")

Back to Journals » Risk Management and Healthcare Policy » Volume 13

Effect of Community-Based Health Insurance on Utilization of Outpatient Health Care Services in Southern Ethiopia: A Comparative Cross-Sectional Study

Authors Demissie B , Gutema Negeri K

Received 15 May 2019

Accepted for publication 9 February 2020

Published 25 February 2020 Volume 2020:13 Pages 141—153

DOI https://doi.org/10.2147/RMHP.S215836

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Dr Kent Rondeau

Bekele Demissie,1 Keneni Gutema Negeri2

1USAID/Integrated Family Health Program, SNNPRS, Hawassa, Ethiopia; 2Health Systems Management and Policy Unit, College of Medicine and Health Sciences, Hawassa University, Hawassa, Ethiopia

Correspondence: Bekele Demissie

USAID/Integrated Family Health Program, SNNPRS, P. O. Box 1383, Hawassa, Ethiopia

Tel +251 916823180

Email [email protected]

Background: Community-based health insurance schemes are becoming increasingly recognized as a potential strategy to achieve universal health coverage in developing countries. Despite great efforts to improve accessibility to modern health-care services in the past two decades, in Ethiopia, utilization of health-care services have remained very low. Given the financial barriers of the poor households and lack of sustainable health-care financing mechanisms in the country has been recognized to be major factors, the country has implemented community-based health insurance in piloted regions of Ethiopia aiming to improve utilization of health-care services by removing financial barriers. However, there is a dearth of literature regarding the effect of the implemented insurance scheme on the utilization of health-care services.

Objective: To analyze the effects of a community-based health insurance scheme on the utilization of health-care services in Yirgalem town, southern Ethiopia.

Methods: The study used both a quantitative and qualitative mixed approach using a comparative cross-sectional study design for a quantitative part using a randomly selected sample of 405 (135 member and 270 non-member) household heads. To complement the findings from the household survey, focus group discussions were used. Multivariate logistic regression was employed to identify the effect of community-based health insurance on health-care utilization.

Results: The study reveals that community-based health insurance member households were about three times more likely to utilize outpatient care than their non-member counterparts [AOR: 2931; 95% CI (1.039, 7.929); p-value=0.042].

Conclusion: Community-based health insurance is an effective tool to increase utilization of health-care services and provide the scheme to member households.

Keywords: community-based health insurance, health-care utilization, health-care financing, universal health coverage, developing countries

Background

In most Low and Middle Income (LMIC) countries, utilization of modern health-care services has remained very low.1 Financial constraint is one of the major barriers for access to and utilization of modern health-care services in these countries. Furthermore, poor quality of health-care services at public providers and the absence of pre-payment financial arrangements for health care were major factors for this lower utilization of health care services.2,3

Moving away from out-of-pocket (OOP) payments for health care at the time of use to pre-payment (health insurance) is an important step towards averting the financial hardship associated with paying for health-care services. Therefore, Community-Based Health Insurance (CBHI) has become part of an overall health financing strategy in a number of countries, several governments in these countries have embraced community-based health financing with national policies and administrative support to the implementation of a number of CBHI for improving utilization of health-care services by reducing OOP health expenditures. CBHI is a prepayment plan by informal sectors in rural areas to overcome financial hardship by pooling of health risks and of funds that takes place at the level of the community.4

Despite shortage of OOP payment for the service at the point of service with respect to the required amount of payment, a household’s income might also be lower compared to the required user fees. Therefore, CBHI is an instrument that minimizes such financial barriers to access the health care. At the same time, the enrollees are relieved from selling of their assets or searching for credit that may predispose them to catastrophic expenditure. Health-care seeking might also be quicker and recovery from disease could be earlier among the enrollees.5

Ethiopia is the second most populous nation in Africa. In terms of access to modern health care and various other health indicators, the country ranks low even as compared to other Sub Saharan African countries.6 Despite Ethiopia’s health sector's encouraging achievements to improve access to modern health-care services (access to primary health-care services was 92.1% in 2014/15, health-service delivery and health status of the population remain low. Between 2010 and 2015 outpatient visit per capita had marginally increased from 0.29 to 0.48.7,8 This is due partly to the low level of health-sector financing. Ethiopia’s health sector remains underfinanced when compared with the WHO-recommended minimum spending of US$60 per person per year to provide basic health-care services in developing countries. In 2010/11, the country's main health-care financing sources were donation (50%), households (34%), and government (only 16%). The financial source from the households are burdened by high OOP costs for health that usually are incurred at time of sickness. Furthermore, access to a well-developed health insurance system in the country was limited and only about 2% of the health-care financing was covered by employers, particularly by private insurance institutions.9

Cognizant of the under financing of health care in Ethiopia, the country approved a health-care financing strategy in 1998. The strategy also identifies health insurance as a mechanism to generate additional sources of revenue, and a way to increase the country’s low level of health service utilization. In light of this, the government has embarked on implementing two types of health insurance schemes, Social Health Insurance (SHI) for the formal sector and CBHI for the informal sector. As a prelude to national coverage, implementation of CBHI has been started as a pilot program in 13 districts of the four largest regional states of the country since June 2011 and is currently being scaled-up throughout the country. One of the major objectives was to promote equitable access to and utilization of sustainable quality health-care services for the majority of Ethiopian families via the health sector.10,11

The Ethiopian CBHI scheme is characterized as a government run program with community involvement in scheme design, management, and supervision. The financial source of the scheme is mainly the premium contribution of members and about 25% of the total premium subsidy from the central government. While district and regional governments are expected to cover the costs of providing a fee waiver for the poorest population groups (about 10% of the total population). Membership to the CBHI scheme is voluntary and at household level. The CBHI scheme benefit package for members includes health-care cost coverage of both outpatient and inpatient health -are services in public facilities, but covers neither treatment outside the country nor medical treatment with largely cosmetic value. CBHI members are expected to first visit a health center, which can provide referral letters to higher level care at district or regional hospitals as needed.11

Theoretically, any price decrease through an insurance claim should enhance the utilization of health-care services during the time of illness. Since CBHI brings down the price of health care, there would be better access to modern/formal health facilities and higher utilization of health-care services by insured individuals. Thus, CBHI provides equitable access to health facilities, irrespective of income and gender while reducing financial burden of illness.12,13

