")

Back to Journals » Risk Management and Healthcare Policy » Volume 15

Why Not Blow the Whistle on Health Care Insurance Fraud? Evidence from Jiangsu Province, China

Received 21 June 2022

Accepted for publication 1 October 2022

Published 12 October 2022 Volume 2022:15 Pages 1897—1915

DOI https://doi.org/10.2147/RMHP.S379300

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Jongwha Chang

Dandan Wang, Changchun Zhan

School of Management, Jiangsu University, Zhenjiang, People’s Republic of China

Correspondence: Changchun Zhan, Tel +86-15952808385, Email [email protected]

Purpose: To identify the factors that influence whistleblowing behavior as it relates to health care insurance fraud in Jiangsu Province, China.

Methods: To construct a factor model and formulate research hypotheses using the Motivation–Opportunity–Ability framework. We designed a questionnaire containing 24 items and distributed it on-site to 2081 respondents in Jiangsu Province, China. Afterward, we applied structural equation modeling to validate the research hypotheses.

Results: Policy awareness negatively contributes to whistleblowing behavior, risk perception does not reduce the incentive to blow the whistle, and an inability to recognize fraud is another critical barrier to converting whistleblowing intentions into behavior.

Conclusion: Practices that are likely to promote citizen whistleblowing on insurance fraud may focus on the constraints identified by the comprehensive Motivation–Opportunity–Ability framework.

Keywords: health care insurance fraud, whistleblowing behavior, Motivation–Opportunity–Ability framework, structural equation modeling

Introduction

Health care insurance fraud, based on the definition by the National Health Care Anti-Fraud Association (NHCAA), “is an intentional deception or misrepresentation made by a person or an entity, with the knowledge that the deception could result in some kind of unauthorized benefits to that person or entity.1 As an international challenge, NHCAA has conservatively estimated that at least 3%—or over $60 billion—of the annual health care spending in the United States was lost due to fraud,2 and other developed and developing countries’ health care insurance schemes are facing the same dilemma.3–6 During the COVID-19 pandemic, health care funds were particularly important in prevention, diagnosis, and treatment, but incidents of malicious fraud increasingly made headlines in China.7 The Statistical Express Report on the Development of the Medical Security Business in 2020 revealed that the country carried out special operations to combat health care insurance fraud through which 401,000 illegal medical institutions and 26,100 insured personnel were investigated and punished and CNY 22.311 billion in fraudulent losses were recovered. Under a fee-for-service payment system with third-party payers, the institution or physician may prefer to increase the number of medical services they offer to obtain higher returns through practices such as falsifying patient diagnoses, billing for services not performed, and treating “ghost patients.”8–12 In a new kind of fraud known as conspiracy, insured patients collude with their physicians to co-opt profits by preparing beds for hospitalization and exchanging self-pay items for health care insurance settlement projects.13–16

Fraud is not only a gross waste of health care resources but also severely hampers access to quality and safe care for patients with genuine needs, thus making a crackdown on it an urgent necessity.17,18 As fraud shifts from explicit to implicit forms and takes on cross-regional and electrical characteristics, the value of whistleblowing for prevention and identification purposes has been recognized and utilized in health care anti-fraud efforts.19–22 The “False Claims Act”, also known as the “Qui Tam Statute”, which represents the earliest whistleblowing legislation dating back to 1863, allows citizens to sue for false claims.23 Historically, 90% of health care fraud has involved qui tam relators, who led to financial recoveries of $9.3 billion between 1996 and 2005, with more than $1.0 billion paid to whistleblowers.24 Given that universal health care coverage insurance is practiced in China, fraud is essentially an unjust enrichment that undermines citizens’ health rights. Therefore, blowing the whistle not only provides tangible benefits but also contributes to savings in terms of regulatory enforcement costs. In 2018, the National Healthcare Security Administration issued the Interim Measures for Whistleblowing Fraudulent and Deceptive Acts against the Medical Security Fund to obtain information related to health care insurance fraud committed by insiders. However, the policy did not have the desired effect, as less than 1% (0.76%) of all fraud losses were recovered through whistleblowing in 2020.25

Citizen participation in health care insurance anti-fraud is both necessary and possible, to address the mismatch of “ strong intention, thin behavior ” in citizen whistleblowing against health care insurance fraud, analyzing what factors will influence whistleblowing behavior to ensure that the policy’s value lives on is critical. Given the paucity of quantitative research on whistleblowing in the context of health care insurance fraud, we designed a questionnaire based on the Motivation–Opportunity–Ability (MOA) framework, administered it on-site to 2081 citizens in Jiangsu Province, and tested our research hypotheses using structural equation modeling (SEM) to understand the underlying drivers of whistleblowing behavior. Moreover, it stands to reason that such research could be very fruitful as fraud becomes more complex, increasingly prevalent, and has increasingly grave consequences.

Literature Review

Whistleblowing has been a topic of interest to researchers and the general public since the 1990s, as it is an ethical practice that attempts to prevent wrongdoing and illegal actions in health care. However, whistleblowing is not taken lightly and may be seen as a supererogatory act, as many health professionals remain passive and hesitant when confronted with wrongdoing.26,27 This implies that in light of the conflict between ethical compliance and the potential impact that whistleblowing would have on their personal or professional lives, potential whistleblowers with evidence of legitimate fraud may be discouraged from coming forward.28–31 Some studies have focused on ethical dilemmas, even though professional codes impose a responsibility on all health care providers to identify and report fraudulent behavior, which stems from the moral imperative to ensure optimal clinical practicum.32–34 Unfortunately, their hesitation in blowing the whistle on wrongdoing is often justified, as the outcome for whistleblowers can be either constructive or harmful.35

From the perspective of weighing the pros and cons of taking whistleblowing action, a small number of studies have considered the positive outcomes from whistleblowing, such as the supportiveness of whistleblowers’ colleagues, superiors, or the public, along with approval and respect from outside the organization.36 Conversely, numerous studies have highlighted that whistleblowers often experience profound negative influences on their careers and private lives.28,37,38 In a federal lawsuit against a US pharmaceutical manufacturer, Kesselheim et al37 conducted semi-structured interviews with 26 whistleblowers,18 of whom reported that the whistleblowing decision “put their careers at risk”, with 13 of those voicing stress-related health disorders, including asthma, insomnia, and generalized anxiety. An analogous phenomenon has been observed in Australia. Jackson et al39 carried out qualitative narrative research among nurses with a history of whistleblowing, which revealed that some whistleblowers were marginalized by colleagues and experienced workplace bullying. Although the “Qui Tam Statute” technically protects whistleblowers, the reality is that the government cannot guarantee a whistleblower’s anonymity once a lawsuit becomes filed.32 Fleming et al40 surveyed delegates attending the Association of Surgeons in Training (ASiT), and only 16% of respondents felt that protection for whistleblowers was sufficient in the National Health Service (NHS), while there was inadequate knowledge of local or national whistleblowing policies if they intended to blow the whistle, with the majority being unaware of what the whistleblowing helpline was.

An empirical investigation of whistleblowing behavior among individuals with different roles in health care organizations showed that nurses were more supportive of whistleblowing than physicians.27,41 One reason for this finding may be that nurses are more effective in keeping doctors and patients honest with each other, which may mitigate the incentives to commit fraud caused by information asymmetries.42,43 National culture was also confirmed as an essential ingredient in bolstering whistleblowing. In comparing British and Chinese health care students, Cheng44 noted that individuals from collectivist cultures are less likely to be whistleblowers and accept whistleblowing behaviors to a lesser extent than those from individualistic cultures. For potential whistleblowers, organizational response (both positive and negative) may also significantly shape whistleblowing behavior.45 A lack of responsiveness—namely, a failure to address the misconduct in follow-up investigations—was cited as a crucial reason for not blowing the whistle.46 In addition, a quantitative study also verified that culture, organizational characteristics, and the seriousness of the wrongdoing in the Iranian health care system were positive predictors of whistleblowing, and the effect of individual elements was nonsignificant.47 It has also been argued that personal perceived behavioral control weighs more heavily on the whistleblowing decision than all other factors. In other words, a person with the motivation to report fraudulent behavior cannot translate that into action if they are not perceived to be competent.48

If the wrongdoing has been suspected or observed by individuals, the degree to which their whistleblowing actions differ has drawn the attention of scholars.49 A qualitative study of the whistleblowing process at a psychiatric hospital in Japan showed that neither suspicion nor observation of wrongdoing induced whistleblowing behavior.50 Another study in Finland pointed out that of 266 of 397 practitioners who suspected misconduct in health care, less than half (107, or 40%) blew the whistle on it, while 262 others observed the wrongdoing and 147 (56%) of them filed reports, thus showing a higher probability of the latter outcome.37 Meanwhile, after observing misconduct associated with patients, physicians, or administrators to internal, external, and shelved whistleblowing behaviors, Pohjanoksa et al51 proposed the existence of 24 pathways, which demonstrated the complexity of the health care whistleblowing process. Findings from several studies suggest that when health care practitioners blow the whistle, they are more likely to do so internally rather than externally, with the likelihood of action decreasing as the scope of the whistleblowing expands.45,52 The reason for this is that potential whistleblowers may perceive the cost of externally whistleblowing wrongdoing to be higher; that is, external whistleblowing may not only negatively impact the wrongdoer but also damage trust among colleagues as well as the hospital’s reputation.46

In summary, scholars have produced abundant research findings in the search for the factors that influence whistleblowing, which has provided insight for the direction of the current research. However, analyses from the perspective of individual behavior-generating mechanisms are nearly nonexistent. Moreover, whistleblowers’ identities are almost exclusively health care providers (eg, doctors, nurses), and little attention has been paid to the demand-side perspective. Within the health care sector, outsiders (eg, patients, insured persons) or individuals not directly employed by a health care organization are more likely to blow the whistle.53 Therefore, there is a need to expand the research population to explore the factors that contribute to whistleblowing behavior.

Description of Whistleblowing on Health Care Insurance Fraud in Jiangsu Province and Research Design

Data Sources

The data for this paper were sourced from fieldwork in Jiangsu Province. Given that the southern, central, and northern regions of Jiangsu Province are well represented in China’s economic development, a stratified random sampling method was used to select the pilot cities of health care insurance fund supervision in Wuxi (southern), Taizhou (central), and Huai’an (northern) as the sample areas in which to conduct the field survey (given that health care insurance fraud is a sensitive issue, cities A, B, and C will be randomly substituted here).

