")

Back to Journals » ClinicoEconomics and Outcomes Research » Volume 13

Barriers and Facilitators of Community-Based Health Insurance Policy Renewal in Low- and Middle-Income Countries: A Systematic Review

Received 23 February 2021

Accepted for publication 27 March 2021

Published 11 May 2021 Volume 2021:13 Pages 359—375

DOI https://doi.org/10.2147/CEOR.S306855

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 2

Editor who approved publication: Professor Giorgio Colombo

Mohammed Hussien,1 Muluken Azage2

1Department of Health Systems Management and Health Economics, School of Public Health, College of Medicine and Health Sciences, Bahir Dar University, Bahir Dar, Ethiopia; 2Department of Environmental Health, School of Public Health, College of Medicine and Health Sciences, Bahir Dar University, Bahir Dar, Ethiopia

Correspondence: Mohammed Hussien

Department of Health Systems Management and Health Economics, School of Public Health, College of Medicine and Health Sciences, Bahir Dar University, P.O. Box: 79, Bahir Dar, 6000, Ethiopia

Tel +251 588209834

Email [email protected]

Purpose: A growing number of low- and middle-income countries are implementing small-scale community-based health insurance schemes to tackle the burdens posed by direct out-of-pocket payments. Apart from a few successful experiences, such schemes suffer from the problem of persistent low membership which could be attributed to either initial low enrollment or low renewal rate. However, there is a lack of comprehensive information on the factors that influence subscribers’ policy renewal decisions. Hence, we systematically synthesize information to answer the review question ”what are the barriers and facilitators of community-based health insurance policy renewal in low and middle-income countries?”.

Methods: We searched PubMed, Scopus, and Hinari electronic databases in line with the PRISMA guidelines. Our search was limited to studies published from January 2005 to February 2020 in the English language. Additional studies and grey literature were searched using Google Scholar. We included quantitative, qualitative, and mixed-method studies in the review. We assessed the methodological quality of the studies using standardized appraisal tools. The findings were synthesized inductively using a thematic analysis approach.

Results: Our searches retrieved 2386 records among which 27 were included in the review. The thematic synthesis identified six major themes that influence the decision to renew scheme policy: socio-demographic factors; scheme-related awareness and understanding; participation in scheme and other voluntary groupings, need and benefit factors; health-care quality; and scheme operation and policy.

Conclusion: Lower socioeconomic status, poor quality of health care, lack of benefit from the scheme, lack of trust in scheme management, and dissatisfaction with scheme services are important barriers for community-based health insurance policy renewal. Better education, understanding the principles of the scheme, active participation in the scheme, and long-term illness experience of member households facilitate renewal decisions. These are important areas of intervention for governments and other relevant stakeholders to retain members and maintain the sustainability of the schemes.

Registration: The review protocol was registered in PROSPERO international prospective register of systematic reviews (ID = CRD42020168971).

Keywords: universal health coverage, community-based health insurance, barriers and facilitators, renewal, low- and middle-income countries

Introduction

The health financing systems in low- and middle-income countries (LMICs) largely rely on out-of-pocket payments, and reliance on out-of-pocket health spending will continue in some countries into the future.1,2 The obligation to pay directly for services at the moment of need hinders the successful implementation of Universal Health Coverage (UHC) targeted efforts. Direct out-of-pocket payment at the time of care is a significant barrier to health-care utilization.3,4 Estimates showed that the majority of the worlds’ 1.3 billion poor have no access to health-care services because they cannot afford to pay at the point of service delivery.4 An over-reliance on out-of-pocket payments in health financing is also an indicator of increased risk of catastrophic financial expenditure and impoverishment from getting health care. Globally, over 808 million people incurred financial catastrophe at the 10% threshold, and 97 million people were pushed into poverty because of direct payments for health services in 2010.5,6

Member countries of the World Health Organization agreed to reform their financing systems to move more quickly towards UHC and to sustain those achievements. Universal health coverage requires that all people in a country have adequate access to the health care they need without suffering financial hardships irrespective of their living standards.4 As coverage expands, the issue of financial sustainability becomes a critical health system challenge in most LMICs.7–9

Moving to UHC requires a strong health system with sustainable financing systems.10 A health financing system that provides sufficient and stable prepaid pooled resources for priority health services is a key to achieve UHC.3 There is a growing global commitment to UHC in the last few years. Many LMICs are implementing UHC inspired health system reforms to increase access to health services and protect their citizens from financial risk.11 In LMICs, current strategies to reach universal coverage combine a variety of revenue sources and a variety of protection systems to cover all population groups, in which Community-Based Health Insurance (CBHI) has a prominent place.7 A growing number of LMICs are implementing small-scale voluntary CBHI schemes as a risk-pooling mechanism for rural communities and informal sector workers to address the access barriers posed by direct out-of-pocket payments.1,7

Apart from a few successful experiences, CBHI schemes suffer from the problem of persistent low membership.7,12 The persistent low membership could be attributed to either initial low enrollment or high dropout rate after joining the scheme.13,14 This shows the need to recognize the barriers and facilitators to the success of CBHI schemes, particularly of the membership growth rate of the schemes.

The focus areas of the existing systematic reviews on CBHI schemes include enrollment and effect of the schemes on healthcare-seeking behavior,15 uptake of or willingness to pay for CBHI schemes,16 factors affecting uptake (enrolment) and renewal of membership in CBHI schemes,17 barriers and facilitators to implementation, uptake and sustainability (renewal) of CBHI schemes,18 all targeting the situation in LMICs except the first one which was limited to the South Asia region. The systematic review and meta-analysis conducted by Dror et al17 primarily focused on factors affecting uptake of CBHI and the studies included in the review were those published from 1990 to 2013. Only two of the studies included in this systematic review were also part of our synthesis. A recent systematic review conducted on CBHI schemes is the one conducted by Fadlallah et al18 which included the studies published from 1992 to 2015. Even though this review tried to synthesize the barriers and facilitators of policy renewal decision (which was operationalized as scheme sustainability), our review could be unique because of the following reasons. First, we have included 27 studies published since 2005, among which 17 have been published after 2015. Only four studies included in the systematic review by Fadlallah et al were also included in our review. Second, our systematic review synthesized a detailed account of the factors influencing policy renewal decisions in LMICs which was not considered in the previously published systematic reviews. Hence, the purpose of this systematic review was to answer the review question” what are the barriers and facilitators of community-based health insurance policy renewal in low and middle-income countries?” This could enrich the pool of information on the area which helps policymakers and relevant stakeholders to retain members and maintain the sustainability of CBHI schemes.

Materials and Methods

Protocol and Registration

The review protocol was registered in PROSPERO international prospective register of systematic reviews (ID = CRD42020168971).

Search Strategy

Search strategies for electronic databases were developed in line with the PRISMA guidelines19 for systematic reviews (Table S1). A search was conducted by the first author (MH) from 02 December 2019–09 Feb 2020, using PubMed, Scopus, and Hinari electronic databases. The terms used in the search strategies were based on three main concepts: “community health insurance”, “renewal or dropout”, and “low- and middle-income countries”. The free text terms used to search the databases are shown under the Supplementary Materials. The reference lists of relevant systematic reviews and the studies included in the review were checked for additional papers. Additional studies and grey literature were also searched manually using Google Scholar. The search was limited to studies published or conducted from 2005 onwards in the English language. We chose this point in time because in this year all member states of the World Health Organization made commitments to achieve the goal of UHC and reform their health-care financing mechanisms through prepaid, voluntary community-based health insurances.4 As a result, many LMICs started to modify the existing community health insurance models and start to implement new ones in line with the World Health Resolution for universal health coverage.7

Eligibility Criteria (Inclusion and Exclusion)

The inclusion criteria were determined by using the “PICOC” concept. Participants who have ever enrolled in a CBHI voluntarily whether they decided to leave the scheme or not; voluntary, mutual, community-based and micro-health insurance Interventions; Comparisons between individuals who renewed/dropped out or decided to renew/drop out of the scheme; Outcomes which related to barriers and facilitators of CBHI policy renewal decision; and Context where the studies are conducted in LMICs (as defined by the World Bank). Among quantitative studies included were descriptive and cross-sectional studies that dealt with factors affecting renewal/dropout. The qualitative studies included case studies, observations, in-depth interviews, key informant interviews, and focus groups with participants who renewed or dropped out, scheme managers/policymakers, health-care providers and managers, and relevant stakeholders. Studies dealing with other health insurance mechanisms (private or social health insurance); and that dealing with enrollment status and effectiveness of CBHI schemes with no specification of renewal or dropout were excluded.

