")

Back to Journals » Psychology Research and Behavior Management » Volume 15

Who is More Likely to Report Medical Insurance Fraud in the Two Scenarios of Whether It Results in a Direct Loss of Individual Benefit? A Cross-Sectional Survey in China

Authors Zhang H, Zhang T, Shi Q, Liu J, Xu J, Zhang B, Wang H, Tian G, Wu Q , Kang Z

Received 24 May 2022

Accepted for publication 18 August 2022

Published 24 August 2022 Volume 2022:15 Pages 2331—2341

DOI https://doi.org/10.2147/PRBM.S375823

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Igor Elman

Hongyu Zhang,1,* Ting Zhang,1,* Qi Shi,1,* Jian Liu,1 Jinpeng Xu,1 Bokai Zhang,1 Haixin Wang,1 Guomei Tian,2,* Qunhong Wu,1 Zheng Kang1

1School of Health Management, Harbin Medical University, Harbin, Heilongjiang, People’s Republic of China; 2Department of Nuclear Medicine, The Fourth Hospital of Harbin Medical University, Harbin, Heilongjiang, People’s Republic of China

*These authors contributed equally to this work

Correspondence: Zheng Kang, School of Health Management, Harbin Medical University, Harbin, Heilongjiang, People’s Republic of China, Email [email protected]

Purpose: An individual’s willingness to report is largely related to whether he or she is a direct victim. This study takes two scenarios of whether medical insurance fraud results in a direct loss of personal benefit and explores the differences in individuals’ willingness to report and influencing factors in the two scenarios.

Methods: In this study, questionnaires were used and participants were selected from 571 individuals in eastern, central, and western China. Analysis was performed using descriptive statistics and logistic regression models.

Results: 51.0% of individuals were willing to report when no direct loss of personal benefit was caused, and conversely, 78.3% of individuals were willing to report when direct loss of personal benefit was caused. The factors influencing the attitude dimension of individuals toward whistleblowing behavior were consistent in the two scenarios. In contrast, there were significant differences among the influences in the perceived behavioral control, consequence perception, and subjective norm dimensions.

Conclusion: There were significant differences in the willingness of individuals to report medical insurance fraud and the factors influencing it in both scenarios. The most significantly influencing factor difference was perceived behavioral control, a dimension that had an effect only when it did not result in a direct loss of personal benefit. When an individual’s direct interests are at stake, the individual’s fear for his or her safety is not a deterrent to his or her willingness to report. And when there is no loss of direct personal benefit, individuals care more about government measures to protect whistleblowers. There are differences in the subjects that influence individuals’ willingness to report in the two scenarios. The factors influencing the attitude dimension are the same in both scenarios, and the more supportive the attitude toward the whistleblower, the stronger the individual’s willingness to report will be.

Keywords: whistleblowing willingness, loss of direct benefits, medical insurance fraud, individual

Introduction

Medical insurance fraud is a serious problem for countries around the world.1,2 Medical insurance funds around the world lose approximately $260 billion annually due to medical insurance fraud, equivalent to 6% of global health spending.3 Countries have attached great importance to the construction of medical insurance anti-fraud tools, among which the reporting of medical insurance fraud by people has become an important tool of great interest because it helps to detect medical insurance fraud early,4–6 and federal regulators in the United States value the information provided by whistleblowers on medical insurance fraud, and almost half of the fraud losses recovered between 1996 and 2005 came from lawsuits filed by whistleblowers.6 China also places great importance on individuals reporting medical insurance fraud.7 The study of people reporting medical insurance fraud has also become an important area of interest for scholars.5,6 People’s willingness to report is an inevitable stage in promoting the occurrence of whistleblowing behavior and is the core prerequisite for behavior to occur.8,9 It is worthwhile for the medical insurance field to explore research on individuals’ willingness to report medical insurance fraud.

An individual’s willingness to report may be more related to whether he or she is a direct victim. Studies in justice-related fields have shown that a victim is more inclined to report,10 while the reluctance of non-victims to report is a serious problem.11,12 Therefore, we hypothesize that whether people are direct victims of medical insurance fraud may have a key impact on their willingness to report. The purpose of this study is to focus on whether there are differences in individuals’ willingness to report medical insurance fraud between two scenarios of whether medical insurance fraud results in a direct loss of benefits to the individual. And analyze how the factors that influence an individual’s willingness to report differ in the two scenarios.

So far, the main areas and hot topics of international medical insurance anti-fraud research are focused on exploring effective medical insurance fraud identification and monitoring by building multiple models,13–15 the construction of anti-fraud laws and regulations.16 While much of the above research has been done in the area of medical insurance anti-fraud. However, few studies have examined whether there are differences in individuals’ willingness to report medical insurance fraud and the factors that influence it, in terms of two scenarios of whether individuals suffer a direct loss of benefits.