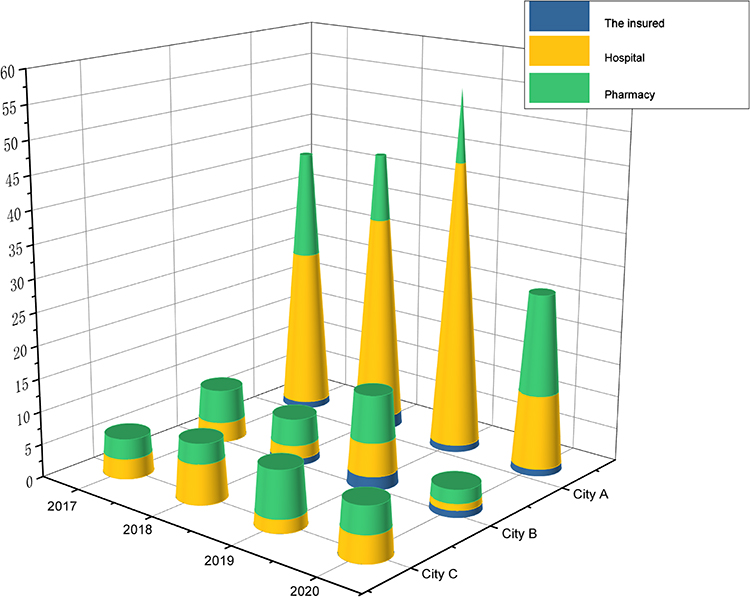

Few Fraud Cases Exposed by Whistleblowing

During 2017–2020, there were relatively few whistleblowing cases in each region, with as many as 55 and as few as four cases. In addition, all three cities introduced a whistleblower reward policy in 2019. By comparing the case volumes before and after the policy implementation, cities B and C saw slight increase of three and two cases, respectively. On the contrary, there was a drop of two cases in city A. In terms of how the whistleblowing on health care insurance fraud targets is distributed, it appears that the sample areas experienced comparatively less coverage on the demand side of health care services and on the insured, and instead tend to cluster around the health care service providers, including designated hospitals and pharmacies (Figure 1).

|

Figure 1 Health care insurance fraud whistleblowing cases. |

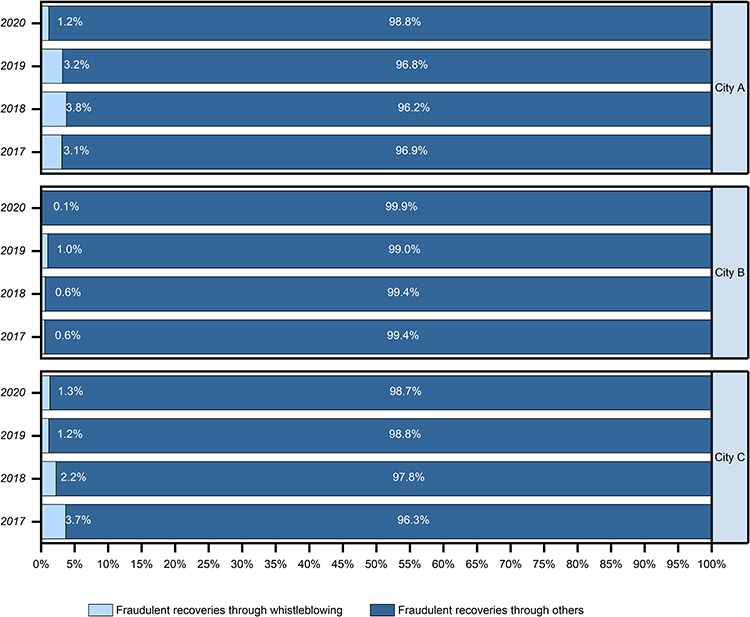

A Low Percentage of Fraud Recovery by Whistleblowing

In general, the ratio of the funds recovered from whistleblowing to total recoveries was low across the sample areas. Before implementing the whistleblower reward policy, the highest observation was 3.8%, while the lowest was 0.6%; after that, the highest was 3.2%, and the lowest was only 0.1%. It is evident that intelligent monitoring and the verification of supervisory staff still play a vital role in recovering fraud losses (Figure 2).

|

Figure 2 Recoveries of health care insurance fraud by whistleblowing. |

A Mismatch Between Whistleblowing Intentions and Behavior

An analysis of 2081 valid questionnaires from the three sample areas revealed that 1539 respondents (73.96%) had the intention to blow the whistle on fraudulent practices, 178 (8.55%) showed no willingness to do so, and another 364 (17.49%) held a neutral attitude. Of those who were willing and neutral, only one submitted a whistleblowing tip, accounting for 0.05% of the sample. Since implementing the whistleblower reward policy, most citizens expressed a high willingness to blow the whistle on fraud but did not proactively do so, thus creating a misalignment of “strong intentions and thin behavior.” Critically, the reasons for this phenomenon remain unexplained.

Research Design

Theoretical Framework and Research Hypothesis

To anchor the theoretical background for our empirical study, one can draw upon the MOA framework to explain the determinants of whistleblowing behavior. Originally developed to understand consumer involvement in the processing of brand information and the corresponding purchasing behavior, the MOA framework asserts that behavior occurs through the confluence of three components:54

—Motivation (M), which can also be described as a goal-oriented incentive expressed by a person’s interest in and desire to do something;55

—Opportunity (O), which is defined as external factors that prompt or inhibit the occurrence of the behavior, namely, the conditions that affect a person’s attentiveness, whether favorable or not;56 and

—Ability (A), which refers to the internal factors that give an individual the ability to perform a behavior; that is, one’s skill and proficiency in interpreting messages.57

Likewise, Kim et al58 proposed that the three factors necessary for any voluntary behavior to occur are “a strong positive intention to carry out the behavior, the opportunity or lack of constraint provided by the environment and the skills required to perform the behavior”. In other words, the motivations possessed by an individual may only induce actual behavior when the necessary abilities and opportunities to do so are present.59 Given its powerful openness and inclusiveness, the MOA framework has been widely adopted in the existing research to interpret various types of behavior.60–62 However, as effective as the MOA framework is as an explanation of behavior, it is not without its drawbacks. In particular, there have been calls to further develop the MOA to more fully capture the complexity of certain behaviors.63,64

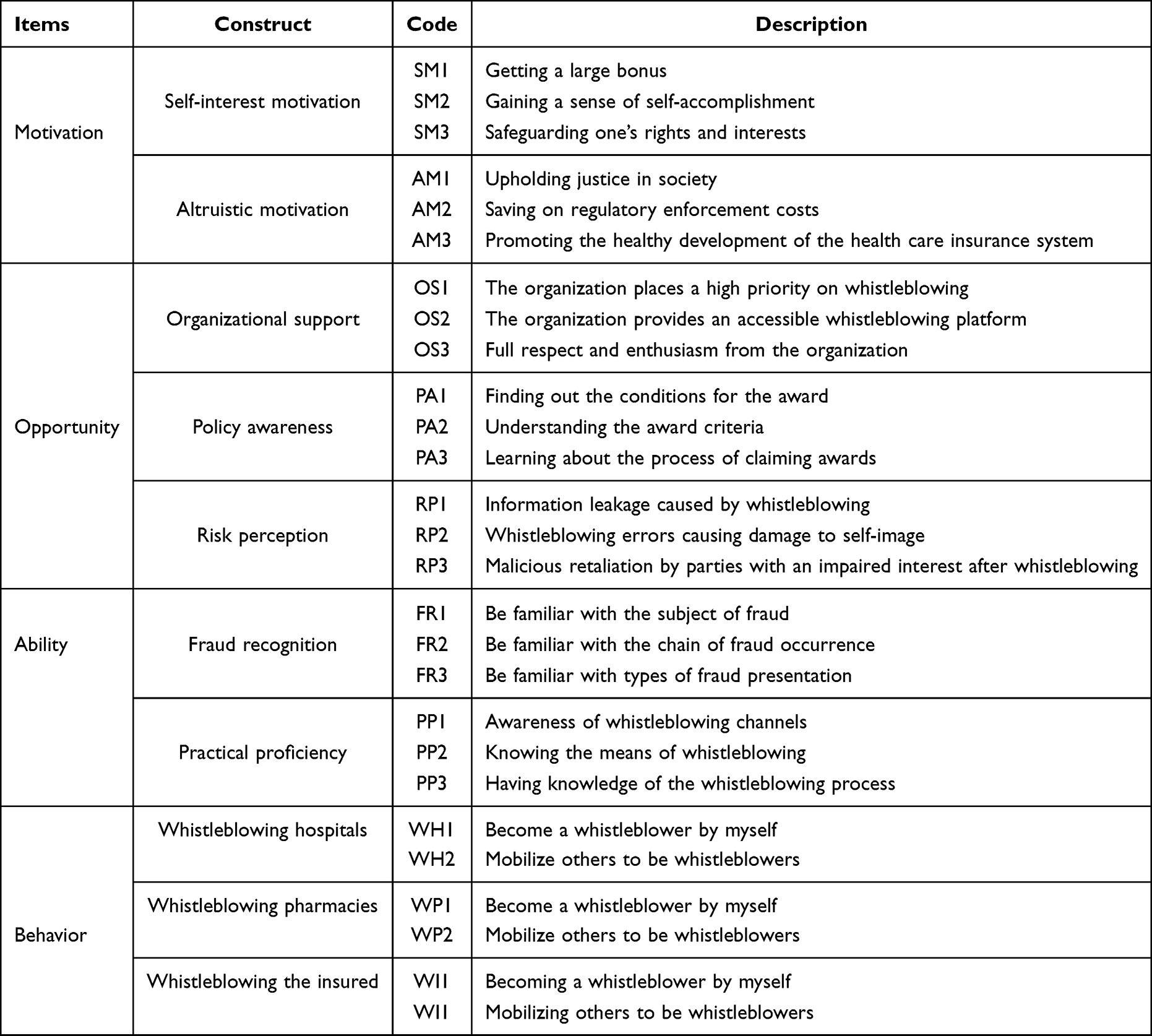

The original purpose of whistleblowing is to discourage improper behaviors, and it is therefore a positive act that benefits society and the organization, among other stakeholders. However, whistleblowers are often characterized by high autonomy and subjectivity, which cannot be forced.65 Since health care insurance fraud is a high-secrecy crime, and the act of whistleblowing is fundamentally characterized as an internalization of losses and a spillover of benefits, potential whistleblowers are constantly adjusting their intentions rather than considering whether to blow the whistle in a direct manner. Therefore, the MOA framework is appropriate for explaining complex whistleblowing behavior. In this paper, the MOA framework is followed and extended by adding endogenous variables based on the existing literature to examine the determinants of whistleblowing behavior as it relates to health care insurance fraud. The factors of MOA were defined as follows. 1) The formation of the motivation to blow the whistle was measured in two dimensions, including self-interest and altruistic motivation. 2) Under the construct of opportunity, the three main elements are organizational support, risk perception, and policy awareness. 3) In the context of whistleblowing behavior, two constructs are chosen to reflect a person’s competence: fraud recognition and practical proficiency (Figure 3).

|

Figure 3 Overview of the integrated MOA framework. |

According to the MOA framework, motivations can be seen as the inherent impetus that guides and motivates whistleblowing behavior, which generally contains both self-interested and altruistic aspects.32 The former is a self-centered decision by the citizens whether to actively blow the whistle, usually premised on the expected benefits of that action, which mainly include monetary rewards and spiritual benefits. Conversely, the latter is the desire to safeguard the common welfare of society, which will promote the security and sustainability of the health care insurance system. With this in mind, we propose the following hypotheses.