Study Selection

The first author (MH) screened the identified studies to determine whether they satisfied the inclusion criteria. The selection process consisted of three stages: duplicates screening, title, and abstract screening, and full-text screening. In the first stage, duplicates were screened and removed. In the next stage, the titles and abstracts of the remaining studies were screened for relevance to the topic and potential eligibility. Third, by reading the full text in detail, the studies were assessed for final inclusion in the review based on the inclusion and exclusion criteria. Thorough discussions were made on the results of the selection process with the second author (MA) and studies were selected through mutual consensus.

Data Extraction

Data were extracted by the first author (MH) using a data extraction sheet tailored to this systematic review. The extracted data included the first author and year, study setting, objective, study design, study population characteristics, sample size, sampling technique, data collection, analysis model, and findings. The second author (MA) critically read the output of data extraction by comparing with the included studies, and then we continued to the next step after resolving the differences through detailed discussions.

Quality Assessment

The first author (MH) assessed the methodological quality of the studies and discussions were made with the second author (MA) until an agreement was reached on the judgments made. We used the critical appraisal tool for use in systematic reviews of prevalence studies developed and tested by Munn et al (2014) to assess the methodological quality of cross-sectional studies, including the quantitative part of mixed method-studies.20 The tool comprises 10 items related to the internal and external validity of the study and aims at targeting all kinds of prevalence studies. Its applicability and user-friendliness have been pilot tested by an experienced group of health-care researchers. The results of the pilot indicated that this tool was a valid approach to assessing the methodological quality of studies reporting prevalence data to be included in systematic reviews. Besides, the authors provide an appendix with detailed descriptions and explanations which is easier to apply. To assess the methodological quality of qualitative and mixed-methods studies, we used the Mixed Methods Appraisal Tool (MMAT) Version 2018, which is designed for the appraisal of mixed studies reviews.21 It permits to appraise the methodological quality of the qualitative and quantitative components separately with a specific criterion for each and the overall quality of a mixed-methods study.

To judge the overall methodological quality, the percentage score for each study was divided into three categories with 0−33% lower, 34–66% moderate, and 67–100% high quality as suggested by Davids EL and Roman NV 2014.22 This was calculated by dividing the total score by the total number of items and multiplied by 100. In this review, we did not exclude any study based on the results of the quality assessment believing that every study might enrich our understanding of the different factors influencing policy renewal.

Data Synthesis

We synthesized the findings narratively using a thematic synthesis.23 We read the result section of the studies line by line to generate an initial list of codes inductively with no pre-existing themes in mind. Codes with similar concepts have been organized into subthemes and themes. The open code software was used for the analysis to assist and to facilitate the coding process, and further categorization of concepts into themes.

Results

Study Selection

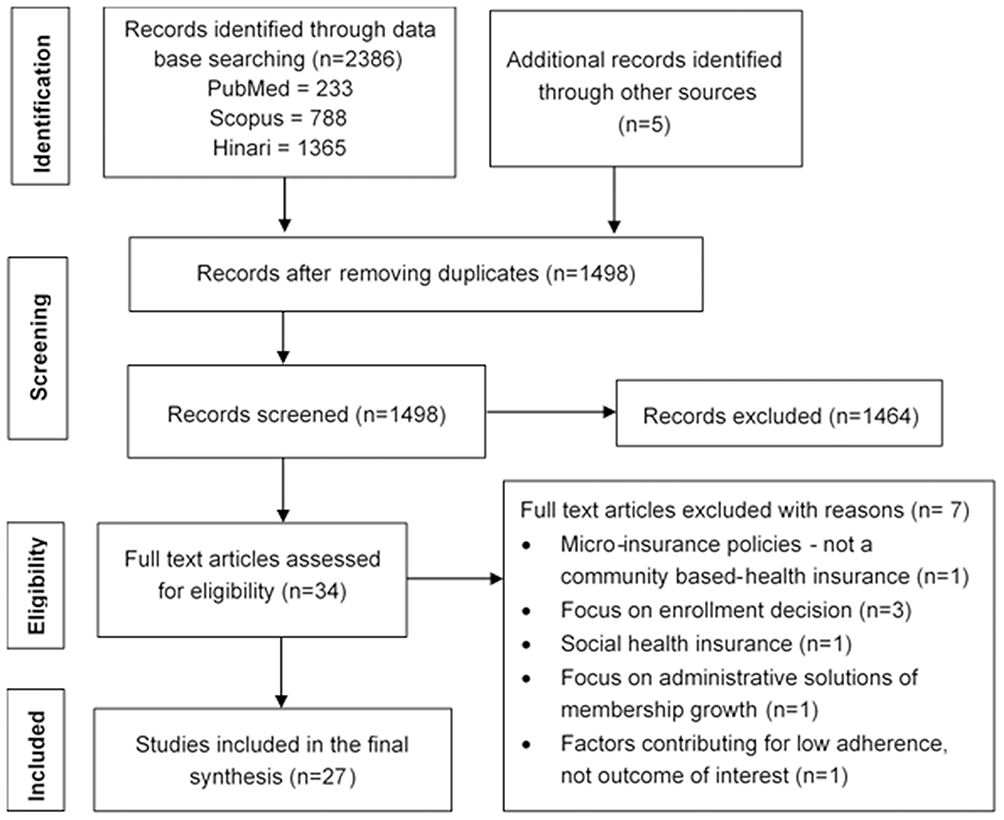

The search process and results are outlined using the PRISMA flow diagram19 as shown in Figure 1. The searches retrieved 2386 records through a comprehensive search of PubMed (n = 233), Scopus (n = 788), and Hinari (n = 1365) electronic databases and 5 from other sources. A total of 2391 records was identified of which 893 were duplicates. After removing the duplicates, 1,464 articles were excluded by reviewing the titles and abstracts of each study for relevance to the topic and potential eligibility. The remaining 34 full texts were reviewed for eligibility. Among the potentially eligible publications, 7 were excluded with reasons, while 27 studies were eligible for this review (one study included two different studies on scheme renewal in India). Under the Supplementary Materials, a list of the excluded studies with reasons for exclusion is included.

|

Figure 1 The PRISMA flowchart diagram of study selection. Note: PRISMA figure adapted from Liberati A, Altman D, Tetzlaff J, et al. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: explanation and elaboration. Journal of clinical epidemiology. 2009;62(10). Creative Commons.19 |

Characteristics of Included Studies

The review included 27 papers: 19 quantitative,24–42 two mixed-method,43,44 and six qualitative types of research.45–50 The studies were conducted in 12 countries (seven LMICs) across two continents (Asia and Africa) among which the largest number of papers was conducted in Sub-Saharan Africa countries. This includes nine studies conducted in Ghana, two in Ethiopia, two in Uganda, and one in each of the following countries: Benin, Burkina Faso, Senegal, Sudan, and Tanzania. Nine studies have been conducted in four Asian countries: one study in Bangladesh, one in Cambodia, one in Indonesia, and six in India. Concerning the period covered by the studies, five studies have been published from 2007 to 2009, four studies from 2012 to 2014, and 18 studies were published from 2015 to 2019.

The 21 studies were conducted on renewal/dropout using quantitative data, among which 20 have employed cross-sectional study design and one study was based on panel data. Concerning the study outcome measured by the studies, 13 studies measured determinants of renewals/dropouts without specification of membership duration,24–27,31,33,35–38,40–42 four studies identified factors related to renewal/dropout after a one-year experience of membership,28–30,43 one study measured factors affecting the consistency of monthly premium payment,32 one study modeled the decision to renew membership in the form of the number of years households are insured,34 while another study is based on willingness to renew membership in the next renewal period.44 Eighteen studies measured factors affecting renewal using multivariable logistic regression and one study applied a zero-inflated negative binomial model. One study compares factors between renewed and dropped using an independent t-test, and one study used descriptive statistics with no statistical tests. Three studies used secondary data obtained from the membership records of the schemes and the rest 18 studies were based on data obtained from household surveys with sample sizes ranging from 145 to 3685 respondents.

Out of the eight studies conducted using qualitative data – including the two mixed-method research – four used both focus groups and in-depth interviews, one used both interviews and prolonged observation and three each used either focus groups or interviews. The study participants include those newly insured, uninsured, renewed, and dropped out; and scheme managers, promoters, health-care providers, health-care managers. An overview of the characteristics and summary findings of the included studies is included as Supplementary Materials.

Quality Appraisal

The mean score of the quality assessment was 8.22 out of 10 for the quantitative cross-sectional studies which range from 3 to 10 and 14 out of 20 for the mixed methods studies. Out of the 18 quantitative studies, 14 were rated as high quality, three moderate quality and only one was rated as low quality. We judged the qualitative studies to have met most of the MMAT tool checklist for methodological quality and all are rated as high quality. The full results of the quality appraisal are described under Supplementary Materials.