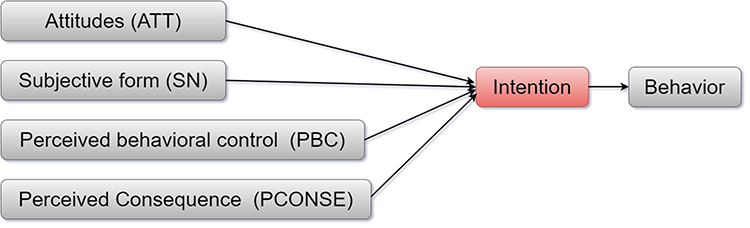

To the best of our knowledge, there are no studies at this time that specifically explore the factors influencing people’s willingness to report medical insurance fraud. This study uses the Theory of Planned Behavior (TPB) framework to explore the factors that influence willingness to report. Several studies have verified its explanatory power for behavior as well as willingness.17 TPB considers intention as the closest determinant of people’s behavior (Ajzen, 1991).8 The theory suggests that the intention to perform the behavior is predicted by three factors: Attitude toward the behavior (ATT), Subjective norm (SN), and Perceived behavioral control (PBC). Attitude toward the behavior (ATT) refers to a positive or negative evaluation of a person or a behavior. Subjective norm (SN) refers to the social pressure that people perceive when they decide whether or not to perform a certain behavior. Perceived behavioral control (PBC) refers to the perceived ease with which an individual performs a behavior and includes the resources, time, experience, information, opportunities, and abilities that would facilitate and hinder the degree of the individual’s intended behavior (Ajzen & Madden, 1986).18–20 The Perceived Consequences variable, which considers risky decisions, will also be introduced. This variable is derived from Triandis, who argues that any behavior can lead to positive or negative outcomes and that the perception of such outcomes directly affects an individual’s willingness to act.21 The specific theoretical framework is detailed in Figure 1.

|

Figure 1 Extending the Theory of Planned Behavior. |

Therefore, this study innovatively explores the differences in people’s willingness to report medical insurance fraud and the factors influencing it under two scenarios of whether medical insurance fraud causes direct harm to people’s interests. Explore further what factors contribute to the willingness to report. It can provide insight into the psychology of individuals facing wrongdoings from a microscopic perspective, and provide a reference for government departments when formulating relevant reporting policies.

Materials and Methods

Study Population and Sample

We used convenience sampling to collect 60 questionnaires for a pilot study as a way to improve questionnaire design and quality. A national cross-sectional survey study was conducted from February 19 to March 1, 2022, using a stratified random sampling method through a widely accepted online questionnaire platform in China. China is divided into eastern, central, and western regions based on economic development. Jiangsu, Liaoning, and Shandong provinces were selected to represent the eastern region. Heilongjiang and Shanxi provinces were selected as representatives of the central region. Shaanxi and Guizhou provinces were chosen to represent the western region. Survey respondents were selected to be residents aged 15 and older in mainland China who were eligible to participate in the survey anonymously. The introductory section of the questionnaire provided electronic informed consent before the response.

Only one response per participant, based on the IP address recorded in the questionnaire. A questionnaire was judged valid and included in the analysis if it was completed in more than 10 minutes, which was the minimum time our team tested to complete the questionnaire, and if two logical questions were answered logically. Otherwise, it is removed.

Measure

Dependent Variable

Willingness. willingness was a binary variable: yes or no. To measure the willingness of individuals to report medical insurance fraud under two scenarios of whether medical insurance fraud results in a direct loss of personal benefit. Two different medical insurance fund supervision scenarios were constructed. One is

How likely would you be to choose to report Medical insurance fraud if you found that someone else was committing it and not causing you a direct personal loss of benefits?

The second question is

If you found out that someone else was committing medical insurance fraud and causing you a direct personal loss of benefits, how likely would you be to report it?

The options for both questions were set to “not at all likely, unlikely, uncertain, more likely, and very likely”. The “not at all likely, unlikely, uncertain” is classified as unwilling to report, and the “more likely and very likely” is classified as willing to report.

