")

Back to Journals » Risk Management and Healthcare Policy » Volume 15

The Persistence and Change in China’s Healthcare Insurance Reform: Clues from Fiscal Subsidy Policies Made for Settling COVID-19 Patients’ Medical Costs

Received 26 November 2021

Accepted for publication 11 May 2022

Published 24 May 2022 Volume 2022:15 Pages 1129—1144

DOI https://doi.org/10.2147/RMHP.S349124

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Kent Rondeau

Teng Ma,1 Bao Guo,2 Ju Xu3

1Law School & Intellectual Property School, Jinan University, Guangzhou, 510632, People’s Republic of China; 2School of Law, Xiamen University, Xiamen, 361005, People’s Republic of China; 3Library, Longyan University, Longyan, 364012, People’s Republic of China

Correspondence: Ju Xu, Library, Longyan University, 1# Dongxiaobei Road, Longyan, 364012, People’s Republic of China, Tel +86 18613048699, Email [email protected]

Background: The system studied in this article is set in the development and reform of China’s healthcare insurance, the time mentioned in this article is during the COVID-19 period and the issues are about healthcare insurance fiscal subsidy policies for COVID-19 patients’ medical costs.

Methods: Method of comparison and method of case study are used. This article compares the healthcare insurance systems, fiscal subsidy policies during the COVID-19 period and takes Yulin’s healthcare insurance reform and Nanjing healthcare insurance administration’s measures to fight against COVID-19 pandemic as specific cases to analyze.

Aim: This article presents the advantages of the coverage of China’s healthcare insurance as well as the insufficiency of the commercial healthcare insurance and market-oriented medical institutions to show the persistence and change in China’s healthcare insurance reform.

Conclusion: Soon after the outbreak of COVID-19 pandemic, the National Healthcare Security Administration and the Ministry of Finance of PRC jointly issued an announcement on how to guarantee the medical security of the novel coronavirus pneumonia pandemic. More specific policies were made by each province to secure that the total medical costs of the COVID-19 confirmed and suspected patients were almost borne by healthcare insurance and government finance subsidy. These policies reveal two basic points ahead China’s healthcare reform: one is that China shall persist in positively promoting the universal healthcare insurance coverage program, which will break down barriers between urban and rural areas; the other is that the commercial medical insurance shall be a supplementary to social healthcare insurance and the market-oriented medical institutions shall be encouraged. The two basic points stand for the persistence and change in China’s healthcare reform. China’s healthcare insurance reform should accord with the requirement in specific age and stage.

Keywords: healthcare insurance, COVID-19 pandemic, medical costs, public health, disease prevention

Nearly everyone has the patient experience, and hospital is a word that will unavoidably appear in one’s life sooner or later. The Third Plenary Session of the 18th Central Committee of the CPC mentioned to let the market play the decisive role in allocating resources and at the same time, the medical costs which concern people’s life and money sharpened the discussion of public opinion. China has always placed emphasis on the healthcare insurance and tried to push the reform; until now, the largest scale of healthcare insurance system network has been built in the world. Since the 1990s, China has been working on the establishment of the basic universal medical insurance system, the medical service coverage has been sharply expanded and the medical service supply system has been optimized as well, the problem of “the difficulty of getting medical service” and the problem of “high cost of getting medical treatment” have been effectively relieved. Meanwhile, the country has greatly increased the resource and investment in medical insurance. China’s medical insurance system has almost achieved universal coverage, the stable coverage rate has been 95%. The universal healthcare insurance reform has been pushed forward since the 18th National Congress of CPC.1

However, the burden for China’s healthcare insurance reform is heavy and the road is still long, although the coverage has been prominently expanded, its governance capability and the system completeness still have many deficiencies. Academic community’s opinions on China’s healthcare insurance reform are various, some scholars adopt holistic study, they frame the modern governance of China’s healthcare insurance according to value and theory, management and operation, technology and support,2 while some other scholars place focus on the break of healthcare insurance; for instance, there are some scholars concerned about the integration of urban and rural healthcare insurance,3 the reform of healthcare insurance payment,4 the sustainability of healthcare insurance fund,5 the administration of healthcare insurance and the countermeasures.6 In addition, some scholars emphasize on bringing the social power and market-oriented insurance into the reform and making use of the big data.7 On 25th February 2020, a significant document named opinions on deepening healthcare insurance system reform by the CPC central committee and the State Council (hereinafter referred to as “opinions”) was formally released and became a guideline for the healthcare insurance reform. The opinions mentioned 2 time nodes (2025 and 2030) as the reform development goals, 4 measures to enhance the security mechanism, 5 principles to guide the reform, 2 services to provide support, 20 “establishment” to deepen the reform task and 8 “explore” to initiate the new reform project. The document of opinions is not only a general guideline, it also has detailed contents which would much help the actual reform work. The implementation of the opinions means that the development of our healthcare insurance reform enters into a new stage, in this stage the system is completing, the whole is advancing, each section is mutually coordinated and the comprehensive coverage will be effective.8

The article takes fiscal subsidy for healthcare insurance during the COVID-19 period as a clue, through this clue it can be seen that the ruling party and the country’s policies firmly and positively support the healthcare insurance, the advantages of the coverage of China’s healthcare insurance are prominent, but the deficiencies of the market-oriented insurance and the social power are obvious too. This article is based on specific healthcare insurance fiscal subsidy policies and small places’ healthcare insurance reform experience to present the possible technique and trajectory for China’s healthcare insurance reform. Therefore, this article places a focus on the method of comparison and would compare medical systems and policies during the COVID-19 period, for example, this article compares China’s one provincial fiscal healthcare insurance subsidy policy with the other, compares China’s policies with other country’s policies. Meanwhile, as this article tries to present the frontier problems that might possibly be met in China’s healthcare insurance reform, case study is necessary and essential, this article takes Yulin’s healthcare insurance reform of Shangxi province and Nanjing Healthcare insurance administration’s measures as specific cases to analyze.

Policies on How Medical Costs of COVID-19 Patients Are Borne in China and the Understanding of the Policies

The document of opinions takes a long time to prepare; however, the outbreak of COVID-19 in 2019 undoubtedly pushed its issuance. Among the 8 “explore” in the opinions, the first “explore” is to establish (major epidemic disease medical rescue) exemption system for special group of people and special disease.

Responsible Organizations for Bearing the Medical Costs of COVID-19 Patients

On 23rd January 2020, the National Healthcare Security Administration and the Ministry of Finance of PRC jointly issued announcement on how to secure the healthcare of novel coronavirus pneumonia (hereinafter referred to as “the announcement”), the announcement specially ascertained that the COVID-19 confirmed patients belonged to the group of people who needed the special security, the principle was “the special means for special matters, put people first”. As per the principle, the medical costs of COVID-19 confirmed patients within the scope of coverage would be paid by the healthcare insurance, and the rest costs for individual would be subsidized by government finance; the confirmed patients, no matter they were local residents or not, would be treated by the local hospital first; the medicine for COVID-19, no matter it was within the list of healthcare insurance or was a new one due to therapeutic scheme, would be applied to the government finance for reimbursement. In order to make sure the announcement can be carried out and prevent delaying the work for pandemic due to local finance deficit, two days after the issuance of the announcement, the Ministry of Finance of PRC and the National Health Commission of PRC issued another notice named announcement on guaranteeing the fund for novel coronavirus pneumonia pandemic prevention and control: the central finance will subsidize the local finance, the subsidy is as high as 60%. From the material security perspective, the above measures are the financial basis for the healthcare insurance to cover the COVID-19 medical costs.