Barriers and Facilitators of CBHI Policy Renewal

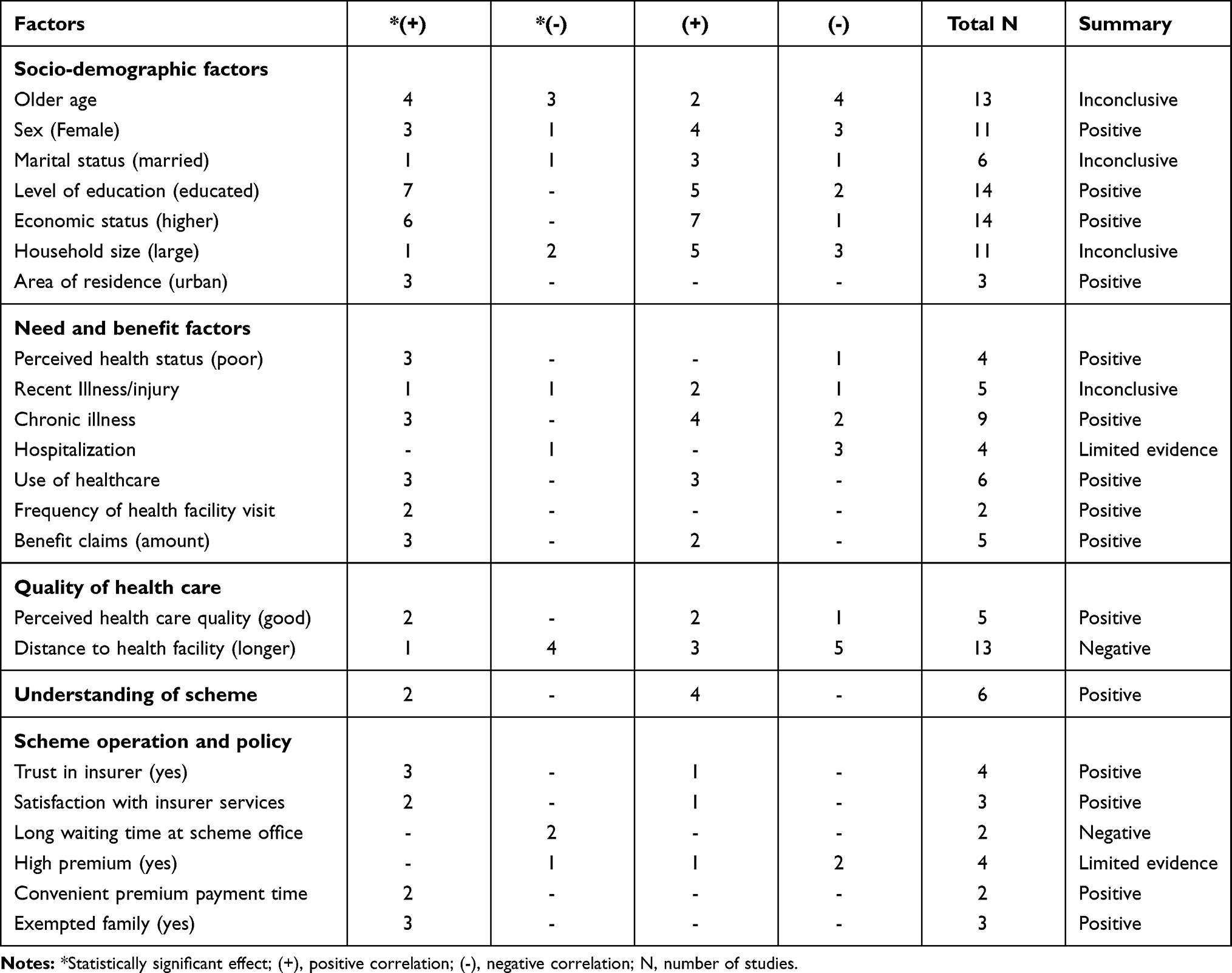

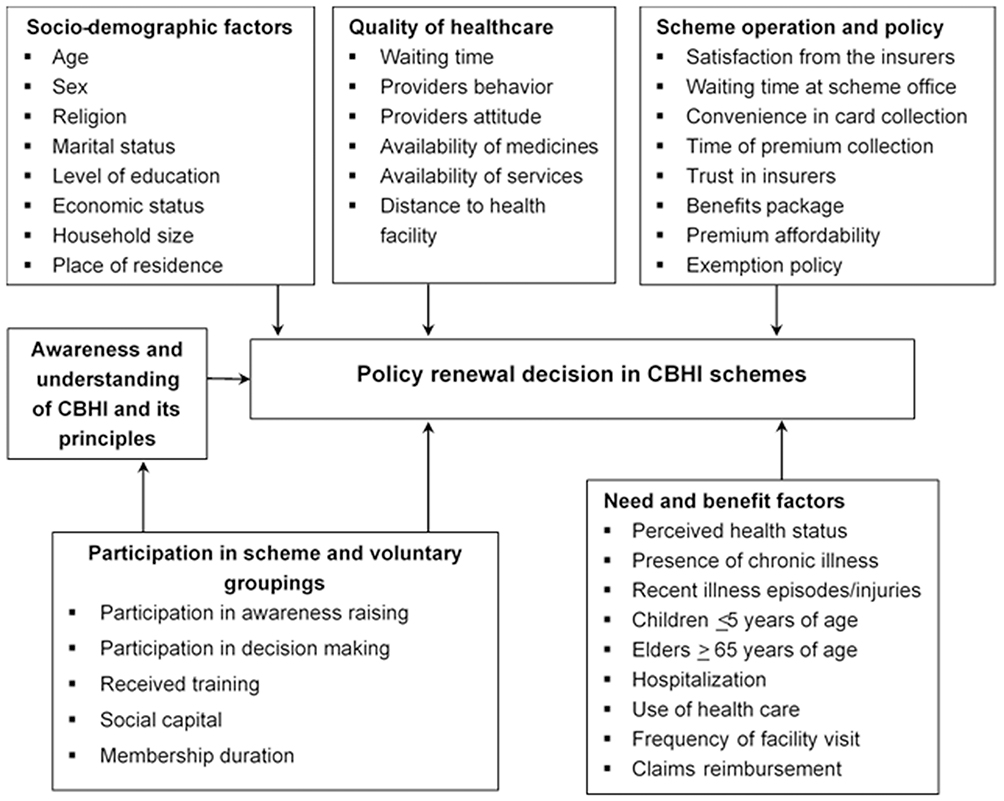

The thematic synthesis identified six major themes that influence the decision to renew scheme policy either positively or negatively: socio-demographic factors; scheme related awareness and understanding; participation in scheme and other voluntary groupings, need and benefit factors; quality of health care; and factors related to scheme operation and policy as displayed in Figure 2. Table 1 collates summary of the factors that facilitate or hinder the decision to renew CBHI membership based on the findings of the quantitative studies.

|

Table 1 Summary of the Factors That Influence Policy Renewal of CBHI Schemes Based on Quantitative Studies |

|

Figure 2 A conceptual framework of barriers and facilitators critical to CBHI policy renewal. |

Theme 1: Socio-Demographic Factors

Age, gender, marital status, religion, place of residence, economic status, level of education, and household size were reported as important socio-demographic factors influencing the renewal decision of CBHI scheme members. The age of the household head or the respondent influences policy renewal decisions with a mixed effect. Six studies reported that age was positively correlated with renewal decisions. Older individuals were more likely to renew their membership as compared to the younger individuals,30,32,34,36,42,43 among which four studies revealed a statistically significant association with renewal decision.32,34,36,42 On the contrary, seven studies reported that younger individuals/household heads were more likely to renew membership compared with older ones,25,26,29,38,40,41,44 among which three studies showed a statistically significant association.26,38,40 Eight studies treated age as a continuous variable (in years) while others use age as dummy variables with a different basis of categorization.