Independent Variables

Demographics Variables

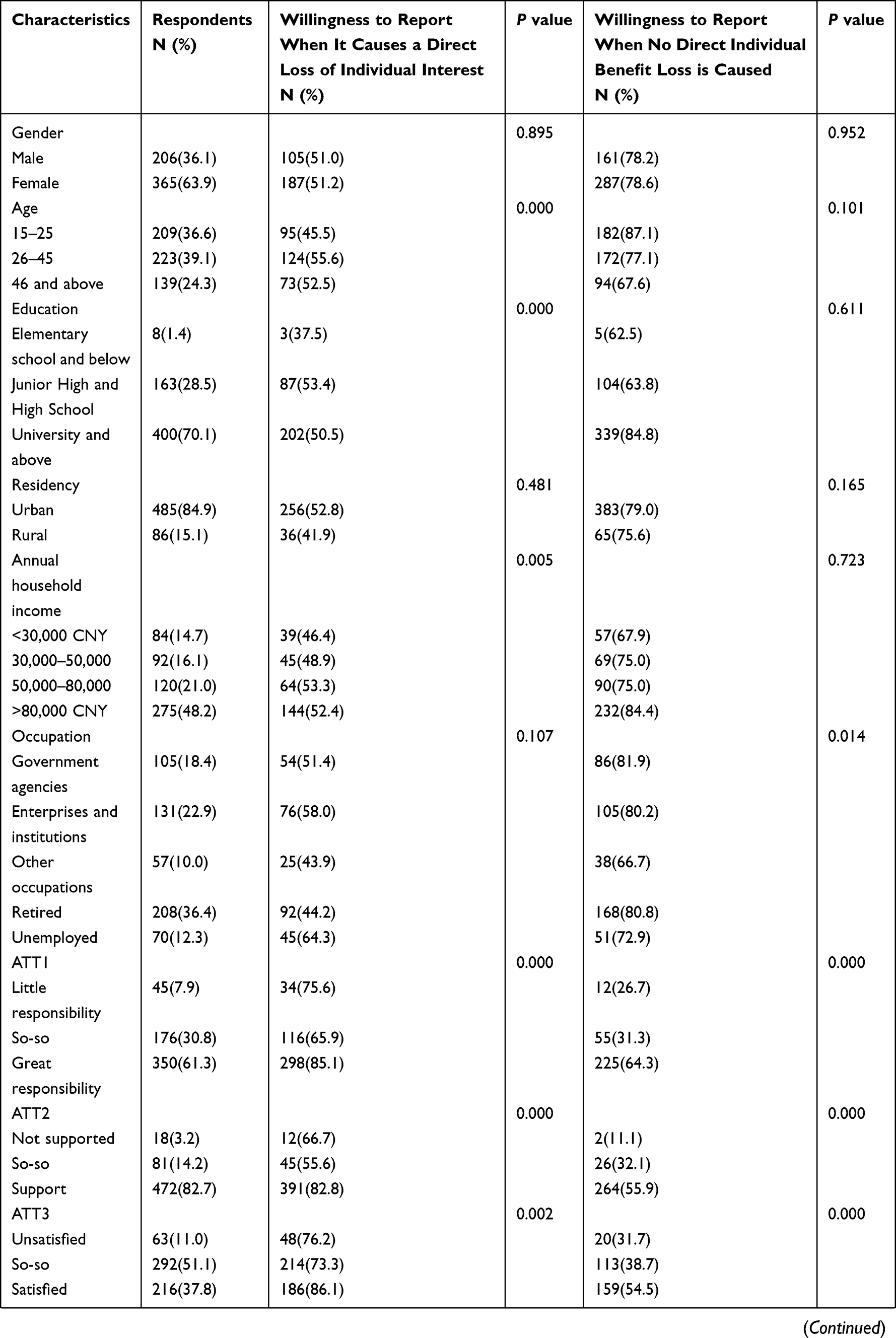

Participants’ gender, age, place of residence, education level, annual household income, and type of occupation were mainly investigated.

Attitudes Toward the Behavior (ATT)

It refers to holding a positive or negative evaluation of a person or an action. The first ATT1 is the participant’s judgment of how much responsibility he or she has to maintain the safety of the medical insurance funds (1=little responsibility; 2=So-so; 3=great responsibility). ATT2 is participants’ attitudes toward others reporting medical insurance fraud (1=not supported; 2=So-so; 3=support). Finally, ATT3 is the participants’ satisfaction with the relevant authorities for reporting medical insurance fraud (1=unsatisfied; 2=So-so; 3=satisfied).

Perceived Consequences (PCONSE)

The effect of perceptions of positive or negative outcomes of behavior on participants’ willingness to behave. Includes PCONSE1 perception of “badness of fraudulent behavior” (1=not bad; 2=So-so; 3=bad). PCONSE2 perception of “severity of harm from fraudulent insurance” (1=not serious; 2=So-so; 3=serious). PCONSE3 Select the level of concern about one’s safety after reporting medical insurance fraud (1=not concerned; 2=So-so; 3=concerned). PCONSE4 level of agreement that the government protects the privacy and safety of whistleblowers (1=disagree; 2=So-so; 3=agree) and PCONSE5 satisfaction with the security measures taken by the government to protect whistleblowers (1=unsatisfied; 2=So-so; 3=satisfied).

Subjective Norm (SN)

It is the influence that participants perceive when they decide whether or not to perform a behavior. These include SN1 whistleblowing behavior by family and friends, SN2 whistleblowing behavior by teachers, leaders, and colleagues, SN3 whistleblowing behavior by experts and scholars, SN4 information released by government departments on the safety of medical insurance funds, SN5 medical insurance fraud News released by the news media, and SN6 government disclosure of medical insurance fraud cases. Indicate the degree to which the behavior of different subjects affects the individual (1=no effect; 2=So-so; 3=effect).