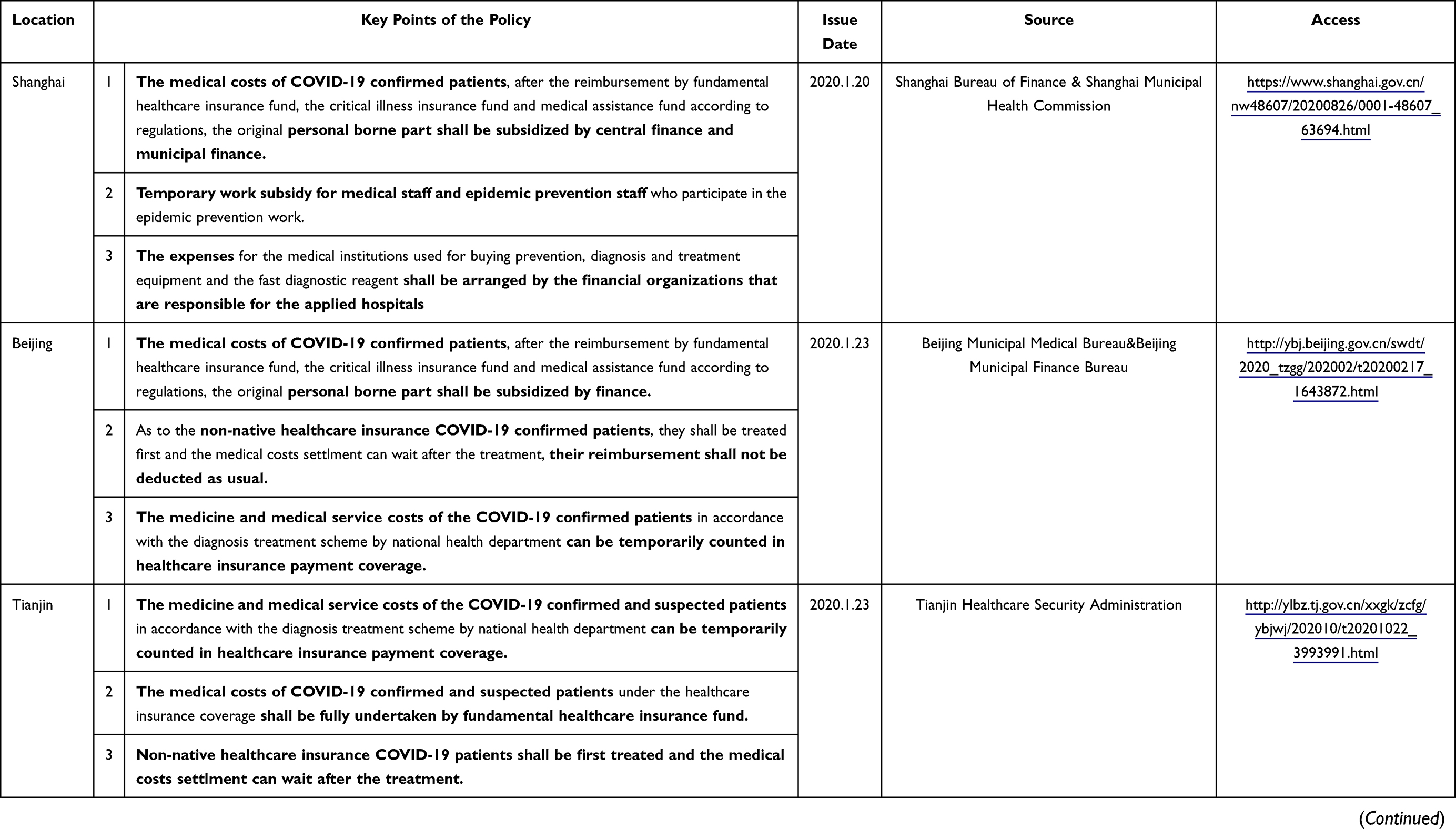

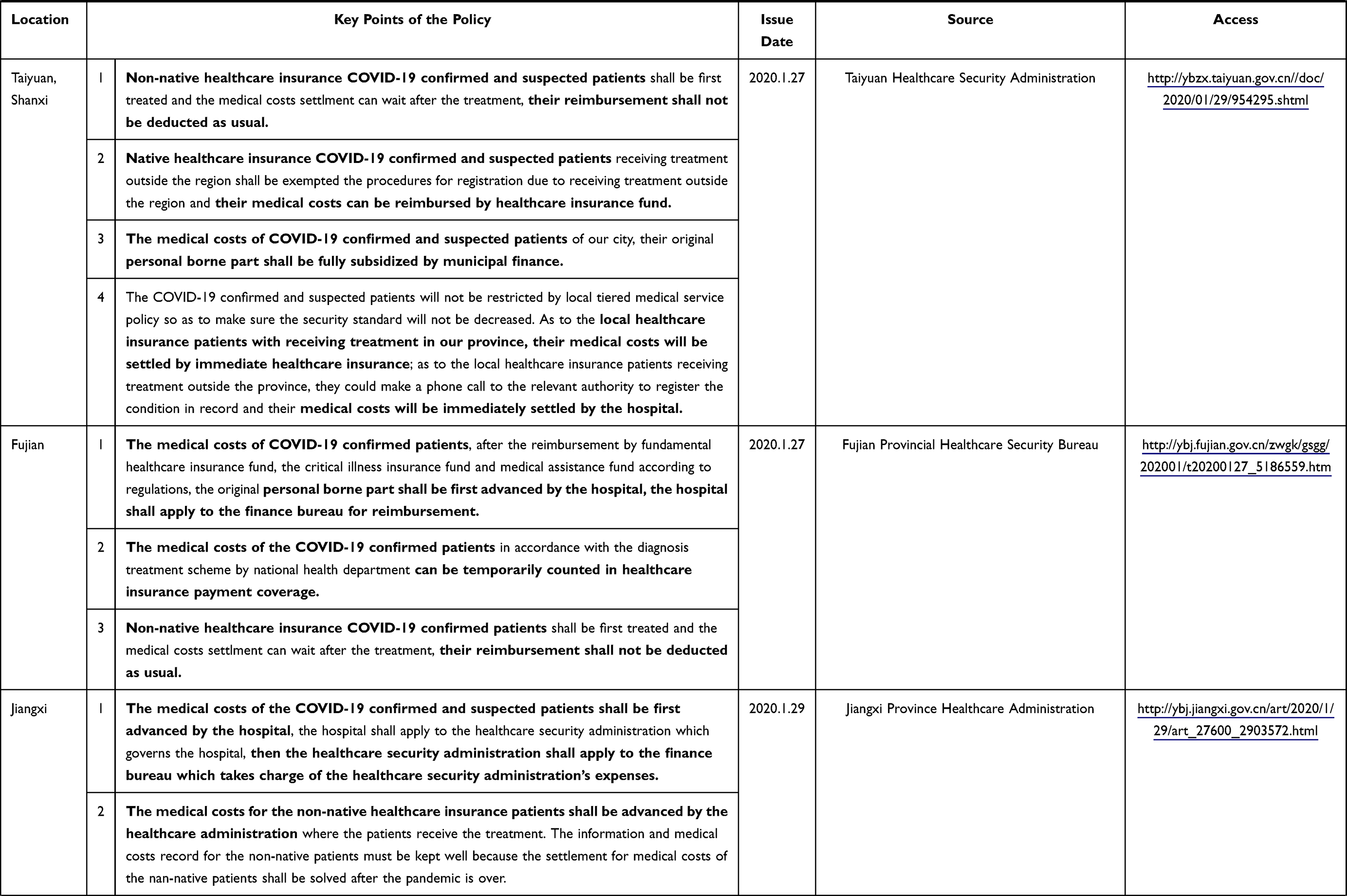

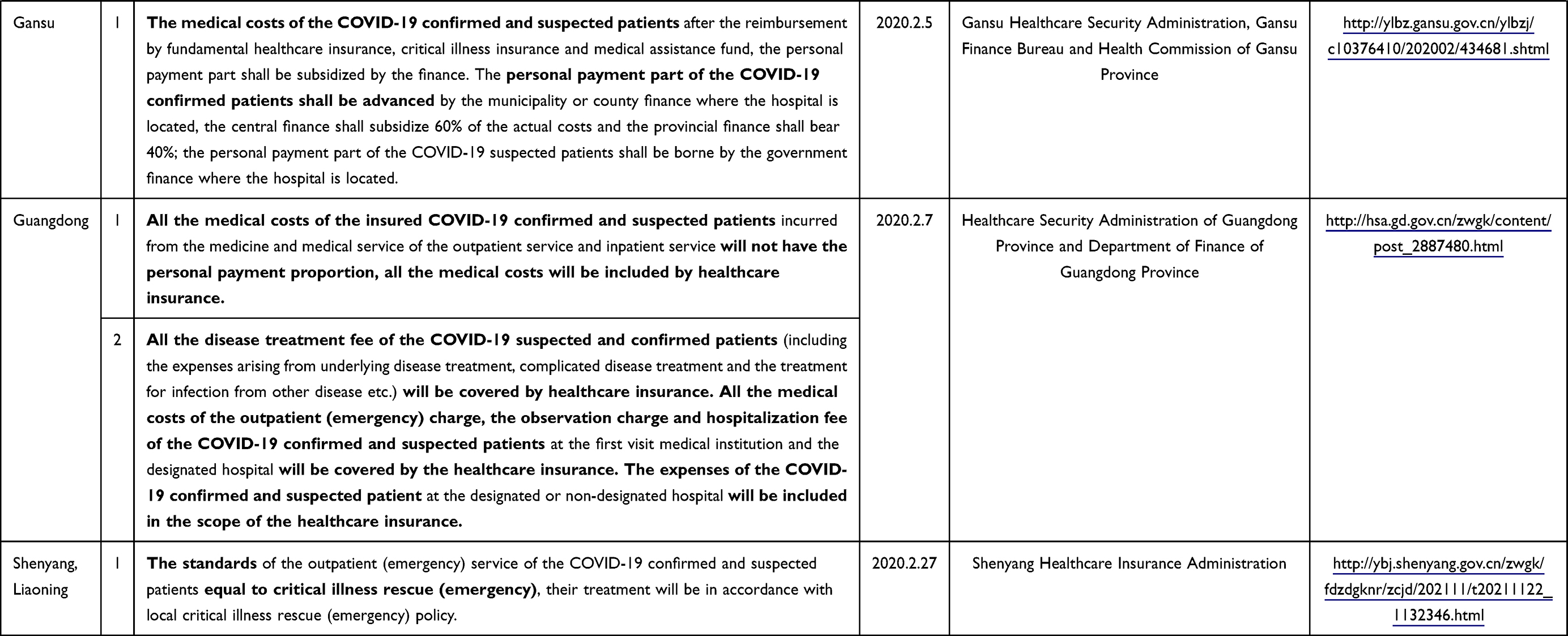

After the arrangement of how to bear medical costs of COVID-19 confirmed patients, China further broadened the healthcare insurance coverage scope to the suspected patients, on 27th January, the office of the National Healthcare Security Administration, the office of the Ministry of Finance of PRC and the office of the National Health Commission of PRC issued supplementary announcement on how to secure the healthcare of novel coronavirus pneumonia which put the COVID-19 suspected patients into the coverage of the healthcare insurance. Subsequently, the office of the National Healthcare Security Administration issued an announcement on optimizing the service of healthcare insurance to push novel coronavirus pneumonia pandemic prevention and control, which optimized the process and reduced the workload of the healthcare insurance institutions. The immediate settlement of medical costs of COVID-19 patients by healthcare insurance would decrease the population mobility and avoid the secondary pollution and was very important to prevent the pandemic spreading.9 Besides the policies made by the central government, each local government also made their own specific policies according to the announcement. Table 1 shows paradigm subsidy policies for the COVID-19 patients medical costs made in late January and early February 2020 by some cities and provinces.

|  |  |

Table 1 Provincial/Municipal Paradigm Fiscal Subsidy Policies for COVID-19 Patients’ Medical Costs |

The medical costs of the COVID-19 confirmed and suspected patients are mostly shared by the healthcare insurance and financial subsidy, and the individual does not need to afford anything. The patients’ economic burden caused by the pandemic will be eased and the measures play an important role in stabilizing society.10 The healthcare insurance requirement for COVID-19 patients breaks the rule that the insured must purchase the corresponding type of insurance first and then after the situation under the insurance coverage occurs he will benefit from the insurance policy, the medical costs for all the confirmed and suspected COVID-19 patients are counted in healthcare insurance coverage. The finance organizations provide special funds for the COVID-19 patients medical costs, some regions even cover the patients’ medical costs for the outpatient (emergency) charge, the observation charge. The healthcare insurance policies for COVID-19 cancel the payment limit and coverage restriction as well as the medicine list coverage and quantity restriction, the fiscal funds solve the remainder of the medical costs after they are settled by the fundamental healthcare insurance fund, the critical illness insurance fund and medical assistance fund.