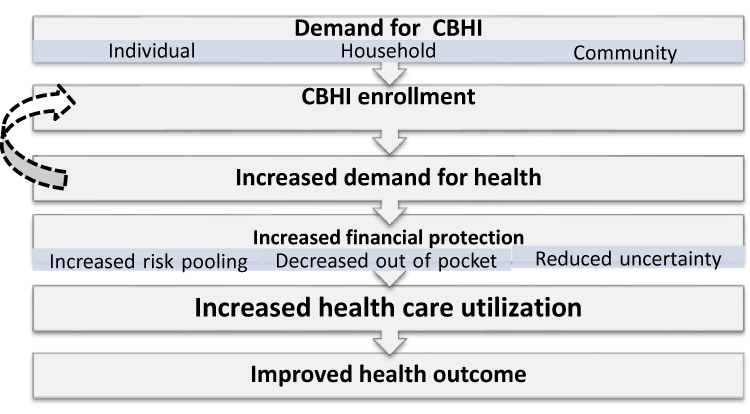

As illustrated in the conceptual framework of the study (Figure 1), demand for CBHI is shaped by factors at the individual household and community levels. These factors might include socio-demographic, economic and health-related characteristics of the household and its individual members. Once enrolled, insurance is expected to increase the demand for health care by lowering the price of care at the point of service delivery which results in demanding more services. Thus, insurance can lead to an increase in health-care utilization (Figure 1).5,14

|

Figure 1 Theoretical mapping of the study. |

Empirical evidence from a systematic review of the studies carried out in LMICs has provided strong evidence for the impact of CBHI on access to and utilization of health-care services.15–18 Other studies on the impact of CBHI also reported a significant difference of utilization of health-care services between the scheme members and non-members.19–22 With regard to the relationship between CBHI membership and choice of health-care service providers during illness incidence, According to a study from rural Cambodia, CBHI did have a significant effect for a person to receive care during a serious health-care incident. CBHI reduces the use of private providers as the first source of care by 11 percentage points (P < 0.05), and increased the use of public health centers as the first source of care by 18 percentage points (P < 0.001) (44).23

Differences between scheme members and non-members in utilization of modern health care was reported by a number of studies.20–22 For instance, in Burkina Faso, outpatient visits during illness was about 40% higher in the insured groups than the non-insured groups.20 On the other hand, one study in the same country reported no statistically significant difference in overall mortality between members and nonmembers.21 In Rwanda, higher utilization of health-care services was found among the insured non-poor than insured poor households.23 However, very few, if any, of these studies completed their quantitative findings with qualitative data.

There are limited reports in the literature on the impact of CBHI on utilization of health-care services in Ethiopia. In one study from North-West Ethiopia, health-care utilization rate for CBHI scheme members was 50.5% while for non-members this was 29.3%, and this difference was significant (P<0.05). The same study verified variables that have shown significant variations for enrollment such as; educational status, family size, occupation, marital status, travel time to the nearest health institution, perceived quality of care, first choice of place for treatment during illness.24 This study used a quantitative approach only.

A study on the impact of Ethiopia’s pilot CBHI scheme on health-care utilization and cost of care by Mebratie et al,25 found that utilization of outpatient services from public providers were 35% and 22% of CBHI members and non-members respectively. In addition to this, the evaluation report of the pilot CBHI scheme in Ethiopia by FMoH indicated that 72.3% of members visited health facilities while 69.3% of non-members from the pilot area had.26

Notwithstanding the scaling up, the CBHI debate continues to revolve around the effect of the scheme, in particular whether or not health insurance membership has improved utilization of health-care services among the target population. Besides, there are limited studies in Ethiopia in general and southern Ethiopia in particular regarding the role of CBHI on health-care utilization among enrolled members when compared to non-members. The few available studies used only quantitative analyses. Therefore, this study aims to analyze the difference in health-care utilization among CBHI enrollees and the non-enrollees using a mixed quantitative and qualitative approach in Yirgalem town of southern Ethiopia. Hence, this study could also provide useful evidence for policy makers health mangers and planners.

Methods

Study Design and Settings

The study used a mix approach of quantitative and qualitative study designs. The quantitative part used a comparative cross-sectional study design, because the same individual household heads were not followed over time, however, there was a need to compare and describe the outcome of interest in terms of the two groups (enrolled and non-enrolled members).

The qualitative study design was employed to have an in-depth insight to the study’s subject of interest. We used Focus Group Discussions (FGDs) in collecting the qualitative data to complement the emerging findings of the quantitative information. Given the cross-sectional nature of the survey, the qualitative results also helped to shed light on the direction of relationships between independent variables and CBHI enrollment.

The study was conducted from February 20, 2017 to March 13, 2017 in Yirgalem Town Administrative areas of Sidama Zone, in Southern Nations and Nationalities People’s Regional (SNNPR) State of Ethiopia. The town is among the CBHI piloted districts, it lies about 45 km south of Hawassa City, the capital city of SNNPR. Administratively the town is sub divided into six Kebeles (the lowest administrative unit). Based on 2007 national census projection, the town had an estimated population of 43,816 and 8,942 households for the fiscal year of 2016/17.24 The town has one public hospital (Yirgalem General Hospital) which serves as one of the referral centers for other health facilities of Sidama Zone and one public health center (Yirgalem Primary Health Care Unit). The choice of this study area is purposefully based on the researcher’s prior knowledge and familiarity of the town for the operational functioning of the CBHI program since piloting of the CBHI scheme in the country. Hence, the selected study setting enhances the availability of data, at least to a certain degree of accuracy, to assess the effect of the CBHI scheme on utilization of health -care services by comparing member households to non-members.

Study Population

The study populations were households in Yirgalem town. Due to the fact that CBHI coverage is modeled as the household head’s coverage in the country, household heads were considered as the study unit. The inclusion criteria of the study were households’ heads that were above 18 years old, who engaged in the informal sector for source of living and were not covered by other insurance schemes for health (ie, Social health insurance and Private Health Insurance). The exclusion criteria were household heads who were employed in the formal sector for source of living (including pension) and/or covered by other insurance schemes.

Sample Size and Sampling Procedure

The sample size was calculated using Open-Epi, version 3 computer-based sample size calculator software. Using a report from a previous similar study in the country: P1= 22% and P2=35% for CBHI non-member and member households respectively;26 95% confidence intervals (CI) and 20% precision; and 1:2 ratio for CBHI member and non-member households was used. Accordingly, a total sample size of 405 households was calculated to solicit the cross-sectional information, yielding 135 CBHI scheme member and 270 non-member households for the final analysis.

The study households were selected using a multistage sampling method. In the first stage three Kebeles (namely Abosto, Mehal Ketema, and Wuha Limat) out of the total six Yirgalem town Kebeles were randomly selected as primary sampling units. In the second stage, nine villages (3 villages per kebele) from the three selected Kebeles of the town were randomly selected, as secondary sampling units. Taking a fresh list of CBHI scheme member households available at the Kebeles administration Office, the required sample size for both groups in each of the selected villages determined using the population proportionate to the sample size (PPS). Finally, systematic sampling was used to select the study subjects for both CBHI member and the comparative non-member groups.