Concerning gender, seven studies showed that female-headed households were more likely to renew their policy compared to male-headed households,28,30,35,38,40,41,44 while four studies reported a positive association between male-headed households and policy renewal.29,33,37,43 Among the 11 studies which reported the association between policy renewal and gender, four studies showed a statistically significant association.35,37,38,44

Four studies found that married household heads were more likely to renew their policy compared with their counterparts of single individuals25,30,35,42 with only one study showing a statistically significant association.42 On the contrary, two studies reported that unmarried household heads were more likely to renew their policy compared to married and widowed individuals.29,36

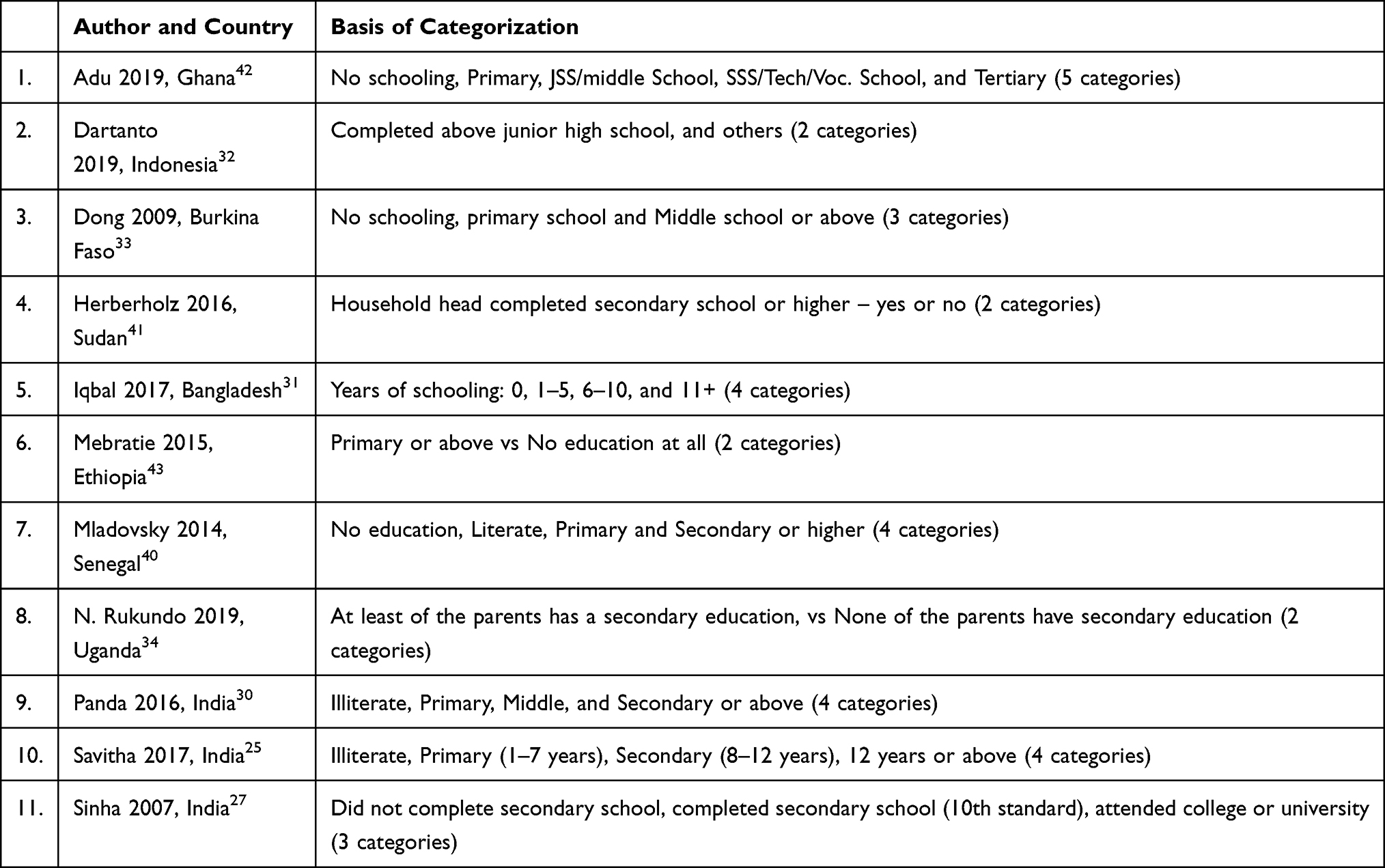

Level of education also plays an important role in influencing the members’ renewal decision as 12 of the 14 studies showed a positive association between higher levels of education and renewal decision26–33,36,40,41,43 among which seven studies revealed a statistically significant correlation.26,27,29,31,33,36,41 Contrary to this, those who attain higher education were less likely to renew membership as noted by two studies,25,34 but it is not statistically significant in both reports. The level of education was also used inconsistently in the included studies. Two studies used the level of education in years as a continuous variable,26,36 while eleven studies used it as a dummy variable with a different basis of classification as shown in Table 2.

|

Table 2 Heterogeneity Across Studies in Using Education as an Independent Variable During Analysis |

Economic status is another key factor that influences an individual’s policy renewal decision. The studies used different measurement indicators: Some refer to income as the indicator of economic status; some consider expenditure level; and others construct economic categories based on household assets as quintile, quartile, or tertile. Thirteen studies found that higher economic status was associated with renewal and six of which reported a statistically significant effect.25,26,28–31,34,36,37,40,41,43,44 Only one study found a different finding. The higher household economic status (a higher household expenditure proxy) was positively correlated with dropping out of community-based health insurance, with a statistically non-significant effect.33 One study in Indonesia identified income stability and experiencing financial hardship as significant factors that influence the sustainability of premium payment. Households with more income stability tend to have an 11-percentage point higher probability of paying the premium regularly than households who have unstable income while experiencing financial hardship has a negative influence as they prioritize expenditures essential for daily life over paying insurance premiums.32

Place of residence (rural or urban) also affected renewal. Three studies revealed that individuals living in urban or semi-urban areas were more likely to renew their policy compared with rural dwellers and the association was statistically significant.25,33,38 Three studies found that religion was associated with renewal decisions with mixed findings: Christians in Ghana,35 Muslims in Burkina Faso,33 and Catholics in Uganda34 were more likely to renew their insurance policy with a statistically significant effect of the latter two studies.

Six studies found that larger households were more likely to renew scheme policy,25,28,29,34,43,44 while five studies found that individuals with a larger family were more likely to drop out of the scheme30,33,36,40 or reluctant to pay the premium regularly.32

Theme 2: Scheme Related Awareness and Understanding

This theme includes whether the individual is exposed to any insurance awareness campaigns; the respondent understands the concept of premiums, risk pooling principles, and insurance in general; and whether the respondent understands the benefits of the schemes. Understanding of scheme positively influences the household’s decision to renew their policy, even though different measurement indexes are used in the studies. Six studies revealed that respondents who have a good understanding of the scheme were more likely to renew their policy and pay the premium regularly compared with those having inadequate knowledge28,29,32,41,43,44 while only one study identified good understanding as a barrier for renewal with statistically non-significant effect.30 A study in Senegal found that members were more likely to report that solidarity is an advantage of CBHI membership compared to ex-members indicating their understanding of the scheme benefit.40

The qualitative studies found that members dropped out of the schemes because of the low awareness about the benefit of the insurance plans43,48 and the lack of awareness of the risk-sharing principle.46,50 These studies pointed out that people who did not fall sick and utilized health care dropped out of the scheme because of the lack of awareness and poor understanding of the risk-sharing principle. One study in Ethiopia identified that members of a productive safety net program were more likely to renew scheme membership, pointing out that households covered by this program were provided ongoing information on the CBHI scheme by government officials as part of integrating different development interventions.43

Households who knew the correct premiums levied were more likely to renew CHBI membership.34 In this study, knowing premiums was considered as a proxy of knowledge about CBHI processes, benefits, requirements, and expectations. Households having a neighbor who is a CBHI member and those with more access to information – had a television, or listened to radio daily, or read a newspaper – had a higher likelihood of renewing membership.34 Respondents from renewed groups were also more likely to know half or nearly all the other members of the scheme than the dropouts.40

A study in India reported that respondents who know a scheme mobilizer who is a relative or a neighbor were more likely to renew membership,27 while another study in Senegal showed that members were more likely than ex-members to know the scheme President, Secretary, Manager and/or another staff member; and to have heard of the scheme from a family member or friend compared to another source40 indicating the social influence of relatives, friends, and leaders on renewal as well as the importance of creating a trusted source of information. One qualitative study in Ghana points out that peer influence had a positive effect on membership renewal as some respondents mentioned that they were influenced by peers to renew their membership.45

Theme 3: Participation in Scheme and Other Voluntary Groupings

This theme includes participation in awareness-raising and/or information dissemination, scheme membership duration, attending meetings related to CBHI, participation in scheme decision-making activities, and other voluntary groupings. A study in Senegal found that the rate of active participation in the scheme was a facilitator for policy renewal. Respondents from the renewed group were more likely to have had informal discussions about the scheme; participated in awareness-raising and/or information dissemination; voted in scheme elections; attended a general assembly; and received training compared with ex-members. Members were also being more likely than ex-members to be informed of mechanisms of controlling scheme abuse or fraud and think they could influence scheme operation.40

In Ethiopia, individuals holding an official position, including village officials, heads of traditional organizations, religious leaders, and other people of influence were less likely to drop out of the scheme. These segments of the population were provided detailed training on the design features of the pilot CBHI and were engaged in awareness-raising activities.43

Participation in other voluntary groupings, which is a measure of social capital, was reported as an enabling factor for membership renewal by two studies. Belonging to an additional voluntary group and belonging to a large burial group were associated with an increased likelihood of renewing membership.34 Member households were more likely to belong to more community associations than ex-members.40 On the contrary, membership in other insurance and social protection schemes (not limited to health insurance), significantly reduces the probability of paying premiums regularly.32 One study in India found that respondents from the renewed group had more years of experience as a scheme member compared to the dropout groups and the effect is statistically significant.27

Theme 4: Need and Benefit Factors

This theme mainly points out the possible existence of adverse selection33,38,40 and includes the perceived health status of households, presence of chronic illness, recent illness episodes or injuries, and presence of children under 5 years of age or elders above 65 years of age in the household. It also includes benefit factors like the use of health care (outpatient or hospitalization), frequency of health facility visits, claims experience, and perceived benefits of the schemes.