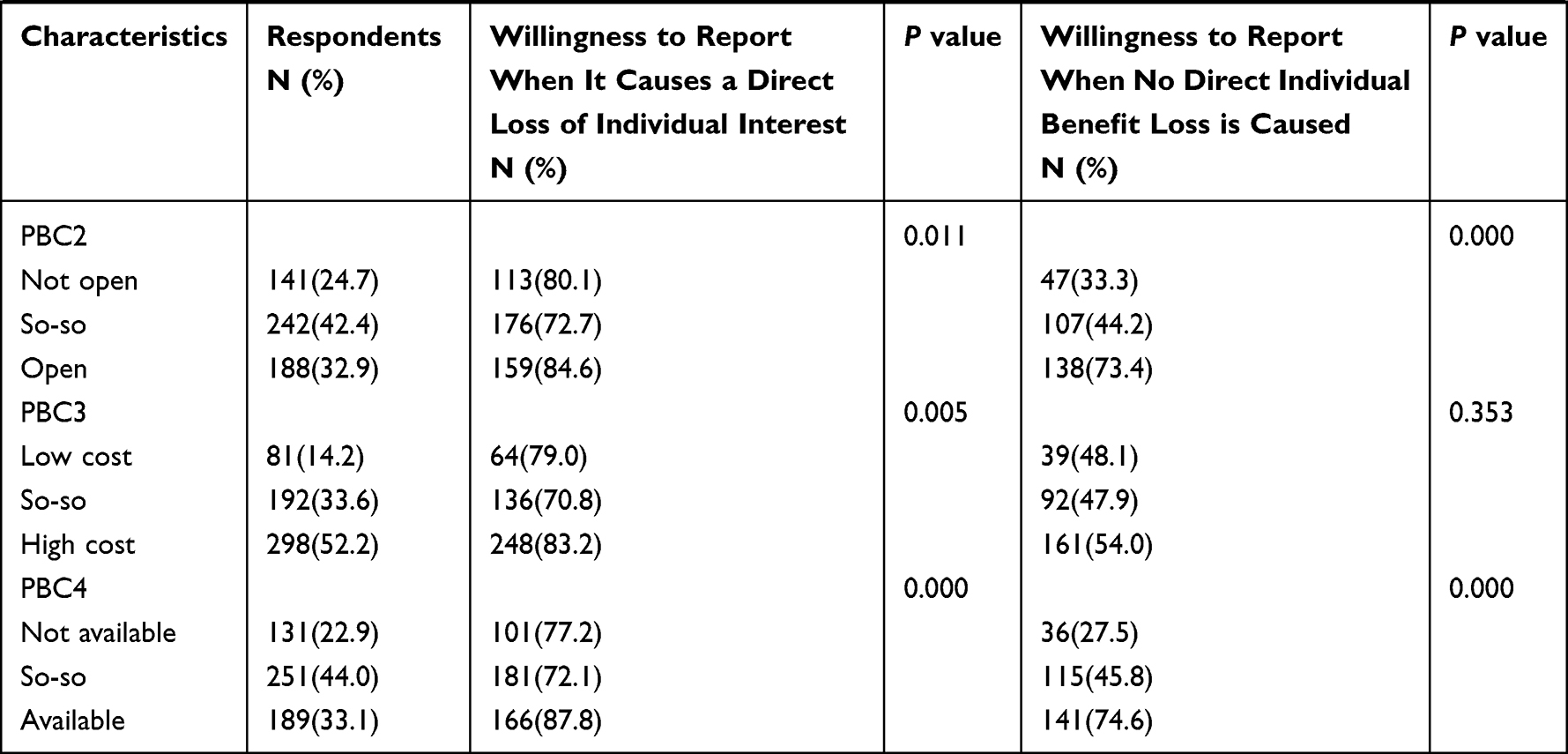

Perceived Behavioral Control (PBC)

It is the perceived ease of an individual in performing a behavior, including the resources, time, experience, information, opportunities, and abilities that would facilitate and hinder the degree of the individual’s intended behavior. This includes PBC1 difficulty of information access (1=not easy; 2=So-so; 3=easy), PBC2 openness of reporting channels (1=not open; 2=So-so; 3=open), PBC3 cost of reporting (time, effort, and money) (1=low cost; 2=So-so; 3=high cost), and PBC4 evaluation of the individual’s own ability to report medical insurance fraud (1=not available; 2=So-so; 3=available).

Data Analysis

To explore how individuals’ willingness to report medical insurance fraud and the factors that influence it differ between the two scenarios of whether individuals suffer a direct loss of benefits, the following methodology is used. First, descriptive statistical analysis was used to describe the characteristics of individuals and their willingness to report in two scenarios. Second, chi-square tests were used to determine the significance of the association between individuals’ willingness to report medical insurance fraud and different categories and levels of independent variables. Finally, logistic regressions were constructed to determine the factors affecting individuals’ willingness to report under both scenarios. OR, P values, and 95% CI were also calculated. All statistical analyses were performed using SPSS 25.0 and bilateral statistical significance was set at P<0.05.

Results

Characteristics of Participants

Overall, 628 people completed the questionnaire, 571 valid data were screened, and the effective recovery rate of the questionnaire was 90.92%. Among them, 273 were in the eastern region, 237 in the central region, and 58 in the western region.

Of the participants, 63.9% were female, with a relatively even distribution of the population across age groups. 70.1% of individuals earned a college degree or higher. In terms of place of residence, close to 85% live in the city. 48.2% of respondents had an annual household income greater than 80,000 CNY (Table 1).

|  |  |

Table 1 Demographic Characteristics of the Participants (n = 571) |

Descriptive Statistics

In the case of medical insurance fraud without direct loss of personal benefit, 49.0% of individuals are not willing to make a report and 51.0% are willing to report. The percentage of individuals who are unwilling to report medical insurance fraud once it has caused a direct loss of personal benefit is only 21.7%, and 78.3% of individuals are willing to report medical insurance fraud.