Study Variables

The dependent variable of the study was utilization of outpatient health-care services for illness episode of the family members. In this context, utilization of health-care services refers to the household visit for outpatient services from modern health-care providers (such as public health center and hospital, and private clinic and hospital). Independent variables were CBHI scheme membership status of the households; demographic and socio-economic characteristics of the individual head and the household (such as age, sex, marital status, education and occupation of the household head and monthly income and size of the household); and any illness of a family member for the last 12 weeks prior to the survey.

Data Collection

The quantitative data was collected from the selected CBHI member and non-member households using pre-tested interviewer-administered structured questionnaires adopted from the Federal Democratic Republic of Ethiopia, Ethiopian Health Insurance Agency Evaluation of CBHI pilot scheme in Ethiopia.27 Then the survey questionnaires were developed to elucidate information on the basic demographic and socio-economic characteristics of the households; incidence of illness and subsequent choice of health providers; and the amounts and sources of money used to finance the health-care services for illness of its members. The recall period was 12 weeks for outpatient health-care service utilization. The survey questionnaire had been translated into Amharic, the national work language in which most of the study area residents adequately listen and speaks; and then back-translated into English to validate its consistency.

Two trained data collector teams were used for the data collection, each team comprising of three data collectors and one field supervisor. The data collectors administered the interview to the selected household heads using Amharic language, which is the working language and respondents of the study were able to understand and speak it very well. Supervisors made spot-checks on the quality of data collection and ensured the questionnaires for completeness on a daily basis. In order to get adequate responses for comparative analysis of the study, the recall period used for utilization of outpatient service was 12 weeks prior to the survey. Further assessment for sources of care provider allowed us to see any possible effect of the scheme for a substantial shift from private to public health care providers.

For the qualitative study design, two villages that were not used for the household survey were purposively selected from two of the three sampled kebeles which were used for the household survey (namely Abosto and Wuha Limat). The two kebeles were selected due to the varying distance from the scheme contracted health center and to see the effect of these differences. Four focus group discussions, two in each of the two villages, were conducted with groups of eight participants. An effort was made to include participants with a range of characteristics to obtain a broad representation of the community. Per village, one of the FGDs was conducted with scheme members focused on their motivation for joining the scheme, while the other was conducted with non-members and focused on why they had never enrolled or had dropped out of membership of the scheme or chosen not to join the scheme. In addition, both insured and non-insured households also discussed about the benefit of the scheme and issues to be improved. All the FGDs were facilitated by trained moderators, and discussionnotes were taken and audio recorded.

Data was gathered using a prepared FGD guide that introduced the participants, described the objective of the study and was followed by open questions centering on status and reasons of their enrollment to CBHI, source of health care sought and utilization status.

Data Management and Analysis

To ensure quality of household survey data, training was given for data collectors and field supervisors on the data collection tools, sampling the study subjects, ethical issues and data collection procedures. The field supervisors monitored the data collection process using an “interviewer control checklist” and randomly re-checked the collected data using sampled questions and households. The collected data were reviewed by the field supervisors and principal investigator on a daily basis. To ensure the FGDs’ data quality, training was given for moderators of the discussions. And also the FGDs’ guide and the disunion procedures were pre-tested prior to the actual data collection.

The data from the completed questionnaires were entered and analyzed using International Business Machines (IBM) Inc. Statistical Package for the Social Sciences (SPSS) version 20 software. Data were also cleaned by running frequency before analysis and re-coded when necessary. Descriptive statistics were computed using cross tab, percentage and mean. Chi-square test was used initially to identify the various variables mentioned as the outcome measures, which could be a determinant for membership of the CBHI scheme and all relationships were tested at 0.05 level of significance. A binary logistic model was used for analysis of the CBHI scheme effect on utilization of health-care services. Initially bivariate analysis was computed to identify the significant effect of independent variables of the study on utilization of outpatient health-care services. Significant factors resulting from the bivariate analysis were subjected to a multivariate analysis to determine the effect of CBHI membership and other factors on the probability of utilization of outpatient health-care services. The final p-value ≤0.05 was considered to declare the significant factors along with Odds ratio and the correspondent 95% CI.

The qualitative data were also analyzed manually using Microsoft Word 2007 and code book. Notes were taken and the entire discussion was audio recorded and latter transcribed for analysis. Analysis was made using a thematic analytic approach. In doing so the emerging themes were coded and summarized under different thematic areas. Then responses were quantified where possible and quotes from participants were presented textually.

Ethical Considerations

The researchers obtained ethical approval from Hawassa University, College of Medicine and Health Sciences Institutional Research Board (IRB). Support letters from Yirgalem Town health unit was also obtained and given to selected kebele administrations to inform and seek their facilitation for this study. Also, after briefing about the study and ensuring confidentiality for their participation, verbal informed consent of the participants was obtained before the face-to-face interview and participation in the FGDs. Verbal informed consent for this research was approved by the same Hawassa University, College of Medicine and Health Sciences IRB as it was considered acceptable.