Four studies assessed the effect of the perceived health status of the household on renewal decisions.35,36,43,44 Respondents who rated the health of the household as poor and/or medium were more likely to renew their policy compared with those who rated their health status as good with a statistically significant effect.35,36,44 As explored by a qualitative study, people who perceived themselves as healthy dropped out of the scheme.47 However, one study found a different result with those households rating their health status as good were less likely to drop out of the scheme, but the effect is not statistically significant.43

Eight studies reported that the presence of chronic illness in the household was an important factor that influences policy renewal decisions. Six studies reported a positive correlation between the existence of chronic illness or disability and renewal decisions among which three studies showed a statistically significant effect.25,28,30,40,41,43 Contrary to these, two studies identified the existence of chronic illness is negatively correlated with renewal, given they are not statistically significant.29,44

Three studies found that households with more episodes of illness in the past 15 days to 3 months had a higher probability of policy renewal,30,33,40 while two studies reported a negative correlation between the presence of recent illness episodes and renewal.29,43

Households having members with more health needs, measured by the presence of children and elderly people, were reported by two studies as a factor affecting renewal. Households having elderly people above 65 years old were more likely to renew membership.33,44 The presence of under-five children in the household was significantly associated with renewal in Burkina Faso,33 while it was negatively correlated in Ethiopia.44

Five studies found that the use of health care under the scheme positively influences an individual’s decision to renew their insurance policy with three studies showing a statistically significant effect.26,33,38,41,43 Households that never utilized insurance benefit services also tend to pay the premium irregularly.32 In addition to utilization, frequency of use was also reported by two studies as an influencing factor with individuals who visited health facilities more frequently were more likely to renew their membership.31,38 A qualitative study in Ghana found access to health care and financial relief from catastrophic payments as enablers of policy renewal.47

Hospitalization, which is an illness and utilization indicator, was inversely associated with contract renewal as reported by four studies,27–30 with having been hospitalized in the past one year as a scheme member leads to a reduction in the probability of renewal. One study showed a statistically significant effect.

Four studies found that benefit claims experience was associated with policy renewal. Three of these studies measured the effect of benefit claims on renewal decisions and found that households who received more benefit claims were less likely to leave the schemes.29–31 Other studies showed that households who submitted benefit claims in the last year were more likely to renew membership as compared to those who did not submit.26,27

Respondents made decisions on renewing their insurance based on the perceived benefits of the scheme. Respondents who disagreed with the assertion that joining the scheme stands to benefit them were less likely to renew their insurance, and those who believe that joining the scheme will help them to save money from paying hospital bills were also more likely to renew membership.35 Households who renewed their insurance policy were more likely to report that health-care access is an advantage of membership.40

Those who did not fall sick and did not utilise health services feel that there are no benefits in paying for membership. People preferred not to renew their policy because they had not fallen sick often39,44–47,50 and they did not benefit from the scheme through service utilization.39,42,45,47,50 For example, one respondent in Ghana said that “It is painful when you don’t use the insurance card but have to renew it every year”.46 In Uganda, discussants said that “It hurts when one does not fall sick and utilize his contributions; for there are no benefits”.50

Theme 5: Quality of Health Care

Factors related to this theme include individuals’ perceived quality of health care in terms of waiting time, providers’ behavior, providers’ attitude towards insured clients; availability of medicines, diagnostics, and services; and distance to the nearest contracted health facilities. Twenty-one studies reported on the different dimensions of quality to measure and explore their effect on renewal decisions,25,26,29–36,39–41,43–50 given that they used different quality measurement indicators. Five quantitative studies assessed the effect of the perceived quality of the services provided by the contracted health facilities on renewal or dropout decision among which four found that good quality of health care is a facilitator of policy renewal,33,40,41,43,44 and one study showed a negative correlation.26 Two qualitative studies showed that members dropped out of the scheme because of issues related to poor-quality health care.39,47

Subscribers who obtained diagnosis services before medicine prescription,36,43 supplied with the required medicines when accessing health care, and provided with surgery services free of charge when necessary were more likely to renew their membership.36 Six studies reported that members dropped-out of the schemes or not willing to renew membership due to the lack of prescribed medicines in the contracted health facilities which forced them to pay extra payment outside,42,44,46,47,49,50 while two studies showed that members dropped-out of the scheme due to their perception of poor quality medicines.33,42 One study in Ghana documented that illegal payment for medicines inside the contracted health facilities was a reason for dropping out of the scheme.47

The behavior of health care providers and their attitude toward insured clients also plays an important role in renewal decisions. The misbehavior of health professionals33,44,48,50 and the differential treatment of the insured patients in favor of the uninsured44–47,50 were the motives for dropping out of the scheme. For example, health care workers were rude to insured patients and sometimes withholding medication,48 and they provided quick service for non-members.46 Two studies reported that members renewed membership because some health providers’ showed positive behavior towards them,45,47 Doctors and Nurses took enough time for them, and they obtained a quick response.45 Respondents who perceived that health workers favor insured patients were less likely to drop out of the scheme.43

A study in Ethiopia found that trust in a public health facility; a composite score computed from five interrelated items using factor analysis was strongly associated with renewal. An increase in the score of household heads’ trust in health-care facilities increases the willingness to renew membership. The items include trust in professional competency, health professional equal treatment of insured and uninsured clients, the availability of sufficient professionals, availability of sufficient medicines, and health facility trustworthiness.44 Other quality dimensions reported as barriers for renewal include the cleanliness of the hospital, long queues,50 lack of diagnostic equipment, and long waiting hours.49

Distance to the nearest contracted health facility was reported as either a barrier or facilitator of policy renewal by 13 studies.25,26,29–34,40–44 Nine studies found that increased distance to the nearest health facility was associated with a decrease in the likelihood of policy renewal25,29–32,34,40,42,44 of which four studies showed a statistically significant effect.31,34,40,42 In support of this, one qualitative study in Ghana reported that transportation costs to the health facilities is a major deterrent to access health care even if one had a valid insurance card.46 The availability of professional health services in the village in which members live increases the probability of routine premium payments significantly.32 On the contrary, four studies showed that people located far from the health facilities were more likely to renew their membership,26,33,41,43 with only one study showing a significant effect.41

Different measurement indicators have been used by the studies to measure the distance to the nearest health facility which provides health care for scheme members. Travel time in minutes as a continuous variable;30,42–44 distance in km as a continuous variable;32,34 distance in km as a dummy variable – within or more than 5 km,41 within or more than 3 km,31 within or more than 2 km;40 other binary classification – nearby or not26 shorter distance or not;33 and the views of respondents on distance with a 5-point Likert scale25 have been used by the respective studies to measure distance.

Theme 6: Scheme Operation and Policy

Factors included under this theme include satisfaction level from the insurers; waiting time at the scheme office; visit by agents during the renewal period; convenience in card and premium collection; trust in insurers; perception on benefits package and premium affordability; and exemption policy.

Three studies reported that members who are satisfied with the scheme services were more likely to renew their policy out of which two studies showing a significant effect.26,40,43 Respondents who agreed that the collection of scheme cards was convenient were more likely to renew their health insurance35 and convenience in time of premium collection was positively correlated with willingness to renew.25,44 One study indicated that households visited by agents at the time of policy renewal were more likely to renew their membership.26 Longer waiting time at the scheme office was reported by two studies as a barrier for renewal decision, indicating that members who spend more time waiting at the scheme office were less likely to renew their policy.36,42 The qualitative studies showed that members dropped out of the scheme due to a delay in getting membership cards46,47 and no one had visited them at the time of renewal.27

Members’ trust in the management of the scheme was reported by four studies as a key enabler of policy renewal.24,26,40,44 Respondents who trusted the scheme were more likely to renew membership with three of the four studies showing a statistically significant correlation.