Regression Analysis

When medical insurance fraud causes personal direct benefit loss, Multiple logistic regression results show that the greater the individual’s own responsibility to maintain the safety of medical insurance funds (OR=1.423, 95% CI [1.018, 1.987]), the more supportive attitude to others reporting medical insurance fraud (OR=1.796, 95% CI [1.193,2.705]) the stronger the willingness to report. The greater the level of concern for one’s safety after choosing to report medical insurance fraud, the greater the willingness to report it (OR=1.349, 95% CI [1.024,1.777]). The greater the impact of the whistleblowing behavior of teachers, leaders, and colleagues and the disclosure of medical insurance fund fraud cases by the government on individuals, the stronger the willingness of individuals to report (OR=1.405, 95% CI [1.021,1.935]) (Table 2).

|

Table 2 Logistic Regression Results When Medical Insurance Fraud Causes Loss of Direct Benefits to Individuals (n = 571) |

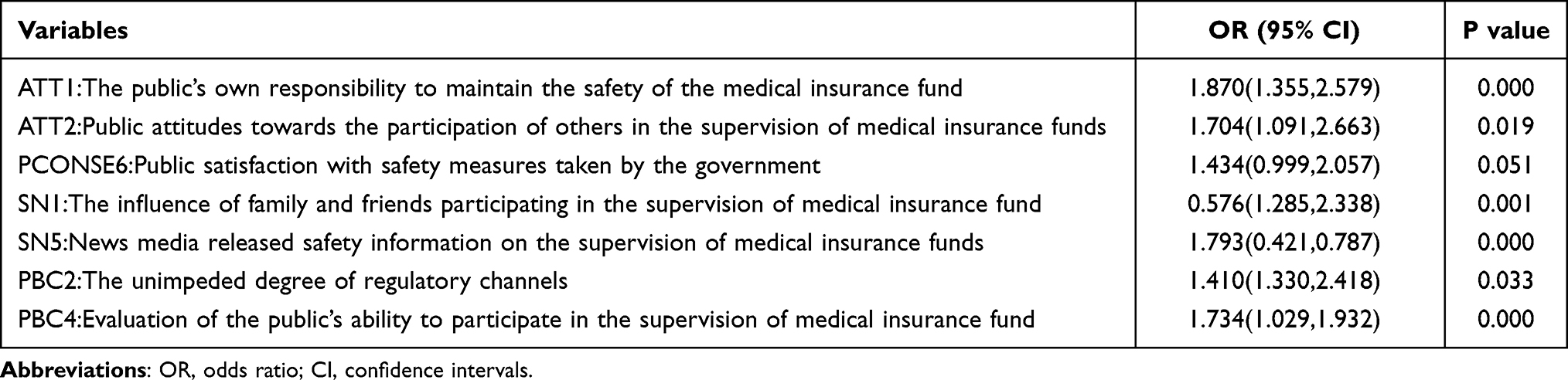

When medical insurance fraud does not cause direct personal benefit losses, Multiple logistic regression results show that the greater the individual’s own responsibility to maintain the safety of medical insurance funds (OR=1.870, 95% CI [(1.355,2.579]), the more supportive the attitude toward others reporting medical insurance fraud (OR=1.704, 95% CI [1.091,2.663]) the stronger the willingness to report. The more satisfied the government is with the security measures taken to protect whistleblowers, the stronger their willingness to report (OR=1.434, 95% CI [0.999,2.057]). The more the news media release information about the safety of medical insurance fund regulation affects individuals, the stronger the willingness to report (OR=1.793, 95% CI [0.421,0.787]). The more open the reporting channels (OR=1.410, 95% CI [1.330,2.418]), the stronger the individual’s own ability to report medical insurance fraud (OR=1.734, 95% CI [1.029,1.932]), the stronger the willingness to report. The degree of influence of family members and friends in reporting medical insurance fraud negatively affects individuals’ willingness to report (OR=0.576, 95% CI [1.285,2.338]) (Table 3).

|

Table 3 Logistic Regression Results When Medical Insurance Fraud Does Not Result in a Direct Loss of Personal Benefit (n = 571) |

Discussion

The study found that the willingness of individuals to report medical insurance fraud in the scenario of direct personal benefit loss was much higher than the willingness of individuals to report in the scenario of no direct benefit loss. In this study, people are more sensitive to violations and therefore more willing to report medical insurance fraud when it directly affects their individual interests. We also note that 51.0% of individuals are still willing to report fraudulent medical insurance fraud when it does not result in a direct loss of benefit to the individual. The reasons for this are as follows. One is that humans can derive satisfaction from the very act of punishing violators; the social preference model suggests that people are willing to punish violations to maintain social justice, and this desire to punish determines individual preferences for pursuing fair outcomes.22 The second is pro-social behavior that creates empathy for victims who have been subjected to medical insurance fraud.23 As a result, there are still some people who are willing to report medical insurance fraud although medical insurance fraud does not result in a loss of personal benefits.