Although the provincial and municipal policies differ, some are specific and some are simple, general measures of healthcare insurance for COVID-19 patients to promote across the country have been formulated. As to the healthcare insurance reimbursement, the outpatient charges are counted in hospitalization expenses, as to the standard of healthcare insurance, COVID-19 patents’ treatment standards equal to that of critical illness rescue, as to the medical costs bearing, the central and local finance organization mainly provide the fiscal subsidies, some regions like Guangdong and Jiangxi even take the medical costs all into healthcare insurance, as to the settlement, the procedures are simplified and the settlement is immediate.

The Understanding of the Policies

Under the circumstances of public risk, the government is obliged to take actions to protect its people. The government’s providing subsidy to the patients is not only for curing the patients but also for effectively quarantining them in order to reduce the risk of other people being infected.11 It is true that the special means for special matters, urgent handling for urgent matter is the government positively performing obligation and is each hospital carrying out the “two guarantee” as well, these measures work effectively.12 However, the measures are more like an emergency plan rather than a legal system. Therefore, “explore to establish (major epidemic disease medical rescue) exemption system for special group people and special disease” become one of the key works of this healthcare insurance reform. The establishment of general adaption standard will prevent the people from worrying the costs at the very beginning. The practice of our neighbor Japan is worth learning from: Japan treats the COVID-19 as “designated infectious disease” recorded in the infectious disease control law, which means both the test and treatment expenses of COVID-19 are for free, in the meantime, the patients shall be forced to designated hospital for treatment according to the law.13 Japan turns the emergency plan and the subsequent measures into legal interpretation and then takes legal actions to handle the outbreak of COVID-19 pandemic. Through this way, the law maintains its stability and the medical security emergency system has the law to abide by. On 7th February 2020, South Korea released support guidelines for the expenses of COVID-19 infection diagnosis and examination, none of the medical costs would be undertaken by the patients, and the medical costs of uninsured patients would be finally settled by Korea Disease Control and Prevention Agency of the Ministry of Health and Welfare. At present, our country’s government has three models in handling the COVID-19 medical costs: the healthcare insurance, the national health service and hybrid insurance. Regarding the settlement for COVID-19 test fees and treatment fees, some countries with sufficient medical support can provide thorough security, some countries do not charge the personal own afford part and expand the healthcare insurance payment coverage, and some countries provide special fiscal funds for help. China needs to consider its own conditions and complete its own legal system to deal with the pandemic.