Premium affordability also played a key role in one’s decision to renew the scheme policy. Four studies reported that respondents who view the insurance premium as high were less likely to renew their membership,26,35,40,42 while one study found that respondents who view premium price as high were more willing to renew membership.44 Six studies reported that members could not renew membership because they could not afford the renewal payment,33,39,42–44,47 but it is an important barrier for the core poor.47 One study pointed out that it is not a major deterrent of renewal.45

The exemption policy of schemes had a significant role in the retention of its members. Three studies conducted in Ghana found that members having exempted family members within the household like children below the age of 18 years, the elderly aged 70 years or older, pregnant women, indigent (core poor), were more likely to renew their membership and the effect is statistically significant.37,38,42

Members’ perception of the benefits package influences their policy renewal decision. One study in India identified that members who perceived insurance plan is providing good coverage of illnesses were more likely to renew their policy. Perception towards coverage of health services was also found to be significant in renewal decisions.26

Six studies based on qualitative data reported that respondents decided not to renew their policy because the benefits package is too limited,44,45,47–50 and raised the following specific issues: the exclusion of some health risks,45,48,50 the limited number of medicines under the scheme,45,47 exclusion of referral service49 and the exclusion of valued health services from the benefits package.48

Respondents of two qualitative studies raised that they only obtained health service at a single health facility with no option to choose among health facilities at the time of service utilization, which negatively affected the renewal decision.46,49 This rule had been set as part of the capitation provider payment method under which members have to choose only one hospital and then they cannot switch to others.46

Discussion

In this review, we identified 27 studies reporting on a range of factors related to policy renewal of CBHI schemes from 12 LIMICs. The included studies used a purely qualitative approach, a quantitative approach, or a mixed-method approach. Our synthesis provided a conceptual framework of factors that are critical for CBHI policy renewal, and the evidence obtained from the included studies is discussed here based on the thematic synthesis.

The age of the household head is significantly related to policy renewal decisions with inconsistent results across the included studies. In some studies, older individuals were more likely to renew their membership as compared to the younger individuals, while in others a contrary finding is reported. It has been argued that as the head of the household becomes older, the risk of getting sick increases. Hence, they prefer to maintain their membership status to avoid money spent on future health expenditures.32,36 On the other hand, older people might have less capacity to pay for health insurance. As a result, they might prefer to leave the scheme. These different views suggest that the effect of the age of the household head on renewal decision requires further study.

The gender of the individual and household head is another significant determinant of policy renewal. Female-headed households were found to be more likely to renew their policy as compared to male-headed households. One exception is a finding from Ghana which reveals that male-headed households have higher odds of renewing membership. In support of the latter, a previous review reported that male-headed households are more likely to renew their policy. It also requires the attention of future researchers.17

Household size was another factor that affected the scheme renewal decision with a mixed effect. Some studies found that larger households were more likely to renew their policy than relatively smaller households, while others reported a contrary finding. Another systematic review found that household size was a facilitator of renewal.17 One study argued that the subscription fee in some schemes varies with family size, which means that having more family members means higher premiums,32 for which those unable to pay may prefer to drop out of the schemes. In other CBHI schemes, the premium does not rise with increased household size,28 hence facilitates renewal. Another argument is that having more family members means a higher level of dependence, which, in turn, requires more resources to support daily life,32,36 hence people prefer other stuff over subscription renewal.

This review showed that the socioeconomic standing of households is significantly associated with policy renewal decisions regardless of whether it is expressed in terms of income, expenditure, or asset category. Households with lower economic status were less likely to renew their policy compared to those with higher economic status and the finding is consistent among all the included studies. The importance of this factor is strengthened by other evidence from our synthesis that (perceived) inability to pay for scheme premium was one of the barriers to renewing membership. This is consistent with reports of previous reviews where those who view the insurance premium as high were less likely to renew their membership.17,18

This review identified education as playing a key role in renewal decisions and this finding was similar across all included studies that reported a statistically significant association. Those household heads or scheme members who attended more years of education were more likely to renew the scheme policy compared to the less educated counterparts. This is consistent with a previous systematic review and meta-analysis.18 In communities where literacy is low and access to information is scarce, people’s decisions not to renew their policy might be related to a low understanding of CBHI and its principles. Our synthesis showed that members’ understanding and knowledge towards scheme benefits and risk pooling principles positively influence the household’s decision to renew its policy. Respondents who have a good understanding of the scheme were more likely to renew their policy and pay the premium regularly. Apart from understanding, the individual’s or household’s attitude towards solidarity and their willingness to share the health-care cost of other scheme members is an inherent factor for policy renewal. This is in line with previous reviews in which members who did not understand the concept of risk pooling and the purpose of co-payment dropped out of the schemes.17,18 This implies the need to comprehensively and extensively disseminate information about the benefits that the scheme offers. In doing so, the source of information needs to consider the target community. Our review revealed that people are more likely to renew their policy if they get scheme related information from relatives, friends, or leaders whom they know. This indicates the positive effect of peer influence and the importance of creating a trusted source of information.

Active participation in the scheme like having informal discussions about the scheme; participation in awareness-raising and/or information dissemination; voting in scheme elections; attending a general assembly; and receiving training facilitates renewal decision. Social capital, which is proxied by participation in other voluntary groupings, was also an enabling factor for membership renewal. This is because having such experiences could improve the individual’s awareness and understanding regarding the scheme principles and its benefits.

The households’ long-term illness experience and the perception towards their health status also influence their decision to renew their policy. Respondents who perceived themselves or the household as healthy dropped out of the schemes, while households that have at least one family member who suffers from a chronic illness or disability prefer to renew their subscription. Those who have not fallen sick and not utilized health services feel that there are no benefits in paying membership. People with greater health-care needs (high-risk individuals) feel that they are at risk of greater health-care expenditure. Knowing this, they decide to renew their policy to avoid future health-care costs that could deteriorate the household’s resources and assets. This mainly points out the possible existence of adverse selection, which is a common phenomenon in schemes where membership is voluntary and premiums are independent of individual health risks.51

History of hospitalization under the scheme, which is an indicator of illness and utilization negatively influence policy renewal, with limited evidence. As argued by one study, the possible reasons could be the poor quality of health care and the negative claims experience faced by members.30 One of the main aims of UHC is to protect people from financial hardship. Hospitalized individuals are at risk of higher health-care expenditures that need to be protected by the designed CBHI schemes. Therefore, further research is needed on this important variable to strengthen the evidence of whether it hinders renewal or otherwise.

Being benefitted from the scheme through health-care utilization or claims reimbursement is also another important factor that influences the members’ decision to renew their policy. The use of health care under the scheme motivates individuals to renew their insurance policies. In addition to utilization, frequency of use, and amount of benefit claims received also influence renewal decisions. Individuals or households who visited health facilities more frequently and those who received more benefit claims were more likely to renew their membership. Similarly, the review conducted by Dror et al reported that receipt of benefit claims in the year prior to the renewal period encourages people to maintain their policy.17

From the health-care providers’ perspective, the perceived quality of health care and distance to the nearest health facility were important variables that influence renewal decisions. When members perceived that the quality of health care is optimum, they decide to maintain their policy. This review identified different dimensions of health-care quality as barriers or facilitators of renewal decisions. Obtaining prescribed medicines and diagnostic services, obtaining quick responses from health service providers, being favored by the health-care providers and positive behavior of service providers have been reported as facilitators of membership renewal. On the other hand, lack of prescribed medicines in the contracted health facilities, receiving poor quality medicines, illegal payment for medicines, misbehavior of health professionals and the differential treatment of the insured patients in favor of the uninsured patients, unclean hospital environment, long queues, lack of diagnostic equipment, and long waiting hours to obtain health care have been reported as the main reasons for dropping out of the schemes. This is strengthened by previous reviews that poor quality of health care is a widely reported reason to drop out of CBHI schemes. Long patient waiting time at the health facility, discrimination against scheme members,18 health-care providers’ lack of technical expertise, and providers’ negative behaviors17 have been pointed out by the reviews as important barriers for policy renewal.

Our review identified that traveling long distances to access health care is a barrier for renewal decisions. This is because most people could not afford the transportation fare when the health facility is far away from their place of residence even though they had a valid insurance card.46 One exception is the finding from Eastern Sudan, which reported a positive association between distances traveled to access health care and renewal decision.41 The authors argued that more distant households seem to appreciate the quality of health care provided under the scheme.