H1: Self-interest motivation is positively associated with whistleblowing behavior. H2: Altruistic motivation is positively associated with whistleblowing behavior.

In the MOA framework, opportunities are understood to be an exogenous factor that facilitates or inhibits whistleblowing behavior, specifically in terms of organizational support, policy awareness, and risk perception.28,40,45 Often, individuals who receive emotional support and resources from the involved organizations may be more positive toward whistleblowing.69 At the same time, the whistleblower reward policy provides an incentive platform for citizens, and the likelihood that actual action will be taken increases as potential whistleblowers become more aware of the nature of the policy. Conversely, if the perceived risk of blowing the whistle is higher and individuals fear such actions as their personal information being disclosed and other forms of retaliation, there is a greater tendency to remain silent.70 We thus propose the following hypotheses.

H3: Organizational support is positively associated with whistleblowing behavior. H4: Policy awareness is positively associated with whistleblowing behavior. H5: Risk perception is negatively associated with whistleblowing behavior.

Abilities in the MOA framework refer to whether an actor has the necessary resources, such as the knowledge and skills needed to complete a task. Effective whistleblowing requires a certain personal quality.48 Whistleblowers should have the expertise and practical proficiency to recognize the existence of harmful behavior, judge the degree of harm, determine the availability of evidence and promptly take action.51 Due to the hidden nature of health care insurance fraud, the whistleblower should be familiar with the subjects and forms through which it is committed so that it can be detected promptly. Also, the more acquainted they are with the whistleblowing channels and processes, the more likely it is for those potential whistleblowers to be inclined to take practical action. In light of this, we propose the following hypotheses.

H6: The ability to recognize fraud is positively associated with whistleblowing behavior. H7: Practical proficiency is positively associated with whistleblowing behavior.

Methods

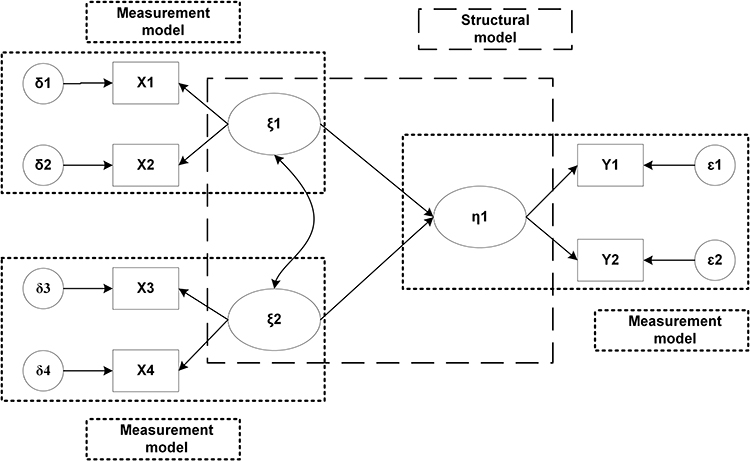

In this paper, an empirical analysis of the causes of whistleblowing dilemmas is conducted using SEM, a statistical method for analyzing the relationship between latent variables based on the covariance matrix of the variables also known as covariance structural analysis.66 In the model, both the exogenous (independent) and endogenous (dependent) variables are latent, abstract concepts that are difficult to directly observe or measure, such as motivation, ability, and behavior. Therefore, these latent variables need to be measured using multiple observed variables or indicators. SEM consists of two components: the measurement model and the structural model (Figure 4). Measurement models are used to analyze whether the selected observed variables are well constructed with respect to the required latent variables by evaluating their reliability and validity. Then, structural models describe the relationship pathways between the latent variables.67,68

|

Figure 4 Structural equation model. |

The mathematical expression of the measurement model is as follows:

The mathematical expression of the structural model is as follows:

Analysis of the Jiangsu Province Case Study

Sample Characteristics

This study selected three pilot cities for health care insurance fund supervision in Jiangsu Province: Taizhou, Wuxi, and Huai’an. In this survey, the Healthcare Security Administration offices in the three regions were used as the interview sites, as these administrations oversee the payment of health care insurance benefits, penalties for fraudulent health care insurance entitlements or fund expenditures, and rewards for whistleblowing behavior. Citizens who visit their offices for related business were selected as respondents because they are likely to make up the majority of the future whistleblowing population and are more interested in health care insurance fraud and anti-fraud efforts.

To ensure the quality of the sample, we conducted two surveys and received support from leaders, staff, and citizens at all levels. Initially, we approached 210 citizens handling business for a pre-survey, and, following the principle of voluntary participation, questionnaires were distributed on-site and modified based on respondents’ feedback. The following formal survey phase was from May 23 to July 29, 2021, when data were collected and 2250 questionnaires were distributed to citizens on-site at the Healthcare Security Administration, of which 2185 (97.1%) were returned. After eliminating 104 invalid questionnaires for providing incomplete or logically contradictory answers to the questions, 2081 valid questionnaires were obtained, for an effective recovery rate of 92.48%. Since whistleblowing represents a sensitive and emotional issue for those who engage in it, it is once again emphasized that participation is voluntary, confidentiality and anonymity are guaranteed, and it is not possible to identify individuals or organizations from their responses to obtain more accurate information.

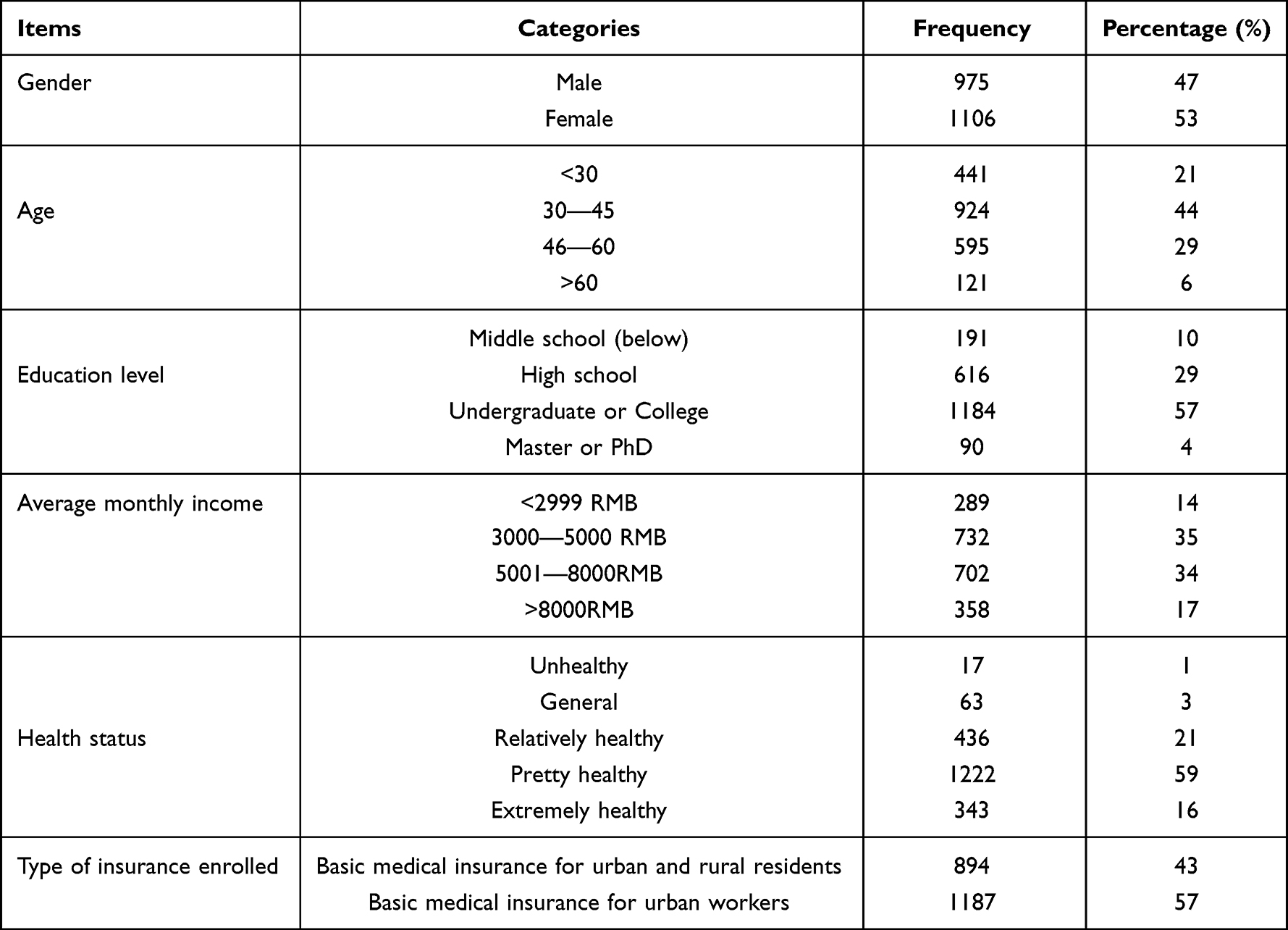

Among the valid responses, 975 were male and 1106 were female; most (73%) were concentrated in the 31–59 year age range; 90% had a high school (secondary school) education or above; the most common average monthly income was RMB 3000–8000; most were in a healthy state, and all of those surveyed had health care insurance. The descriptive statistics of the sample are detailed in Table 1.