Results

Quantitative Findings

Background Description of the Study Participants

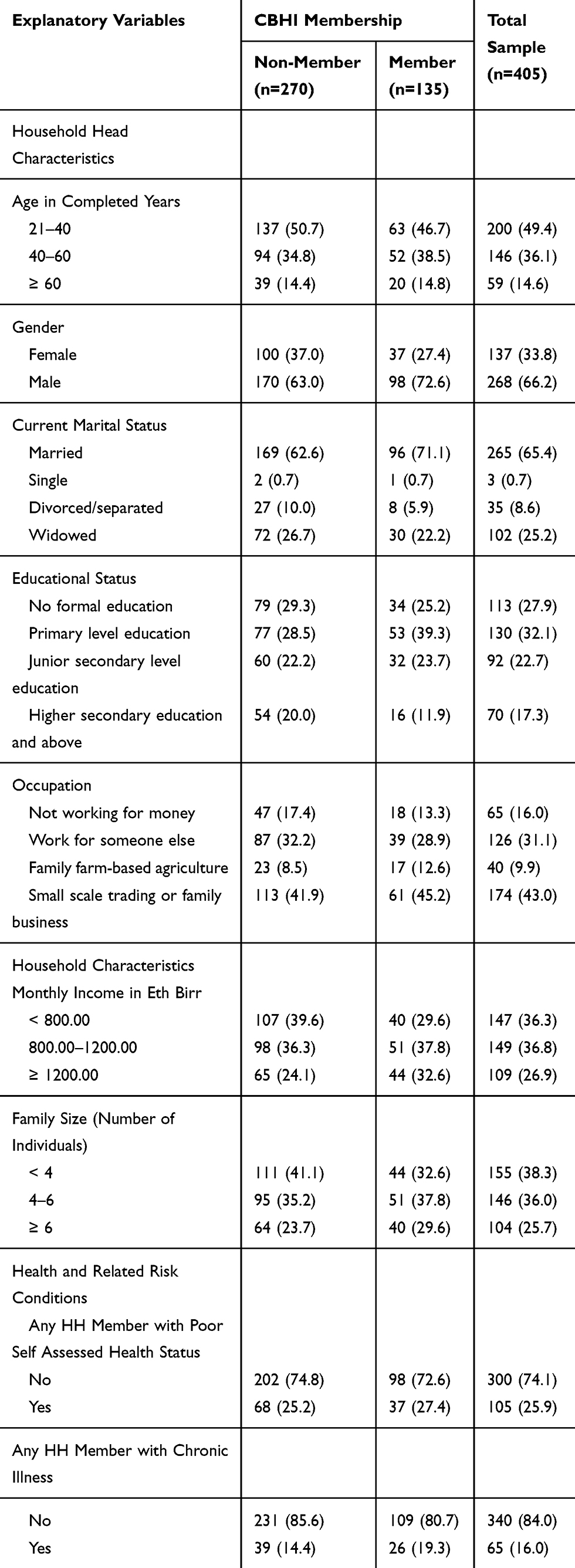

The quantitative household survey of this study included a sample of 405 households and 405 household heads (HH) participated in the study. They included 135 CBHI members and 270 non-member households, yielding a 100% response rate (Table 1).

|

Table 1 Description of the Household Survey Respondents by Current CBHI Scheme Membership Status in Yirgalem Town of Southern Ethiopia, February 2017 |

Descriptive statistics of the sampled households is shown in Table 1. Accordingly, about half of the sampled household heads (50.7% of non-members and 46.7% of the scheme members) were between the age 21 and 40 years.

Heads of the sample households were predominantly males and currently married, with 72.6% and 71.1% for CBHI members compared to 63.0% and 62.6% non-member households respectively. The greater proportion of the sampled households had formal education, of which 39.3% of the CBHI members and 28.5% of the non-member households had completed primary level education. With regard to occupation of the household head, 45.2% of CBHI members had an occupation of small scale trade or family business compared to 41.9% of the CBHI non-member households.

Estimated monthly income for the study households ranged between 300.00 and 3600.00 Eth. Birr. The mean monthly income was 1151.19 Eth Birr for CBHI members compared to 1041.35 Eth Birr for non-member households. A large proportion (51, 37.8%) of CBHI members’ estimated monthly income fell between 800.00 and 1200.00 Eth Birr. Family size less than 4 was 41% and 32.6% for enrolled and non-enrolled members respectively (Table 1). While poor self-assessed health status was 37 (27.4%) among the CBHI member HHs, it was 68 (25.2%) for non-members. Likewise, HH members with a history of chronic illness were 26 (19.3%) and 39 (14.4%) for CBHI members and non-members respectively (Table 1).