This study found that people’s willingness to report medical insurance fraud in the context of direct personal benefit loss due to medical insurance fraud was not related to perceived behavioral control (PBC) factors. In contrast, people’s willingness to report the context of medical insurance fraud without direct personal benefit loss is related to perceived behavioral control factors. According to the prospect theory of risky decision making, most people become willing to take risks when medical insurance fraud causes a direct loss of personal benefit.24 The theory of planned behavior states that Perceived behavioral control is difficult to predict willingness when attitudes are strong,8 which is consistent with our findings. As a result, individuals may be more inclined to report medical insurance fraud when it results in a direct loss of personal benefit rather than sitting on the sidelines. When Medical insurance fraud does not result in a direct loss of benefit to the individual, the individual’s willingness to report is not as strong as when it results in a direct loss of benefit,11 so individuals are more concerned about the ease of perception when reporting. Ajzen argued that as volitional control over behavior decreases, increasing Perceived behavioral control has a facilitative effect on enhancing willingness to report.8 This is the same result found in this study, and therefore, the above differences in the relationship between perceived behavioral control (PBC) and willingness to report are related to whether the attitude toward reporting is strong.

Another important finding of this study is that the weaker the perceived consequences of “fear for one’s safety if one chooses to report medical insurance fraud”, the greater the willingness to report in the context of direct personal benefit loss due to medical insurance fraud. In the case of medical insurance fraud without direct loss of benefits to the individual, the more satisfied one is with the consequences of “the government’s satisfaction with the safety measures taken to protect whistleblowers”, the more likely one is to be willing to report. When Medical insurance fraud causes a scenario of direct personal benefit loss, the perception of one’s own safety is not able to hinder one’s willingness to report medical insurance fraud, as individuals are more sensitive to the pain they feel when they lose24 and are guided by a strong reporting attitude. In contrast, the main reason why individuals are reluctant to report medical insurance fraud in the absence of a direct loss of personal benefit scenario is that they have their own different fears about the consequences that may result from their reporting.25 Individuals have the possibility to become “potential whistleblowers”, that is, individuals who find wrong behaviors but do not report them.26 The fear of retaliation and the potential threat of whistleblowing is more likely to arise than others, leading to an “ethical dilemma for potential whistleblowers”. Avdi S Avdija’s study showed that witness security protection is an important tool to increase people’s willingness to testify and ensure effective investigation, prosecution, and adjudication.27 Therefore, the more satisfied individuals in this scenario are with the government’s safety measures to protect whistleblowers, the stronger their willingness to report. There are differences in individual perceptions of consequences in the two scenarios, which have different effects on their willingness to report.

The results also indicate that the stronger the perceived responsibility to maintain the safety of the medical insurance funds, the more supportive the attitude toward others reporting Medical insurance fraud, and the higher the willingness of individuals to report it, regardless of whether Medical insurance fraud causes a direct loss of personal benefit. where perceived liability has been shown to be an influential factor in willingness to report.28 And attitudes toward others reporting Medical insurance fraud are a side-effect of sociocultural attitudes toward reporting behavior. Among them, there are sociocultural differences in the understanding of the concept and phenomenon of whistleblowing.29 Dilek Zamantili Nayir and Christian Herzig found that culture is an important factor influencing individuals in a country or organization to report disciplinary infractions,30 which is consistent with our findings. Numerous studies have shown that although the current conception of whistleblowing in society or culture is evolving into a more positive one,29 support or opposition to whistleblowing is usually accompanied by ethical considerations.31–36 Related studies have also found that socio-cultural contexts that place special importance on group loyalty and saving face usually perceive whistleblowing as undermining the most fundamental value, namely harmony.37 Empirical studies using Hofstede’s cultural dimensions theory to analyze the impact of culture on whistleblowing have shown that whistleblowing is more likely to occur in social cultures with lower power distance, higher individualism, and higher uncertainty avoidance.29 Thus, Hofstede’s cultural dimensions provide a framework for revealing cultural differences between groups. This dimension helps predict the probability or acceptance of whistleblowing based on cultural factors, and also informs research on whistleblowing behavior across cultures and countries.38

Finally, this study shows that individuals’ willingness to report medical insurance fraud in a scenario of direct personal benefit loss is influenced by the actions of teachers, leaders, and colleagues and by government disclosure of medical insurance fraud cases. In scenarios where medical insurance fraud does not result in a direct loss of benefits to the individual, the individual is more likely to be guided by medical insurance fraud safety information published by the news media. In the scenario of medical insurance fraud resulting in direct personal benefit loss, the present study is consistent with the findings of Godin and Hagger et al. Who argued that China is a country with a collectivist culture where subjective norms and opinions have a significant impact on behavioral intentions.39,40 In contrast, in scenarios where Medical insurance fraud does not result in a direct loss of benefit to the individual, individuals are more influenced by the release of information about the event itself than by the actions of those they consider important41(eg, parents and teachers). Among them, news media and government disclosures of medical insurance fraud cases can release more detailed information,42 and the whistleblowing information they convey can act as an incentive for the general public to report medical insurance fraud. Subjective norms in medical insurance fraud reporting are one of the effective factors influencing willingness to report.