|

Table 1 Descriptive Statistics of Survey Respondents |

Variable Measurement

Based on the above research hypotheses and referring to expert consultation and the existing literature, a scale to measure the factors that influence whistleblowing on health care insurance fraud is shown in Table 2. The five-point Likert scale is adopted for each question, with “1–5” representing five logical options of “strongly disagree, do not agree, neither agree nor disagree, somewhat agree, strongly agree”, respectively, and the respondents make their choices according to what they perceive.

|

Table 2 Main Variables and Associated Survey Questions for Motivation, Opportunity, and Ability |

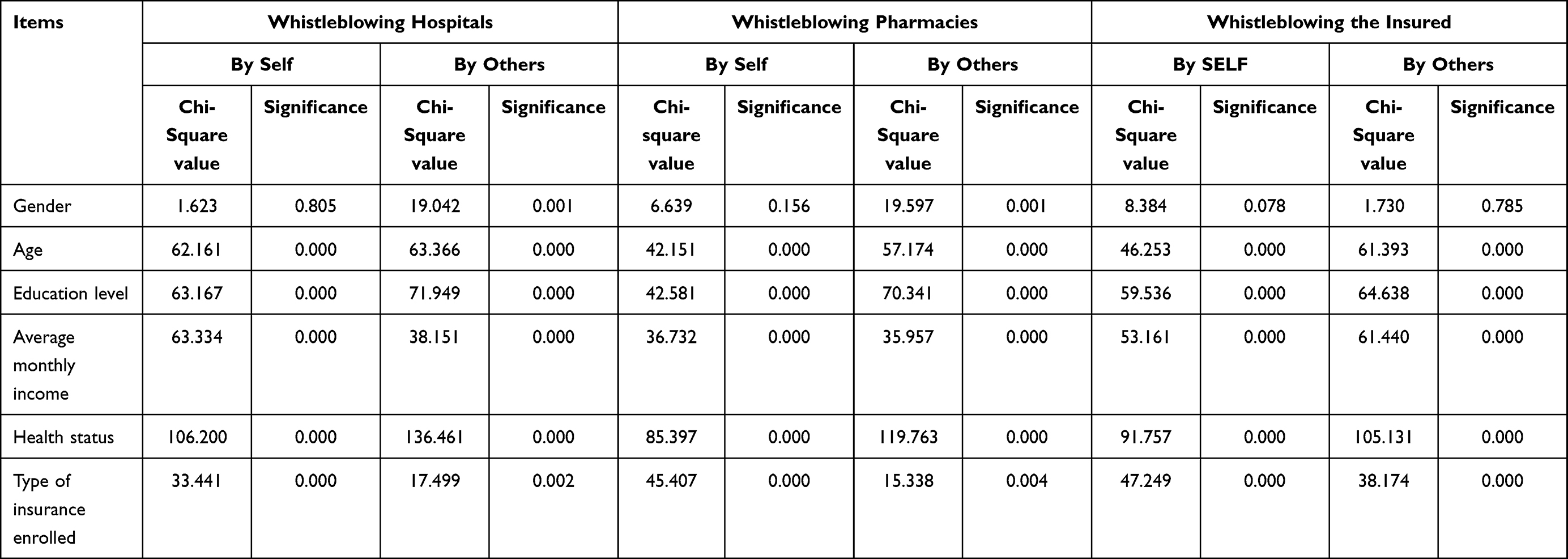

We now seek to determine whether there are differences in whistleblowing behaviors among citizens with varying demographic characteristics. Table 3 shows that there are significant differences by age, education level, average monthly income, health status, and type of insurance in whistleblowing behavior, while differences in gender are not statistically significant.

|

Table 3 Analysis of Whistleblowing Behavior Across Demographic Characteristics |

Empirical Results

Measurement Model

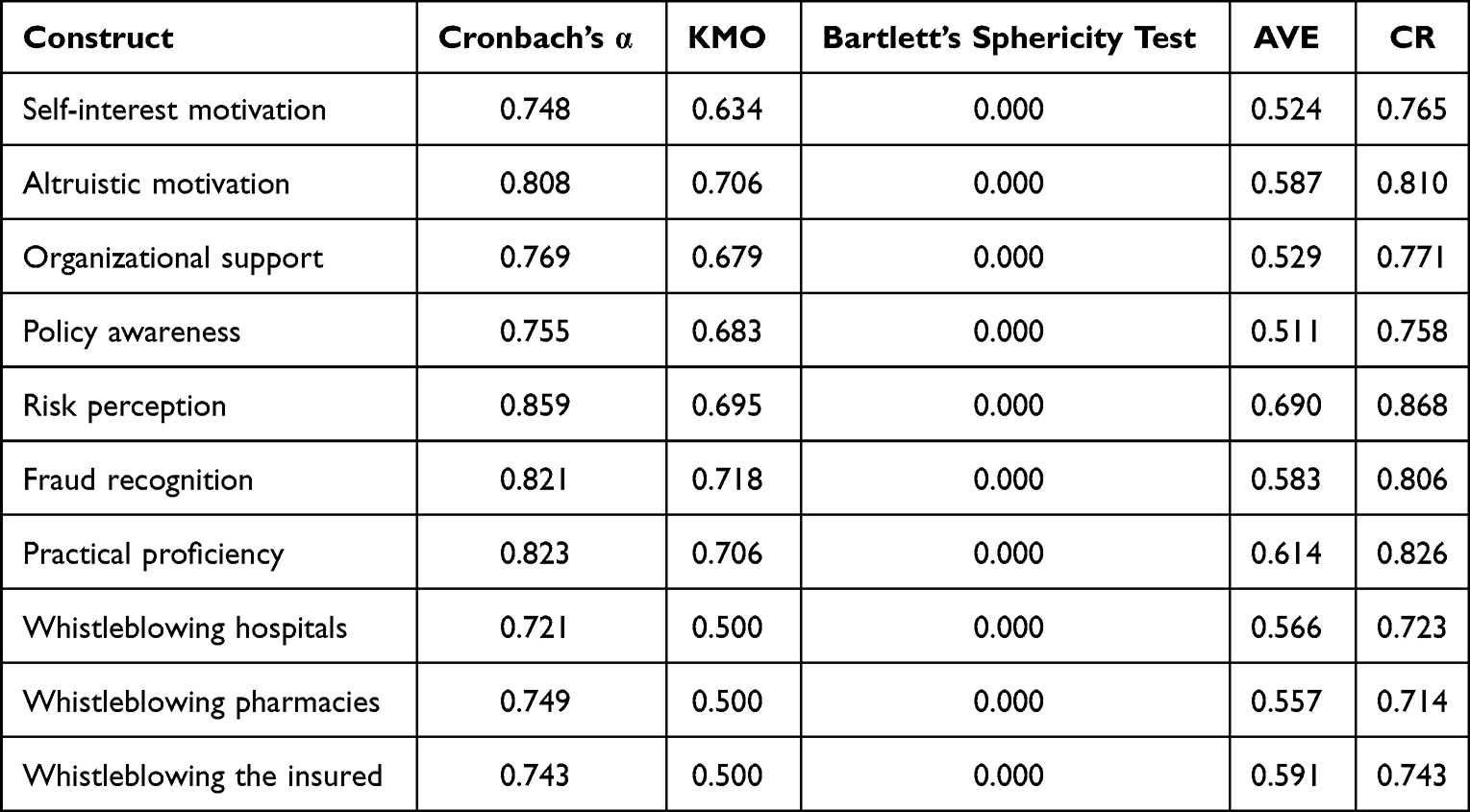

To ensure that the structural model is practically meaningful, the reliability and validity of a dataset need to satisfy the following conditions. Cronbach’s alpha (Cronbach’s α) is an important reference indicator to test the internal consistency of a scale or construct that should be no less than 0.70; the combined reliability (CR) is a criterion for judging the intrinsic quality of the model. If the CR for each latent variable is greater than 0.6, which means the intrinsic quality of the measurement model is favorable. From Table 4, Cronbach’s α for the constructed terms ranging from 0.721 to 0.859, and the CR value was between 0.714 and 0.868, indicating that the measurement model has more confidence and the internal consistency is high.

|

Table 4 Fitness of the Measurement Model |

Regarding the validity test, firstly, exploratory factor analysis (EFA) was used to analyze the questionnaire data, and the results showed that the Kaiser Meyer Olkin (KMO)measures reached above 0.5, and the p-values of Bartlett’s spherical test were all less than 0.001, indicating that the questionnaire data collected in this study were suitable for factor analysis. Next, convergent validity analysis (CFA) was conducted on the questionnaire data using validated factor analysis. Table 4 presents the average extracted variance (AVE) of the measurement indexes maxed out at 0.690 and mined at 0.511, which met the criterion of AVE greater than 0.5, while the CR all exceeded their threshold value of 0.6, indicating that the scale data possessed rather better convergent validity.71,72

Structural Model

We used covariance-based structural equation modeling to test the research hypotheses for how motivation, opportunity, and ability might affect whistleblowing behavior, the fitting efficacy of which was measured on a series of metrics, including the comparative fit index (CF=0.9), the incremental fit index (IFI=0.9), parsimony goodness of fit index (PGFI=0.6), and the parsimony-adjusted normed fit index (PNFI=0.7). All of the fitness indices of the model are within the ideal range, which indicates that the actual data are well fitted with the theoretical module constructed above.73,74