In a sense, the COVID-19 pandemic can yet be regarded as a large-scale social random test, the healthcare insurance system is tested first. Each country in this world responds to the pandemic differently: in South Korea, people have the compulsory health insurance, after the outbreak of COVID-19 the country published the subsidy handbook immediately and let the country and local government bear the total costs of the treatment expenses of COVID-19; in Germany, the universal medical insurance would pay for the total costs of the treatment expenses of COVID-19 and as the analysis of the COVID-19 virus progresses, the expenses of COVID-19 test scope borne by the insurance expanded from 14 days travel history of middle and high-risk areas or close contacts to the condition that doctor thinks necessary and further to the self-doubt suspected patients or the close contacts of asymptomatic carrier; the USA in March 2020 issued Families First Coronavirus Act, which required the employer to afford the employee’s COVID-19 test fees, as this act aggravated the employer’s obligation and burden, when it was practised it met with a lot of resistance. Given that the USA did not carry out universal coverage, there were obstacles to pushing the act. However, the commercial medical insurance played an important role in this COVID-19 pandemic; many commercial medical insurances had exempted the co-payment and starting payment of COVID-19 treatment expenses. But the reactions of federation and state governments were not so satisfied, they did not allocate enough fund to pay for the COVID-19 treatment expenses and the vulnerable groups did not get prompt treatment because they could not afford the expenses in this pandemic.

We are not going to judge how each country affords the COVID-19 medical costs, we are trying to find the common problems behind different healthcare insurance systems or medical insurance policies of each country. There are four problems that need us to discuss: the first one, what would be the worst condition of healthcare insurance in COVID-19 pandemic? After the pandemic spread, the medical systems were overwhelmed by large quantity of infected patients, the healthcare insurance fund faced great challenge, in the wake of the pandemic the national economy would decline very soon and the income of the healthcare insurance would be seriously influenced. The second one, who would be the most suitable one to solve the problem upstream? Doctors were necessary for sure, they had professional knowledge and worked at the first front line. The pandemic of COVID-19 in China was actually first found by doctors but the one who was capable of solving the problem was the one who finally paid the bill for the pandemic. Therefore, it was the healthcare insurance administration and the government financial departments that were capable of solving the problem in the current system. The third one, how to let the healthcare insurance administration be willing to solve the problem upstream? The answer is to systematize the relationship between the nation and the medical profession. On the one hand, the policy maker must respect the professional medical decision, and in the meantime, the collective responsibility of the doctors must be enhanced in order to make sure they will cooperate effectively. Given that the above two conditions were satisfied by the healthcare insurance system, could the doctors “follow the heart without breaking the rule”.14 The fourth one, how to define the payment coverage and reasonable use method of the funds of healthcare insurance, public health service and fiscal assistance? From the current situation, it seems that the responsibility coverage of the healthcare insurance and the public health service needs to be clearly defined. For example, the expenses for testing nucleic acid and antibody should be included into healthcare insurance fund or be settled by public health service fund? In tradition, healthcare insurance just covers illness treatment, the epidemic prevention largely belongs to the public health service, but in this COVID-19 pandemic, the boundary between healthcare insurance and public health service is vague, the healthcare insurance settling the medical costs of COVID-19 patients takes charge of part of the responsibility of the public health service. This is the reason why this article discusses healthcare insurance rather than discussing the public health service.

In other words, as the prevention and control of COVID-19 pandemic is in stable condition in China, it is necessary to consider the problems of healthcare insurance system that may incur in the middle- and long-term pandemic prevention and control. On the one hand, the current workable emergency measures can be ascertained as long-term regulations so as to gradually establish and complete our own medical security emergency management system; on the other hand, the current policies need to be reconsidered whether they really accord with Chinese characteristic healthcare insurance development so as to help us find the more suitable policy instrument.15

The “Persistence” and the “Change” in China’s Healthcare Insurance Reform

The policies on how the medical costs of the COVID-19 patients are borne in the pandemic present us with two basic points ahead of healthcare insurance reform. One is good practice that shall persist in the reform; the other one is new change that shall be made by the reform.

The Persistence and Its Outcome in the Reform

In China’s fight against COVID-19 pandemic, the healthcare insurance plays an important role because it guarantees the patients free from worrying about the medical costs and maximizes the medical treatment to each patient. The accomplishment is backed up by the universal healthcare insurance coverage, which breaks down the barriers between rural and urban areas. The universal healthcare insurance coverage should remain unchanged in our healthcare insurance reform and be further progressed, and the activities for the farmers to buy new rural cooperative medical insurance should be especially encouraged. Health Policy in 2015 attributed China’s basically achieving universal healthcare insurance coverage to 7 reasons: (1) the SARS outbreak as a wake-up call, (2) strong public support for government intervention in health care, (3) renewed political commitment from top leaders, (4) heavy government subsidies, (5) fiscal capacity backed by China’s economic power, (6) financial and political responsibilities delegated to local governments and (7) programmatic implementation strategy.16 The measures taken in this pandemic that effect most are from the experience of the last SARS pandemic: political commitment, social recognition, economic investment. Therefore, through this COVID-19 pandemic, the policy of universal healthcare insurance coverage should be firmly insisted and further deepened.