Effect of CBHI on Utilization of Health-Care Services

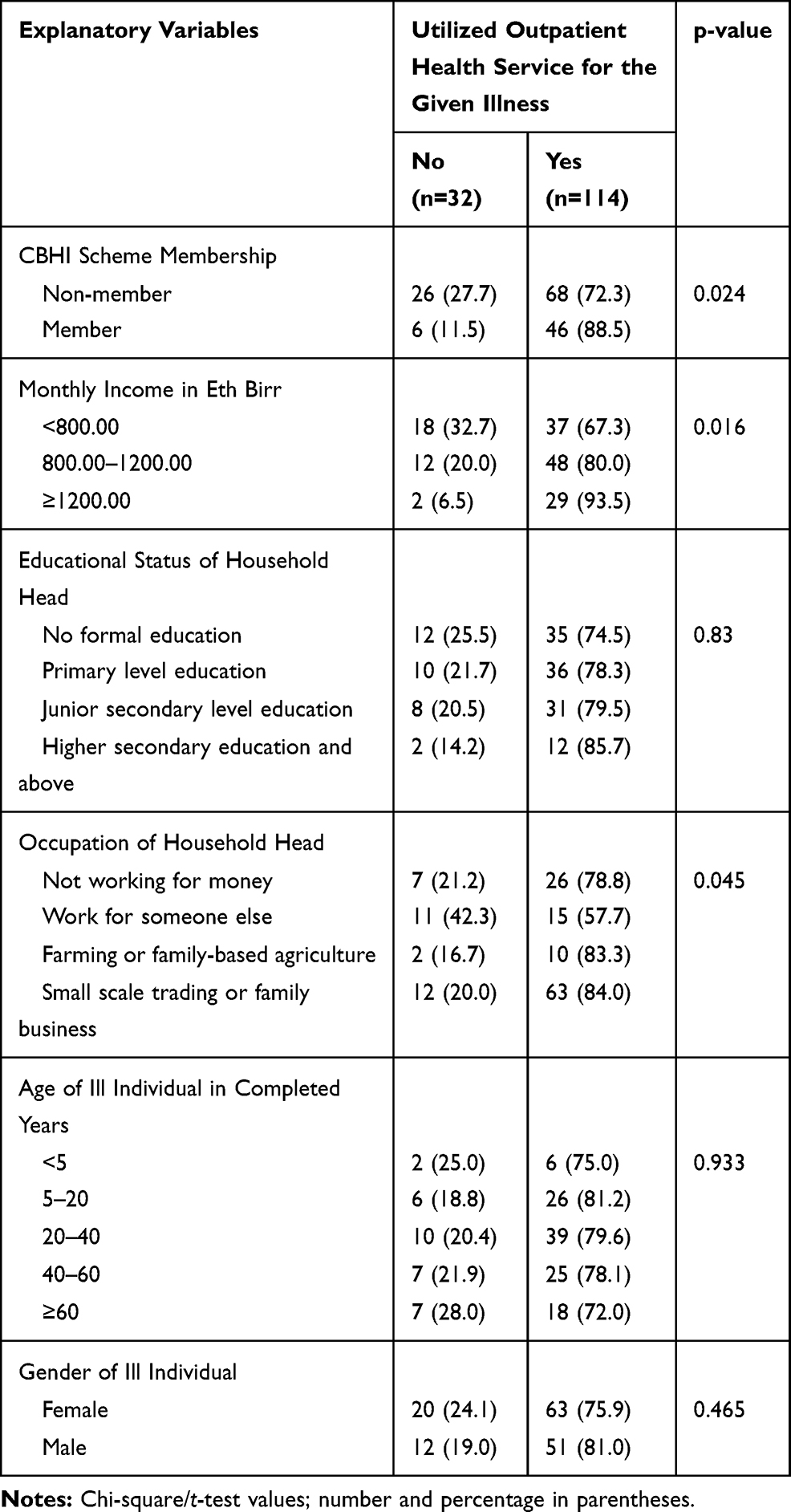

The household survey of this study covered 405 sampled households with a total of 2,112 individual members. Among these, a total of 146 individuals had reported at least one recent illness episode in the last 12 weeks prior to the survey, 52 and 94 individuals from CBHI scheme member and non-member households, respectively, as detailed in Table 2. Out of 114 (78%) individuals who had utilized outpatient services from modern health-care services providers, a higher proportion of individuals with illness from CBHI scheme members (46, 88.5%) sought outpatient health services compared to 68 (72.3%) non-member households. More individuals from higher (29, 93.5%) and middle income category (48, 80.0%) had sought health care than individuals from the lower income group (37, 67.3%). Also utilization of outpatient health-care services was higher for female than male individual household members, and ill individuals in the age group 20–40 had utilized outpatient health services than other age groups in both groups (Table 2).

|

Table 2 Description of Variables: Utilization of Outpatient Health Services for Illness in Yirgalem Town of Southern Ethiopia, February 2017 |

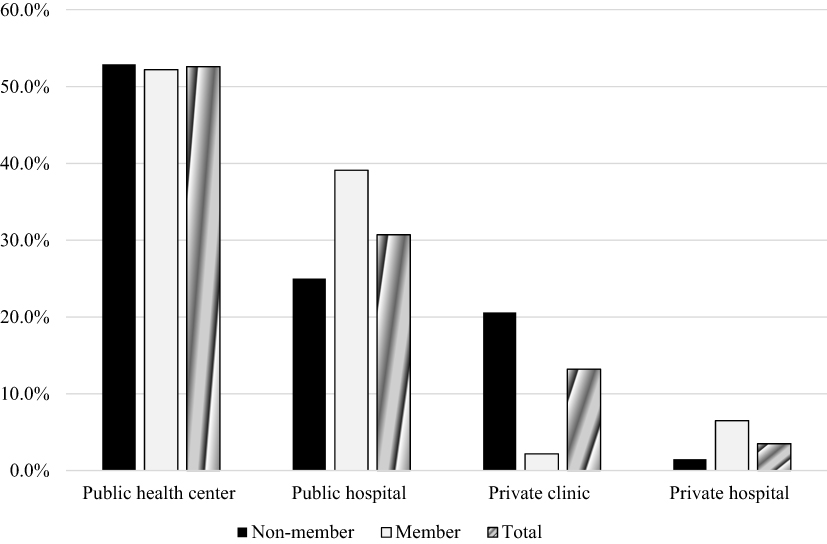

The types of health-service providers visited by CBHI scheme membership status is detailed in Figure 2 below. Accordingly, member households had higher utilization rate (39.1%) than non-member households (25%) in public hospitals, while a similar proportion (52.9% and 52.2%) for scheme member and non-member respectively utilized health care at public health centers.

|

Figure 2 Types of health care facilities visited for illness by CBHI scheme membership status of the households in Yirgalem town of Southern Ethiopia, February 2017. |

On the other hand, about 20.6% of the CBHI non-member ill individuals did utilize private clinics as compared to 2.2% of the ill individuals from CBHI member households.

In order to make sure that the observed differences were not just simply caused by the individual household head or household characteristics, a binary logistic model was estimated. The bivariate analysis of explanatory variables, including CBH scheme membership status, with outcome variable of the study was computed. Then, all the independent variables that were significant in the bivariate analysis were taken for multivariate analysis. Table 3 displays the results of the binary logistic regression analysis of the study.