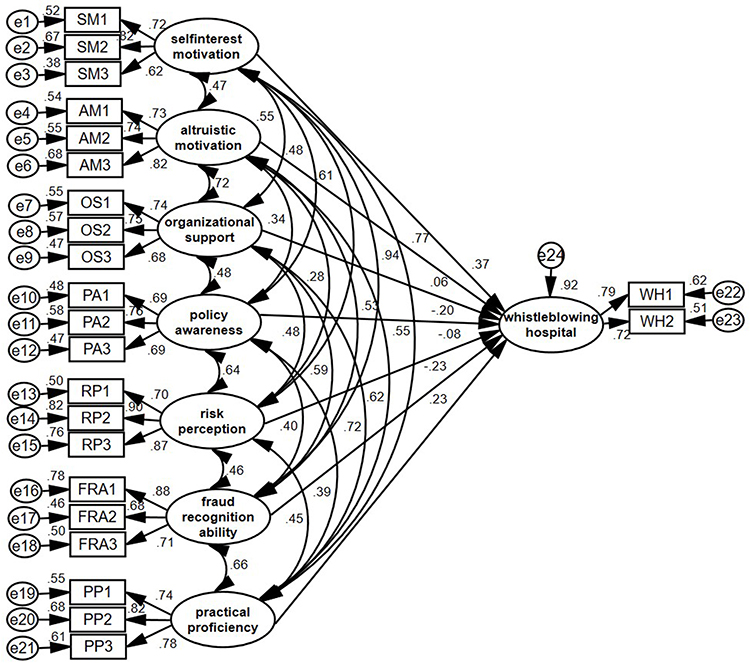

Whistleblowing Hospitals

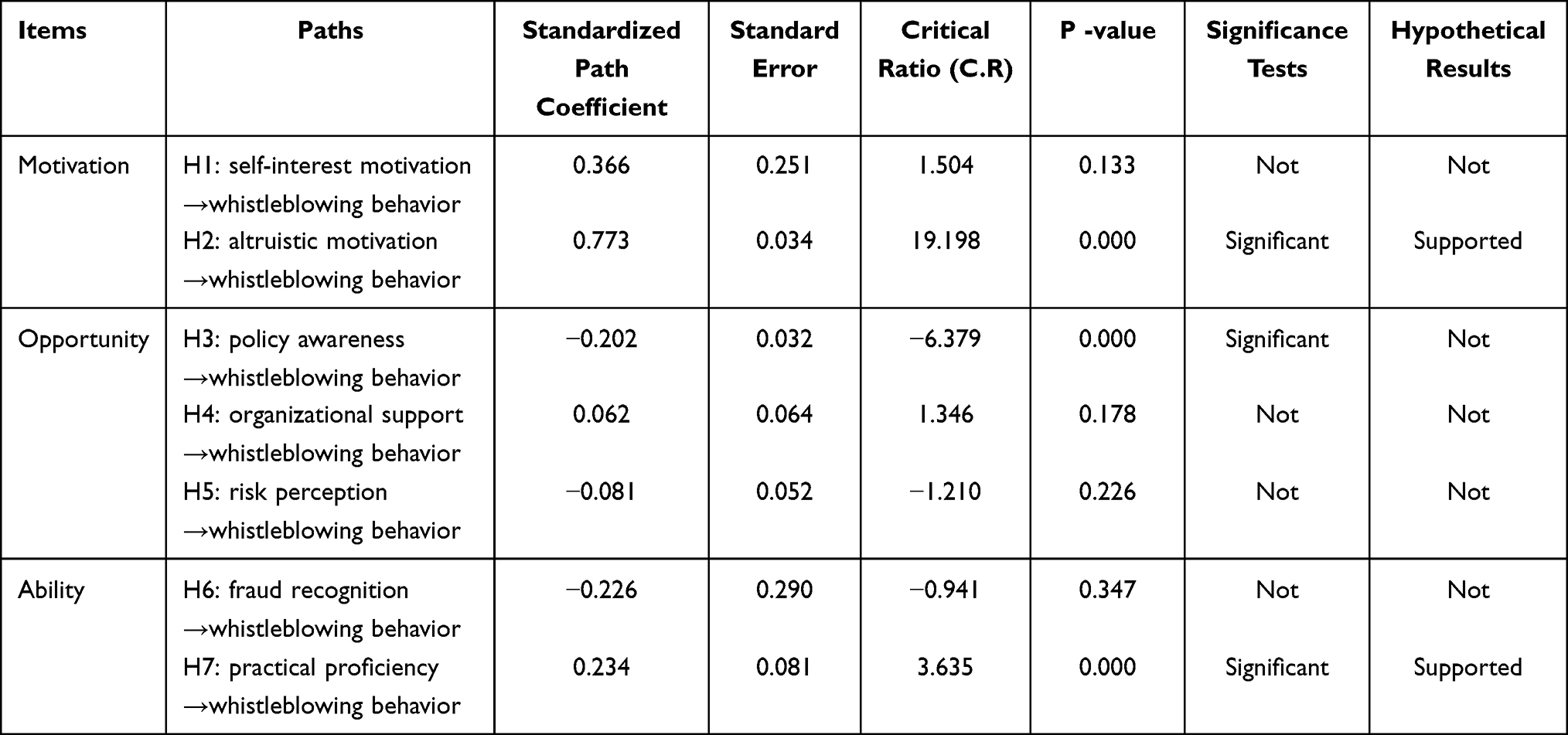

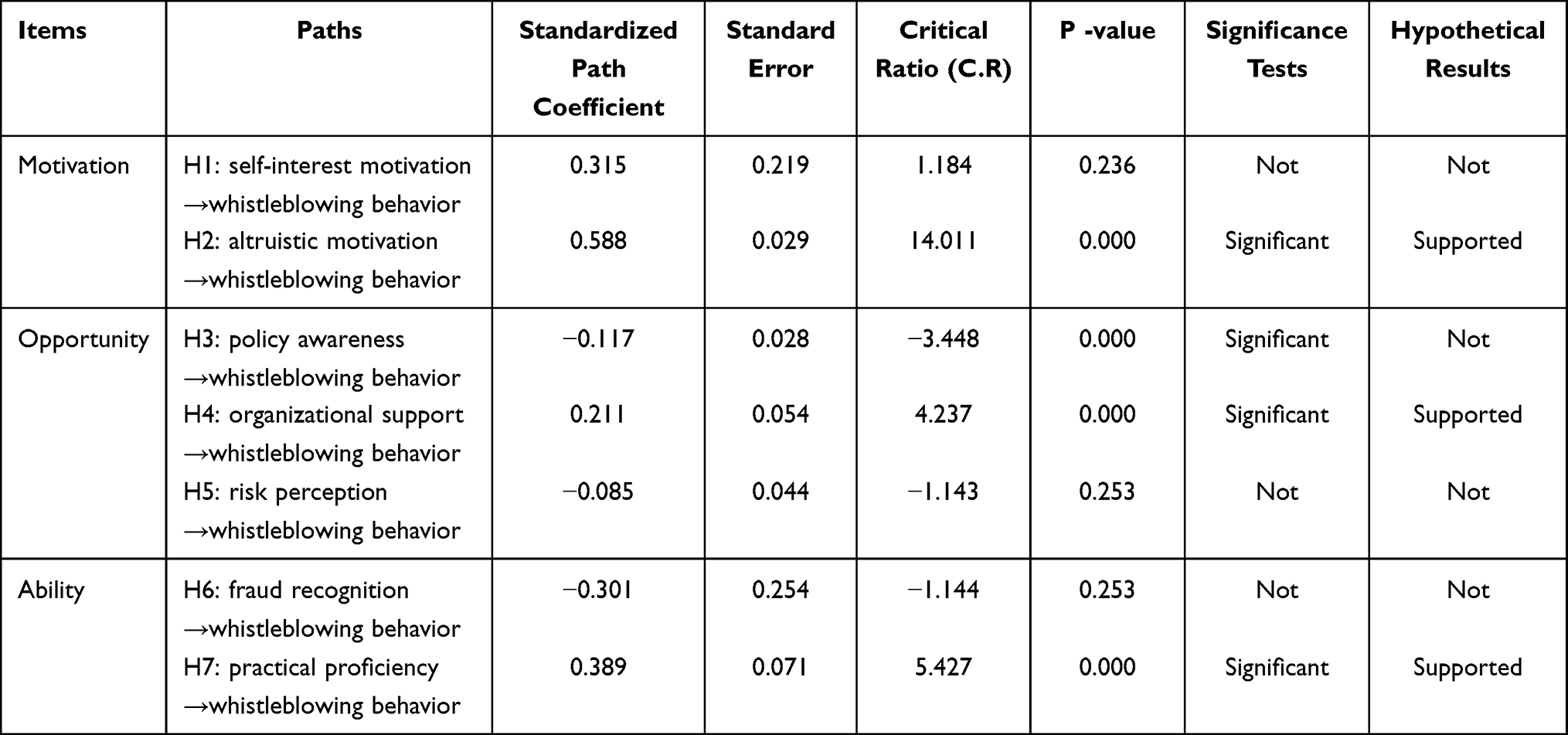

The effects of each factor on insurance fraud whistleblowing practices in hospitals are portrayed in Table 5 and Figure 5. It can be seen from Table 5 that altruistic motivation (p<0.001, β=0.773) and practical proficiency (p<0.001, β=0.234) significantly and positively affect whistleblowing behavior, thus supporting H2 and H7. In H4, we predicted that higher policy awareness (p<0.001, β=−0.202) would increase the whistleblowing rate on insurance fraud practices, but instead of supporting this positive effect, it was negative. When testing the impacts of self-interest motivation (p>0.05), organizational support (p>0.05), risk perception (p>0.05), and the ability to recognize fraud (p>0.05) on whistleblowing behavior, none were found to play a significant role, thus making H1, H4, H5, and H6 invalid.

