")

Back to Journals » Psychology Research and Behavior Management » Volume 13

Investment Behavior of Orphan and Nonorphan Investors During COVID-19 in Shanghai Stock Market

Authors Ahmad MI , Zhuang W , Sattar A

Received 4 May 2020

Accepted for publication 28 July 2020

Published 25 August 2020 Volume 2020:13 Pages 705—711

DOI https://doi.org/10.2147/PRBM.S260541

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Igor Elman

Muhammad Ishfaq Ahmad,1 Weiqing Zhuang,1 Anika Sattar2

1School of Internet Economics and Business, Fujian University of Technology, Fuzhou, Fujian, People’s Republic of China; 2Department of Public Administration and Law, Liaoning Technical University, Fuxin, Liaoning, People’s Republic of China

Correspondence: Weiqing Zhuang

School of Internet Economics and Business, Fujian University of Technology, No.33 Xue Yuan Road, University Town, Minhou, Fuzhou, Fujian, People’s Republic of China

Tel +86-13805012485

Email [email protected]

Purpose: Orphaned children carry many psychological and emotional issues with them throughout their lives, which influence every decision they make, including investment decisions. A lack of self-determination and low confidence may make orphans make more risky decisions than their nonorphan counterparts. In this study, we aimed to see how this risky behavior was reflected in investment choices during the COVID-19 pandemic.

Methods: A well-structured questionnaire was distributed to 230 adult investors (130 orphans and 100 nonorphans) between January 22 and March 13, 2020.

Results: Orphans were found to be risk-takers during the COVID-19 pandemic, as hypothesized from their childhood history. Moreover, female investors showed more sensible (less risky) behavior than male investors when investing in fixed-income securities. Income and age showed significant inverse relationships with risk tolerance, while education showed a positive but insignificant effect.

Conclusion: This study indicates that orphan investors enjoy taking risks and their behavior toward risk remains consistent, even in abnormal conditions, such as a global pandemic. It also suggests that their risk-taking behavior remains stable from orphanhood through to adulthood, contradicting many reports that orphans make reasonable decisions in adulthood.

Keywords: global pandemic, risk-taking behavior, adulthood, investment choices

Introduction

Investment theories suggest that investors make their decisions rationally, based on publicly available information. Individual investment decisions depend on several characteristics, ranging from market characteristics (eg, expected risk, rate of return, transaction costs, market environment)1 to investor demographics (eg, education, age, sex)2,4 and personal characteristics (eg, personality traits, values, emotions, risk tolerance).5 However, how orphanhood affects future investment decisions is a unique investor characteristic that has been largely ignored in the finance literature.

According to one census, 153 million adolescents had lost their mother (maternal orphans) or father (paternal orphans), of whom 17.8 million had lost both parents. The stress experienced during orphanhood is a risk factor for poor mental health in children, as well as influencing individuals’ psychology and personality in adulthood. The stressful experiences faced by orphans damage their personalities and creativity and influence their interpersonal relationships,6,7 while communication deficiencies result in poor self-image and poor management of internal and external stressors. Given the significant number of adults who have experienced orphanhood, there is an urgent need to explore the financial decisions and investment behavior of these individuals compared to nonorphan investors. During the COVID-19 pandemic, the whole world went into lockdown and world-leading stocks showed negative returns. This study is an effort to measure investment behavior among Chinese orphan and nonorphan investors during COVID-19.

Literature Review and Hypothesis Development

The difference between maternal orphans and paternal orphans’ output in terms of socioeconomics and education remains inconclusive. Several studies have reported that children who have lost their mother (maternal orphans) show poor schooling results compared to children who have lost their father (paternal orphans), and loss of the father is associated with poor socioeconomic status.8,11 In contrast, paternal orphans were more likely to be behind in school.12,13 Along the same lines, maternal orphans suffer a permanent gap of 1 year of formal education, with no effect found for paternal orphans. Undoubtedly, investment decisions on different securities have a direct effect on socioeconomic status. On the basis of the cited literature, we hypothesized that:

H1: There is a significant difference between orphan investors and nonorphan investors in risk-taking behavior through investment choices during COVID-19. H2: There is a significant difference between maternal orphan investors and paternal orphan investors in risk-taking behavior through investment choices during COVID-19.