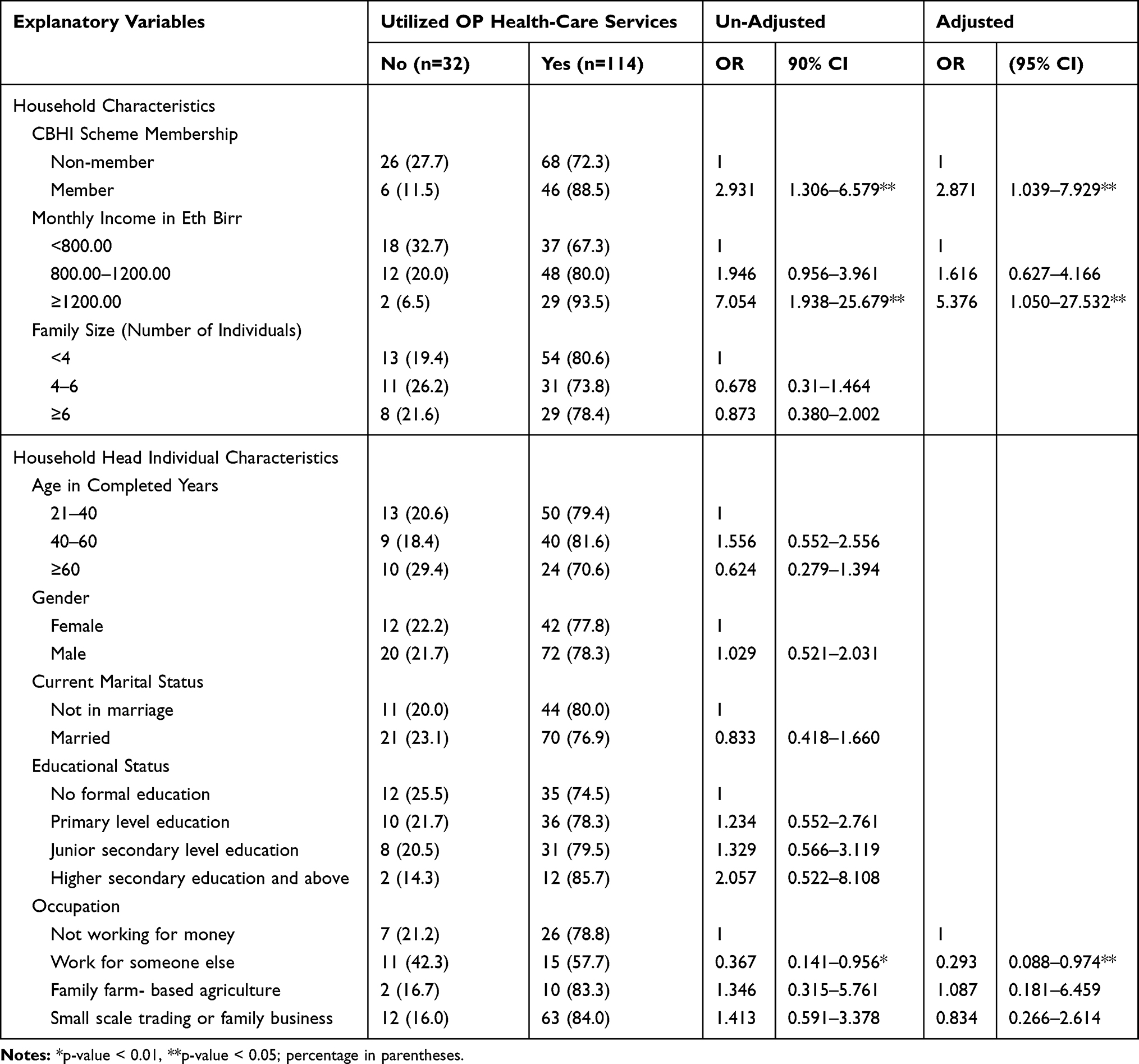

|

Table 3 Effect of CBHI and the Associated Factors on Utilization of Outpatient Health Care Services in Yirgalem Town of Southern Ethiopia, February 2017 |

The result of the current study reveals that there exists statistically significant association (P< 0.05) between CBHI scheme membership and utilization of outpatient health-care services. Compared to non-member households, scheme member households are about 2.87 times more likely to utilize outpatient services during illness of the individual household (AOR: 2.871; CI: 1.039–7.929).

With respect to other explanatory variables, this study found that monthly income is one that has shown a statistically significant association with utilization of outpatient health-care services. Households with a monthly income of more than or equal to 1200.00 Eth Birr were about 5 times more likely to utilize outpatient health-care services compared to those households with a monthly income less than 800.00 Eth Birr (AOR: 5.376; 95% CI: 1.050–27.532). Another observed significant factor is occupation of the household heads in which household heads category of “work for someone else" (household occupation group whose sources of income is wage from daily labor or professional employment in non-formal sectors) were found to be about 70% less likely to utilize outpatient health-care services compared to household heads category of “not working for money” (household occupation group whose sources of income are remittances and renting houses) (AOR: 0.297; 95% CI: 0.088–0.974). However other occupational groups of the household head have no significant associations.

Findings of the Qualitative Data

Analysis of the qualitative data from all the four FGDs indicated that the motives for enrollment for the CBHI scheme was risk pooling and social solidarity for the non-predicted illness incidences of family members of the households. All the FGDs’ participants who ever enrolled for the scheme (both current members and those whose membership had lapsed) reported that most eligible households were impressed by the sensitization and mobilization of the scheme, and showed an interest in becoming a member of the CBHI scheme. During the earlier years of the scheme implementation the premium was 10.50 Eth. Birr per month for a household, and almost all eligible households were enrolled for the scheme. One scheme member participant of the FGDs expressed the reason for enrollment as follows:

Incidence of illness in the family is not predictable as of death in the family. We have good culture for social solidarity in case of emergency situation for a household in the community, like “Edir” (a traditional mutual association to which members make monthly contributions and receive a payment to help cover funeral expenses in return) as a means of social, material and financial support for death of the household family member. We all are member of “EDIR” in our community and have regular financial contribution as a risk pooling mechanism. So I feel that CBHI scheme is novel venture for the household to cop up with health shock. This is the main reason for me to enroll for CBHI scheme, and I am still member of the scheme even with all its limitations.

–CBHI member from Wolima Village, Wuha Limat Kebele of Yirgalem Town

Furthermore, the FGDs found that the presence of a family member suffering from a chronic health condition was the second most frequently cited reason for the household enrollment to the scheme.

Joining CBHI is really convenient as I often see doctors about my diabetes and high blood pressure. Sometimes it is not only me who sees the doctors, but also my family members: one person has a fever or another person has a problem with his stomach.

–CBHI member from Wolima Village, Wuha Limat Kebele

In my case, I always get sick. Both the public health center and hospital are like my second home! I had an operation five months after enrolling in the scheme and several visits to the health center, but I did not pay anything for the health care services got there.

–CBHI member from Mehal Ketema Village of Abosto Kebele

In all two FGDs with non-members, the most frequent reason for never enrolling in CBHI was the inability to afford the premiums, followed by health problems were not a frequently occurring situation in the family. One FGD participant explained why his family’s financial situation prevents him from enrolling:

For me, it’s already difficult to pay for the insurance premium. Let alone the current premium amount of 300.00 Eth Birr per household annually, it was much difficult to pay the premium amount of 10.50 Eth Birr per month for the household in the earlier time. I have four children and three of them are attending school. So it much difficult even to meet other basic needs of my family with the income I got from daily labor work wage.

–Non-member from Mehal Ketema Village, Abosto Kebele of Yirgalem Town

In relation with infrequent occurrence of disease in the family one participant said:

No one in my family gets sick; I am not really interested in this scheme. When someone in my family gets sick, we just go to the hospital like any other patients.

–Non-member from Wolima Village, Wuha Limat Kebele of Yirgalem Town

Beside the above-mentioned reasons by the FGDs’ participants, the differential treatment given to members and non-members (cash-paying clients) and poor quality of health-care services at the scheme contracted public-health facilities were the most frequently stated challenges by most of the FGDs’ participants in both groups. Although a few respondents complained about the cleanliness of the hospital, most participants’ felt that the facilities were clean but that lack of equipment is a problem in the health center.

The findings from the FGDs also substantiates the quantitative descriptive facts that the scheme member HHs most frequently utilize the health service for illness while some non-members responded that they wait for improvement with home care before seeking modern health services. As one FGD participant stated:

Joining CBHI is really convenient as I often see doctors for my diabetes and high blood pressure…

–CBHI member from Wolima Village, Wuha Limat Kebele

The most frequent reason was the cheaper health-care costs relative to other providers. Some preferred using OOP health service from public hospitals than HCs due to the preference for quality services (including availability of basic drugs) and its geographical proximity for one of the sampled kebele. And a few participants expressed a preference for utilization of OOP health services from private providers due to perceived quality of health-care services, and presence of more competent and compassionate care providers.