|

Table 5 Path Estimation and Hypothesis Tests (for Whistleblowing Hospitals) |

|

Figure 5 Structural pathway for whistleblowing hospital. |

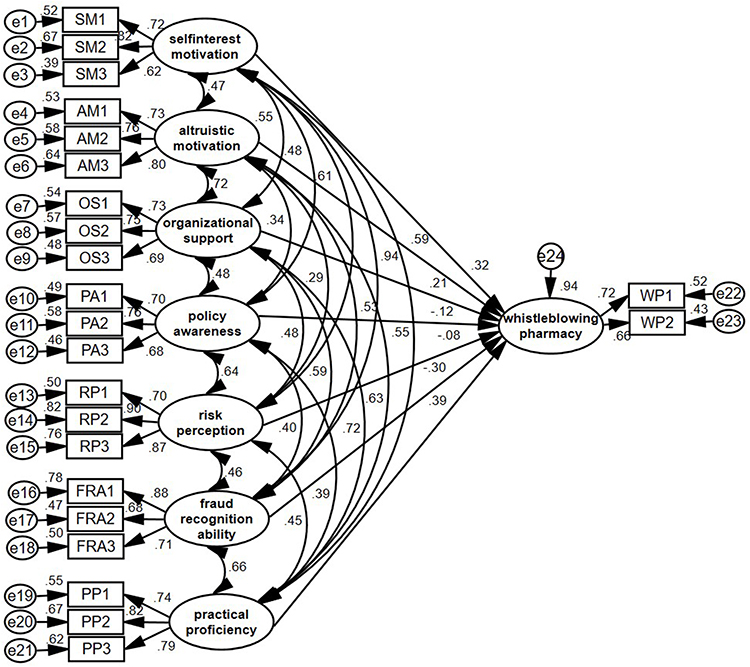

Whistleblowing Pharmacy

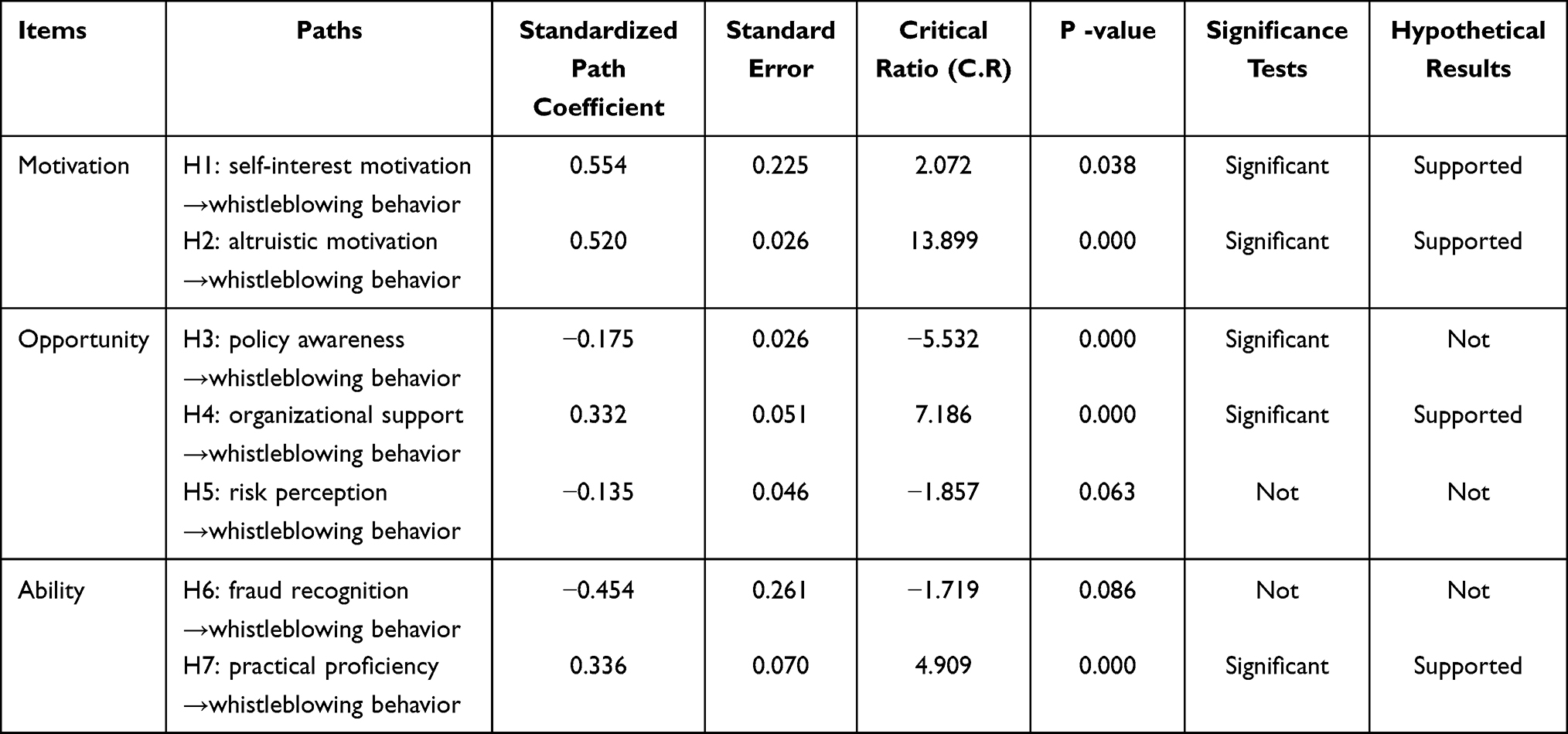

We proposed that motivation positively affects blowing the whistle on pharmaceutical fraud, as shown in Table 6 and Figure 6, where it can be seen that altruistic motivation is significantly related to whistleblowing behavior, thus supporting H2 (p<0.001, β=0.588). However, self-interest motivation (p>0.05) was not tested and therefore does not support H1. Likewise, there is no significant correlation between policy awareness (p>0.05), risk perception (p>0.05), and the ability to recognize fraud (p>0.05) and whistleblowing behavior, which does not support H3, H5, and H6. The positive impact of organizational support (p<0.001, β=0.211) and practical proficiency (p<0.001, β=0.389) support both H4 and H7.

|

Table 6 Path Estimation and Hypothesis Tests (for Whistleblowing Pharmacy) |

|

Figure 6 Structural pathway for whistleblowing pharmacy. |

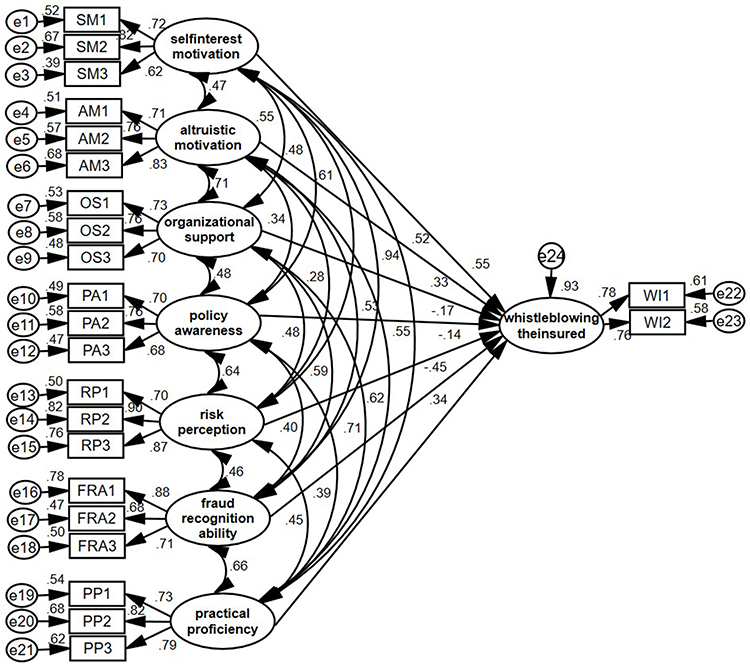

Whistleblowing the Insured

Table 7 and Figure 7 depicts that at the level of motivation, there was a significant positive correlation between self-interested motivation (p<0.05, β=0.554), altruistic motivation (p<0.001, β=0.520), and whistleblowing among the insured, which supports H1 and H2. With regard to opportunity, organizational support (p<0.001, β=0.332) was significantly positive for whistleblowing behavior, while the impact of risk perception was statistically nonsignificant (p>0.05), and policy knowledge shows a clear negative relationship with it (p<0.001, β=−0.175). Therefore, we assume that H4 is valid, but H3 and H5 are not. In terms of ability, the hypothesis regarding the positive effect on practice proficiency was verified (p<0.001, β=0.336), and H7 was supported, while that of the ability to recognize fraud was nonsignificant (p>0.05) and H6 was unsupported.

|

Table 7 Path Estimation and Hypothesis Tests (Whistleblowing Among the Insured) |

|

Figure 7 Structural pathway for whistleblowing the insured. |

Discussion and Policy Implications

Discussion

This study presents an empirical analysis of the underlying factors that shape whistleblowing behavior by extending the MOA framework. Meanwhile, an empirical analysis reinforces the applicability and reliability of the MOA framework in predicting individual behavior. A hypothesized impact of only some of those variables on whistleblowing behavior is supported in the current research.

If potential whistleblowers are unaware of what the policy contains, they might not engage with it.40 Contrary to the assertion set forth in H3, policy awareness not only failed to promote citizens’ whistleblowing on fraudulent activity involving health care insurance in hospitals, pharmacies, and the insured but in fact, had a dampening role. An analysis of the survey results revealed that the reason is that the greater the awareness of the whistleblower reward policy, the more individuals can notice problems associated with setting harsh reward thresholds. If rewards are only granted in the event that the information is verified to be true, enthusiasm for blowing the whistle on fraud is likely to be reduced.

Experience and previous studies have shown that personal risk may be the most prominent factor affecting whistleblowers’ decisions.38,45,75 However, our empirical analysis revealed that risk perception would not be a disincentive for whistleblowing behavior, which is inconsistent with H5. It is possible that departments at all levels strictly act in accordance with the law to protect the legitimate rights and interests of and not disclose information related to whistleblowers, and any damage done to their interests will be handled under the relevant provisions. Similarly, findings from an empirical analysis using structural equation modeling did not support the assumptions regarding the ability to recognize fraud on whistleblowing behavior stated in H6. Given the opaque and specialized nature of health care insurance fraud, it follows that potential whistleblowers are currently ill-equipped to accurately identify the targets of fraud with respect to hospitals, pharmacies, and the insured as well as when and how it occurs, thus failing to incentivize whistleblowing.

The catalytic role of self-interested and altruistic motivation, organizational support, and practical proficiency in whistleblowing has been recognized by many scholars over the years46,51 In addition, this study further found that their specific pathways of influence vary. The self-interest motivation’s (H1) specific pathway of impact occurs only when the insured blow the whistle on fraud, but not for hospitals and pharmacies. Due to information asymmetries, it may be easier to successfully blow the whistle—and thus to receive a whistleblower reward—on insurance fraud among the insured compared to in hospitals and pharmacies. Potential whistleblowers are more likely to participate in anti-fraud efforts when the available organizational support can meet their socio-emotional needs and provide the relevant resources and help. It is worth noting that organizational support (H4) works for blowing the whistle on fraudulent activities in pharmacies and among the insured, but has no effect on hospitals. The reason for this finding is most likely the lack of understanding and clinical knowledge among citizens, the failure of organizations to provide effective guidance on hospital platforms, and inadequate organizational support.

Both altruistic motivation and practical proficiency produce a favorable influence on whistleblowing behavior while targeting hospitals, pharmacies, and the insured for health care insurance fraud, which supports H2 and H7. Potential whistleblowers are more inclined to focus on the social benefits gained by whistleblowing. In addition, one of the necessary competencies for potential whistleblowers is familiarity with how the system operates, which will influence one’s whistleblowing behavior.