There have been a number of studies showing that men are more risk-tolerant than women.14,15 The role of women as mothers may be one explanation of this difference, as they prefer a lower fixed income rather than a greater amount of uncertain income. Women estimate the likelihood of gains and losses differently from men.16 This role of sex difference may vary with different cultures.17 In light of this literature, we hypothesized that:

H3: There is a significant difference between men and women in their risk-taking behavior through investment choices during COVID-19.

Education plays an important role in the acceptance of financial risk associated with different types of financial investments. Investors avoid engaging in transactions of which they lack understanding.15 Investors with higher levels of education exhibit more risk tolerance.14 There is no significant influence of education on financial risk tolerance.11 Therefore, we hypothesized that:

H4: Education level matters significantly in investors’ risk tolerance during COVID-19.

Income level has an important role in investment decisions. Higher-income investors exhibit lower risk aversion than those on lower incomes.14,18 Higher-income investors are more likely to invest in risky investment options. In light of the literature, we hypothesized that:

H5: There is a positive relationship between income level and risk-taking during COVID-19.

The relationship between age and financial risk tolerance remains inconclusive. Studies have shown that risk tolerance increased with age.14,19 On the other hand, young investors are more risk-tolerant than their older counterparts.20 Therefore, it was hypnotized that:

H6: Age has a significant impact on investors’ risk tolerance during COVID-19.

Methods

We collected the primary data online through WeChat, the most commonly used social software in China. We used nonprobabilistic sampling, a mix of judgmental and convenience sampling, to determine which individuals to approach. A total of 250 questionnaires were received, of which 20 were incomplete, leaving 230 questionnaires that were used for analysis. Data were analyzed using the Mann–Whitney U and χ2 tests.

The survey was conducted in China from January 22 to March 13, 2020 during the COVID-19 outbreak. The questionnaire consisted of two parts. The first part asked about demographic characteristics (eg orphan/nonorphan, sex) and the second part presented five statements for response about risk-taking behavior during COVID-19. Risk was characterized into two dimensions: aboveaverage risk and below average. The statements were taken from Weber et al (2002),21 and responses were on a five-point Likert scale. Sample statements are shown below.

Statement: When investing money, the word safety is more important for me than the word return. Response: Strongly disagree 1 2 3 4 5 Strongly agree Statement: In the investment process, if it happens, I would not mind losing some money. Response: Strongly disagree 1 2 3 4 5 Strongly agree

We employed the following regression model in our analysis of responses.

where β1 represents male vs female, β2 orphan vs nonorphan, β3 maternal orphan vs paternal orphan, β4 age of participants, β5 education level of respondents, and β6 income of the participants.

Results and Discussion

Demographics

Table 1 summarizes the demographic details of all the included respondents. Of 230, 56% were orphans, which is a significant representation in the sample from which to measure the effect of this demographic characteristic on investment behavior. In sum, 57% of the orphans were maternal orphans, while 42% were paternal orphans. Subjects were in diverse age-groups, starting from 25 years to >45 years. The largest age-group representation was 26–35 years (39.6% of the total sample) followed by 35–45 years (33.9% of the total sample). There have been controversial findings with regard to age related to financial risk.2 The majority of respondents’ level whad had school/college education (53.9%) and master’s degree holders comprised 5.7%. Income played significant role in investment decisions and risk tolerance: 61.7% of participants were in the income bracket of CN¥3,100–8,100/month) and only 10.5% of respondents earned >CN¥13,000/month.

|

Table 1 Respondent Demographics |

Investment Preferences

Respondents were asked to rank four investment types from most preferred (1) to least preferred (4; Table 2). Equity was the most preferred investment option for our respondents during COVID-19 and bonds the least preferred. This finding is interesting, as equity investment is considered the riskiest investment and investment in debt considered relatively safe, as it gives fixed returns.