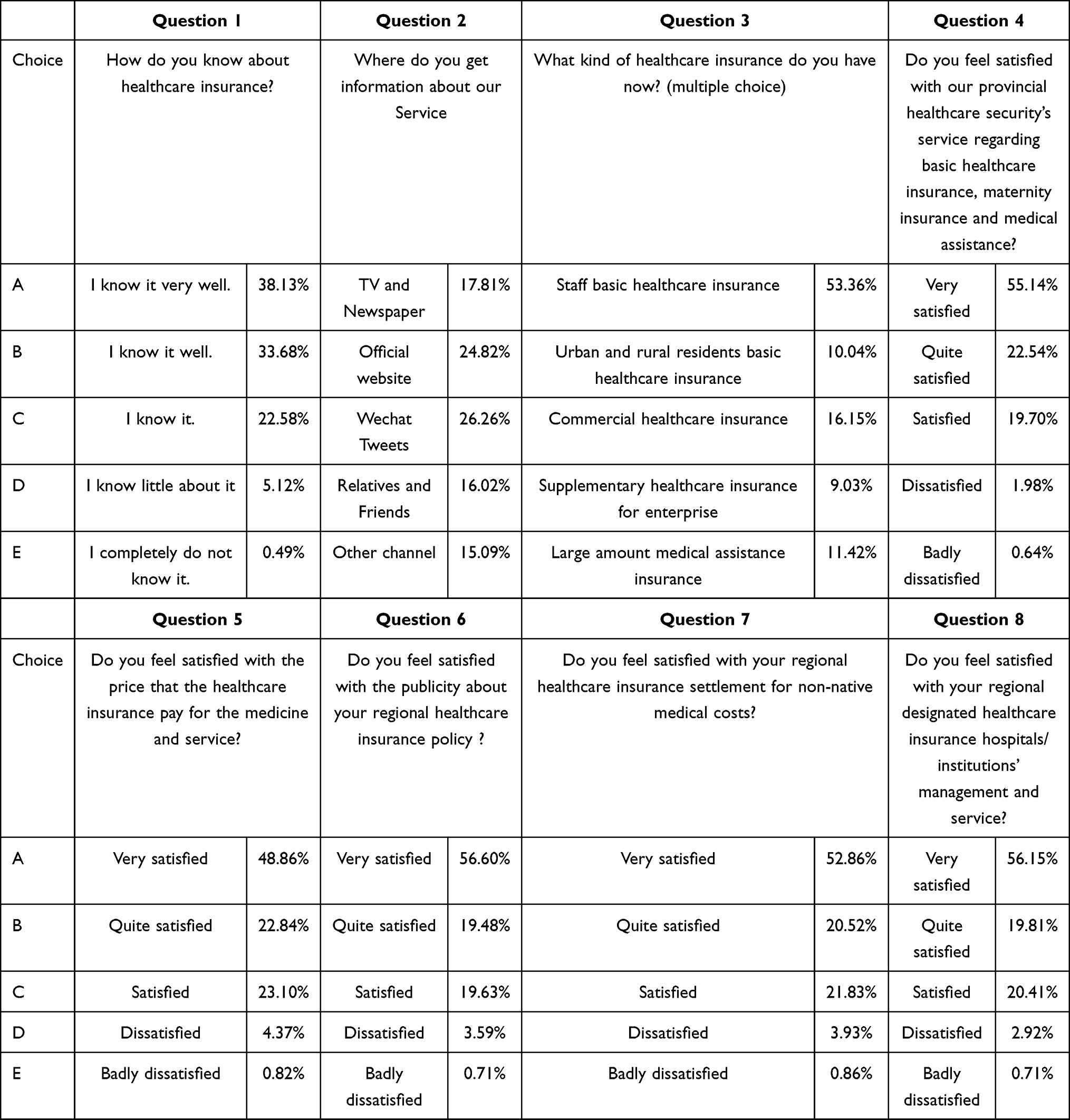

China’s universal healthcare insurance coverage includes: Staff’s medical insurance, urban residents medical insurance and farmers' new rural cooperative medical insurance. People will choose one of the above three social healthcare insurances according to their own condition (the urban residents medical insurance and farmers new rural have been bound together as “urban and rural residents healthcare insurance„). In 2014, there was a questionnaire, which surveyed how many patients under the above three social healthcare insurance coverages in Hubei province were satisfied with universal healthcare insurance coverage and healthcare insurance reform. The survey results show that although people under different healthcare insurance, 90% of them in each healthcare insurance were satisfied that the healthcare insurance solved the problem of high cost of getting medical treatment.17 Moreover, a recent service satisfaction survey in relation to the service of healthcare administration was conducted by healthcare security of Guangdong province (hereinafter referred to as “Guangdong healthcare security”) in November 2021. Guangdong healthcare security received 2675 valid feedback, the total satisfaction rate of the valid feedback was more than 95%. Among the valid 2675 feedback, the urban residents accounted for 70.88%, while the rural residents accounted for 29.12%.18 Table 2 shows the specific survey contents and each feedback results.

|

Table 2 Service Satisfaction Survey in Relation to Guangdong Healthcare Security |

Guangdong province is opening up to the world early, and it can always make foresight policies, which would be soon followed by other provinces and cities. Guangdong healthcare security first conducted an online survey and opened its results in the public, which indicates the healthcare security administrations are more and more concerned about the patients’ feelings and would like to make efforts to improve its service. From the result of question 3, it can be inferred that the public healthcare insurance (staff basic healthcare insurance + urban and rural residents healthcare insurance) is still in the dominant position, the people who have public healthcare insurance reached 63.4% (53.36%+10.04%), while the people who participate in commercial healthcare insurance only 16.15%. Commercial healthcare insurance needs to be developed.

The Change to Be Made by Healthcare Insurance Reform

Commercial Medical Insurance as a Supplementary

The first change that shall be made by healthcare insurance reform is to make the commercial medical insurance as a supplementary to social healthcare insurance. In this pandemic, if there are no national policies to provide support, our healthcare insurance system is hard to resist the impact brought by the pandemic. If all the medical costs arising from the pandemic are borne by individuals, many people might be driven into poverty, even if not into poverty, the high medical expenses will be a heavy burden and may cause many social problems, the social stability will be in danger in the end.

China’s healthcare insurance reform cannot only rely on the country and the government, the market economic means can also be adopted. Commercial medical insurance can be taken as an important supplementary to social healthcare insurance and shall much help the people afford the medical expenses besides the basic healthcare insurance coverage.19 The commercial medical insurance will take part in national public emergency management and will be guided by the government to make emergency plan to improve the country’s emergency security capability to deal with black swan event.20 The way to take part in the commercial medical insurance can be different from compulsory social healthcare insurance, it can be advertised by suggestion or joint-promotion.

Specifically, the benefits to be brought by the commercial medical insurance will be: first, it contains many critical disease insurances excluded by social healthcare insurance and has wider coverage scope, moreover its insured amount is much higher than that of social healthcare insurance. Second, the higher insured amount insurance will be easier to provide their clients with good quality medical resources. The quantity of 3A hospitals in Wuhan is in the top rank of China, but when the COVID-19 pandemic broke out, the hospitals were overwhelmed by large quantity of infected patients and the good quality medical resources were getting scarcer. The commercial medical insurance companies like to regularly invest in some good quality medical institutions according to their risk management mode, and once the insurance mechanism is initiated, the best medical resources and service will be provided to their insured patients.

The changes in healthcare insurance reform brought by COVID-19 pandemic not only have the above benefits but also have a good social support basis. After this pandemic, the social awareness of risk management and people’s awareness of health risk were both raised. In the long run, the pandemic will change the characteristics of the needed party in the insurance market and create a large space for the performance of insurance functions.21 In the first half of 2020, the situation was severe, but the data showed the year-over-year growth of insurance premium of commercial medical insurance reached 38.86% which was 6 times comparing 6.61% of insurance industry. The comparison of the first quarter of the beginning of the pandemic sharpened, the year-over-year growth of the income of commercial medical insurance was more than 20%, while the year-over-year growth of the income of the whole insurance industry was just 2.29%, there was a 10 times gap (the above data come from statistics of China Banking and Insurance Regulatory Commission). On 8th January 2021, at the annual meeting hosted by Chinese Medical Information and Big Data Association, a research paper entitled Research on the Frontier Development Model of Commercial Health Insurance under the Big Data Ecosystem was released. This research paper shows four health insurance needs tendencies through making questionnaire survey to more than one thousand of consumers, the tendencies are as follows: people’s health insurance needs are trending from “ask me to purchase health insurance” to “I want to purchase health insurance”, from “simple health insurance” to “diverse insurances”, from “sole one” to “interaction”, from “to insure for the basic needs” to “focus on health”. The survey also shows 47.8% consumers express that it is necessary to have commercial health insurance.

It is easy to see that after the pandemic people’s enthusiasm for purchasing commercial medical insurance runs high and the sales of commercial medical insurance reach a new level. It can be inferred that the commercial medical insurance shall be a supplementary to social healthcare insurance and shall be the new change in healthcare insurance reform.