Discussion

Universal equitable access to health services is a health policy goal. The importance of the CBHI scheme as a policy tool to eliminate financial barriers to access and utilize health services is being increasingly emphasized.12,13 To realize this effect the government of Ethiopia has demonstrated its commitment by providing its policy and administrative support and started the implementation of the CBHI scheme in June 2011.10,11 In the backdrop of limited studies in the country as well as in SNNPR on this aspect, the current study examined the extent to which the CBHI scheme, targeted at the poor households in the informal sector of Yirgalem town, has affected utilization of outpatient health-care services. This study applied quantitative techniques to household level survey data complemented with FGDsto analyze the effect of the CBHI scheme effect on utilization of outpatient health-services for the scheme member compared to non-member households.

The findings of this study support the hypotheses generated from the conceptual theory discussed in the introduction section, and it highlights two noteworthy findings: the CBHI scheme has had a positive effect on utilization of outpatient health-care services and the scheme members visited public health-care providers more than private providers to seek health care for illness of their individual members.

According to this study, 88.5% of individuals with illness from CBHI member households had utilized outpatient health services compared to 72.3% individuals from non-member households and the difference was significant (P<0.05). This finding is consistent with results from previous studies.17–22 In the study from India, utilization of health-care services were 6–7% higher for the scheme members than non-members.18 Similarly a study in Cambodia found that visits to public health-service providers were increased by 18% and by 11% from private providers by CBHI members.22 Another study from Burkina Faso also reported rates of health-care visits as 30% for insured compared to 12% for uninsured household members.20 In Rwanda, utilization of health services by CBHI members increased by 15% more than non-members.23 Correspondingly, a study in Ethiopia also found 40% of CBHI members utilized outpatient services compared to 29% of non-members.26 Therefore, in Ethiopia where utilization of outpatient service is low, the effect of CBHI to improve access to and utilization of health-care services is an important forward step.

In addition to increasing utilization, the finding of the current study shows that CBHI members use public sector facilities rather than private clinics. About 91.3% of ill individuals from the scheme member households utilized outpatient services from public health facilities compared to 77.9% of ill individuals from non-member households. In contrast, more of the non-member ill individuals had received outpatient services from private providers than member households, 22.1% and 8.7%, respectively. This might be due to the fact that most public health facilities (hospitals and health centers) in the piloted area of the study are contracted by the CBHI scheme to provide services to scheme members. The CBHI operational guideline also dictates scheme members to seek service from public health centers for first line care, and to visit public hospitals with proper written referral papers. Thus, utilization of care from private providers is rarely permitted for scheme members unless a specific care or drug is unavailable at a public facility. According to the operational guide, members can only be referred from the public health center to the closest referral hospital and those who do not follow the referral system are charged 50% of the hospital user fee as a bypassing fee.22,23 Although the results do not indicate whether greater use of services at public hospital level represents a shift from the public health center level or a flux of new users to the public hospital level (because of the cross-sectional nature of the study), it is possible that insurance can encourage users to move from the health center level to the hospital level for their advanced health care. Such a shift can bring about cost savings to the government in the long term. Similarly, a study in Cambodia, found that visits to public health service providers were increased by 18% and by 11% from private providers by CBHI members.22

A critical look at the results of the multivariable regression using a binary logistic regression model revealed that members of CBHI are 2.87 times more likely to utilize outpatient health-care services compared to non-members during illness of the individual household members and this was statistically significant (AOR: 2.871; CI: 1.039–7.929). This was consistent with the study in rural Burkina Faso, that indicated a statistically significant association between membership of the CBHI scheme and the utilization of health services after adjusting for the covariates in which members are 2.23 times more likely to use health services compared to non-members.21

In our study, household monthly income is significantly associated with increased odds of utilizing modern health-care services following an illness. Households with monthly income category of 1200.00 Eth Birr and more were 5.38 times more likely to utilize outpatient health-care services relative to those households with a monthly income less than 800.00 Eth Birr (AOR: 5.376; 95% CI: 1.050–27.532). This means households from the lower- and middle-income group were actually less likely to utilize outpatient services than higher income groups. This was also consistent with findings in Burkina Faso and Rwanda, where the richest income groups had utilized health-care services more than the lower- and middle-income groups.21,23

The qualitative findings also revealed that for mild-to-moderate illnesses, both the CBHI scheme member and non-member households reported use of public health centers for mild-to-moderate illness of family members as first-line care provider. This was because of its geographical accessibility in terms of distance and relatively lower cost of health-care services. These findings are consistent with other studies that found that distance to facilities, transportation costs and poor quality of care create additional cost barriers that limit access to services even in the presence of insurance.15 But in case of severe illness; they usually prefer health-care services from hospitals in preference to the availability of qualified provider and quality health-care services.

Limitations of the Study

The main limitation of the current study was the cross-sectional nature of the survey, which leads to the possibility of selection bias due to un-observable variables. From an econometric perspective, as the household decision to join the CBHI program is likely to be determined by factors which the study cannot observe, but which could at the same time also affect the utilization of health-care services. Therefore, level of understanding of the CBHI program and thinking about the initial health status of the family members was expected to influence the effect of the scheme on utilization of health-care services. These different incentives do leave this study with an endogeneity problem and will render the estimation results subject to adverse selection and omitted variable bias.

Another limitation of this study was the use of 12 weeks recall period, in order to get adequate study population with health care need for the assessment of the effect of CBHI on utilization of health-care services and its associated cost of health care. Thus, it may induce recall bias of the study, especially in recalling the incurred health-care expenditures for utilization of outpatient services for the given illness in the household. Needless to say, the CBHI scheme in the current study is vulnerable to adverse selection. However, the enrolment was voluntary and takes place on the household level in order to limit adverse selection.

Conclusion

This study paves the way to enhance the understanding of the effect of the CBHI scheme on utilization of health-care services in Yirgalem town of Southern Ethiopia. In this context, the study certainly elucidated that the CBHI scheme had positive effects on utilization of outpatient health-care services during the time of illness. Utilization of outpatient health-care services for illness was significantly higher for CBHI scheme member households compared to non-member households. Furthermore, the scheme member households have utilized outpatient health-care services more from public providers than from private clinics. This was in line with the scheme design strategy. However, higher utilization of outpatient health services from hospitals (both public and private) by the scheme members and lower current enrollment status of the target households to the CBHI scheme has shed light on the findings of this study of the effect of the CBHI scheme on the expected health system goals. Our detailed analysis of qualitative data of the study provides information on lower enrollment of the target households to the CBHI scheme: such as high cost of the premium and the expected annual premium payment for renewal of membership; poor quality of health-care services in the scheme contracted public-health facilities (Including lack of basic drugs and unfair attitude of health workers); and difficult geographical accessibility of the contracted public-health facilities.