|

Table 2 Investment Preferences Among Total Sample |

Investment Decisions Made by Orphan versus Nonorphan Investors

Orphan and nonorphan investors differed significantly in equity investments during COVID-19 (Table 3). This may have been due to orphan investors being accustomed to taking more risks during their childhood, due to the loss of their parents. There was also a difference between investments in mutual funds at the 10% level of confidence (Table 3).

|

Table 3 Differences between Investment Decisions Made by Orphan and Nonorphan Investors |

Investment Decisions Made by Maternal versus Paternal Orphan Investors

Interestingly, there was a significant difference between maternal and paternal orphans in their investments in mutual funds (at the 1% confidence level) and bonds (at the 5% confidence level) (Table 4). However, surprisingly no significant difference was found between these groups in equity investment (Table 4). This may have been a result of paternal orphans staying with the mother, which may influence a child’s behavior, as women are more risk-averse than men.

|

Table 4 Differences Between Investment Decisions Made by Maternal and Paternal Orphans |

Investment Decisions Made by Male and Female Investors

A significant difference was found between men and women making equity investments, which — given that these are among the riskier investments — is consistent with the previous argument that women are more sensitive to risk. This difference also existed in bond investments at the 10% confidence level in Table 5.

|

Table 5 Differences Between Investment Decisions Made by Men and Women |

Investment Decisions Made by Different Age-Groups

The Kruskal–Wallis test was employed to assess whether investment choices varied by age-group. The results in Table 6 showed that age did matter significantly in equity, mutual funds, or bonds as a choice of investment avenue.

|

Table 6 Differences Between Investment Decisions Made by Different Age-Groups |

Investment Decisions Made as per Different Education Levels

To test whether education level affected the choice of investment avenue, the Kruskal–Wallis test was applied. The results in Table 7 showed that education differences were significant in choices of equity, mutual funds, bonds, and real estate. This implies that education plays an important role in investment decisions.

|

Table 7 Differences Between Investment Decisions Made by Different Education Levels |

Investment Decisions Made by Different Income Levels

Kruskal–Wallis test results presented in Table 8 show that people of different income groups vary significantly with respect to equity and mutual bonds investment. Different income groups did not vary in respect to investment in bonds or real estate (0.821 and 0.352, respectively).

|

Table 8 Differences Between Investment Decisions Made by Different Income Groups |