Conclusion

In summary, the willingness of individuals to report medical insurance fraud and the factors influencing it differed significantly between the two scenarios of whether medical insurance fraud resulted in a direct loss of personal benefit. First, perceived behavioral control was the most significant difference between the two scenarios, and this dimension only had an effect when medical insurance fraud did not result in a direct loss of personal benefit. Second, in the Perceived Consequences dimension, fear for one’s own safety after choosing to report medical insurance fraud is inversely related to the willingness to report when medical insurance fraud causes a direct personal benefit loss scenario. The more satisfied the government is with the security measures taken to protect whistleblowers, the stronger the willingness to report when medical insurance fraud does not cause direct personal benefit loss scenarios. Furthermore, the influencing factors of the attitude dimension are the same in both scenarios, and the more supportive the attitude toward the whistleblower, the stronger the individual’s willingness to report will be. Finally, subjective norms are one of the effective factors influencing the willingness to report medical insurance fraud. However, there are shortcomings in our analysis. First, cross-sectional studies provide useful information but cannot elucidate causal relationships. Future studies will further investigate temporal order through a longitudinal design to explain causal relationships. Second, although it is reasonable and theoretically intuitive to explore the willingness to report under two scenarios of whether an individual suffers a loss of benefits. But the potential mechanism of action is not yet well understood. However, our study can be taken as a starting point, inspiring more contextually relevant hypotheses for future research.

Ethics Statement

Ethics approval for the study protocol was obtained from the Ethics Committee of Harbin Medical University. Informed consent was obtained from all participants through online responses before the start of the survey. The Ethics Committee of Harbin Medical University approved the procedure for obtaining informed consent.

Acknowledgments

The authors would like to thank all respondents for their willingness to take their valuable time to participate in our study questionnaire. Special thanks to Dr. Kang Zheng for his help and for providing guidance to all authors. We wish to thank the reviewers for their insightful comments and suggestions.

Funding

This study was funded by the National Natural Science Foundation of China (72074064, 71573068), China Postdoctoral Science Foundation (2019M650068), China Postdoctoral Fund Special Grant Program (2018T110319) and the National Social Science Fund of China (19AZD013). The funding body did not influence the study design, data collection, data analysis, data interpretation, or writing the manuscript.

Disclosure

The authors declare no conflict of interest.

References

1. Johnson JM, Khoshgoftaar TM. Medicare fraud detection using neural networks. J Big Data. 2019;6(1):63. doi:10.1186/s40537-019-0225-0

2. Lorenz FA. Healthcare Fraud in the United States: Assessing Current Policy and Its Role in Fraud Prevention. California State University Northridge.; 2013.

3. Ai J, Brockett PL, Golden LL. Assessing consumer fraud risk in insurance claims. N Am Actuar J. 2009;13(4):438–458. doi:10.1080/10920277.2009.10597568

4. Kaplan SE, Lanier D

5. Faunce TA, Bolsin SN. Three Australian whistleblowing sagas: lessons for internal and external regulation. Med J Aust. 2004;181(1):44–47. doi:10.5694/j.1326-5377.2004.tb06160.x

6. Kesselheim AS, Studdert DM. Whistleblower-initiated enforcement actions against health care fraud and abuse in the United States, 1996 to 2005. Ann Intern Med. 2008;149(5):342–349. doi:10.7326/0003-4819-149-5-200809020-00009

7. Central People’s Government of the People’s Republic of China. National health insurance agency statistics 2021 statistical snapshot of health insurance business development (nhsa.gov.cn); 2021.

8. Ajzen I. The theory of planned behavior. Organ Behav Hum Decis Process. 1991;50(2):179–211. doi:10.1016/0749-5978(91)90020-T

9. Gibbons FX, Gerrard M, Ouellette JA, Burzette R. Cognitive antecedents to adolescent health risk: discriminating between behavioral intention and behavioral willingness. Psychol Health. 1998;13(2):319–339. doi:10.1080/08870449808406754

10. Xie M, Baumer EP. Crime victims’ decisions to call the police: past research and new directions. Ann Rev Criminol. 2019;2(1):217–240. doi:10.1146/annurev-criminol-011518-024748

11. van Erp J, Loyens K. Why external witnesses report organizational misconduct to inspectorates: a comparative case study in three inspectorates. Adm Soc. 2018;52(2):265–291. doi:10.1177/0095399718787771

12. Demir M. The perceived effect of a witness security program on willingness to testify. Int Crim Justice Rev. 2017;28:105756771772129.