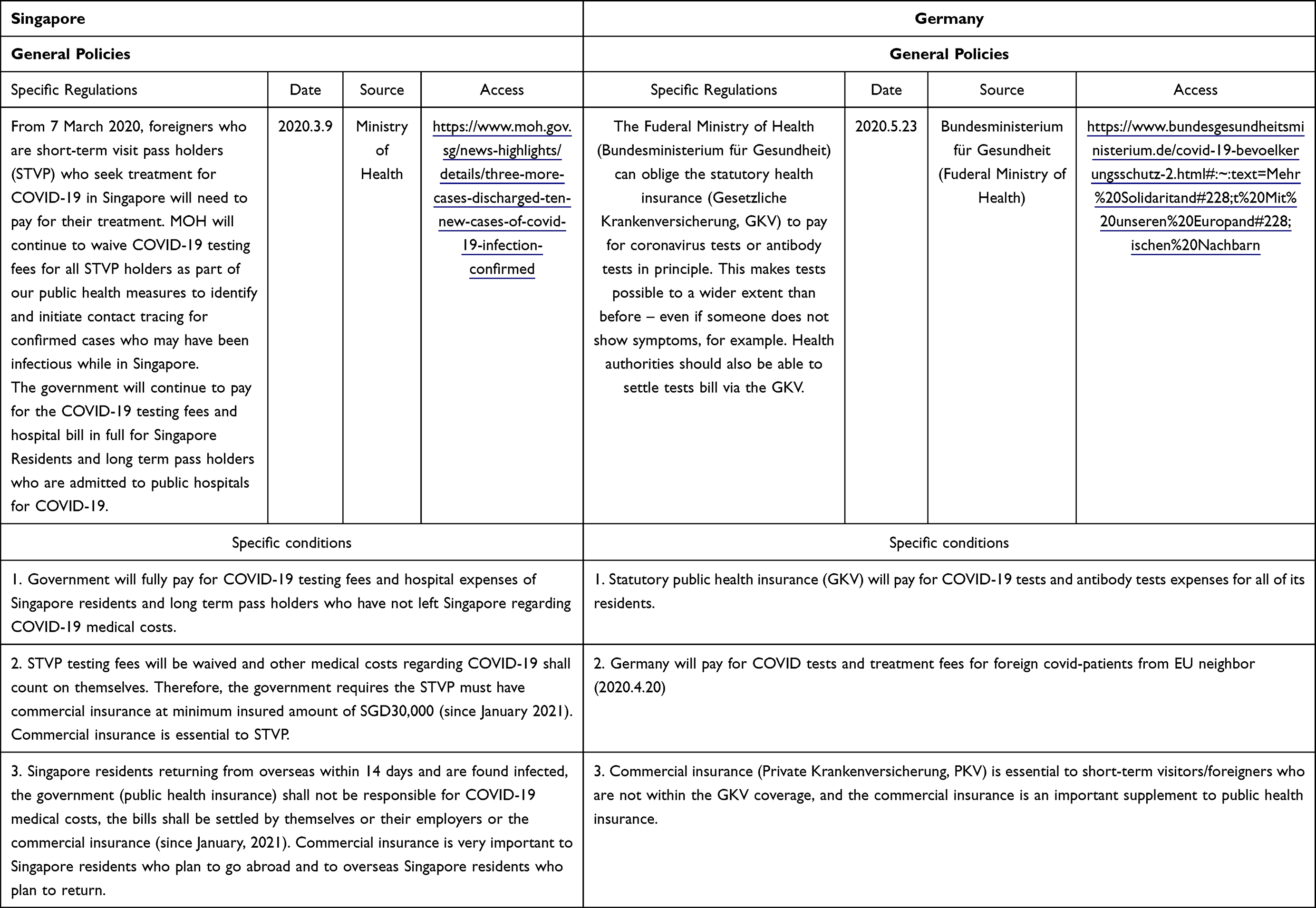

In conclusion, the government and commercial insurance company establishing insurance pool will bring many benefits to the medical field and will deal with catastrophe more effectively. There are some successful experiences of other countries’ “social insurance+commercial insurance” mode that we could learn from. Singapore and Germany are two paradigms that take “social insurance+commercial insurance” to fight against the COVID-19 pandemic and gain great accomplishment, Table 3 shows Singapore and Germany general public policies regarding the COVID-19 and the specific performance of the policies by public health insurance and commercial insurance regarding COVID-19 patients’ medical costs in different situation.

|

Table 3 Paradigm “Commercial Insurance + Social Insurance” Examples |

Based on Table 3, both Singapore and Germany provide their residents with free nucleic testing charges. Singapore mode is like China, the public health service department shall undertake the expenses, but Singapore requires statutory commercial insurance for STVP which will effectively reduce the financial stress of the government and medical system. Germany has a high rate of statutory public insurance coverage, and its covered scope is very wide; people do not need to concern about COVID-19 medical costs, and commercial insurance also help the government relieve the financial stress. China’s commercial insurance has not been well developed yet, in this pandemic the leading actor is healthcare insurance, commercial insurance does not have prompt reaction.

The Marketization of Medical Institutions

The second new change in the healthcare insurance reform shall be the marketization of medical institutions. It is true that healthcare insurance reform should focus on the system reform, but in order to make the healthcare insurance system be effective, the marketization of medical institutions cannot be avoided. Review the problem of scarce medical resource in Wuhan at the beginning of the pandemic, reasons could be concluded as: one was that the current distribution of medical resources was imbalanced, the high-quality medical resources were overloaded in daily life, which meant the current medical resources especially the high-quality resources (public hospital) had already overloaded and had little room to receive the sudden increased huge amount of patients, the other reason was that at the beginning of the pandemic in Wuhan, the handling was inappropriate, people were in panic and the virus was totally new to the hospital and the hospital needed time to learn how to deal with, these factors led that a large number of patients rushed into the hospital, the hospital could not operate smoothly and the medical systems were overwhelmed.

The healthcare insurance reform, to some extent, can help the problem of medical resources insufficient in daily life be lightened. The healthcare insurance reform shall have some changes that will encourage the growth of the medical resources to meet the daily needs. What can encourage the rapid growth of medical resources? The answer is marketization of the medical institutions. In market-oriented condition, there will be more hospitals and medical resources, after the proper allocation of medical resources, the capacity of medical institutions to receive patients shall be increased and the situation that the medical systems being overwhelmed by large number of patients under major epidemic disease will be relieved or even eliminated. It should be noted that we cannot equal the marketization of medical institutions to new changes brought by COVID-19 to China’s healthcare insurance reform, but the COVID-19 pandemic intensified the contradiction and pushed the reform to a new stage and made the reform in urgent need. From the perspective of view, the medical institution being market-oriented will be the new change brought by COVID-19 pandemic to healthcare insurance.

The medical institution being market-oriented shall be one of the new key points of the healthcare insurance reform, whether it can effectively raise the capacity of hospital to receive more patients and improve the medical resource to handle disease similar to COVID-19 pandemic? The logic that follows may explain: if the insured patients are taken as demanders, the hospitals that provide medical services should be the suppliers. Although the universal coverage is nearly done, the healthcare insurance fund subsidy has increased year by year and the patients’ capability of affording the medical costs has grown, the high medical expenses are still a severe social problem. Why the problem still exists? The reason is the reforms for the demanders and suppliers are unsynchronized. The social healthcare insurance system of the demanders which adjusts to market economic system is almost established but the system of the suppliers is still in administrative hierarchy.22 People in China prefer public hospitals to private ones; once the public hospital is in a monopoly position, it will soon acquire the designated healthcare insurance qualification otherwise it will be very inconvenient for the patients as their healthcare insurance must be spent in designated hospitals. Furthermore, if the public hospital does not have healthcare insurance income, its state-owned property and staff development will be seriously impacted. For these reasons, the healthcare insurance administration has little room to decide on a designated healthcare insurance hospital and also loses its punishment for canceling the designation qualification. Healthcare insurance as the biggest payer for medical costs will finally afford the hospital’s unreasonable makeups, what is worse if the healthcare insurance fund collapses there will be serious financial risks.23

Now that the suppliers who are public hospitals in monopolistic position are blamed for the problem, the medical institution being market-oriented will be a must. In the highly market-oriented market, the above problems will be alleviated, and there will be market competition which will cause catfish effect to truly invigorate the vitality of medical service market. Once there is real “service” provided in the medical care, the patients will get options to choose the real fine quality hospital. In the meanwhile, the healthcare institution will regain the commanding rights to decide or cancel the “designated hospital”.