Policy Implications

Participation in health care insurance anti-fraud efforts is both necessary and possible. To ensure that the value of the whistleblower reward policy is fully realized, it is critical to transform the potential whistleblower’s intention into action, the nature of which is the focus of this research. Hence, several noteworthy references for policymakers may be provided herein.

First, it is advisable to optimize the whistleblower reward policy. Specifically, close attention should be paid to the manner with which rewards are granted, and we suggest that whistleblowers should be awarded with honorary titles such as “advanced and outstanding citizen.” Given that whistleblower rewards are only granted after fraud has been definitively proven, we advise that all projects which can provide clues after investigation should be rewarded to guarantee that whistleblowers are properly rewarded. In particular, adjusting the stipulation that rewards are a certain percentage of the amount recovered in the case could also be incorporated to maximize the social impact of whistleblowing.76

Second, the whistleblowing infrastructure can be improved by taking the receiving agencies as an entry point. The fundamental constraint on the viability of the whistleblower system lies in the protection of whistleblowers; otherwise, higher rewards are unlikely to encourage potential whistleblowers to come forward. At present, citizens are not concerned with the possible risks that whistleblowing may bring, thus any follow-up work should consolidate and improve the whistleblower safety protection system by strengthening the confidentiality of the existing whistleblowing channels. Moreover, it is advisable to establish reception agencies with full-time staff to communicate with whistleblowers and promptly answer their questions, which will enhance the whistleblowers’ sense of trust in and reliance on regulators.77

Third, procedural rules should be established for the whistleblowing system. Whistleblowing on specific links and procedural steps as well as the rights and obligations of the whistleblower, receiving authorities in the form of legal provisions to ensure that citizens are in accordance with the statutory unified procedures for processing, whistleblowing materials can be carefully reviewed, cases can be handled in a timely manner, and the relationship between the whistleblower and the receiving authorities is positive and productive. Furthermore, it is necessary to grant whistleblowers the right to file administrative lawsuits, which requires that receiving organizations fulfill their statutory duties by bearing an important social responsibility and overcoming the arbitrariness of industry regulation.

Finally, given the current deficiencies in citizens’ ability to recognize health care insurance fraud, anti-fraud education efforts should be strengthened in the future. On the one hand, the process of occurrence–detection–whistleblowing–acceptance of fraud can be displayed through scenario simulation, so that citizens can learn by example. On the other hand, the educational materials should be enriched. Not only is it necessary to leverage the Internet to spread quickly and to a large audience, but it is also necessary to use public service platforms like buses and subways to set up banners, which may improve the ability to accurately identify health care insurance fraud.

Conclusion

The present study proposes an integrated MOA framework with definitions and measurable dimensions for its three components, thereby providing researchers with a mechanism to systematically analyze the complexity of whistleblowing behavior from citizens’ perspective. Our empirical findings demonstrate both the theoretical and empirical necessity to extend the basic MOA framework to explain complex behavior. They also provide evidence for investigating the determinants of health care insurance fraud whistleblowing by citizens, and ultimately clarify that reducing constraints on whistleblowing behavior can be done using the elements identified by the integrated MOA framework.

Limitations and Future Research

While this paper enriches our understanding of the factors that influence whistleblowing behavior, it still has some limitations, which also provide opportunities for further research.

Investigating the distribution area is crucial to obtaining quality responses. Therefore, future research should extend the regional scope to include all urban areas across Jiangsu and other provinces in China for comparison purposes. Furthermore, examining the factors that currently influence whistleblowing behavior may not be comprehensive enough. Beyond the psychosocial factors already considered in this paper, the impact of policy satisfaction, situational judgment, trust perception, and future expectations on whistleblowing behavior also deserve further exploration in subsequent studies. As blowing the whistle on health care insurance fraud is still in its infancy in China, there are many other topics that have not been explored to date. Overall, future research should integrate more variables within a broader range of inquiry to enhance the representativeness and veracity of the results.

Despite these limitations, we believe that our framework and findings will prove useful to policymakers who seek to achieve alignment between whistleblowing intentions and actions. Likewise, we hope to inspire further research to address the important issue of health care insurance fraud.

Ethics Statement

This study was approved by the Ethics Committee of Jiangsu University, Zhenjiang, Jiangsu Province, China. The participants provided their written informed consent to participate in this study.

Funding

This study was supported by the National Social Science Foundation of China [grant number 19BGL200] and the Jiangsu Provincial Postgraduate Research Innovation Program in 2021 [grant number KYCX21_3318].

Disclosure

The authors report no conflicts of interest in this work.

References

1. Kose I, Gokturk M, Kilic K. An interactive machine-learning-based electronic fraud and abuse detection system in healthcare insurance. Appl Soft Computing. 2015;36:283–299. doi:10.1016/j.asoc.2015.07.018

2. Hill C, Coustasse HA. Medicare Fraud in the United States: can it Ever be Stopped? Health Care Manager. 2014;33:254–260. doi:10.1097/HCM.0000000000000019

3. Alonazi WB. Fraud and Abuse in the Saudi Healthcare System: a Triangulation Analysis. J Health Care Org Provision Financing. 2020;1:57.

4. Kang H, Hong J, Lee K, et al. The effects of the fraud and abuse enforcement program under the National Health Insurance program in Korea. Health Policy. 2010;95:41–49. doi:10.1016/j.healthpol.2009.10.003

5. Putter R, Naidoo S. Dental fraud in South Africa 2007-2015. South African Dental J. 2018;73:546–553. doi:10.17159/2519-0105/2018/v73no9a1

6. Zhang CH, Xiao XY, Wu C. Medical Fraud and Abuse Detection System Based on Machine Learning. Int J Environ Res Public Health. 2020;17:548.

7. Yulin Qiu ZW. Maintaining Principle, Progress and Innovation: the Development Ideas of Health Security during the 14th Five-Year Plan Period. Admin Reform. 2021;4:32–41.

8. Crea G, Galizzi MM, Linnosmaa I, et al. Physician altruism and moral hazard: (no) Evidence from Finnish national prescriptions data. J Health Econ. 2019;65:153–169. doi:10.1016/j.jhealeco.2019.03.006

9. Abdallah A, Maarof MA, Zainal A. Fraud detection system: a survey. Journal of Network and Computer Applications. 2016;68:90–113. doi:10.1016/j.jnca.2016.04.007

10. Joudaki H, Rashidian A, Minaei-Bidgoli B, et al. Improving Fraud and Abuse Detection in General Physician Claims: a Data Mining Study. Int J Health Policy Manag. 2016;5:165–172. doi:10.15171/ijhpm.2015.196

11. Meyers TJ. Examining the network components of a Medicare fraud scheme: the Mirzoyan-Terdjanian organization. Crime Law Social Change. 2017;68:251–279. doi:10.1007/s10611-017-9689-z

12. Han JQ, Zhang XD, Meng YY. Out-Patient Service and in-Patient Service: the Impact of Health Insurance on the Healthcare Utilization of Mid-Aged and Older Residents in Urban China. Risk Manag and Healthcare Policy. 2020;13:2199–2212. doi:10.2147/RMHP.S273098

13. Berwick DM, Hackbarth AD. Eliminating Waste in US Health Care. J Amer Med Assoc. 2012;307:1513–1516. doi:10.1001/jama.2012.362

14. Legotlo TG, Mutezo A. Understanding the types of fraud in claims to South African medical schemes. Samaj South Afr Med J. 2018;108:299–303. doi:10.7196/SAMJ.2018.v108i4.12758

15. Jator EK, Hughley K. ABO/Rh Testing, Antibody Screening, and Biometric Technology as Tools to Combat Insurance Fraud: an Example and Discussion. Lab Medicine. 2014;45:E3–E7. doi:10.1309/LMIEC52ZF7RLLURK

16. Tavaglione N, Hurst SA. Why Physicians Ought to Lie for Their Patients. Amer J Bioethics. 2012;12:4–12. doi:10.1080/15265161.2011.652797

17. Auener S, Kroon D, Wackers E, et al. COVID-19: a Window of Opportunity for Positive Healthcare Reforms. Int J Health Policy Manag. 2020;9:419–422. doi:10.34172/ijhpm.2020.66

18. Shrank WH, Rogstad TL, Parekh N. Waste in the US Health Care System: estimated Costs and Potential for Savings. J Amer Med Assoc. 2019;322:1501–1509. doi:10.1001/jama.2019.13978

19. Boumil SJ, Mariani A, Boumil MM, et al. Whistleblowing in the pharmaceutical industry in the United States, England, Canada, and Australia. J Public Health Policy. 2010;31:17–29. doi:10.1057/jphp.2009.51

20. Mackey TK, Liang BA. Combating healthcare corruption and fraud with improved global health governance. BMC Int Health Human Rights. 2012;12:58.

21. Okafor ON, Adebisi FA, Opara M, et al. Deployment of whistleblowing as an accountability mechanism to curb corruption and fraud in a developing democracy. Account Auditing Accountability J. 2020;33:1335–1366. doi:10.1108/AAAJ-12-2018-3780

22. Rashidian A, Joudaki H, Vian T. No Evidence of the Effect of the Interventions to Combat Health Care Fraud and Abuse: a Systematic Review of Literature. PLoS One. 2012;7:325.

23. Carson TL, Verdu ME, Wokutch RE. Whistle-blowing for profit: an ethical analysis of the federal false claims act. J Business Ethics. 2007;77(3):361–376. doi:10.1007/s10551-007-9355-y

24. Kesselheim AS, Studdert DM. Whistleblower-initiated enforcement actions against health care fraud and abuse in the United States, 1996 to 2005. Ann Int Med. 2008;149:342–W371. doi:10.7326/0003-4819-149-5-200809020-00009

25. Huang H. Taking a new start, meeting new challenges and pushing forward with new leaps in fund supervision. Chin Health Insurance. 2021;4:6–8.

26. Blenkinsopp J, Snowden N, Mannion R, et al. Whistleblowing over patient safety and care quality: a review of the literature. J Health Org Manag. 2019;33:737–756. doi:10.1108/JHOM-12-2018-0363

27. Harrison R, Birks Y, Hall J, et al. The contribution of nurses to incident disclosure: a narrative review. Int J Nursing Stud. 2014;51:334–345. doi:10.1016/j.ijnurstu.2013.07.001

28. Jackson D, Hickman LD, Hutchinson M, et al. Whistleblowing: an integrative literature review of data-based studies involving nurses. Contemp Nurse. 2014;48:240–251. doi:10.1080/10376178.2014.11081946

29. Okuyama A, Wagner C, Bijnen B. Speaking up for patient safety by hospital-based health care professionals: a literature review. Bmc Health Services Res. 2014;14:887.