Factors related to scheme operation, including satisfaction level from the insurers; shorter waiting time at the scheme office; visit by agents during the renewal period;26 convenience in receiving card and time of premium collection; and trust in insurers were found to be important enablers of renewal decision. This is in line with previous reviews which indicated that convenience in the timing of premium collection and consumer satisfaction with services provided by the scheme positively influenced decisions to renew membership in a scheme.18 Individuals who place higher trust in scheme management renewed their policy as well.17,18

The exemption policy (targeted subsidization) had a significant role in the retention of members. Members having exempted individuals within the household like children below the age of 18 years, the elderly aged 70 years or older, pregnant women, indigent (core poor), were more likely to renew their membership. These are individuals who have higher health care needs compared to the other segment of the population, and subsidization for such groups could be a short-term solution to improve the equity goal of UHC. Members’ perception of the benefits package affects their policy renewal decision. Members who perceived that the insurance plan is providing good coverage of illnesses and health services were more likely to renew their policy. Issues related to the benefits package like the exclusion of some health risks, a limited number of medicines under the scheme, exclusion of referral service, and the exclusion of valued health services from the benefits package were reported as important barriers to membership renewal. In line with this, a previous systematic review reported that people’s dissatisfaction with the insurance benefits package was a major cause of low membership renewal.17

Policy Implication

Policymakers and relevant stakeholders working on the sustainability of CBHI schemes could be benefited from the findings of this synthesis by taking their country or scheme context into consideration. To maintain the sustainability of CBHI schemes, policymakers should balance the trade-offs between equity and efficiency. We identified evidence suggestive of the presence of adverse selection in CBHI schemes. The financial sustainability of the schemes could be hampered if the adverse selection is not fully taken into account. Therefore, it is essential to minimize certain adverse selection behaviors without compromising the equity goal of UHC. The unit of enrollment at the household level rather than at the individual level was found to be effective in reducing adverse selection in Burkina Faso.51 Retaining healthy members through awareness and information campaigns could also balance the negative effect of adverse selection. Peer learning programs with individuals whom they trust could be one awareness creation alternative to retain the members into the schemes. This should be coupled with the creation of opportunities for the active participation of community members to enhance scheme trust, sense of responsibility, and understanding of the scheme.

Our synthesis also found the existence of inequity, where the poor are systematically excluded from the schemes. Usually, CBHI schemes charge a flat premium, and only those who can afford the premiums decide to stay as scheme members. To close the existing inequity gaps, policymakers could consider cross-subsidization from the rich to the poor members, retaining healthy members, and provision of targeted premium subsidies. The latter has been effective in retaining members in Ghana, where exempted groups adhere to the scheme.37,38 However, as more groups are subsidized, the efficiency of the schemes could be diminished.

Lack of affordability might not be synonymous with a higher premium or low income but could also mean an inability to pay at the time of premiums collection, or preference to other expenditures essential for daily life over paying insurance premiums. It is important to adjust a convenient premium collection time depending on the area context.

Many health-care quality issues that are within the control of the health-care system can be adjusted to enhance renewals as well. Issues related to access to essential health services and medicines, health-care providers’ behavior, and geographical accessibility of health facilities should be well addressed given their central role in enhancing the members’ trust in health facilities and hence facilitate their renewal decision. It is important to take the necessary institutional and regulatory measures to steer health-care providers’ attitudes towards insured clients. Relevant stakeholders should also consider how the current payment methods of CBHI schemes and claims reimbursement practices influence the behaviors and performances of health care providers.

Limitations

This review could suffer from the following limitations. First, as the largest number of studies dealt with CBHI schemes was obtained from Sub-Saharan Africa countries and India, the conclusions might be less relevant to other contexts. Particularly, the studies conducted in two countries – Ghana and India – dominated the number of studies included in the review, where 15 out of 27 studies were conducted in these countries. Second, we may have missed potentially relevant studies that could be available in other electronic databases since we could not access beyond the ones searched for this review. Finally, we could not able to show the pooled effect of the variables on policy renewal through a meta-analysis due to the heterogeneity of the reviewed studies. Given the heterogeneity in study settings, population groups, and outcome measures, we fail to conduct meta-analyses. Particularly the studies use different outcome measures, making it difficult to identify a common effect size. Because of this, we synthesized the findings narratively.

Conclusions

This systematic review examined the evidence of barriers and facilitators for policy renewal of community-based health insurance schemes in LMICs, which are designed to achieve UHC. The evidence shows that certain factors affecting policy renewal emerged from the individual members or households, while others are driven by situations controlled by the health-care providers and the scheme governance.

Education, the gender of household heads (female), urban residence, and the socioeconomic status of households are all factors that positively affect policy renewal. Moreover, when individuals understand insurance principles and the functions of CBHI, they are more likely to renew their policy; active scheme participation increased retention. When people have a positive claims experience and benefited from the scheme through health-care utilization, they are more likely to renew their policy. The existence of chronic conditions in the family enhances the likelihood of renewal; the perception that health care is of good quality and being located nearer to the health facilities act as a factor enhancing policy renewal. Scheme related factors, including convenience in time of premium collection, short waiting time to obtain scheme services, satisfaction with scheme services, and trust in the scheme management all facilitate contract renewal. Social exclusion (inequity), lack of benefit from the CBHI scheme, poor quality of care, and lack of trust in insurers are the major deterrent factors of membership renewal.

Abbreviations

CBHI, community-based health insurance; LMICs, low and middle-income countries; UHC, universal health coverage.

Disclosure

The authors reported no conflicts of interest in this work.

References

1. McIntyre D, Obse AG, Barasa EW, Ataguba JE. Challenges in financing universal health coverage in sub-Saharan Africa. 2018.

2. Dieleman JL, Templin T, Sadat N, et al. National spending on health by source for 184 countries between 2013 and 2040. Lancet. 2016;387(10037):2521–2535. doi:10.1016/S0140-6736(16)30167-2

3. Dieleman JL, Sadat N, Chang AY, et al. Trends in future health financing and coverage: future health spending and universal health coverage in 188 countries, 2016–40. Lancet. 2018;391(10132):1783–1798. doi:10.1016/S0140-6736(18)30697-4

4. World Health Organization. The world health report: health systems financing - the path to universal coverage. World Health Organization; 2010.

5. Wagstaff A, Flores G, Hsu J, et al. Progress on catastrophic health spending in 133 countries: a retrospective observational study. Lancet. 2018;6(2):e169–e179. doi:10.1016/S2214-109X(17)30429-1

6. World Health Organization, The World Bank. Tracking universal health coverage: 2017 global monitoring report. World Health Organization and International Bank for Reconstruction and Development/The World Bank; 2017.

7. Waelkens M-P, Soors W, Criel B. Community health insurance in low- and middle-income countries. Elsevier. 2017;2:82–92.

8. Kruk ME, Gage AD, Arsenault C, et al. High-quality health systems in the sustainable development goals era: time for a revolution. Lancet. 2018;6(11):e1196–e1252.

9. Umeh CA. Challenges toward achieving universal health coverage in Ghana, Kenya, Nigeria, and Tanzania. Int J Health Plann Manage. 2018;33(4):794–805. doi:10.1002/hpm.2610

10. Chu A, Kwon S, Cowley P. Health financing reforms for moving towards universal health coverage in the western pacific region. Health Syst Reform. 2019;5(1):32–47. doi:10.1080/23288604.2018.1544029

11. Wagstaff A, Cotlear D, Eozenou PH-V, Buisman LR. Measuring progress towards universal health coverage: with an application to 24 developing countries. Oxf Rev Econ Policy. 2016;32(1):147–189. doi:10.1093/oxrep/grv019

12. De Allegri M, Sauerborn R, Kouyate B, Flessa S. Community health insurance in sub-Saharan Africa: what operational difficulties hamper its successful development? Trop Med Int Health. 2009;14(5):586–596. doi:10.1111/j.1365-3156.2009.02262.x

13. International Labour Organization. Health Microinsurance Schemes: Monitoring and Evaluation Guide. Geneva: International Labour Organization; 2007.