The above discussion is not only a theoretical assumption; far before the COVID-19 pandemic, a small county named Shenmu, located in Yulin, Shannxi province, started a healthcare insurance reform in 2009 which incurred many discussions. The Shenmu Reform, which had a high government subsidy and actual reimbursement ratio and covered a wide scope, was so-called “free healthcare insurance reform for all people”. The Shenmu reform was no longer simply increasing government financial subsidy and making the government pay the medical costs bill but to bring in the market-oriented medical institutions and increase the financial subsidy as well. The result of Shenmu reform was very attractive: in 2010 one year after the reform, there was only one public county hospital, which was equipped with 400 beds, but there were other 15 the same level hospitals with more than 1300 beds. The reform re-allocated the medical resource and effectively settled the problem of high cost of getting medical treatment: on the one hand, whether the medical treatment fee was high depended on how much would be borne by the patients. The government financial subsidy in Shenmu was very high (85% of hospitalization expenses would be subsidized by the government), the rest expenses that patients would afford were not much, so the problem of high cost of getting medical treatment was settled. On the other hand, whether it was hard to get medical treatment depended on whether the patients would get treated nearby. According to the formal data published by Shenmu county: in 2009, there were 29847 hospitalized patients, the expenses were RMB149000000; in 2010, there were 40600 hospitalized patients, the expenses were RMB213000000 and in 2011, there were 42517 hospitalized patients, the expenses were RMB220000000.24 In the three consecutive years of reform, the numbers of hospitalized patients were quite stable, and there were seldom conditions that patients asked for transferring to other hospitals located outside Shenmu, the medical resources in Shenmu generally matched the patients’ demand. The high cost of getting medical treatment was well settled in Shenmu reform.

Shenmu reform is a good example to learn, and if the medical resource allocation is further completed, there will be three benefits: the first is to save the government financial cost; the second is to ensure that the healthcare insurance administration has the power to restrict the medical institutions, and the third is to decline the medical costs. It is true that every reform cannot be flawless and it must undergo the modification and improvement. How to prevent over-treatment and overspending medical costs awaits further exploration.25 The essence of this healthcare insurance reform is as follows: medical institutions being market-oriented will break the situation that the healthcare insurance institution passively pays for medical costs and presents how the healthcare insurance money should be spent. Although Shenmu healthcare insurance reform was only a pilot scheme, it well proved that the medical institution being market-oriented was not an internal need but it also had feasibility and effectiveness.

The “Technique” and “Trajectory” for China’s Healthcare Insurance Reform

Traditional Chinese Confucianism were fond of dealing with things by the doctrine of the mean. The Doctrine of the mean is far more than compromise, it means to find a properest solution between two ends according to the situation. The old Chinese wisdom may lead us in another way to think about the impact of the COVID-19 pandemic. The COVID-19 pandemic brought severe consequences, which could be felt directly, but it also brought many opportunities that could not be seen directly. The COVID-19 pandemic pushed government to take immediate actions to make policies to guarantee people’s receiving medical treatment without hesitation. China’s healthcare insurance does not only play an important role in paying the medical costs but shall also make efforts to healthy China initiative. There are technique and trajectory for China’s healthcare insurance reform ahead.

The Technique for China’s Healthcare Insurance Reform

The technique for healthcare reform means new technology to be adopted in healthcare insurance reform. Modern technology develops quickly, but due to the technology process of the current healthcare insurance system and the regional problems, new technologies are very hard to be used in healthcare insurance system, the technologies advance everyday but the healthcare insurance system remains conservative.

Although the overall system of healthcare insurance system is lagging behind, there have been some successful cases in the relevant parts of the local medical insurance system: under the situation of fighting against the COVID-19 pandemic, Nanjing healthcare insurance administration, relying on Nanjing monitoring platform of medical consumables, urgently organized technical units to develop the “purchase and deploy hall of epidemic prevention and medical appliance”, exploring to deploy epidemic materials in short supply to designated medical institutions by big data technology. It was the first step for medical security departments to deploy medical materials by using digital technology innovation.26 Specifically, Nanjing Healthcare Insurance Administration used big data technology to supervise the medical materials market in real time, and then found the fluctuations and changes in the market from time to time, reflecting the current demand for epidemic prevention materials in Nanjing. And then, the accurate portrait of the demands of existing medical material was made, after which guidance would be provided to healthcare insurance institutions. Under this circumstance, the demander and the supplier could be in touch directly. The big data technology deployed the epidemic material and also improved the working capacity of Nanjing Healthcare Insurance Administration.

In the United States, there was also a similar ice breaking case: Oscar Health company developed an App by internet and big data technology to have interactions with the patients in the whole medical care process in order to solve the problems like complexity of treatment process, the difficulty in making an appointment with a doctor, etc. By the beginning of 2018, the company had 250,000 registered members and completed 6 rounds of financing, with a financing amount of more than US $700 million. The medical security systems of China and the United States both have the practice of adopting the technology, though their dominant organization differs. It is easy to see technologies to be used in healthcare insurance reform will be the most common choice of the times. It is easy to see that COVID-19 is more like a high-performance catalyst to drive China’s healthcare insurance reform to meet the new challenges.

The Trajectory for China’s Healthcare Insurance Reform

The emergence of healthcare insurance system is the inevitable product of human social and economic development, its appearance is for human to avoid the risk of illness and the economic risk caused by illness. The establishment of each country’s healthcare insurance system is always affected and restricted by its nation’s politics, economy, society and cultures; therefore, the form of the system and the implementation differ.27 The fundamental goal of China’s healthcare insurance system should still be for protection of people’s health, including the level and the various ways to protect people’s health as well as the affordability and availability of the protection of people’s health.

After hundreds of years of evolution, the current model design of healthcare insurance system includes Beveridge model, Bismarck model, highly market-oriented model, Shemashko model and savings accumulation model. The model design for China’s healthcare insurance reform could be adjusted according to the state condition. The healthcare security should always adhere to the people-centered development concept, in the new development stage it should implement the new development concept, integrate into the new development pattern and lay emphasis on ensuring and improving people’s livelihood and continuously improve people’s well-being.28 Only when the trajectory for the healthcare insurance achieves “inclusiveness” in ensuring people’s livelihood and improving people’s well-being can it truly accord with the model design for the fundamental goal of China’s healthcare insurance reform to better ensure people’s livelihood and serve the implementation of “Healthy China Strategy” mentioned in the reports of 19th National Congress of CPC and serve the performance of “Outline of Healthy China 2030 Plan”. The trajectory of the healthcare insurance has distinct characteristics like the public takes precedence over the individual, well-being is beyond freedom, plan as a whole replaces dispersion, government guides the market, etc., the model advantages which were ascertained by history and in accordance with China’s national condition should be developed, meanwhile the weakness of the reform as mentioned above should be considered as well.

Regarding the healthcare insurance coverage and inclusiveness, there are still two issues that call for attention: the first one, China’s current urban and rural resident healthcare insurance is a type of voluntary insurance, there are still some people who are not insured, some related laws to promote the universal statutory insurance or let the people voluntarily be insured should be in consideration of legislation. In 2020, 1016.76 million people in China accepted the urban and rural resident healthcare insurance, the participation rate decreased by 0.8% compared with the previous year.29 The population mobility grows fast and it is a common phenomenon that people and their registered permanent residence are separated, the current fiscal subsidy to the healthcare insurance of people as per their registered permanent residence cannot sufficiently react to the urgent need in the public crisis, this situation needs to be improved through adjusting the fiscal subsidy methods. The second one, methods like fiscal subsidy should be adopted to help the poor and difficult people participate in healthcare insurance. The healthcare insurance admission should be expanded, government should take measures like lowering down the personal afford ratio and providing fiscal subsidy to make sure that difficult and poor people can participate in the healthcare insurance. Universal healthcare insurance does not only mean that every person is insured, it also means that the insurances can offer sufficient security, to achieve a high-quality standard of the healthcare insurance is our target.

