojjam zone, Northwest Ethiopia. BMC Res Notes. 2019;12(1):31. doi:10.1186/s13104-019-4060-3

28. Central Statistical Agency of Ethiopia. The 2007 Population and Housing Census of Ethiopia. Addis Ababa: CSA; 2007.

29. Gisha A. Willingness to Pay for Community Based Health Insurance and Its Determinants Among Households in Wondo District, Oromia Region, South East Ethiopia. Addis Abeba Universty; 2017.

30. Ololo S, Jirra C, Hailemichael Y, Girma B. Indigenous Community Insurance (IDDIRS) as an alternative health care financing in Jimma city, Southwest Ethiopia. Ethiop J Health Sci. 2009;19(1).

31. Agency CS, ICF. Ethiopia Demographic and Health Survey 2016: Addis Ababa, Ethiopia, and Rockville, Maryland, USA. CSA and ICF; 2016.

32. Mickey RM, Greenland S. The impact of confounder selection criteria on effect estimation. Am J Epidemiol. 1989;129(1):125–137. doi:10.1093/oxfordjournals.aje.a115101

33. Zhang Z. Model building strategy for logistic regression: purposeful selection. Ann Transl Med. 2016;4(6).

34. Jahangeer A, Ul Haq R Willingness to purchase health insurance in Pakistan.

35. Bamidele J, Adebimpe W. Awareness, attitude and willingness of Artisans in Osun State Southwestern Nigeria to participate in community based health insurance. J Community Med Prim Health Care. 2012;24(1–2):1–10.

36. Adedeji AS, Doyin A, Kayode OG, Ayodele AA. Knowledge, practice, and willingness to participate in community health insurance scheme among households in Nigerian Capital City. Sud J Med Sci. 2017;12(1):9–18. doi:10.18502/sjms.v12i1.854

37. Asgary A, Willis K, Taghvaei AA, Rafeian M. Estimating rural households’ willingness to pay for health insurance. Eur J Health Econ. 2004;5(3):209–215. doi:10.1007/s10198-004-0233-6

38. Asenso-Okyere WK, Osei-Akoto I, Anum A, Appiah EN. Willingness to pay for health insurance in a developing economy. A pilot study of the informal sector of Ghana using contingent valuation. Health Policy (New York). 1997;42(3):223–237. doi:10.1016/S0168-8510(97)00069-9

39. Allcock SH, Young EH, Sandhu MS. Sociodemographic patterns of health insurance coverage in Namibia. Int J Equity Health. 2019;18(1):16. doi:10.1186/s12939-019-0915-4

40. Dong H, Kouyate B, Cairns J, Mugisha F, Sauerborn R. Willingness-to-pay for community-based insurance in Burkina Faso. Health Econ. 2003;12(10):849–862. doi:10.1002/hec.771

41. Workneh SG, Biks GA, Woreta SA. Community-based health insurance and communities’ scheme requirement compliance in Thehuldere district, northeast Ethiopia: cross-sectional community-based study. Clinicoecon Outcomes Res. 2017;9:353. doi:10.2147/CEOR.S136508

42. Derseh A, Sparrow R, Debebe ZY, Alemu G, Bedi AS. Enrolment in Ethiopia’s Community Based Health Insurance Scheme. International Institute of Social Studies of Erasmus University (ISS); 2013.

43. Oriakhi H, Onemolease E. Determinants of rural household’s willingness to participate in community based health insurance scheme in Edo State, Nigeria. Stud Ethno Med. 2012;6(2):95–102. doi:10.1080/09735070.2012.11886425

44. Chankova S, Sulzbach S, Diop F. Impact of mutual health organizations: evidence from West Africa. Health Policy Plan. 2008;23(4):264–276. doi:10.1093/heapol/czn011

45. Mebratie AD, Sparrow R, Yilma Z, Alemu G, Bedi AS. Dropping out of Ethiopia’s community-based health insurance scheme. Health Policy Plan. 2015;30(10):1296–1306.

46. Bayked EM, Kahissay MH, Workneh BD Factors affecting community based health insurance utilization in Ethiopia: a systematic review.

47. Ghosh S, Mondal S. Morbidity, health expenditure and willingness to pay for health insurance amongst the urban poor: a case study. J Health Manag. 2011;13(4):419–437. doi:10.1177/097206341101300404

48. Ahmed S, Hoque ME, Sarker AR, et al. Willingness-to-pay for community-based health insurance among informal workers in urban Bangladesh. PLoS One. 2016;11:2. doi:10.1371/journal.pone.0148211

49. Usman AB, Bukola A. Willingness to pay for community based health care financing scheme: a comparative study among rural and urban households in Osun State, Nigeria. J Dent Med Sci. 2013;5(6):27–40.

50. Yismaw M. Role of Community Based Health Insurance on Health Service Provision and Healthcare Seeking Behavior of Households in Rural Ethiopia: The Case of Tehuledere District, South Wollo Zone. Addis Ababa University; 2017.

51. Nocera S, Bonato D, Telser H. The contingency of contingent valuation how much are people willing to pay against alzheimer’s disease? Int J Health Care Finance Econ. 2002;2(3):219–240. doi:10.1023/A:1020441726964

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.