14. Wipf J, Garand D. Performance Indicators for Microinsurance: A Handbook for Microinsurance Practitioners.

15. Bhageerathy R, Nair S, Bhaskaran U. A systematic review of community-based health insurance programs in South Asia. Int J Health Plann Manage. 2017;32(2):e218–e231. doi:10.1002/hpm.2371

16. Adebayo EF, Uthman OA, Wiysonge CS, Stern EA, Lamont K, Ataguba JE. A systematic review of factors that affect uptake of community-based health insurance in low-income and middle-income countries. BMC Health Serv Res. 2015;15(543):543. doi:10.1186/s12913-015-1179-3

17. Dror DM, Hossain SAS, Majumdar A, Koehlmoos TLP, John D, Panda PK. What factors affect voluntary uptake of community-based health insurance schemes in low- and middle-income countries? A systematic review and meta-analysis. PLoS One. 2016;11(8):e0160479. doi:10.1371/journal.pone.0160479

18. Fadlallah R, El-Jardali F, Hemadi N, et al. Barriers and facilitators to implementation, uptake and sustainability of community-based health insurance schemes in low- and middle-income countries: a systematic review. Int J Equity Health. 2018;17(1):13. doi:10.1186/s12939-018-0721-4

19. Moher D, Liberati A, Tetzlaff J, Altman DG. Preferred reporting items for systematic reviews and meta-analyses: the PRISMA statement. PLoS Med. 2009;6(7):e1000097. doi:10.1371/journal.pmed.1000097

20. Munn Z, Moola S, Riitano D, Lisy K. The development of a critical appraisal tool for use in systematic reviews addressing questions of prevalence. Int J Health Policy Manag. 2014;3(3):123–128. doi:10.15171/ijhpm.2014.71

21. Hong QN, Pluye P, Fàbregues S, et al. Mixed Methods Appraisal Tool (MMAT) Version 2018. Canada: McGill University; 2018.

22. Davids EL, Roman NV. A systematic review of the relationship between parenting styles and children’s physical activity. Afr J Phys Health Edu Recreat Dance. 2014;2(1):228–246.

23. Gough D, Oliver S, Thomas J. An Introduction to Systematic Reviews. Sage; 2012.

24. Ozawa S, Walker DG. Trust in the context of community-based health insurance schemes in Cambodia: villagers’ trust in health insurers. Adv Health Econ Health Serv Res. 2009;21:107–132.

25. Savitha B. Why members dropout? An evaluation of factors affecting renewal in micro health insurance. J Health Manag. 2017;19(2):292–303. doi:10.1177/0972063417699691

26. Bhat R, Jain N. A study of factors affecting the renewal of health insurance policy [Working paper]. Ahmedabad:Indian Institute of Management; 2007.

27. Sinha T, Ranson MK, Patel F, Mills A. Why have the members gone? Explanations for dropout from a community-based insurance scheme. J Int Dev. 2007;19(5):653–665. doi:10.1002/jid.1346

28. Raza W, Poel E, Panda P. Analyses of enrolment, dropout and effectiveness of RSBY in northern rural India [Working paper]. Munich Personal RePEc Archive, Erasmus University Rotterdam; 2016.

29. Panda P, Chakraborty A, Raza W, Bedi AS. Renewing membership in three community-based health insurance schemes in rural India. Health Policy Plan. 2016b;31(10):1433–1444. doi:10.1093/heapol/czw090

30. Panda P, Chakraborty A, Raza W, Bedi AS. Renewing membership in three community-based health insurance schemes in rural India. Health Policy Plan. 2016a;31(10):1433–1444.

31. Iqbala M, Chowdhury AH, Mahmooda SS, Mia MN, Hanifia SMA, Bhuiya A. Socioeconomic and programmatic determinants of renewal of membership in a voluntary micro health insurance scheme: evidence from Chakaria, Bangladesh. Glob Health Action. 2017;10(1):1287398. doi:10.1080/16549716.2017.1287398

32. Dartanto T, Halimatussadiah A, Rezki JF, et al. Why do informal sector workers not pay the premium regularly? Evidence from the National Health Insurance System in Indonesia. Appl Health Econ Health Policy. 2020;18:81–96.

33. Dong H, Allegri MD, Gnawali D, Souares A, Sauerborn R. Drop-out analysis of community-based health insurance membership at Nouna, Burkina Faso. Health Policy (New York). 2009;92(2–3):174–179. doi:10.1016/j.healthpol.2009.03.013

34. Nshakira-Rukundo E, Mussa EC, Nshakira N, Gerber N, Braun J. Determinants of enrolment and renewing of community based health insurance in households with under-5 children in rural south-western Uganda. Int J Health Policy Manag. 2019;8(10):593–606. doi:10.15171/ijhpm.2019.49

35. Boateng D, Awunyor-Vitor D. Health insurance in Ghana: evaluation of policy holders’ perceptions and factors influencing policy renewal in the Volta region. Int J Equity Health. 2013;12:1–10. doi:10.1186/1475-9276-12-50

36. Boateng S, Amoako P, Poku AA, Baabereyir A, Gyasi RM. Migrant female head porters’ enrolment in and utilisation and renewal of the National Health Insurance Scheme in Kumasi, Ghana. J Public Health. 2017;25:625–634. doi:10.1007/s10389-017-0832-1

37. Nsiah-Boateng E, Nonvignon J, Aryeetey GC, et al. Sociodemographic determinants of health insurance enrolment and dropout in urban district of Ghana: a cross-sectional study. Health Econ Rev. 2019;9(1):1–9. doi:10.1186/s13561-019-0241-y

38. Duku SKO, Asenso-Boadi F, Nketiah-Amponsah E, Arhinful DK. Utilization of healthcare services and renewal of health insurance membership: evidence of adverse selection in Ghana. Health Econ Rev. 2016;6(1):43. doi:10.1186/s13561-016-0122-6

39. Atinga RA, Abiiro GA, Kuganab-Lem RB. Factors influencing the decision to drop out of health insurance enrolment among urban slum dwellers in Ghana. Trop Med Int Health. 2015;20(3):312–321. doi:10.1111/tmi.12433

40. Mladovsky P. Why do people drop out of community-based health insurance? Findings from an exploratory household survey in Senegal. Soc Sci Med. 2014;107:78–88. doi:10.1016/j.socscimed.2014.02.008

41. Herberholz C, Fakihammed WA. Determinants of voluntary national health insurance drop-out in Eastern Sudan. Appl Health Econ Health Policy. 2016;15(2):215–226. doi:10.1007/s40258-016-0281-y

42. Adu KO. National health insurance scheme renewal in Ghana: does waiting time at health insurance registration office matter? [Working paper]. Munich Personal RePEc Archive, University of Professional Studies Accra; 2019.

43. Mebratie AD, Sparrow R, Yilma Z, Alemu G, Bedi AS. Dropping out of Ethiopia’s community-based health insurance scheme. Health Policy Plan. 2015;30(10):1296–1306. doi:10.1093/heapol/czu142

44. Atnafu AA Community-based health insurance in Ethiopia: enrollment, membership renewal, and effects on health service utilization [Working paper], Seoul National University; 2018.

45. Andoh-Adjei FX, van der Wal R, Nsiah-Boateng E, Asante FA, van der Velden,K, Spaan E. Does a provider payment method affect membership retention in a health insurance scheme? A mixed method study of Ghana’s capitation payment for primary care. BMC Health Serv Res. 2018;18(1):1–11. doi:10.1186/s12913-018-2859-6

46. Fenny AP, Kusi A, Arhinful DK, Asante FA. Factors contributing to low uptake and renewal of health insurance: a qualitative study in Ghana. Glob Health Res Policy. 2016;1:1–10. doi:10.1186/s41256-016-0018-3

47. Kotoh AM, Aryeetey GC, Geest S. Factors that influence enrolment and retention in Ghana’ National Health Insurance Scheme. Int J Health Policy Manag. 2017;7(5):443–454. doi:10.15171/ijhpm.2017.117

48. Turcotte-Tremblay AM, Haddad S, Yacoubou I, Fournier P. Mapping of initiatives to increase membership in mutual health organizations in Benin. Int J Equity Health. 2012;11(1):1–15. doi:10.1186/1475-9276-11-74

49. Macha J, Kuwawenaruwa A, Makawia S, Mtei G, Borghi J. Determinants of community health fund membership in Tanzania: a mixed methods analysis. BMC Health Serv Res. 2014;14(1). doi:10.1186/s12913-014-0538-9

50. Basaza R, Criel B, Stuyft P. Community health insurance in Uganda: why does enrolment remain low? A view from beneath. Health Policy. 2008;87(2):172–184. doi:10.1016/j.healthpol.2007.12.008

51. Parmar D, Souares A, Allegri M, Savadogo G, Sauerborn R. Adverse selection in a community-based health insurance scheme in rural Africa: implications for introducing targeted subsidies. BMC Health Serv Res. 2012;12(1):1–8. doi:10.1186/1472-6963-12-181

© 2021 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2021 The Author(s). This work is published and licensed by Dove Medical Press Limited. The full terms of this license are available at https://www.dovepress.com/terms.php and incorporate the Creative Commons Attribution - Non Commercial (unported, v3.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted without any further permission from Dove Medical Press Limited, provided the work is properly attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.