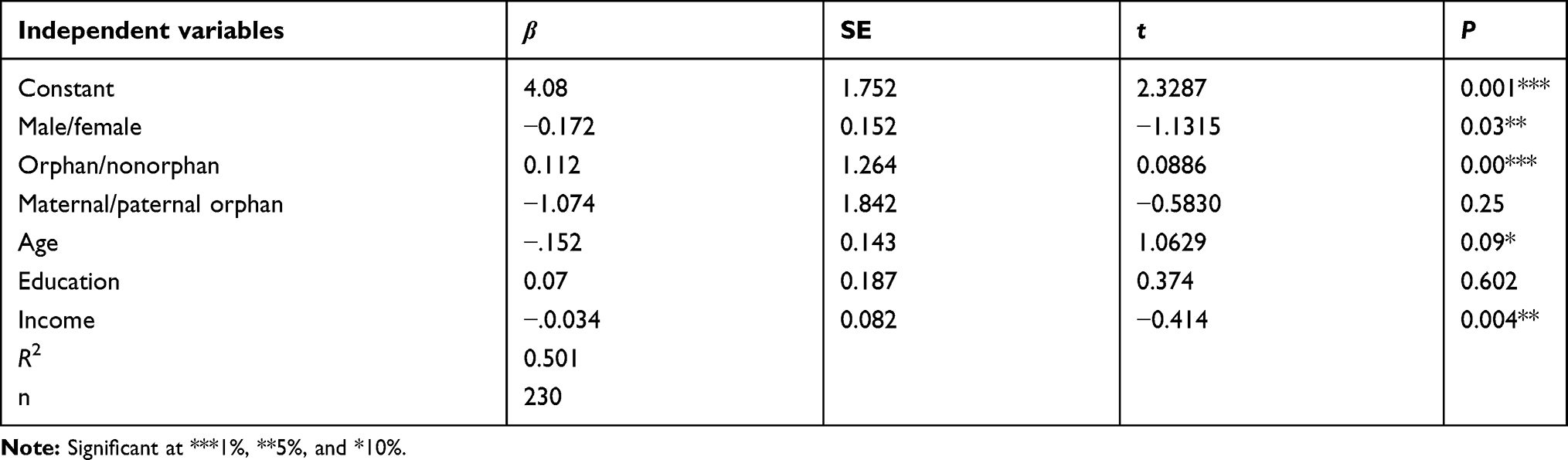

Risk Tolerance

As expected, the regression analysis clarified that sex negatively affected risk tolerance during COVID-19 investment decisions (Table 9). Most interestingly, orphans continued to take risks during the COVID-19 pandemic, showed a significant positive trend. This suggests that during this period, when world-leading stock markets showed negative returns, orphans enjoyed taking even more risk, reflected in their investment behavior. This is also evident in the former analysis, as orphans preferred to invest in equities, which are very risky investments. Attitudes toward risky investments in maternal vs paternal orphans showed a slight negative trend, but it was not significant. Age-group was found to be negative and significant at the 10% level of significance. This showed that young investors were more likely invest in risky options. Education remained positive with risk tolerance, but insignificant. The results are consistent with prior research that showed there was insignificant influence on education on financial risk tolerance.22 The overall model was significant, with an acceptable R2 of 0.501.

|

Table 9 Risk Tolerance Among the Groups |

Conclusion

Behavioral finance explains the psychological and emotional factors that influence individual investment decisions. This study examined investors’ behavior during COVID-19 in the Shanghai Stock Market. We focused in particular on the effect of orphanhood on individual investors and risk-taking behavior. The study revealed that orphan investors tended to invest in risky securities like equities, even during the COVID-19 pandemic, which caused worldwide stock-market volatility. Regression analysis of gender and risk tolerance indicated that women tended to make less risky decisions than men.

A limitation of this study was that it was conducted with investors of only one country, one nationality, and on one stock exchange. Future studies should similarly examine how orphan and nonorphan investors around the world behave with regard to global stock exchanges during the COVID-19 pandemic. This study suggests that irrational behaviors persist in orphans even into adulthood, consistent with the literature that indicates orphanhood disturbs such psychological traits as creativity and decision-making throughout life. Furthermore, it contradicts traditional investment-behavior theories that investors make rational decisions based on the available information.

Ethical Approval and Consent to Participate

All participants provided written informed consent to participate in the study after having received a description of the aims. Confidentiality and anonymity were ensured. Instructions were given in written form. Participants were given the right to withdraw from the study at any time and their responses would not be included in the study. The study was approved by the ethical committee of Fujian University of Technology.

Acknowledgments

We are thankful to Professor Wang Chun for his valuable comments and guidance throughout the project. Additionally, we are grateful to anonymous reviewers for their valuable suggestions for overall improvement of the document.

Author Contributions

All authors made substantial contributions to conception and design, acquisition of data, or analysis and interpretation of data, took part in drafting the article or revising it critically for important intellectual content, gave final approval to the version to be published, and agree to be accountable for all aspects of the work.

Disclosure

The authors report no conflicts of interest in this work.

References

1. Mayfield S, Shapiro M. Gender and risk: women, risk taking and risk aversion. Gend Manag. 2010;25(7):586–604. doi:10.1108/17542411011081383

2. Bali T, Demirtas O, Levy H, Wolf A. Bond versus stocks: investors’ age and risk taking. J Monet Econ. 2009;56(6):817–830. doi:10.1016/j.jmoneco.2009.06.015

3. Ozmen O, Sumer Z. Predictors of risk-taking behaviors among Turkish adolescents. Pers Individ Dif. 2011;50(1):4–9. doi:10.1016/j.paid.2010.07.015