13. Zhang G, Zhang X, Bilal M, Dou W, Xu X, Rodrigues JJ. Identifying fraud in medical insurance based on blockchain and deep learning. Future Gener Comput Syst. 2022;130:140–154. doi:10.1016/j.future.2021.12.006

14. Daehyeon P, Ryu D. Blockchain in health insurance: sharing medical information and preventing insurance fraud. Korean J Financ Stud. 2019;48(4):417–447. doi:10.26845/KJFS.2019.08.48.4.417

15. Tang X-B, Wei W, Liu G-C, Zhu J. An inference model of medical insurance fraud detection: based on ontology and SWRL. Knowl Organ. 2017;44(2):84–96. doi:10.5771/0943-7444-2017-2-84

16. Kalb PE. Health care fraud and abuse. JAMA. 1999;282(12):1163–1168. doi:10.1001/jama.282.12.1163

17. Radaelli G, Lettieri E, Masella C. Physicians’ willingness to share: a TPB-based analysis. Knowl Manag Res Pract. 2015;13(1):91–104. doi:10.1057/kmrp.2013.33

18. Ajzen I, Madden TJ. Prediction of goal-directed behavior: attitudes, intentions, and perceived behavioral control. J Exp Soc Psychol. 1986;22(5):453–474. doi:10.1016/0022-1031(86)90045-4

19. Ajzen I. Residual effects of past on later behavior: habituation and reasoned action perspectives. Pers Soc Psychol Rev. 2002;6(2):107–122. doi:10.1207/S15327957PSPR0602_02

20. Ajzen I. Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior. J Appl Soc Psychol. 2002;32(4):665–683. doi:10.1111/j.1559-1816.2002.tb00236.x

21. Triandis HC. Values, attitudes, and interpersonal behavior. Nebr Symp Motiv. 1979;27:195–259.

22. Fehr E, Schmidt KM. A theory of fairness, competition, and cooperation. Q J Econ. 1999;114(3):817–868. doi:10.1162/003355399556151

23. Singer T, Seymour B, O’Doherty JP, Stephan KE, Dolan RJ, Frith CD. Empathic neural responses are modulated by the perceived fairness of others. Nature. 2006;439(7075):466–469. doi:10.1038/nature04271

24. Kahneman D, Tversky A. Prospect theory: an analysis of decision under risk. Econometrica. 1979;47(2):263–291. doi:10.2307/1914185

25. Fu Ding YF. Research on the effect of the interrogation method of alleviating consequences perception. J Sichuan Police Coll. 2009;21(06):18–25.

26. Miceli MP, Near JP. The incidence of wrongdoing, whistle-blowing, and retaliation: results of a naturally occurring field experiment. Employee Responsibilities Rights J. 1989;2(2):91–108. doi:10.1007/BF01384940

27. Avdija AS. Examining the effect of witness-offender and witness–victim relationship on crime-reporting behavior. Crim Justice Stud. 2019;32(4):317–329. doi:10.1080/1478601X.2019.1627531

28. Kaplan S, Whitecotton S. An examination of auditors’ reporting intentions when another auditor is offered client employment. Auditing. 2001;20(1):45–63. doi:10.2308/aud.2001.20.1.45

29. Vandekerckhove W, Uys T, Rehg M, Brown AJ. International handbook on whistleblowing research. In: Understandings of Whistleblowing: Dilemmas of Societal Culture. Edward Elgar Publishing; 2014:37–70.

30. Gorta A, Forell S. Layers of decision: linking social definitions of corruption and willingness to take action. Crime Law Soc Change. 1995;23(4):315–343. doi:10.1007/BF01298447

31. Ceva E, Bocchiola M. Theories of whistleblowing. Philos Compass. 2020;15(1):e12642.

32. Grant C. Whistle blowers: saints of secular culture. J Bus Ethics. 2002;39(4):391–399. doi:10.1023/A:1019771212846

33. Kumar M, Santoro D. A justification of whistleblowing. Philos Soc Crit. 2017;43(7):669–684. doi:10.1177/0191453717708469

34. Larmer RA. Whistleblowing and employee loyalty. J Bus Ethics. 1992;11(2):125–128. doi:10.1007/BF00872319

35. O’Sullivan P, Ngau O. Whistleblowing: a critical philosophical analysis of the component moral decisions of the act and some new perspectives on its moral significance. Bus Ethics. 2014;23(4):401–415. doi:10.1111/beer.12058

36. Vandekerckhove W, Commers MSR. Whistle blowing and rational loyalty. J Bus Ethics. 2004;53(1):225–233. doi:10.1023/B:BUSI.0000039411.11986.6b

37. Davis AJ, Konishi E. Whistleblowing in Japan. Nurs Ethics. 2007;14(2):194–202. doi:10.1177/0969733007073703

38. Tavakoli AA, Keenan JP, Cranjak-Karanovic B. Culture and whistleblowing an empirical study of croatian and United States managers utilizing Hofstede’s cultural dimensions. J Bus Ethics. 2003;43(1):49–64. doi:10.1023/A:1022959131133

39. Godin G, Kok G. The theory of planned behavior: a review of its applications to health-related behaviors. Am J Health Promot. 1996;11(2):87–98. doi:10.4278/0890-1171-11.2.87

40. Hagger MS, Chatzisarantis NL, Biddle SJ. The influence of autonomous and controlling motives on physical activity intentions within the Theory of Planned Behaviour. Br J Health Psychol. 2002;7(Part 3):283–297. doi:10.1348/135910702760213689

41. Savin-Williams RC, Berndt TJ. Friendship and peer relations. In: At the Threshold: The Developing Adolescent. Cambridge, MA, US: Harvard University Press; 1990:277–307.

42. Dyck A, Morse A, Zingales L. Who blows the whistle on corporate fraud? J Finance. 2010;65(6):2213–2253. doi:10.1111/j.1540-6261.2010.01614.x

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.