The key point of China’s healthcare insurance reform should accord with the requirement in specific age and stage. China’s healthcare insurance reform did have the above basic point of persistence, but in different periods, the fundamental goal and the core of China’s healthcare insurance reform shall present the corresponding major problems. Taken the COVID-19 pandemic as an example, when the pandemic broke out, China’s healthcare insurance made adjustments and even many innovations to guarantee that the patients would not worry about the medical care due to expenses, guarantee that the medical institutions would conduct the treatment regardless of medical costs payment policies, optimize the process of healthcare insurance and improve the service efficiency, push the “internet +” healthcare insurance to meet people’s regular medical care needs, reduce enterprise burden and assist in the economic development in the pandemic.30 The next stage of post-COVID-19 era, the problems of treatment to special group of people in major epidemic disease, the exemption system for medicine of special disease and normalization of emergency medical insurance system in China’s healthcare insurance must be the new concerns. The key points of China’s healthcare insurance reform keep pace with time, which embodies the fundamental goal and core of China’s healthcare insurance reform in different development periods.

The trajectory of China’s characteristic healthcare insurance reform shoulders heavy responsibilities and has many possibilities, the above illustration is just based on authors’ analysis of the tendency and policies arising from the current healthcare insurance system. Moreover, this article places focus on the comparison of official policies and only presents people’s basic satisfaction data of China’s healthcare insurance and does not conduct thorough survey from the insured patients, the perspective is incomplete, and also our capability of prospecting the commercial insurance development is a little inadequate, this article does not show a more specific trajectory from perspective of insurance industry planning and technology.

China’s popular movie Dying to Survive tells a sad story that a man as a purchase agent of Indian generic cancer drug for other cancer patients who could not afford the patent drug was called “god of medicine” by the cancer patients, he got crime punishment due to his actions, but in the end of the movie the healthcare insurance became the new “god of medicine”. The end of movie turns the audience’s pessimism of medicine patents into optimism of the healthcare insurance system. There shall be a question mark for whether the healthcare insurance in realistic world could be “god of medicine”. On the one hand, the payment capacity of the healthcare insurance highly correlated with the economic development level, the developed country can bring the high price medicine into healthcare does not mean China’s healthcare insurance can afford. On the other hand, the fund of healthcare insurance is limited, even in developed country only a part of medical needs can be satisfied, it is impossible to bring all the items into the coverage scope.31 Indeed, the test from COVID-19 pandemic made the China’s healthcare insurance reform more important and accelerated the new changes and technologies. To the public, only if they clearly know the healthcare insurance system is not the panacea can they correctly and positively treat China Characteristic healthcare insurance system and enjoy the security and happiness to be brought by the healthcare insurance reform. China’s healthcare insurance has distinct features: public is over individual, well-being is over freedom, integration is over dispersion, government orients the market. On the one hand, China’s healthcare insurance should develop its advantages that are certified by the history and explore the trajectory for universal coverage and inclusiveness; on the other hand, the challenges and deficiencies mentioned above need to be seriously treated, ie the development of commercial insurance and its market-orient way as well as the medical high technology promotion in the period of big data.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Lou H, Ying Y. Deepen Chinese characteristic healthcare insurance reform: with clear target and path. China Health Insurance. 2020;4:10.

2. Huang G, Qiu Y. The modernization of insurance governance: internal logic and choice of path. J Sichuan Univ. 2019;2:92–104.

3. Wang Z. The difference between urban and rural healthcare system and the strategy of integration. China Soc Sec. 2017;10:75–77.

4. Xin G. The exploration and rethink of China’s healthcare insurance payment reform: a case study of DRGs payment. Int Soc Secur Rev. 2019;3(3):78–91.

5. Song Z, Zhu L. The impact on urban healthcare insurance fund sustainability by the promotion of critical illness healthcare insurance. Insur Study. 2014;1:98–107. doi:10.13497/j.cnki.is.2014.01.011

6. Lei X. Current problems and countermeasures of medical insurance fund supervision in China. Chin Health Economics. 2019;38(8):31–33. doi:10.7664/che20190807

7. Wang W, Zhan K. The role of Non-Governmental Sectors in the modernization of health insurance governance. Int Soc Secur Rev. 2018;2(1):82–91.

8. Wang Z. These points have been clarified by healthcare insurance reform. Health Newspaper. 2020. sect. 7.

9. Zhang R, Yang W, Chen J. Analysis and countermeasures of immediate settlement of medical insurance for patients with covid-19. China Health Insurance. 2020;4:70. doi:10.19546/j.issn.1674-3830.2020.4.018

10. Zhu M, Zhao Y, Xie J. The security system establishment and completion for special pandemic emergency medical rescue and personal injury. Insurance Theory Pract. 2020;2:8.

11. De L, Hong Q. The responsibility of the healthcare insurance to SARS- interview with Yao Hong the deputy director general of healthcare insurance department of social security. China Soc Sec. 2003;6:38.

12. Hai Y, Xiaonan L. How does the healthcare insurance react to covid-19 pandemic and the consideration. China Health Insurance. 2020;3:12. doi:10.3969/j.issn.1674-3830.2020.3.010

13. Ying Hua. The healthcare insurance policies of typical countries and the inspiration. China Soc Sec. 2020;12:80.

14. Zhu H. The effect of strategic purchasing of healthcare insurance fund to push the development of healthcare insurance and medical care. China Health Insurance. 2020;2:6.

15. Quan L. the effect of healthcare insurance in public health emergency management. China Health Insurance. 2020;3:9.

16. Lin W. China’s success on universal health insurance coverage for 1.3 billion people. Chin Med J. 2015;9:39.

17. Wang C, Shubin H, Yang X, Mao Z. The quick survey on satisfaction of people under different healthcare coverage in Hubei Province. China J Soc Med. 2014;3:82. doi:10.3969/j.issn.1673-5625.2014.03.013

18. Healthcare Security Administration of Guangdong Province. Guangdong: service satisfaction survey in relation to healthcare security administration of Guangdong Province; 2021. Available from: http://hsa.gd.gov.cn/.

19. Guo J, Zhu J. The Importance of commercial medical insurance in the prevention and control system of major epidemic disease. China Insur. 2020;2:10.

20. Jiang Z, Wang L, Guo J. The impact brought by the covid-19 pandemic on China’s insurance industry and the response. China Econ Trade Herald. 2020;4:82.

21. Sun W, Yang L, Wang L, Liu C. The impact of covid-19 pandemic and the transformation and development of insurance industry: short run and long run perspective. Insurance Theory Pract. 2021;5:19.

22. Zhu H. Supplier’s marketization reform is the breakthrough of healthcare insurance. China Health Insurance. 2016;12:26–27. doi:10.3969/j.issn.1674-3830.2016.12.011

23. Zhu H. Fiscal investment mechanism and the modernization of National Governance System: learning experience from decisions of the fourth plenary session of the 19th CPC Central Committee. J Econ Perspect. 2019;12:13.

24. Niu B, Liu Z. Analysis of “Shenmu healthcare insurance”. Chin Health Service Manage. 2013;9:646.

25. Yang Y. The significance of Shenmu healthcare reform. Soc Sci Dig. 2009;7:37.

26. Diao R, Wang G, Wang Y, Min L, Liu J. The exploration and practice of Nanjing healthcare insurance administration to use big data to deploy epidemic materials. China Health Insurance. 2020;4:49.

27. Qunhong W, Gao L, Liang L. Healthcare Security System: Opportunity and Challenge.

28. Zheng Z. Insist on the people-centered development concept of healthcare insurance. China Health Insurance. 2021;6:23. doi:10.3969/j.issn.1674-3830.2021.6.021

29. National Healthcare Security Administration. Beijing: statistical bulletin of healthcare security development in 2020; 2021. Available from: http://www.nhsa.gov.cn/.

30. Shen S, Zhu Y. The prevention and control of major epidemic disease and the completion of our health care system. J Party Sch Cent Committee C P C. 2020;24(3):30–31. doi:10.14119/j.cnki.zgxb.2020.03.004

31. Zhu H. The healthcare insurance is not “god of medicine”. Popular Tribune. 2019;2:38.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2022 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.