4. Young S, Gudjonsson G, Carter P, Terry R, Morris R. Simulation and risk-taking and it relationship with personality. Pers Individ Dif. 2012;53(3):294–299. doi:10.1016/j.paid.2012.03.014

5. Gaviţa OA, David D, Bujoreanu S, Tiba A, Ionuţiu DR. The efficacy of a short cognitive–behavioral parent program in the treatment of externalizing behavior disorders in Romanian foster care children: building parental emotion-regulation through unconditional self- and child-acceptance strategies. Child Youth Serv Rev. 2012;34(7):1290–1297. doi:10.1016/j.childyouth.2012.03.001

6. Mohammadzadeh M, Awang H, Ismail S, Kadir Shahar HK. Stress and coping mechanisms among adolescents living in orphanages: an experience from Klang Valley, Malaysia. Asia Pac Psychiatry. 2018;10(1):e12311. doi:10.1111/appy.12311

7. Weber E, Blais A, Betz N. A domain-specific risk-attitude scale: measuring risk perceptions and risk behavior. J Behav Decis Mak. 2002;15(4):263–290. doi:10.1002/bdm.414

8. Case A, Ardington C. The impact of parental death on school outcomes: longitudinal evidence from South Africa. Demography. 2006;43(3):401–420. doi:10.1353/dem.2006.0022

9. Case A, Paxson C, Ableidinger J. Orphans in Africa: parental death, poverty, and school enrollment. Demography. 2004;41:483–508. doi:10.1353/dem.2004.0019

10. Nyamukapa C, Gregson S. Extended family’s and women’s roles in safeguarding orphans’ education in AIDS-afflicted rural Zimbabwe. Soc Sci Med. 2005;60(10):2155–2167. doi:10.1016/j.socscimed.2004.10.005

11. Yamano T, Jayne TS. Measuring the impact of working-age adult mortality on small-scale farm households in Kenya. Wld Devlt. 2004;32(1):91–119.

12. Parikh A, DeSilva MB, Cakwe M, et al. Exploring the Cinderella myth: intrahousehold differences in child well-being between orphans and non-orphans in Amajuba District, South Africa. AIDS. 2007;21:S95–S103. doi:10.1097/01.aids.0000300540.12849.86

13. Timaeus IM, Boler T. Father figures: the progress at school of orphans in South Africa. AIDS. 2007;21(Suppl 7):S83–S93. doi:10.1097/01.aids.0000300539.35720.a0

14. Grable JE. Financial risk tolerance and additional factors that affect risk taking in everyday money matters. J Bus Psychol. 2000;14(4):625–630. doi:10.1023/A:1022994314982

15. Anbar A, Eker M. An empirical investigation for determining of the relation between personal financial risk tolerance and demographic characteristic. Ege Acad Rev. 2010;10(2):503–523.

16. He X, Inman J, Mittal V. Gender jeopardy in financial risk taking. J Mark Res. 2007;45(4):414–424.

17. Maxfield S. Stock exchanges in low and middle income countries. Int J Emerg Mark. 2009;4(1):43–55. doi:10.1108/17468800910931661

18. Grable JE, Lytton R. Development of a risk assessment instrument: a follow-up Study. Fin Svcs Rev. 2003;12(3):257–274.

19. Kourtidis D, Sevic Z, Chatzoglou P. Investors’ trading activity: a behavioral perspective and empirical results. J Socio-Econ. 2011;40(5):548–557. doi:10.1016/j.socec.2011.04.008

20. Grable J, Lytton R, O’Neill B. Projection bias and financial risk tolerance. J Behave Finance. 2004;5(3):142–147. doi:10.1207/s15427579jpfm0503_2

21. Weber E, Blais A, Betz N. A domain-specific risk-attitude scale: measuring risk perceptions and risk behavior. J Behav. 2002;15(4):263–290.

22. Hallahan T, Faff R, McKenzie, M. An exploratory investigation of the relation between risk tolerance scores and demographic characteristics. J Multi Financ Mngmt. 2003;13(4/5 ):483–502.

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.