30. Ahern K. The beliefs of nurses who were involved in a whistleblowing event. J Adv Nursing. 2002;38:303–309. doi:10.1046/j.1365-2648.2002.02180.x

31. Rao PR. Ethical Considerations for Healthcare Organizations. Semi Speech Lang. 2020;41:266–278. doi:10.1055/s-0040-1710323

32. Hannigan NS. Blowing the whistle on healthcare fraud: should I? J Amer Acad Nurse Practitioners. 2006;18:512–517. doi:10.1111/j.1745-7599.2006.00175.x

33. Ion R, Smith K, Moir J, et al. Accounting for actions and omissions: a discourse analysis of student nurse accounts of responding to instances of poor care. J Adv Nursing. 2016;72:1054–1064. doi:10.1111/jan.12893

34. Roberts M, Ion R. A critical consideration of systemic moral catastrophe in modern health care systems: a big idea from an Arendtian perspective. Nurse Educ Today. 2014;34:673–675. doi:10.1016/j.nedt.2014.01.012

35. Lim CR, Zhang MWB, Hussain SF, et al. The Consequences of Whistle-blowing: an Integrative Review. J Patient Safety. 2021;17:e497–e502. doi:10.1097/PTS.0000000000000396

36. Ion R, Smith K, Nimmo S, et al. Factors influencing student nurse decisions to report poor practice witnessed while on placement. Nurse Educ Today. 2015;35:900–905. doi:10.1016/j.nedt.2015.02.006

37. Kesselheim AS, Studdert DM, Mello MM. Whistle-Blowers’ Experiences in Fraud Litigation against Pharmaceutical Companies. New Eng J Med. 2010;362:1832–1839. doi:10.1056/NEJMsr0912039

38. Peters K, Luck L, Hutchinson M, et al. The emotional sequelae of whistleblowing: findings from a qualitative study. J Clin Nursing. 2011;20:2907–2914. doi:10.1111/j.1365-2702.2011.03718.x

39. Jackson D, Peters K, Andrew S, et al. Trial and retribution: a qualitative study of whistleblowing and workplace relationships in nursing. Contemp Nurse. 2010;36:34–44. doi:10.5172/conu.2010.36.1-2.034

40. Fleming CA, Humm G, Wild JR, et al. Supporting doctors as healthcare quality and safety advocates: recommendations from the Association of Surgeons in Training (ASiT). Int J Surgery. 2018;52:349–354. doi:10.1016/j.ijsu.2018.02.002

41. DesRoches CM, Rao SR, Fromson JA, et al. Physicians’ Perceptions, Preparedness for Reporting, and Experiences Related to Impaired and Incompetent Colleagues. J Amer Med Assoc. 2010;304:187–193. doi:10.1001/jama.2010.921

42. Goel RK. Medical professionals and health care fraud: do they aid or check abuse? Manag Decision Econ. 2020;41:520–528. doi:10.1002/mde.3117

43. Dalton D, Radtke RR. The Joint Effects of Machiavellianism and Ethical Environment on Whistle-Blowing. J Business Ethics. 2013;117:153–172. doi:10.1007/s10551-012-1517-x

44. Cheng X, Karim KE, Lin KJ. A cross-cultural comparison of whistleblowing perceptions. Int J Manag Decision Making. 2015;14:15–31. doi:10.1504/IJMDM.2015.067374

45. Rauwolf P, Jones A. Exploring the utility of internal whistleblowing in healthcare via agent-based models. BMJ Open. 2019;9:936.

46. Moore LM. E “Is inadequate response to whistleblowing perpetuating a culture of silence in hospitals?”. Clin Gov. 2010;15:166–178. doi:10.1108/14777271011063805

47. Nasrin Alinaghian A. Factors influencing whistle-blowing in the Iranian health system. J Human Behav Soc Environ. 2018;28:177–192. doi:10.1080/10911359.2017.1349703

48. Kuilman L, Jansen G, Mulder LB, et al. Facilitating and motivating factors for reporting reprehensible conduct in care: a study among nurse practitioners and physician assistants in the Netherlands. J Eval Clin Practice. 2021;27:776–784. doi:10.1111/jep.13462

49. Mansbach A, Ziedenberg H, Bachner YG. Nursing students’ willingness to blow the whistle. Nurse Educ Today. 2013;33:69–72. doi:10.1016/j.nedt.2012.01.008

50. Ohnishi K, Hayama Y, Asai A, et al. The process of whistleblowing in a Japanese psychiatric hospital. Nurs Ethics. 2008;15:631–642. doi:10.1177/0969733008092871

51. Pohjanoksa J, Stolt M, Suhonen R, et al. Wrongdoing and whistleblowing in health care. Journal of Advanced Nursing. 2019;75(7):1504–1517. doi:10.1111/jan.13979

52. Mansbach A, Bachner YG. Internal or external whistleblowing: nurses’ willingness to report wrongdoing. Nurs Ethics. 2010;17(4):483–490. doi:10.1177/0969733010364898

53. Mannion R, Davies HT. Cultures of Silence and Cultures of Voice: the Role of Whistleblowing in Healthcare Organisations. Int J Health Policy Manage. 2015;4(8):503–505. doi:10.15171/ijhpm.2015.120

54. MacInnis DJ, Moorman C, Jaworski BJ. Enhancing and Measuring Consumers‘ Motivation, Opportunity, and Ability to Process Brand Information from Ads. J Marketing. 1991;55(4):32–53. doi:10.2307/1251955

55. Hasbullah NN, Sulaiman Z, Masood A, et al. Drivers of Sustainable Apparel Purchase Intention: an Empirical Study of Malaysian Millennial Consumers. Sustainability. 2022;14:87.

56. Bos C, van der Lans IA, van Rijnsoever FJ, et al. Heterogeneity in barriers regarding the motivation, the opportunity and the ability to choose low-calorie snack foods and beverages: associations with real-life choices. Public Health Nutr. 2016;19(9):1584–1597. doi:10.1017/S1368980015002517

57. Siemsen E, Roth AV, Balasubramanian S. How motivation, opportunity, and ability drive knowledge sharing: the constraining-factor model. J Oper Manag. 2008;26(3):426–445. doi:10.1016/j.jom.2007.09.001

58. Kim KY, Pathak S, Werner S. When do international human capital enhancing practices benefit the bottom line? An ability, motivation, and opportunity perspective. J Int Business Stud. 2015;46(7):784–805. doi:10.1057/jibs.2015.10

59. Hallahan K. Enhancing motivation, ability, and opportunity to process public relations messages. Public Relations Rev. 2000;26(4):463–480. doi:10.1016/S0363-8111(00)00059-X

60. Hung K, Sirakaya-Turk E, Ingram LJ. Testing the Efficacy of an Integrative Model for Community Participation. J Travel Res. 2011;50(3):276–288. doi:10.1177/0047287510362781

61. Leung XY, Bai B. How Motivation, Opportunity, and Ability Impact Travelers‘ Social Media Involvement and Revisit Intention. J Travel Tourism Marketing. 2013;30(1–2):58–77. doi:10.1080/10548408.2013.751211

62. Singh SK, Del Giudice M, Chierici R, et al. Green innovation and environmental performance: the role of green transformational leadership and green human resource management. Tech Forecasting Social Change. 2020;150.

63. Li D, Xu X, Chen C, et al. Understanding energy-saving behaviors in the American workplace: a unified theory of motivation, opportunity, and ability. Energy Res Social Sci. 2019;51:198–209. doi:10.1016/j.erss.2019.01.020

64. Yu W, Chavez R, Feng M, et al. Green human resource management and environmental cooperation: an ability-motivation-opportunity and contingency perspective. Int J Production Econ. 2020;219:224–235. doi:10.1016/j.ijpe.2019.06.013

65. Dozier JB, Miceli MP. Potential Predictors of Whistle-Blowing: a Prosocial Behavior Perspective. Acad Manag Rev. 1985;10(4):823–836. doi:10.2307/258050

66. MacCallum RC, Austin JT. Applications of structural equation modeling in psychological research. Annual Rev Psychol. 2000;51(1):201–226. doi:10.1146/annurev.psych.51.1.201

67. Maslowsky J, Jager J, Hemken D. Estimating and interpreting latent variable interactions: a tutorial for applying the latent moderated structural equations method. Int J Behav Dev. 2015;39(1):87–96. doi:10.1177/0165025414552301

68. Bagozzi RP, Yi Y. Specification, evaluation, and interpretation of structural equation models. J Acad Marketing Sci. 2012;40(1):8–34. doi:10.1007/s11747-011-0278-x

69. Cho YJ, Song HJ. Determinants of Whistleblowing Within Government Agencies. Public Personnel Manag. 2015;44(4):450–472. doi:10.1177/0091026015603206

70. Keil M, Tiwana A, Sainsbury R, et al. Toward a Theory of Whistleblowing Intentions: a Benefit-to-Cost Differential Perspective. Decision Sci. 2010;41(4):787–812. doi:10.1111/j.1540-5915.2010.00288.x

71. Bentler PM, Bonett DG. Significance tests and goodness of fit in the analysis of covariance structures. Psychol Bulletin. 1980;88(3):588–606. doi:10.1037/0033-2909.88.3.588

72. Niemand T, Mai R. Flexible cutoff values for fit indices in the evaluation of structural equation models. J Acad Marketing Sci. 2018;46(6):1148–1172. doi:10.1007/s11747-018-0602-9

73. Steiger JH. Structural Model Evaluation and Modification: an Interval Estimation Approach. Multivariate Behav Res. 1990;25(2):173–180. doi:10.1207/s15327906mbr2502_4

74. Weston R, Gore PA. A brief guide to structural equation modeling. Counseling Psychol. 2006;34(5):719–751. doi:10.1177/0011000006286345

75. Latan H, Jabbour CJC, Ali M, et al. What Makes You a Whistleblower? A Multi-Country Field Study on the Determinants of the Intention to Report Wrongdoing. J Bus Ethics;2022. 1–21. doi:10.1007/s10551-022-05089-y

76. Seufen W. Research on the whistleblower system of social insurance anti-fraud. Theory J. 2019;3:130–136.

77. Antinyan A, Corazzini L, Pavesi F. Does trust in the government matter for whistleblowing on tax evaders? Survey and experimental evidence. J Economic Behav Org. 2020;171:77–95. doi:10.1016/j.jebo.2020.01.014

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.