In order to maximize the population’s capacity to enjoy the benefits of the CBHI scheme and ensure sustainable health-care financing mechanisms, serious deliberation and policy action needs to address those factors contributing to lower CBHI scheme enrollment of the target population and the quality issues of health-care services at the scheme contracted public-health facilities.

Acknowledgments

We are grateful for the opportunity given us by the School of Environmental and Public Health, College of Medicine and Health Sciences at Hawassa University in the early stages of conceptualizing and carrying out this study. We would like to appreciate Abt Associate SNNPR RPO, and Yirgalem Town Administration Health Desk and CBHI process owner staff for their support in providing available information to conduct this research project. Special thanks to Dr Bekele Demissie’s wife Miss Mulubrehan Gebeyehu and his daughter Tsion Bekele for their priceless support and encouragement to pursue this study.

Disclosure

The authors report no conflicts of interest in this work.

References

1. WHO. Recommendations action: international conference on social insurance in developing countries. In: Extending Social Protection in Health: Developing Countries’ Experiences, Lessons Learnt and Recommendations. GTZ House,Berlin: ILO, GTZ and WHO; 2007:168–175.

2. Garg CC, Karan AK. Reducing out-of-pocket expenditures to reduce poverty: a disaggregated analysis at rural-urban and state level in India. Health Policy Plan. 2009;24:116–128. doi:10.1093/heapol/czn046

3. Wagstaff A. Doorslaer EV. Catastrophe and impoverishment in paying for health care: with applications to Vietnam 1993–1998. Health Econ. 2003;12(11):921–934. doi:10.1002/hec.776

4. Wang H, Switlick K, Ortiz C, Zurita B, Connor C. Health insurance handbook: how to make it work. In: World Bank Working Paper 219. Washington, The World Bank; 2012:1–10.

5. Jütting JP. Do community-based health insurance schemes improve poor people’s access to health care? Evidence from rural Senegal. World Dev. 2004;32(2):273–288. doi:10.1016/j.worlddev.2003.10.001

6. The Data Repository [Internet]. World Health Organization. 2012. Available from: http//www.who.int/gho/database/en/. Accessed Januaray 16, 2018.

7. FMOH. HSDP IV: Annual Performance Report 2014/15. Addis Ababa, Ethiopia: Federal Ministry of Health; 2015:44.

8. FOMH. Health and Health Related Indicators. Addis Ababa, Ethiopia: Federal Ministry of Health; 2015:47–51.

9. FMOH. Ethiopia’s Fifth National Health Accounts 2010/2011. Addis Ababa, Ethiopia: Ethiopia Federal Ministry of Health; 2014.

10. FMOH. Health Insurance Strategy. Addis Ababa, Ethiopia: Federal Ministry of Health Planning and Program Department; 2008.

11. FMOH. A Directive to Provide Legal Backing for Piloting and Promotion of CBHI. Addis Ababa, Ethiopia: Ethiopia Federal Ministry of Health; 2011.

12. Ouimet M-J, Fournier P, Diop I, Haddad S. Solidarity or financial sustainability: an analysis of the values of community-based health insurance subscribers and promoters in Senegal. Can J Public Health. 2007;98(4):341–346. doi:10.1007/BF03405415

13. Jacobs B, Bigdeli M, van Pelt M, Ir P, Salze C, Criel B. Bridging community-based health insurance and social protection for health care – a step in the direction of universal coverage? Trop Med Int Health. 2008;13(2):140–143. doi:10.1111/tmi.2008.13.issue-2

14. Alkenbrack SE. Health Insurance in Lao PDR: Examining Enrolment, Impacts, and the Prospects for Expansion [PhD thesis]. London School of Hygiene & Tropical Medicine; 2011. doi:10.17037/PUBS.01544173

15. Giedio U, Alfonso EA, Día Y. The impact of universal coverage schemes in the developing world: a review of the existing evidence. World Bank; Washington DC: 2013; 51–72.

16. Preker AS, Carrin G, Dror D, Jakab M, Hsiao W, Arhin-Tenkorang D. Effectiveness of community health financing in meeting the cost of illness. Bull World Health Organ. 2002;80(2):143–150.

17. Ekman B. Community-based health insurance in low-income countries: a systematic review of the evidence. Health Policy Plan. 2004;19(5):249–270. doi:10.1093/heapol/czh031

18. Mebratie AD, Sparrow R, Alemu G, Bedi AS. Community-based health insurance schemes: a systematic review. In: ISS Working Paper Series. Report No 568. 2013:1–47.

19. Aggarwa A. Impact evaluation of India’s ‘Yeshasvin’ community based health insurance programme. Health Econ. 2010;19:5–35. doi:10.1002/hec.1605

20. Gnawalia DP, Pokhrel S, Sié A, et al. The effect of community-based health insurance on the utilization of modern health care services: evidence from Burkina Faso. Health Policy. 2009;90:214–222. doi:10.1016/j.healthpol.2008.09.015

21. Hounton S, Byass P, Kouyate B. Assessing effectiveness of a community based health insurance in rural Burkina Faso. BMC Health Serv Res. 2012;12:363. doi:10.1186/1472-6963-12-363

22. Levine D, Polimeni R, Ramage I. Insuring health or insuring wealth? An experimental evaluation of health insurance in rural Cambodia. Am Econ J. 2012;20(20):1–15.

23. Shimele A. Community based health insurance schemes in Africa: the case of Rwanda. In: Working Papers Series No 120. African Development Bank, Tunis, Tunisia; 2010.

24. Atnafu DD, Tilahun H, Alemu YM. Community-based health insurance and healthcare service utilisation, North-West, Ethiopia: a comparative, cross-sectional study. BMJ Open. 2018;8:e019613. doi:10.1136/bmjopen-2017-019613

25. Mebratie A, Sparrow R, Yilma Z, Abebaw D, Alemu G, Bedi A. The impact of Ethiopia’s pilot community based health insurance scheme on healthcare utilization and cost of care. Social Science & Medicine. 2019;220:112–119.

26. FMOH. Evaluation of Community-Based Health Insurance Pilot Schemes in Ethiopia. Final Report. Addis Ababa, Ethiopia: Ethiopian Health Insurance Agency; 2015.

27. FDRE. Summary and Statistical Report of the 2007 Population and Housing Census. Addis Ababa, Ethiopia: Population Census Commission, Federal Democratic Republic of Ethiopia; 2008.

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2020 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.